- Semiconductor Materials & Components

- Flat Panel Antenna Market

Flat Panel Antenna Market Size, Share, and Growth Forecast 2026 - 2033

Flat Panel Antenna Market by Antenna Type (Electronically Steered, Mechanically Steered), Frequency Band (L & S Band, C & X Band, Ku Band, Ka Band), Industry (Aviation, Maritime, Military, Telecommunication, Defense & Government, Industrial, Commercial, Others), and Regional Analysis, 2026 - 2033

Flat Panel Antenna Market Size and Trend Analysis

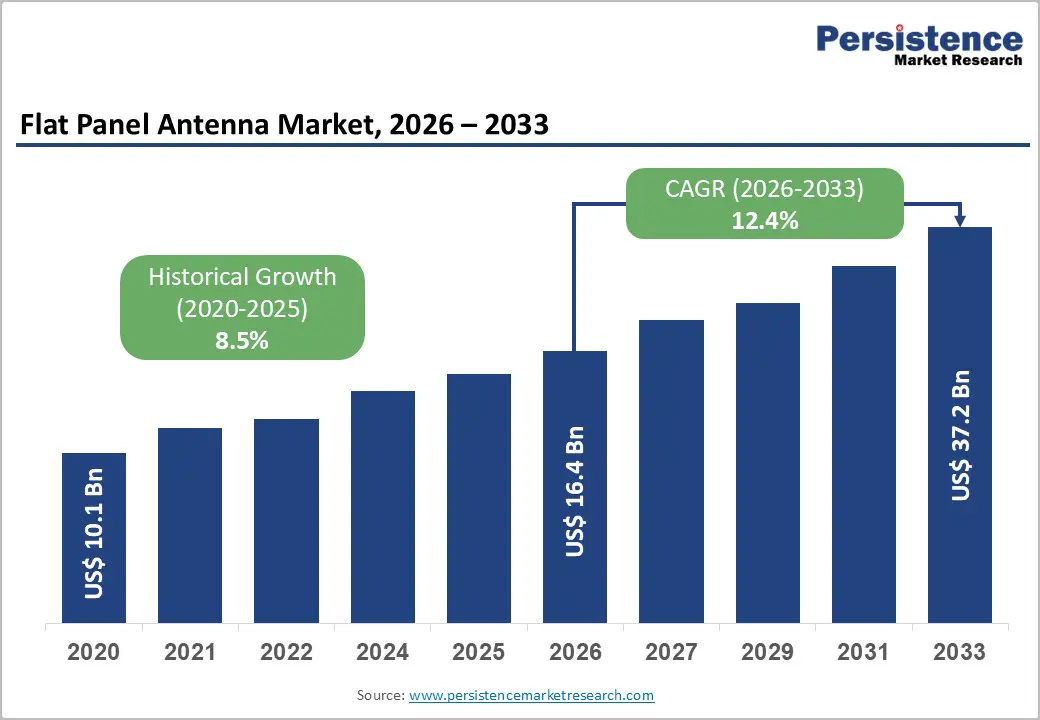

The global flat panel antenna market is expected to be valued at US$ 16.4 billion in 2026 and is projected to reach US$ 37.2 billion by 2033, growing at a CAGR of 12.4% between 2026 and 2033, driven by converging demand across commercial aviation, defence modernization, and low Earth orbit (LEO) satellite network expansion.

The proliferation of LEO constellations such as Starlink (SpaceX), OneWeb (OneWeb), and Project Kuiper (Amazon), coupled with advancements in multi-band satellite communications, is further strengthening adoption. Regulatory frameworks established by agencies such as the FCC and ITU are facilitating spectrum access and accelerating commercialization timelines across key geographies.

Key Industry Highlights:

- Leading Antenna Type: Electronically Steered Antennas dominate with 67.0% share in 2026, valued at over US$ 10.99 billion, driven by their ability to enable real-time beam steering, seamless LEO satellite tracking, and multi-orbit connectivity without mechanical movement.

- Leading Frequency Band: Ku Band leads the market with 40% share in 2026, valued at over US$ 6.56 billion, supported by its large installed base in GEO satellite infrastructure and widespread use across maritime, aviation, and enterprise VSAT networks.

- Fastest Growing Frequency Band: Ka Band is the fastest-growing, driven by high-throughput satellite demand, LEO constellation integration, and superior bandwidth efficiency for next-generation broadband services.

