- Medical Devices

- Dental Diamond Burs Market

Dental Diamond Burs Market Size, Share and Growth Forecast, 2026-2033

Dental Diamond Burs Market by Material (Diamond Burs, Stainless Steel, Carbide), Application (Oral Surgery, Implantology, Orthodontics, Cavity Preparation), End Use (Hospitals, Dental Clinics), and Regional Analysis for 2026 - 2033

Dental Diamond Burs Market Share and Trends Analysis

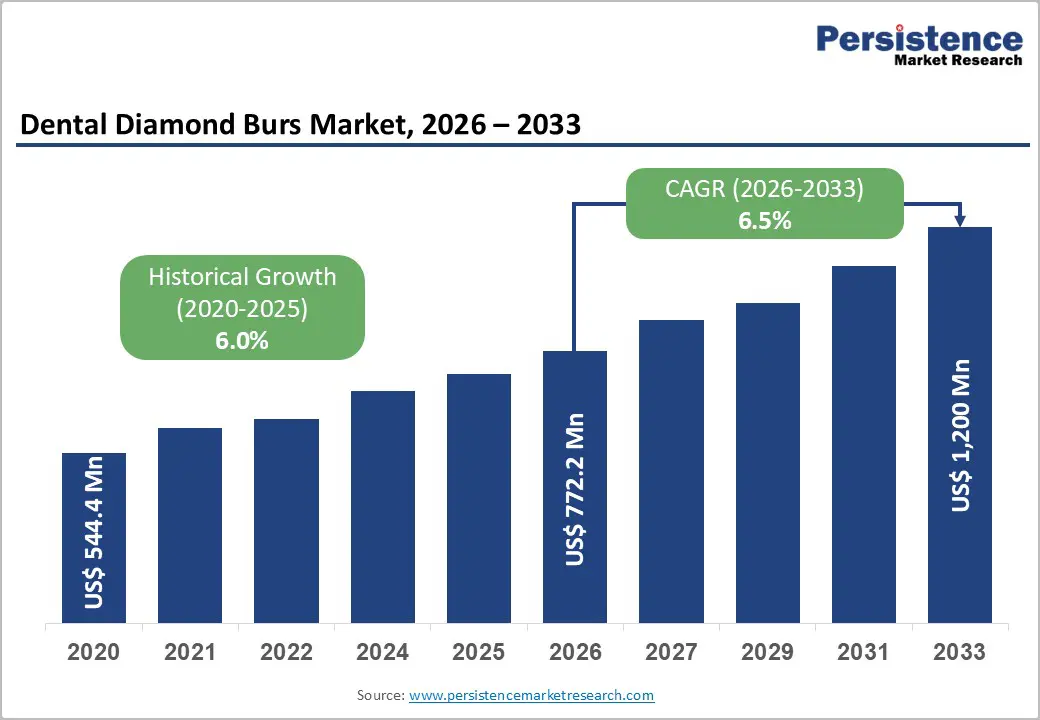

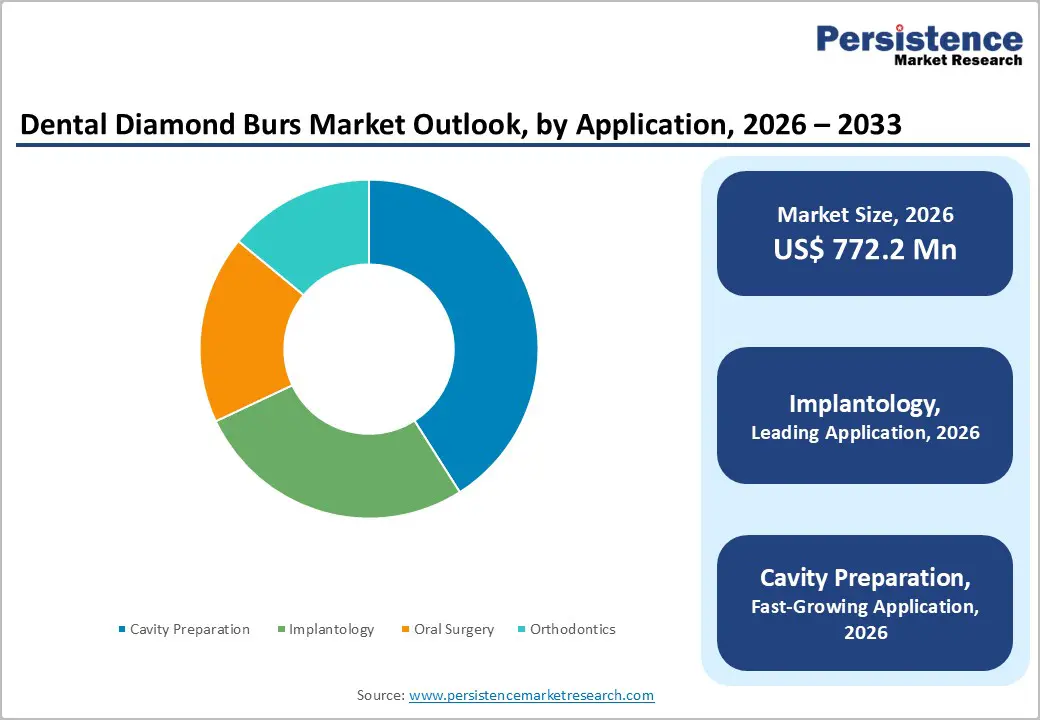

The global dental diamond burs market size is likely to be valued at US$772.2 million in 2026 and is projected to reach US$1,200 million by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by the increasing volume of restorative and cosmetic dental procedures, rising prevalence of dental disorders, and growing adoption of advanced dental instruments, dental consumables, and precision-driven treatment technologies. Increased awareness regarding oral healthcare, expanding dental infrastructure across emerging economies, and continuous innovation in dental burs and minimally invasive dentistry are supporting demand growth. Furthermore, growing investments in digital dentistry and implantology are strengthening the long-term outlook for the global dental diamond burs market.

Key Industry Highlights:

- Leading Material: Diamond burs are expected to dominate with an estimated 56% share in 2026, while carbide burs are projected to be the fastest-growing material segment at a 7.2% CAGR through 2033, supported by increasing demand for high-speed and precision cutting applications.

- Dominant Application: Cavity preparation is anticipated to lead with approximately 41% of market revenue in 2026, while implantology is likely to register the fastest growth at a 6.8% CAGR during 2026–2033, driven by rising dental implant adoption and digital treatment planning.

- Leading End-user: Dental clinics are set to account for around 68% of the market share in 2026, whereas hospitals are expected to be the fastest-growing end-use segment, expanding at a 7.0% CAGR through 2033 as specialized oral healthcare services continue to develop.

