- Healthcare Services

- Cloud-based Drug Discovery Platform Market

Cloud-based Drug Discovery Platform Market Size, Share, and Growth Forecast 2026 - 2033

Cloud-based Drug Discovery Platform Market by Service Type (Software as a Service (SaaS), Platform as a Service (PaaS), Infrastructure as a Service (IaaS)), by Technology (Artificial Intelligence (AI) & Machine Learning, Computational Chemistry, Molecular Modeling & Simulation, Bioinformatics & Genomics Analytics, Others), by Application, by Therapeutic Area, by End User, by Regional Analysis, 2026 - 2033

Cloud-based Drug Discovery Platform Market Size and Trend Analysis

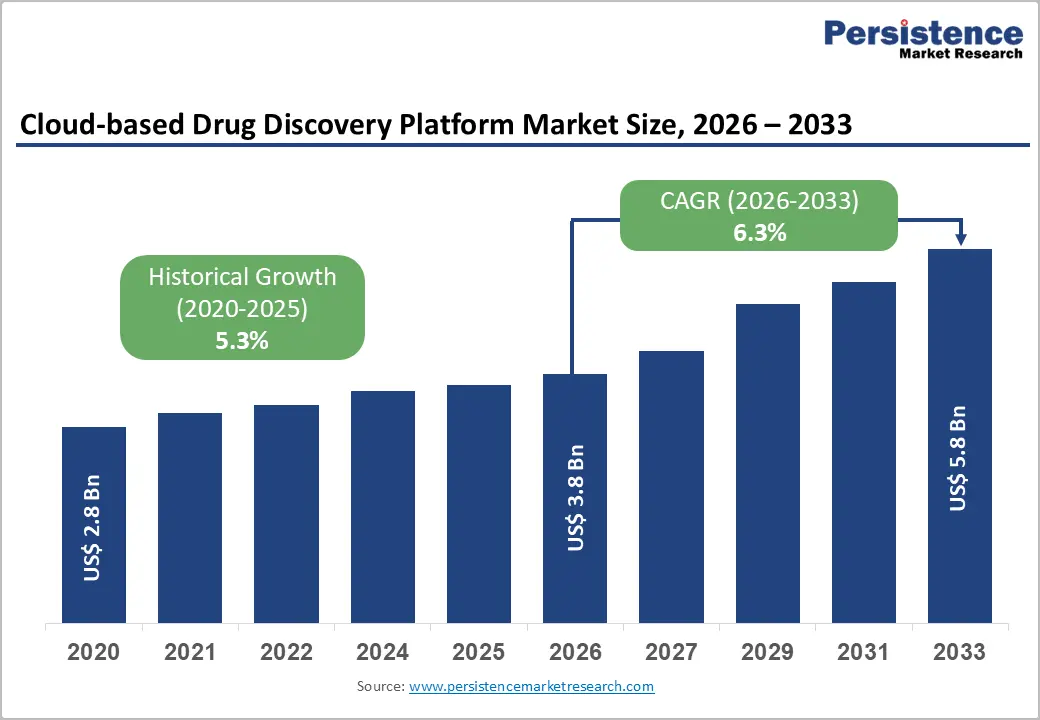

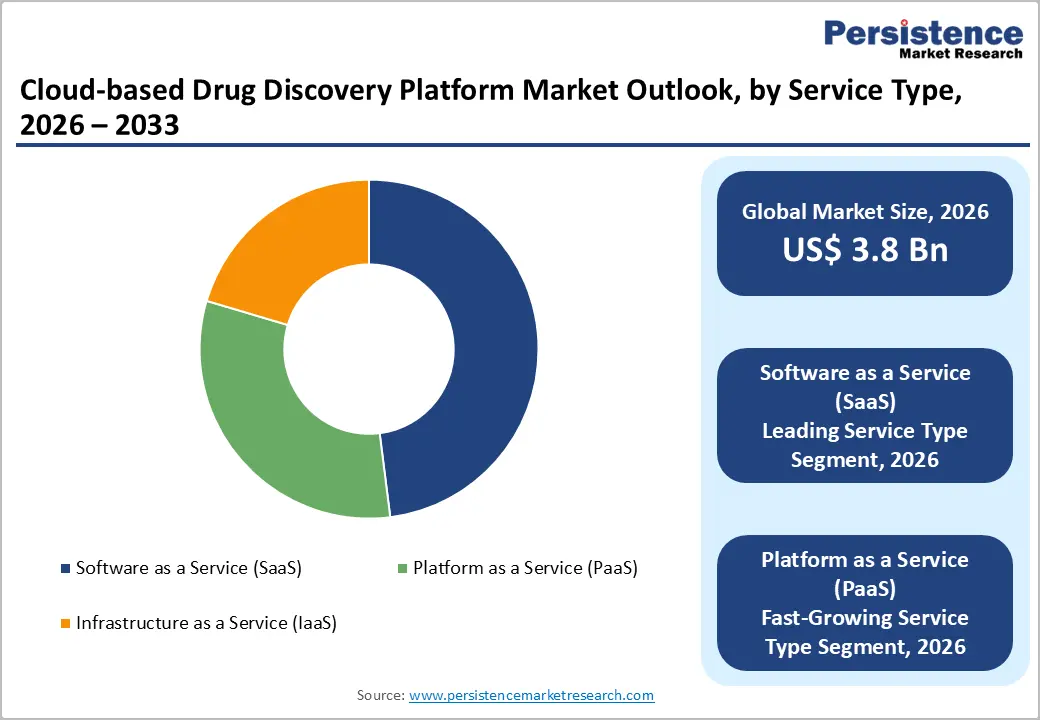

The global cloud-based drug discovery platform market size is expected to reach US$ 3.8 billion in 2026 and US$ 5.8 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The market growth is fundamentally driven by converging forces: the growing cost and complexity of traditional drug