Industry: Healthcare

Published Date: July-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 156

Report ID: PMRREP34695

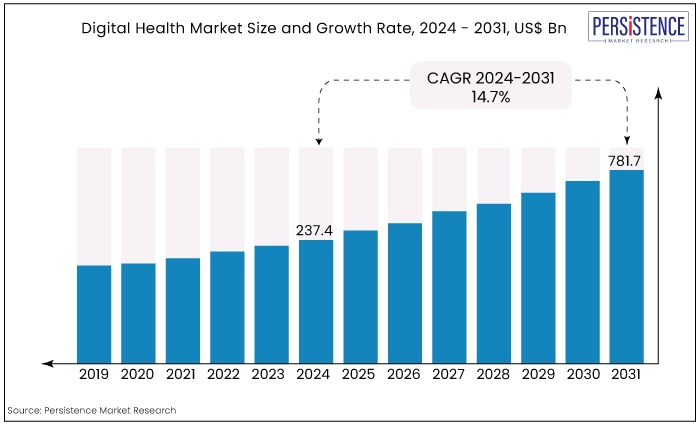

The global digital health market is estimated to value at US$781.7 Bn by the end of 2031 from US$202.9 Bn recorded in 2023. The market is expected to secure a CAGR of 18.6% in the forthcoming years from 2024 to 2031.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Digital Health Market Size (2024E) |

US$237.4 Bn |

|

Projected Market Value (2031F) |

US$781.7 Bn |

|

Forecast Growth Rate (CAGR 2024 to 2031) |

14.7% |

|

Historical Growth Rate (CAGR 2018 to 2023) |

18.6% |

Digital health refers to the integration of technology into healservices to enhance efficiency, accessibility, and patient outcomes. It encompasses a broad spectrum of innovations, including telemedicine, wearable devices, health apps, and AI-driven diagnostics.

By leveraging digital tools, healthcare providers remotely monitor patients, streamline administrative tasks, and personalize treatment plans. This transformative approach not only empowers individuals to actively manage their health but also enables healthcare systems to deliver more timely and cost-effective care.

As the digital health market continues to evolve, it promises to revolutionize the healthcare landscape by improving access to medical expertise and promoting proactive health management globally.

The industry is witnessing transformative market trends and innovations that are reshaping healthcare delivery. Artificial intelligence (AI), and machine learning (ML) are being integrated for predictive analytics and personalized patient care, enhancing diagnostic accuracy and treatment outcomes.

Virtual reality (VR), and augmented reality (AR) technologies are revolutionizing medical training and patient engagement, particularly in mental health and surgical fields. Mobile health (mHealth) apps and wearable devices are expanding remote monitoring capabilities, empowering patients to manage their health actively.

The field of digital health has experienced significant growth driven by rapid technological advancements and increasing demand for accessible healthcare solutions. From the initial stages of telemedicine to today's sophisticated AI-driven diagnostics and wearable devices, digital health has transformed how healthcare is delivered and managed.

Looking forward, the trajectory of digital health continues to advance with innovations such as personalized medicine through data analytics, AI for diagnostics, and wearable technologies for remote monitoring. These technologies aim to empower individuals in managing their health proactively and facilitate more efficient healthcare delivery.

The future holds promise for further integration of technologies like blockchain for secure health data management and virtual reality for enhanced medical training and patient education.

Integration of AI, ML, and IoT for Enhanced Diagnostic Capabilities, and Remote Monitoring

Technological advancements in telehealth, including the integration of AI, ML, and Internet of Things (IoT), are revolutionizing healthcare by enhancing diagnostic accuracy and remote monitoring capabilities.

AI and ML algorithms analyse extensive patient data to offer insights for early disease detection and personalized treatment planning, aiding healthcare providers in making informed decisions.

IoT devices such as wearable sensors provide real-time health data from patients outside clinical settings, enabling proactive healthcare management and improving chronic disease monitoring.

These innovations support more efficient, personalized care delivery, aiming to enhance healthcare quality and patient outcomes through advanced digital health solutions.

Rising Acceptance and Integration of Telehealth Platform

Healthcare provider adoption of telehealth platforms is driven by the desire to expand service capabilities and improve patient access to care. Telehealth allows providers to offer virtual consultations, remote monitoring, and telemedicine services, reaching patients in rural or underserved areas where access to healthcare may be limited.