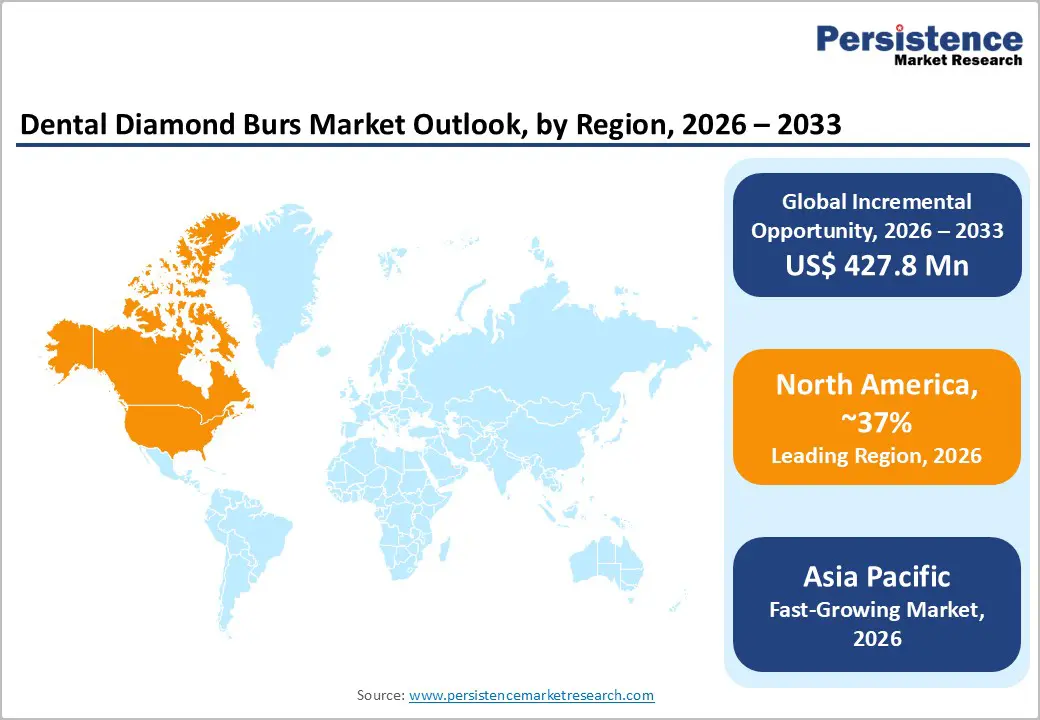

- Regional Leadership: North America is poised to lead the global market with an estimated 37% share in 2026, while Asia Pacific is projected to record the fastest growth at a 7.4% CAGR through 2033, supported by expanding dental infrastructure and increasing oral healthcare awareness.

- Technology & Procedure Trends: Growing adoption of digital dentistry, CAD/CAM workflows, minimally invasive procedures, and implant-based restorations is accelerating demand for advanced diamond-coated rotary instruments.

- Competitive Environment: Competitive activity is centered on digital dentistry integration, advanced diamond-coating technologies, minimally invasive treatment solutions, and expansion across emerging markets to strengthen product portfolios and market presence.

DRO Analysis

Driver - Rising Global Burden of Dental Diseases and Growth in Restorative Dentistry

The increasing prevalence of dental disorders remains the most significant growth driver for the dental diamond burs market. According to the World Health Organization (WHO), oral diseases affect approximately 3.5 billion people globally, while untreated dental caries in permanent teeth remains among the most common health conditions worldwide. The WHO estimates that severe periodontal disease impacts nearly 19% of the global adult population, representing over one billion cases. Growing incidences of tooth decay, enamel erosion, periodontal conditions, and tooth loss have increased the demand for restorative procedures requiring precision cutting and finishing instruments such as diamond burs.

Simultaneously, the expansion of cosmetic dentistry, crown preparation, veneer placement, and dental implant procedures is driving higher utilization rates of advanced dental rotary instruments. Dental clinics are increasingly adopting premium diamond-coated burs because they provide superior cutting efficiency, reduced vibration, improved procedural accuracy, and better patient outcomes. As healthcare systems continue to emphasize preventive and restorative oral care, the demand for high-performance dental burs is expected to grow consistently throughout the forecast period.

Restraint – Cost Pressures and Preference for Lower-Cost Alternatives

The adoption of premium dental diamond burs continues to face challenges from cost-sensitive purchasing behavior, particularly in emerging markets. Diamond burs carry higher production costs due to diamond-coating processes, strict sterilization requirements, and medical-device quality standards, making them significantly more expensive than stainless steel or carbide alternatives.

According to the World Bank, healthcare spending remains below 6% of GDP in many developing economies, limiting procurement budgets for public dental facilities. Additionally, inflation, raw material price volatility, and supply chain disruptions have increased manufacturing costs across the dental industry. These pressures encourage clinics to extend product replacement cycles or opt for lower-cost alternatives, constraining recurring sales opportunities and creating pricing pressure for manufacturers.

Opportunity - Expansion of Implantology and Aesthetic Digital Dentistry

The rapid growth of implantology and digital dentistry presents a significant opportunity for the dental diamond burs market. Increasing adoption of CAD/CAM systems, intraoral scanners, guided surgery, and digital treatment planning is driving demand for highly precise preparation and finishing instruments. Additionally, growing consumer spending on cosmetic dentistry, including veneers, smile design, tooth reshaping, and aesthetic restorative procedures, is increasing the use of precision diamond burs.

According to the World Health Organization (WHO), oral diseases affect nearly 3.5 billion people globally, while aging populations continue to increase demand for restorative and implant treatments. The International Team for Implantology (ITI) also reports sustained growth in dental implant adoption worldwide. Combined with expanding dental infrastructure across Asia-Pacific, Latin America, and the Middle East, these trends create substantial opportunities for manufacturers offering specialized diamond burs for implantology, aesthetic dentistry, and digitally guided procedures.