discovery, rapid maturation of artificial intelligence and machine learning tools, and the pharmaceutical industry's accelerating shift toward cloud-native research infrastructure. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), the average cost to bring a new drug to market exceeds US$ 2.6 billion, underscoring the urgency for cost-efficient, data-driven discovery platforms.

The integration of AI-powered virtual screening, high-throughput molecular simulation, and collaborative cloud environments is enabling pharmaceutical and biotechnology firms to compress discovery timelines, reduce experimental failure rates, and unlock precision medicine applications that were previously computationally infeasible.

Key Highlights

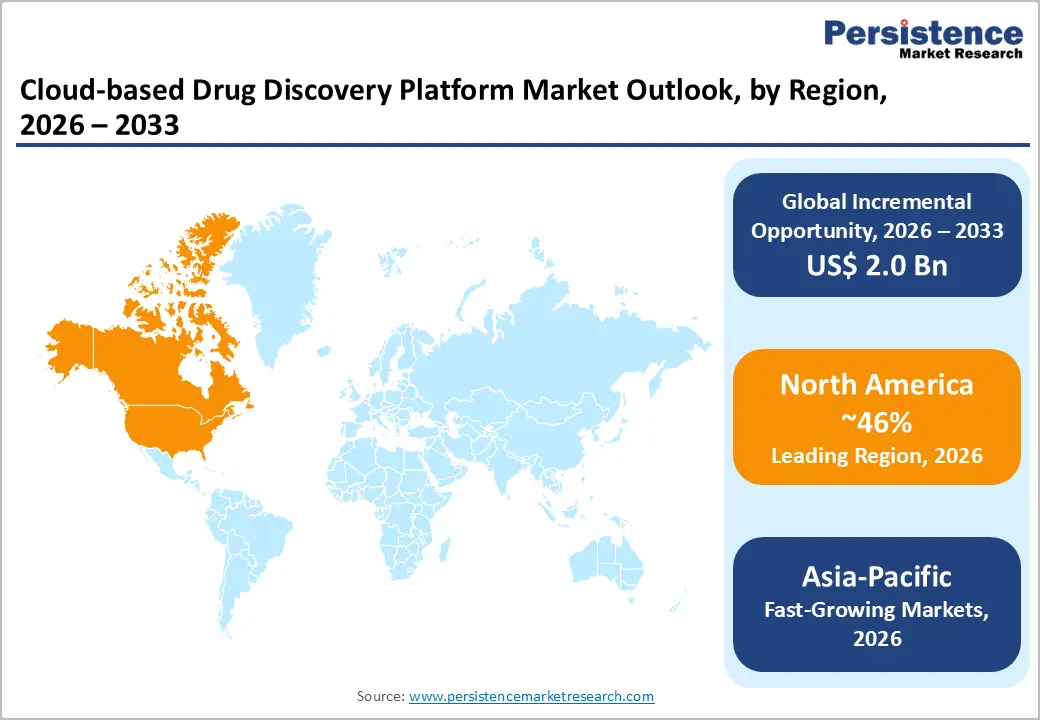

- Regional Leadership: North America holds 46% global share in 2026, supported by the world's largest pharmaceutical R&D ecosystem, NIH funding exceeding US$ 47 billion, and a dense concentration of AI drug discovery companies.