Integration of telehealth enhances practice efficiency by reducing wait times, optimizing scheduling, and streamlining administrative tasks. Moreover, telehealth enables healthcare professionals to collaborate more effectively across specialties and geographic locations, facilitating quicker consultations and second opinions.

The COVID-19 pandemic accelerated provider adoption as a necessity to maintain care continuity while minimizing infection risks.

Moving forward, healthcare providers are increasingly leveraging telehealth to deliver patient-centered care, improve patient outcomes, and meet the evolving demands of modern healthcare delivery.

Regulatory Challenges

Regulatory challenges pose significant restraints to the digital health market's growth and innovation. The complexity arises from varying regulatory frameworks across different regions and the need to ensure patient safety, data privacy, and the effectiveness of digital health solutions.

One major challenge is the slow adaptation of existing regulations to keep pace with rapidly evolving technologies. Regulatory bodies often struggle to define clear guidelines for emerging technologies such as AI-driven diagnostics, wearable devices, and mobile health apps. This uncertainty can deter investment and slow down the development and deployment of new digital health solutions.

Moreover, compliance with regulations like HIPAA in the United States or GDPR in the European Union adds complexity and cost to digital health startups and established companies alike. Navigating these regulations requires significant resources and expertise, which can be a barrier, especially for smaller firms.

Addressing regulatory challenges requires collaboration between industry stakeholders, regulators, and policymakers to develop flexible, forward-thinking frameworks that foster innovation while ensuring patient safety and data protection.

Clear, harmonized regulations can ultimately enable the digital health market to thrive and deliver on its promise of improving healthcare accessibility and outcomes globally.

Reimbursement Issues

Financial barriers in the digital health market, particularly related to reimbursement issues, hinder healthcare providers from adopting telehealth services.

Many insurers and healthcare systems offer lower reimbursement rates for telehealth visits compared to traditional in-person consultations. This disparity discourages providers from investing in telehealth infrastructure.

Furthermore, reimbursement policies vary widely among payers, adding administrative burdens and uncertainty for providers integrating telehealth into their practice models. The complexities of billing and coding for telehealth services exacerbate these challenges, impacting revenue streams for healthcare organizations.

To overcome these barriers, aligning reimbursement policies with the demonstrated value and efficiency gains of telehealth is crucial.

Establishing equitable payment structures that incentivize providers to embrace telehealth while ensuring financial sustainability in healthcare delivery models is essential. This alignment encourage broader adoption of telehealth, enhancing accessibility and efficiency in healthcare services.

Expansion in Developing Markets

Expansion into emerging markets presents significant opportunities for telehealth providers to address healthcare disparities and tap into underserved populations.

Developing regions often face challenges such as limited access to healthcare facilities, shortages of healthcare professionals, and geographical barriers that hinder timely medical care.

By introducing telehealth services, providers bridge these gaps, offering remote consultations, diagnostics, and monitoring to patients who otherwise might struggle to access healthcare.

Improving infrastructure, including internet connectivity and mobile technology penetration, further enhances the feasibility of telehealth solutions in these regions.

Moreover, partnerships with local healthcare organizations and governments facilitate tailored telehealth implementations that meet the specific needs and cultural contexts of emerging markets, fostering sustainable healthcare delivery and improving overall health outcomes. Thereby, providing significant opportunities for the players in the digital health market.

Growing Partnerships, and Collaborations

Forming strategic partnerships and collaborations presents significant opportunities for telehealth providers to expand their service offerings and reach new patient populations.

By partnering with technology firms, telehealth providers leverage advanced platforms and innovations such as AI-driven diagnostics and remote monitoring solutions.

Collaborations with healthcare providers allow for integrated care models, combining telehealth services with in-person care to enhance patient outcomes and streamline healthcare delivery.

Additionally, partnerships with insurers facilitate reimbursement agreements and financial sustainability, ensuring telehealth services are accessible and economically viable for patients.

These alliances not only broaden the scope of digital health offerings but also foster innovation, efficiency, and scalability in healthcare delivery, ultimately improving access to quality care and addressing healthcare challenges across diverse populations and healthcare settings.

|

Category |

Projected CAGR through 2031 |

|

Component- Software |

19.40% |

|

Technology- Telehealthcare |

18.83% |

Software Segment to Account for the Most Significant Market Share

The software segment is set to dominate the global market in 2023 and is likely to maintain its dominance during in the forthcoming years recording a CAGR of 19.40%.

The growth of this segment is driven by increasing demand for electronic health records (EHR) systems, telemedicine platforms, mobile health applications, and AI-driven diagnostics.