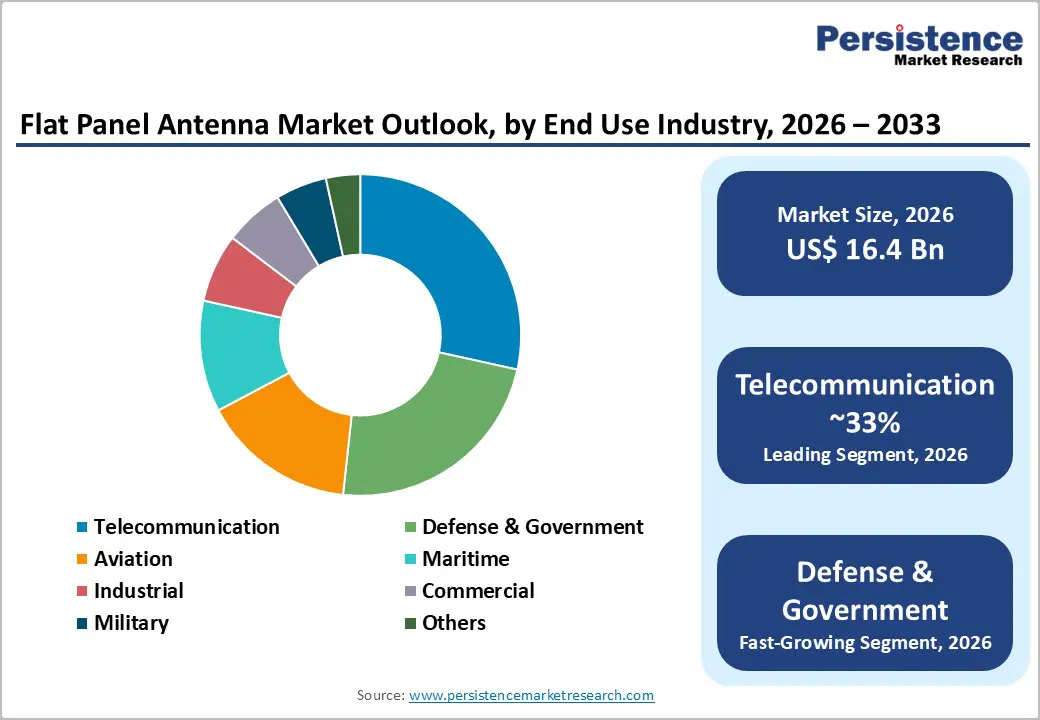

- Leading End-Use Industry: Telecommunication is the largest end-use segment with 33.0% share in 2026, valued at over US$ 5.41 billion, driven by rising demand for satellite-based broadband in rural, remote, maritime, and enterprise environments.