- Fast-growing Market: Asia Pacific is projected to register a leading CAGR by 2033, fueled by China's and India's expanding pharmaceutical R&D investment, government AI mandates, and a growing cloud-enabled CRO sector.

- Leading Service Type: Software as a Service holds 48% market share in 2025, driven by its low capex model, rapid deployment capability, and broad adoption across pharmaceutical companies and CROs globally.

- PaaS is the Fast-Growing Service Type Segment: Platform as a Service is forecast to reach the high CAGR, as drug discovery organizations seek customizable, scalable cloud environments to deploy proprietary AI models and integrate multi-source research datasets.

- Key Opportunity: The convergence of cloud AI platforms with multi-omics oncology data and precision medicine workflows is expected to generate the largest incremental revenue opportunity through the forecast period to 2033.

Market Dynamics

Drivers - Surging R&D Costs and the Imperative for Computational Drug Discovery

The unsustainable economics of traditional drug discovery are among the most powerful tailwinds for cloud-based platforms. The PhRMA estimates that pharmaceutical companies invested over US$ 102 billion globally in R&D in 2021, yet the industry's average probability of clinical success remains below 10%. Cloud-based platforms equipped with AI-driven molecular docking, predictive toxicology, and generative chemistry tools dramatically reduce wet-lab dependency and accelerate hit identification.

A 2022 study in Nature Reviews Drug Discovery found that AI-assisted drug design reduced lead optimization timelines by up to 50% in select therapeutic programs. This cost-efficiency imperative is compelling both large pharmaceutical companies and emerging biotech firms to migrate discovery workflows onto scalable cloud infrastructure, generating sustained platform demand.

AI and Machine Learning Integration: Transforming Target Identification and Lead Optimization

The rapid integration of artificial intelligence and machine learning into cloud-based drug discovery is a defining market driver. Breakthroughs such as DeepMind's AlphaFold2 protein structure prediction model, which has made over 200 million protein structures publicly accessible, have fundamentally expanded the scope of structure-based drug design on cloud platforms.

The U.S. National Institutes of Health (NIH) has allocated substantial funding toward AI-integrated biomedical research infrastructure, including cloud-based genomics analytics. Companies such as Exscientia plc and Insilico Medicine Inc. have demonstrated the ability to advance AI-designed drug candidates into clinical trials within timelines previously unachievable, validating cloud AI platforms as credible accelerators of the drug development pipeline.

Restraints - Data Privacy, Security, and Regulatory Compliance Concerns

The cloud migration of sensitive pharmaceutical research data presents significant cybersecurity and regulatory compliance challenges. The U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) impose strict data integrity and audit-trail requirements for drug development processes, complicating cloud deployments.

High-profile pharmaceutical cyberattacks, including a 2020 breach at Dr. Reddy's Laboratories coinciding with COVID-19 vaccine trials, highlight the operational risks. Concerns over intellectual property protection, cross-border data sovereignty regulations, and compliance with GDPR in Europe further constrain adoption among organizations with legacy IT infrastructure and conservative data governance policies.

High Implementation Complexity and Interoperability Barriers

Despite their transformative potential, cloud-based drug discovery platforms face significant barriers related to implementation complexity, data standardization, and interoperability with existing laboratory information management systems (LIMS) and enterprise resource planning (ERP) tools. Many established pharmaceutical companies maintain decades-old data silos in incompatible proprietary formats.

A 2023 Deloitte Life Sciences report noted that over 60% of biopharma organizations cite data integration as a primary obstacle to digital transformation. These technical and organizational friction points elevate the total cost of ownership and extend deployment timelines, particularly for mid-size and smaller research institutions that lack the specialized IT talent required for successful platform implementation.