Category-wise Analysis

Material Insights

Diamond burs are expected to dominate with approximately 56% market share in 2026, supported by their superior hardness and ability to cut enamel, zirconia, and ceramic materials with high precision. Their widespread adoption is strongly linked to the rise in aesthetic dentistry procedures, particularly all-ceramic crowns and veneers, which require fine finishing accuracy. Clinical dentistry practices increasingly prefer diamond-coated instruments for their consistency and reduced procedural time. The American Dental Association (ADA) notes steady growth in cosmetic restorative procedures across developed markets, indirectly reinforcing demand for high-precision rotary tools.

Carbide burs are projected to expand at a 7.2% CAGR through 2033, driven by their efficiency in removing old restorations and cutting metal-based dental materials. Their usage is increasing in prosthodontic re-treatment cases where speed and durability are critical. Growth is further supported by the rising adoption of CAD/CAM restorations, which often require adjustment and finishing using carbide instruments. Dental service organizations (DSOs) in North America are increasingly standardizing carbide burs for high-volume clinical workflows due to their cost-efficiency and performance stability.

Application Insights

Cavity preparation is expected to account for around 41% market share in 2026, driven by the high global incidence of dental caries. Data from the Institute for Health Metrics and Evaluation (IHME) confirms that untreated dental decay remains the most widespread oral condition globally. This creates continuous demand for restorative procedures in primary dental care settings. Diamond burs remain essential in these procedures due to their ability to remove decayed tissue precisely while preserving healthy tooth structure, improving long-term treatment outcomes.

Implantology is projected to grow at a 6.8% CAGR during 2026–2033, supported by increasing adoption of dental implants as a permanent tooth replacement solution. Clinical reports from the International Team for Implantology (ITI) indicate rising implant penetration across aging populations in Japan, Germany, and South Korea. Growth is also supported by improved surgical success rates and expanding insurance coverage in select developed markets. These factors are driving demand for specialized diamond burs used in bone preparation and implant site finishing.

End-user Insights

Dental clinics are expected to hold approximately 68% market share in 2026, as they represent the primary setting for restorative, orthodontic, and cosmetic dental procedures. OECD healthcare utilization data shows that outpatient dental clinics account for the majority of dental visits in developed economies. Increasing patient preference for private dental care and elective cosmetic procedures such as smile design and veneers continues to strengthen demand for precision rotary instruments. This positions clinics as the largest consumers of dental burs globally.

Hospitals are projected to grow at a 7.0% CAGR through 2033, driven by increasing integration of oral and maxillofacial surgery departments. Many healthcare systems in Europe and Asia are expanding hospital-based dental infrastructure to manage complex surgical cases and trauma-related procedures. Government-led investments in tertiary healthcare facilities are also supporting this shift. As hospitals adopt more advanced surgical workflows, demand for high-performance burs used in implant and reconstructive procedures continues to rise.

Regional Insights

North America Dental Diamond Burs Market Trends

North America is estimated to lead the dental diamond burs market with around 37% global share in 2026, driven by high procedural intensity in restorative and implant dentistry. The region records one of the highest dental care utilization levels globally, with the U.S. accounting for over 200 million annual dental visits, supporting consistent consumable demand. Strong penetration of CAD/CAM systems in more than 60% of mid-to-large dental practices in the U.S. is further increasing reliance on precision diamond burs for crown, veneer, and implant-related procedures.

U.S. Dental Diamond Burs Market Trends

The U.S. is estimated to account for nearly 82% of the North America market share in 2026, supported by a large base of private dental clinics and DSOs with high procedural throughput. High cosmetic dentistry penetration, where veneers and crowns represent a major share of elective treatments, continues to drive demand for precision burs. Expansion of DSOs is enabling standardized procurement across multi-clinic networks, while increasing adoption of zirconia restorations and chairside milling systems is strengthening usage in finishing applications.

Canada Dental Diamond Burs Market Trends

Canada is estimated to hold around 18% of the North America market share in 2026, supported by rising insurance-backed dental visits, with nearly two in three Canadians covered under some form of dental insurance, improving access to restorative care. Gradual adoption of CAD/CAM-supported workflows in urban clinics is increasing reliance on precision rotary instruments for crown and bridge procedures. The growing preference for minimally invasive dentistry is further supporting steady demand for diamond burs in restorative and preventive applications.