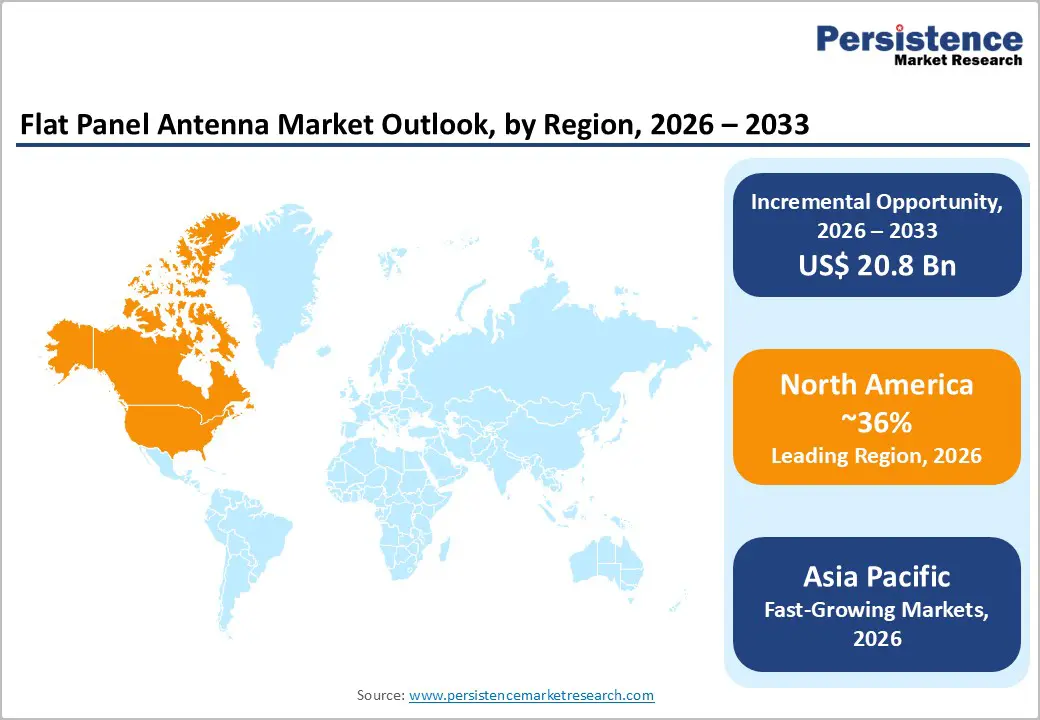

- Leading Region: North America leads with 36.0% share in 2026, valued at over US$ 5.90 Billion, driven by strong LEO operator presence, advanced defence SATCOM modernization, and large-scale broadband infrastructure initiatives.

- Fastest Growing Region: Asia Pacific is the fastest-growing market with a CAGR of 17.5%, fueled by rapid satellite programme expansion in China, India, and Japan, alongside increasing maritime connectivity and rural broadband penetration demand.

Market Dynamics

Drivers - Rapid Proliferation of LEO Satellite Constellations Creates Structural Demand for Advanced Flat Panel Antennas

LEO satellite constellations, which require ground-based user terminals capable of dynamically tracking fast-moving satellites across low orbital altitudes, are driving demand for the flat panel antenna market. Electronically steered flat panel antennas are uniquely suited to this requirement because they deliver beam steering without mechanical movement, enabling seamless satellite handoffs at speeds exceeding 27,000 kilometres per hour.

Operators such as SpaceX (Starlink), Eutelsat OneWeb, and Amazon are collectively deploying large-scale LEO constellations numbering in the tens of thousands of satellites, creating sustained long-term demand for compatible user terminals. This structural shift is transforming the market from a project-based procurement cycle into a multi-year platform-driven growth cycle across consumer, enterprise, aviation, maritime, and government connectivity applications.

Accelerating Defence Modernisation and Tactical Communications Upgrades Across NATO and Indo-Pacific Alliances

Defence and government agencies worldwide are actively upgrading legacy parabolic antenna systems with low-profile, electronically steered flat panel solutions to support enhanced situational awareness, secure SATCOM links, and platform integration on unmanned aerial vehicles (UAVs), naval vessels, and armoured ground platforms.

NATO member states collectively committed to increasing defence spending, with a significant proportion directed at communications, intelligence, and surveillance modernisation programmes through 2030. The U.S. Department of Defense (DoD) has specifically identified phased array antenna technology as a critical capability enabler under its Advanced Battle Management System (ABMS) initiative, injecting sustained procurement demand into the flat panel antenna sector.

Restraints - High Unit Costs and Complex Manufacturing Processes Constrain Mass-Market Adoption Timelines

The elevated per-unit cost of electronically steered phased array antennas relative to conventional dish or mechanically steered alternatives, driven by the complexity of fabricating thousands of radiating elements with precise phase control circuitry at scale, is limiting the adoption. Advanced antenna-on-chip (AoC) and antenna-in-package (AiP) manufacturing processes require specialised semiconductor fabrication capabilities that only a small number of global foundries currently possess, restricting supply-side flexibility. This cost barrier is particularly acute in price-sensitive maritime and rural broadband segments, where potential customers cannot yet justify a terminal cost premium that industry data suggests remains 2-4 times higher than legacy alternatives.

Spectrum Regulatory Fragmentation Across Jurisdictions Creates Market Entry and Deployment Barriers

The flat panel antenna industry faces a structurally complex regulatory environment in which spectrum access rules, power flux density limits, and terminal approval frameworks vary significantly across national jurisdictions, adding cost and timeline friction for vendors seeking global commercial deployment.

Operators targeting multi-region deployments must navigate separate approval processes with bodies including the FCC in the United States, Ofcom in the United Kingdom, and the European Union Agency for the Space Programme (EUSPA), each with distinct technical standards and certification timelines that extend go-to-market windows by 12-24 months. This fragmentation disproportionately disadvantages smaller and mid-tier vendors who lack the regulatory affairs resources to manage simultaneous multi-jurisdictional certification programmes.