Opportunities - Platform as a Service (PaaS) Adoption: Unlocking Customizable Drug Discovery Ecosystems

Platform as a Service (PaaS) is emerging as the fastest-growing deployment model within the cloud-based drug discovery market, offering research organizations the ability to build, deploy, and scale custom computational chemistry and AI workflows without managing underlying infrastructure. The National Science Foundation (NSF) and other public research funders are increasingly supporting open cloud PaaS environments for collaborative biomedical research.

Leading vendors, including Schrödinger, Inc. and Dassault Systèmes SE are building extensible PaaS ecosystems that enable pharmaceutical clients to integrate proprietary datasets, third-party AI models, and experimental automation tools. As biopharma organizations prioritize differentiated computational capabilities, the flexibility and scalability of PaaS are positioning it as the preferred model for next-generation drug discovery infrastructure investment.

Oncology and Precision Medicine Applications Creating Substantial Demand for Cloud AI Platforms

Oncology remains the most active therapeutic area for cloud-based drug discovery, driven by the extraordinary genomic complexity of cancer and the rapid growth of precision medicine. The National Cancer Institute (NCI) reports that the U.S. alone spends over US$ 200 billion annually on cancer care, underscoring the clinical and commercial imperative for better drugs.

Cloud platforms capable of integrating multi-omics data, patient-derived organoid screening results, and real-world clinical evidence are enabling targeted therapy discovery at an unprecedented scale. Recursion Pharmaceuticals, Inc. and Absci Corporation are actively leveraging cloud AI infrastructure for oncology indication expansion. The convergence of cloud computing with precision oncology is expected to remain a primary commercial opportunity through the forecast horizon.

Category-wise Analysis

Service Type Insights

Software as a Service (SaaS) leads the cloud-based drug discovery platform market, commanding approximately 48% of the market share in 2025. SaaS dominance is rooted in its low upfront capital expenditure, rapid deployment capability, and elimination of infrastructure maintenance burdens, attributes that are highly valued in fast-moving pharmaceutical and biotechnology R&D environments. According to Gartner, global SaaS revenues across enterprise sectors have grown by double digits annually since 2019, reflecting broad organizational confidence in subscription-based cloud delivery.

In drug discovery specifically, SaaS platforms such as Veeva Vault and Schrödinger's LiveDesign provide streamlined access to advanced molecular design, data management, and regulatory submission workflows with minimal IT overhead, driving their widespread adoption across pharmaceutical companies and contract research organizations globally.

Technology Insights

Artificial Intelligence (AI) & Machine Learning is the dominant technology segment in the cloud-based drug discovery platform market, estimated to account for approximately 38% share in 2026. The segment's leadership reflects the transformative impact of deep learning, generative models, and natural language processing on drug candidate identification, property prediction, and clinical trial design.

A 2023 paper in Nature Machine Intelligence demonstrated that AI models could predict drug-target binding affinities with accuracy rivaling experimental assays. The breadth of AI applications spanning virtual screening, ADMET prediction, de novo molecule generation, and biomarker identification positions it as the foundational technology layer for virtually all cloud drug discovery workflows, reinforcing its commanding share across the competitive landscape.

Application Insights

Small molecule drug discovery represents the leading application segment, accounting for an estimated 40% market share in 2025. This segment's dominance reflects the deep historical and commercial foundation of small molecule therapeutics, which constitute the majority of approved drugs and active pharmaceutical pipelines globally. The FDA approved 55 novel drugs in 2023, with small molecules continuing to represent the majority of approvals.

Cloud platforms enable high-throughput virtual screening of billions of chemical compounds, accelerating early-stage hit discovery. The maturity of cheminformatics tools, extensive public chemical databases such as PubChem (containing over 111 million compounds), and established computational docking methodologies make small molecule discovery the most computationally tractable application for cloud deployment.

Therapeutic Area Insights

Oncology is the dominant therapeutic area in the cloud-based drug discovery platform market, representing an estimated 33% of market share in 2025. The extraordinary scientific complexity of cancer, characterized by tumor heterogeneity, resistance mechanisms, and intricate signaling networks creates an ideal use case for AI-powered cloud platforms capable of processing vast multi-omics and imaging datasets.

According to the IQVIA Institute for Human Data Science, oncology accounted for over 25% of all clinical trials globally in 2022. The pipeline density in immuno-oncology, targeted therapy, and antibody-drug conjugates demands continuous computational optimization of candidate molecules, sustaining disproportionate demand for cloud-based discovery tools within this indication area.