Europe Dental Diamond Burs Market Trends

Europe is estimated to account for approximately 30% of the global dental diamond burs market share in 2026, driven by high adoption of implant dentistry and structured dental healthcare systems. The region benefits from a strong aging population, with over 21% of residents aged above 65, which is increasing demand for restorative and prosthodontic procedures. Europe also maintains strong implant penetration, particularly across Western countries, supporting consistent utilization of precision dental burs.

Germany Dental Diamond Burs Market Trends

Germany is estimated to contribute around 24% of the Europe market share, making it the largest country-level market in the region. High dentist density and strong procedural output in implantology and restorative dentistry continue to support demand. Widespread use of zirconia restorations is increasing reliance on diamond burs for finishing and contouring, while digital impression systems and milling technologies are further enhancing precision-driven workflows in private clinics.

U.K. Dental Diamond Burs Market Trends

The U.K. is estimated to hold nearly 18% of the Europe market share, supported by strong growth in private dental care, where over 50% of adults opt for private treatment for faster access and aesthetic procedures. Rising demand for veneers, whitening, and smile correction procedures is increasing the usage of precision rotary instruments. Expansion of digital scanning technologies in clinics is improving workflow efficiency and indirectly increasing bur consumption in restorative finishing applications.

Asia Pacific Dental Diamond Burs Market Trends

Asia Pacific is estimated to be the fastest-growing region and account for approximately 25% of the global share in 2026, driven by rapid expansion of dental infrastructure and increasing adoption of cosmetic and implant dentistry. Growth is supported by rising urban clinic penetration and increasing awareness of oral aesthetics. Expanding demand for implantology and restorative dentistry procedures is significantly increasing consumption of precision dental burs across both private and institutional settings.

China Dental Diamond Burs Market Trends

China is estimated to represent around 38% of the Asia Pacific market share, making it the largest contributor in the region. Rapid expansion of private dental chains and increasing demand for cosmetic dentistry in urban centers are driving higher procedural volumes. Growth in implant procedures is being supported by rising middle-class spending on restorative care, while expansion of Tier-1 and Tier-2 city dental networks is accelerating adoption of precision diamond burs used in zirconia and ceramic restorations.

India Dental Diamond Burs Market Trends

India is estimated to account for approximately 22% of the Asia Pacific market share, supported by increasing dental clinic penetration and rising awareness of aesthetic dentistry in urban populations. Expansion of private dental chains and multi-specialty clinics in metropolitan cities is improving access to advanced restorative procedures. Growing adoption of cosmetic treatments such as veneers and smile correction, along with increasing use of rotary instruments in dental education, is further supporting steady market expansion.

Competitive Landscape

The global dental diamond burs market exhibits a moderately fragmented competitive structure characterized by the presence of multinational dental equipment manufacturers, specialized rotary instrument producers, and regional suppliers. The top five companies collectively account for an estimated 35–45% of global market revenue, while numerous regional manufacturers compete through pricing, product customization, and distribution capabilities.

Competition is primarily based on product quality, cutting performance, durability, sterilization compatibility, and innovation in coating technologies. Leading companies focus on expanding premium product portfolios, strengthening distribution networks, and developing specialized burs for implantology, prosthodontics, and digital dentistry applications. The market also benefits from recurring demand generated through routine replacement cycles within dental practices.

Companies Covered in Dental Diamond Burs Market

- Dentsply Sirona

- Komet Dental

- Brasseler USA

- COLTENE Group

- MANI Inc.

- Henry Schein Inc.

- Kerr Corporation

- SHOFU Inc.

- Microcopy Dental

- Prima Dental Group

- Meisinger

- Horico

- DentalEZ Group

- NSK Ltd.

- Young Innovations

Frequently Asked Questions

The global dental diamond burs market is projected to reach US$772.2 million in 2026.

Rising restorative dental procedures, increasing cosmetic dentistry demand, and growing adoption of digital dentistry drive the market.

The dental diamond burs market is expected to grow at a CAGR of 6.5% from 2026 to 2033.

Expansion of implantology, rising aesthetic dentistry demand, and growth of CAD/CAM-based workflows create key opportunities.

Key players include Dentsply Sirona, Komet Dental, Brasseler USA, COLTENE Group, and MANI Inc.