Opportunities - Defence Sector Demand for Conformal and Vehicle-Integrated Antenna Solutions

The expanding requirement for conformal flat panel antennas, those designed to integrate flush with aircraft fuselages, naval hull structures, and armoured vehicle surfaces without aerodynamic or signature penalties, creates a structurally attractive, high-margin opportunity. Programmes such as the U.S. Army's Integrated Tactical Network (ITN) and NATO's Federated Mission Networking (FMN) initiative are generating active procurement demand for low-profile, broadband-capable antenna systems that maintain connectivity during high-mobility operations.

Vendors with demonstrated experience in military qualification, conformal phased array design, and electronically steered antenna systems should actively engage these programmes through direct government contracting channels and prime contractor teaming arrangements.

LEO-Enabled Consumer & Enterprise Flat Panel Terminal Market Expansion

The convergence of rapidly expanding LEO satellite constellations and declining launch costs is creating a significant growth opportunity for flat panel antenna manufacturers, particularly in underserved and unserved broadband markets such as rural regions, maritime operations, and airborne connectivity. With an estimated 2.2 billion people still lacking reliable internet access globally, demand for low-cost, high-performance user terminals is expected to rise as LEO coverage scales.

Vendors that successfully reduce terminal costs toward the sub-US$300 range through advanced ASIC-based beamforming integration are likely to secure a strong competitive advantage in the emerging high-volume adoption phase.

Forming early strategic partnerships with LEO constellation operators through certified or preferred terminal programs will be critical for achieving scalable market access. As operator ecosystems continue to mature and standardize, the window for early positioning is becoming increasingly time-sensitive, making near-term engagement a key strategic priority for market participants.

Category-wise Analysis

Antenna Type Insights

Electronically Steered segment accounts for 67.0% of the global flat panel antenna market in 2026, reaching over to US$ 10.99 billion value, driven by their solid-state, no-moving-parts architecture that enables rapid electronic beam steering essential for LEO and MEO satellite tracking. These systems support low-latency beam handover and continuous satellite tracking requirements that are critical in dense low-earth orbit constellations, where terminals must dynamically switch between satellites in near real time. ESAs are the only commercially scalable solution capable of meeting the speed, reliability, and form-factor constraints required for modern high-throughput satellite connectivity networks.

Mechanically steered is likely to experience a significant growth, due to cost sensitivity in maritime, fixed broadband, and selected enterprise applications where affordability outweighs advanced beam agility requirements. Improvements in motor control systems and hybrid architecture have enhanced operational reliability, but do not fully bridge the performance gap with electronically steered solutions.

While electronically steered antennas remain the dominant technology in LEO constellation-driven applications due to their superior beam agility and multi-satellite tracking capabilities, mechanically steered systems are expanding the total addressable market by enabling adoption among price-sensitive users previously excluded from flat panel antenna solutions.

Frequency Band Insights

Ku Band segment is expected to account for approximately 40% of the share in 2026, reaching over US$ 6.56 billion value, due to the large installed base of geostationary (GEO) satellites and mature VSAT ecosystems across maritime, aviation, and enterprise connectivity markets. It benefits from decades of infrastructure development by operators such as SES, Intelsat, and Eutelsat, which have created a stable and deeply embedded global user base.

It continues to represent the majority share of legacy VSAT deployments, although its share in new installations is gradually moderating. Despite increasing competition from Ka Band, Ku remains essential due to widespread ground equipment compatibility and long replacement cycles in satellite terminals.

Ka Band is the fast-growing frequency band, driven by its ability to support higher bandwidth efficiency and high-throughput satellite (HTS) architectures. It enables significantly higher data capacity compared to lower frequency bands by utilizing wider bandwidth allocations and advanced frequency reuse techniques. It is also central to next-generation LEO satellite constellations, including Starlink and Amazon Kuiper, where it is widely used in gateway and user link architectures, often alongside Ku Band in hybrid systems. Growth is further supported by declining terminal costs and increasing demand for high-speed broadband connectivity in underserved and mobile applications.

Industry Insights

Telecommunication is the largest end-use industry, accounting for approximately 33.0% share, equivalent to around US$ 5.41 billion. This is driven by strong demand for satellite-enabled broadband connectivity, particularly in rural, remote, maritime, and enterprise environments where terrestrial fiber or cellular networks are economically limited or unavailable. Flat panel antennas are primarily deployed as user terminal devices supporting LEO satellite broadband services, enabling high-speed connectivity for fixed and portable applications. Global fixed broadband demand continues to grow steadily at around mid-single-digit rates annually, and satellite-based broadband is expanding significantly faster due to increasing LEO constellation coverage and declining launch costs.