End-user Insights

Pharmaceutical companies constitute the leading end-user segment, commanding approximately 45% of the cloud-based drug discovery platform market in 2025. Large pharmaceutical organizations including Pfizer, AstraZeneca, and Novartis, have invested heavily in proprietary cloud discovery infrastructure and strategic partnerships with platform providers. Their R&D budgets, which collectively exceeded US$ 200 billion globally in 2022 per EFPIA data, enable sustained investment in cutting-edge AI platforms.

The competitive pressure to reduce time-to-IND and leverage external data partnerships further accelerates cloud platform adoption among pharmaceutical companies seeking operational agility and scientific differentiation.

Regional Insights

North America Cloud-based Drug Discovery Platform Market Trends and Insights

North America accounted for approximately 46.2% of the global cloud-based drug discovery platform market in 2025, driven by deep pharmaceutical R&D budgets, advanced hyperscale cloud infrastructure, and rapid adoption of AI-enabled discovery workflows. Strong collaboration among pharmaceutical companies, biotechnology firms, and academic research centers accelerates the deployment of scalable computational platforms for molecular modeling, omics analytics, and virtual screening.

The region also benefits from increasing regulatory clarity on the use of AI in pharmaceutical development and the presence of leading innovators such as Schrödinger, Recursion Pharmaceuticals, and Isomorphic Labs. High concentrations of venture capital and specialized computational biology talent further reinforce North America’s leadership in next-generation drug discovery technologies.

U.S. Cloud-Based Drug Discovery Platform Market

The U.S. is likely to represent nearly 88.7% of the North America smarket in 2026. Leadership is supported by more than US$48 billion in annual NIH biomedical research funding, extensive cloud adoption across pharmaceutical R&D, and major innovation clusters in Boston-Cambridge, the San Francisco Bay Area, and San Diego. Large pharmaceutical companies and AI-native biotech firms increasingly rely on AWS, Microsoft Azure, and Google Cloud to accelerate target identification, lead optimization, and translational research workflows.

Canada Cloud-Based Drug Discovery Platform Market

Canada is poised for an estimated 7.9% regional share sin 2026. Growth is fueled by federal AI initiatives, strong research ecosystems in Toronto, Montreal, and Vancouver, and expanding biotechnology activity using cloud-native bioinformatics and simulation platforms. Government-backed institutes such as the Vector Institute and Mila are strengthening Canada’s position as a hub for machine learning applications in drug discovery.

Europe Cloud-Based Drug Discovery Platform Market Trends and Insights

Europe captured approximately 28.4% of global revenue in 2026, supported by coordinated public research funding, a strong pharmaceutical manufacturing base, and rising adoption of AI and bioinformatics platforms. Horizon Europe and the European Medicines Agency are fostering digital transformation and harmonized approaches to advanced analytics in drug development. The region benefits from world-class universities, established pharmaceutical leaders, and a growing network of AI-driven biotech companies. Increasing cross-border collaborations and sovereign cloud investments are enhancing secure data sharing and accelerating computational discovery workflows across Europe.

Germany Cloud-based Drug Discovery Platform Market

Germany accounted for about 24.8% of the European market in 2026. The country benefits from robust pharmaceutical R&D, industrial cloud adoption, and active use of computational chemistry platforms by Bayer and numerous biotech startups. Research institutions such as Max Planck and Helmholtz centers further support high-performance computing and data-intensive life sciences applications.

UK Cloud-based Drug Discovery Platform Market

The Uk represented roughly 22.6% of the regional market in 2026. Oxford, Cambridge, and London remain global hubs for AI-driven discovery, anchored by companies such as Exscientia and BenevolentAI. Strong venture funding, NHS-linked datasets, and supportive life sciences policies continue to expand the adoption of cloud-based discovery platforms.

France Cloud-based Drug Discovery Platform Market

France held approximately 16.9% of Europe’s market in 2026, supported by expanding cloud adoption in pharmaceutical research and innovation activity led by Sanofi and a growing biotech ecosystem. Public investments in health data infrastructure and precision medicine are strengthening national capabilities in computational drug development.