Software solutions enable the digital transformation of healthcare delivery and management, making them essential in modern healthcare systems.

Factors such as advancements in artificial intelligence (AI) and machine learning (ML) for healthcare analytics, interoperability of health IT systems, and the expansion of telehealth services globally are expected to fuel the growth of software solutions in digital health.

Telehealthcare Accounts for a Considerable Share Globally

Telehealthcare technology account for a significant share in the global industry due to its ability to enhance healthcare accessibility, convenience, and cost-effectiveness. It enables patients to consult remotely, reducing the need for physical visits and overcoming geographical barriers.

Advancements in technology support secure and efficient communication between patients and healthcare providers, fostering continuity of care. The COVID-19 pandemic further underscored its importance, accelerating its adoption and integration into mainstream healthcare delivery systems globally.

|

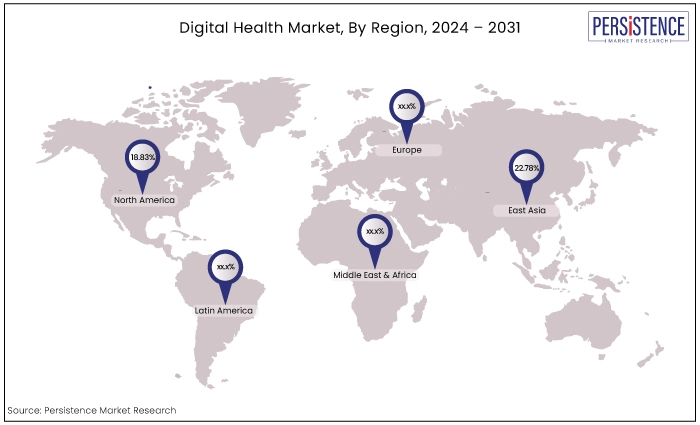

Region |

CAGR through 2034 |

|

North America |

18.83% |

|

East Asia |

22.78% |

North America to Account for a Significant Share of Global Market

North America is a significant shareholder in the global market and is expected to grow at a CAGR of 18.83% during the forecast period. This is driven by robust technological infrastructure, widespread adoption of digital health solutions, and supportive regulatory frameworks.

Factors such as increasing healthcare costs, expanding telecommunication networks, and growing patient preference for remote healthcare services contribute to the region's leadership in telehealth adoption.

Pandemic further, accelerated acceptance, prompting healthcare providers and patients alike to embrace telehealth solutions for safer and more accessible care delivery.

East Asia All Set to Exhibit a Notable CAGR Through 2031

East Asia Market is projected to secure a CAGR of 22.78% in the forecast period from 2024 to 2031. This growth is fuelled by advancements in technology, particularly in countries like China, Japan, and South Korea, where there is rapid adoption of digital health solutions.

Factors driving this expansion include increasing healthcare expenditures, aging populations, and efforts to improve healthcare access in remote areas.

Government support and investments in telehealth infrastructure further bolster growth. The COVID-19 pandemic accelerated the acceptance of telehealth, paving the way for sustained growth in East Asia's digital health market in the coming years.

In the digital health market, competition is fierce among established healthcare providers, tech firms, and startups. Leaders are known for their advanced telemedicine platforms, while tech giants are entering with innovative services. The market thrives on developments in remote patient monitoring, virtual consultations, and telemedicine software.

Companies focus on improving user experience, interoperability, and meeting regulatory standards. This dynamic landscape reflects ongoing efforts to enhance healthcare accessibility and efficiency through digital solutions, driven by increasing demand for remote healthcare services globally.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2018 to 2023 |

|

Market Analysis |

US$ Million for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Component

By Mode of Delivery

By Technology

By End User

By Region

To know more about delivery timeline for this report Contact Sales

The increasing demand for digital health solutions is driven by the need for convenient access to healthcare, advancements in technology, cost-effectiveness, and the COVID-19 pandemic accelerating virtual care adoption.

Some of the key players operating in the market are Teladoc Health, Inc., GE Healthcare, Siemens Healthineers, Koninklijke Philips N.V., and Medtronic among others.

The telehealthcare segment recorded the significant market share in 2023.

A compelling opportunity in the digital health market is its capacity to enhance healthcare accessibility and efficiency through remote consultations, digital health solutions, and integration of advanced technologies like AI and IoT, alongside expanding services into underserved regions and forging strategic partnerships.

North America is set to account for the significant share in the market.