The defense & government segment are likely to experience fast-growth driven by sustained investments in military satellite communications modernization and secure, resilient connectivity systems. Increasing geopolitical tensions and defense digitalization programs are accelerating the adoption of electronically steered flat panel antennas across land, naval, airborne, and unmanned platforms. These antennas are particularly critical in applications where size, weight, and power (SWaP) constraints make traditional mechanically steered systems impractical. Rising use of UAVs, tactical communication networks, and mobile command systems is further strengthening demand.

Regional Insights

North America Flat Panel Antenna Market Trends and Insights

North America accounts for 36.0% of the global flat panel antenna market in 2026, representing US$ 5.90 billion, driven by a concentrated ecosystem of LEO satellite operators, advanced defence SATCOM modernization programmes, and a mature enterprise VSAT installed base that supports sustained replacement and upgrade demand. Expanding aviation in-flight connectivity deployments across commercial fleets and rural broadband expansion initiatives enabled through federal infrastructure funding programmes, which are increasing terminal penetration in underserved geographies.

The United States flat panel antenna market represents 80.0% of the North America regional market in 2026, reaching over US$ 4.7 Billion, due to large-scale LEO constellation operators such as SpaceX, alongside emerging demand from Amazon’s Project Kuiper and sustained SATCOM services from Viasat. The U.S. Department of Defense continues to invest heavily in advanced electronically steered SATCOM and phased-array communication systems, reinforcing defense-grade demand. Federal broadband expansion initiatives such as the BEAD Programme are expected to indirectly expand rural connectivity requirements, further supporting long-term terminal adoption across underserved regions.

Europe Flat Panel Antenna Market Trends and Insights

Europe accounts for 27.0% of the market share in 2026, exceeding a value of over US$ 4.43 Billion. The region’s demand is driven by strong adoption in commercial aviation connectivity upgrades, maritime broadband deployment across major shipping corridors, and increasing defense SATCOM investments by NATO member states following heightened geopolitical tensions after 2022. EU initiatives such as the IRIS are expected to strengthen long-term demand for advanced satellite communication terminals across government and institutional users, with secondary spillover into commercial applications.

The Germany Flat Panel Antenna market represents 22.0% of the European market in 2026, equivalent to US$ 0.97 Billion, driven by the country's position as Europe's largest economy, its advanced industrial manufacturing base, and its status as a leading NATO defence spender targeting the alliance's 2% GDP benchmark. Strong demand from Germany's automotive and industrial IoT sectors, which are increasingly integrating satellite connectivity into connected vehicle and smart factory infrastructure, adds a commercially diverse demand dimension beyond traditional aviation and maritime verticals.

The United Kingdom Flat Panel Antenna market is expected to cross over US$ 0.89 Billion value by 2026, anchored by the country's strong maritime heritage, its significant defence technology industrial base. The UK Space Agency's National Space Strategy, which committed over £1.8 Billion in public and private space investment, is channeling development resources toward ground segment technologies, including flat panel antenna terminal innovation.

France Flat Panel Antenna market is expected to cross over US$ 750 million value by 2026, supported by France's position as one of Europe's leading defence technology exporters and its substantial commercial aviation sector centered on Airbus and the broader aerospace supply chain based in and around Toulouse.

Asia Pacific Flat Panel Antenna Market Trends and Insights

Asia Pacific accounts for more than 25.0% of the global flat panel antenna market in 2026, representing US$ 4.10 billion, and is the fastest growing regional market in the flat panel antenna industry, expanding at a projected CAGR of 17.5% through 2033. The region's structural acceleration reflects a powerful combination of government-backed satellite broadband connectivity programmes targeting rural and island populations across Southeast Asia and South Asia, rapid maritime trade growth demanding vessel connectivity upgrades, and aggressive national space programme investments by China, India, and Japan.

The China Flat Panel Antenna market is expected to account for over 35.0% of the Asia Pacific regional market in 2026, reaching over to US$ 1.44 billion, driven by state-directed investment in domestic satellite constellation programmes, including Guowang (GW), a planned 13,000-satellite LEO constellation, alongside rapidly expanding demand for maritime and aviation connectivity across China's Belt and Road-connected trade routes.

Japan Flat Panel Antenna market accounts for over US$ 660 million in 2026, underpinned by the country's world-leading consumer electronics manufacturing capabilities, its technologically sophisticated defence establishment, and strong maritime sector demand across one of the world's most active coastal shipping economies. Japan's Ministry of Defence has committed to doubling defence expenditure toward 2% of GDP by 2027, with SATCOM modernisation and joint operations connectivity identified as priority capability investment areas.

India Flat Panel Antenna market accounts for over US$ 530 million in 2026, as the government's liberalisation of satellite broadband licensing including approvals for operators such as Starlink and OneWeb expands the commercial terminal addressable market to a potential user base. India's ambitious space sector reform agenda, managed through the Indian National Space Promotion and Authorisation Centre (IN-SPACe), is stimulating domestic antenna manufacturing investment and attracting international joint ventures targeting the country's vast unserved rural connectivity market.

Competitive Landscape

The global flat panel antenna market exhibits a moderately fragmented competitive structure, characterised by a small number of well-capitalised technology leaders competing based on electronically steered phased array innovation and constellation operator partnerships, alongside a broader tier of specialised vendors through differentiated form factors and qualification credentials.

Companies are focusing on technological differentiation, specifically, beamforming chipset performance, terminal size, weight, and power (SWaP) optimization, and multi-orbit compatibility, reflecting the market's current growth phase where technical capability commands premium positioning. Leading players are actively pursuing vertical integration strategies, acquiring RF semiconductors and beamforming IP assets to reduce supply chain dependency and accelerate development cycles.

Key Developments:

- March 2025: Kymeta launched its Goshawk u8, a next-generation electronically steered flat panel satellite antenna designed for defense and government applications. The solution supports multi-orbit connectivity to enhance resilient, on-the-move communications for European and allied forces amid rising security pressures.

- March 2025: Intellian completed its enterprise flat panel antenna series, with the terminals now going live on the Eutelsat OneWeb LEO satellite network. The solution enables high-performance, electronically steered connectivity for enterprise users across mobility, maritime, and fixed applications.

Flat Panel Antenna Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 10.1 Billion |

| Current Market Value (2026) | US$ 16.4 Billion |

| Projected Market Value (2033) | US$ 37.2 Billion |

| CAGR (2026 - 2033) | 12.4% |

| Leading Region | North America, 36.0% Share |

| Dominant Antenna Type | Electronically Steered, 67.0% Share |

| Top-ranking Frequency Band | Ku Band, 40.0% Share |

| Incremental Opportunity (2026 - 2033) | US$ 20.8 Billion |

Companies Covered in Flat Panel Antenna Market

- Kymeta Corporation

- ThinKom Solutions

- L3Harris Technologies

- Cobham SATCOM

- Viasat

- Intellian Technologies

- All.Space (Isotropic Systems)

- Hanwha Phasor

- Ball Aerospace

- Gilat Satellite Networks

- ST Engineering

- China Starwin

- ALCAN Systems

- C-COM Satellites

- Others

Frequently Asked Questions

The Flat Panel Antenna market is valued at US$ 16.40 Billion in 2026 and is projected to reach US$ 37.17 Billion by 2033, growing at a CAGR of 12.4%. The strong growth is driven mainly by expanding LEO satellite networks requiring large-scale compatible user terminals.

The rapid deployment of LEO satellite constellations is creating large-scale demand for electronically steered terminals. Rising defence SATCOM modernization and secure connectivity needs are accelerating adoption across military applications.

The Electronically Steered segment dominates with 67.0% share in 2026, due to its ability to track fast-moving LEO satellites in real time. Its performance advantage makes it the essential technology for next-generation satellite broadband connectivity.

North America leads with a 36.0% market share in 2026, supported by strong presence of LEO operators and heavy U.S. defence SATCOM investments. Government broadband funding and advanced space infrastructure further reinforce its dominance.

Key opportunities lie in developing low-cost terminals (below US$ 300) to enable mass adoption in consumer and enterprise broadband markets. Early partnerships with LEO operators and government-backed programmes also present strong growth potential.

The leading companies in the Flat Panel Antenna market include Kymeta Corporation, Viasat, ThinKom Solutions, L3Harris Technologies, Cobham SATCOM, Intellian Technologies, All.Space and Hanwha Phasor.