Asia Pacific Cloud-based Drug Discovery Platform Market Trends and Insights

Asia Pacific accounted for nearly 19.7% of the global market in 2026 and is projected to register a fast- CAGR of 18.9% in the coming years. Growth is driven by rising pharmaceutical R&D spending, expanding CRO capabilities, and government initiatives promoting AI and cloud integration in life sciences. The region offers a large pool of scientific talent, competitive operating costs, and increasing investments in genomics and precision medicine. Strengthening digital infrastructure and supportive policy frameworks are enabling rapid adoption of cloud-based discovery platforms across both developed and emerging markets.

China Cloud-based Drug Discovery Platform Market

China contributed around 39.4% of the Asia Pacific market in 2026. National bioeconomy policies and a rapidly expanding biotech ecosystem are accelerating the use of AI-based molecular design and cloud analytics platforms. Strong government funding and increasing partnerships between domestic innovators and global pharmaceutical companies continue to boost adoption.

Japan Cloud-based Drug Discovery Platform Market

Japan accounted for approximately 21.8% of the regional market in 2026. Adoption is supported by advanced pharmaceutical research, regulatory guidance for AI in drug development, and strong demand for high-performance computational tools. Leading companies are integrating cloud platforms to improve translational research and biologics discovery efficiency.

India Cloud-based Drug Discovery Platform Market

India represented nearly 14.6% market share in 2026. Expansion of the domestic CRO sector and increasing investments in bioinformatics and precision medicine are driving rapid uptake of cloud-based discovery platforms. Cost-effective scientific talent and growing partnerships with global biopharmaceutical companies are strengthening India’s strategic role in computational drug discovery.

Competitive Landscape

The cloud-based drug discovery platform market exhibits a moderately fragmented competitive landscape, with a mix of diversified technology conglomerates such as IBM Corporation, Oracle Corporation, and Accenture and specialized AI drug discovery firms including Schrödinger, Exscientia, and Recursion Pharmaceuticals. Key competitive strategies include strategic alliances with pharmaceutical companies, acquisition of AI startups, and expansion of modular SaaS/PaaS offerings.

Differentiation is increasingly achieved through proprietary AI model performance, molecular simulation accuracy, and platform interoperability. Emerging business models combining cloud platform licensing with co-development milestone payments are gaining traction as indicators of market maturation.

Key Developments:

- In May 2026, Amazon Web Services launched Amazon Bio Discovery, an AI-powered platform that combines more than 40 biological foundation models with agentic assistants and CRO partnerships to integrate computational and wet-lab drug discovery workflows. The lab-in-the-loop platform is designed to accelerate candidate design and significantly reduce early-stage drug research timelines.

- In April 2026, Novo Nordisk partnered with OpenAI to expand the use of artificial intelligence across its drug development operations. The collaboration supports Novo Nordisk’s strategic initiative to apply AI in target discovery, clinical development, and operational decision-making to accelerate the development of new therapies and improve R&D productivity.

- In June 2024, Athos Therapeutics, a clinical-stage biotech focused on precision small-molecule therapeutics for autoimmune and chronic inflammatory diseases, selected Vultr’s private cloud to power its AI-driven drug discovery engine.

- In January 2024, Accenture, through Accenture Ventures, strategically invested in QuantHealth, an AI-powered clinical trial design company. This investment helped pharmaceutical and biotech firms accelerate cloud-based trial simulations, enabling faster and cost-effective drug development for patients.

Companies Covered in Cloud-based Drug Discovery Platform Market

- Accenture Global Services Limited

- Dassault Systèmes SE

- Tata Consultancy Services Limited

- International Business Machines Corporation

- SAS Institute Inc.

- BioXcel Therapeutics, Inc.

- Schrödinger, Inc.

- Veeva Systems Inc.

- Oracle Corporation

- Insilico Medicine Inc.

- Recursion Pharmaceuticals, Inc.

- Alphabet Inc.

- Exscientia plc

- Absci Corporation

- Others

Frequently Asked Questions

The global cloud-based drug discovery platform market is expected to be valued at US$ 3.8 billion in 2026, growing from US$ 2.8 billion in 2020 at a historical CAGR of 5.3%. It is projected to reach US$ 5.8 billion by 2033, reflecting the accelerating adoption of AI-driven and cloud-native drug discovery infrastructure across the global pharmaceutical industry.

Rising adoption of AI-driven drug discovery, growing pharmaceutical R&D spending, expanding biological and genomic datasets, and the need for scalable, cost-efficient cloud computing infrastructure.

North America is the leading region, holding approximately 46% of the global market share in 2025. The region's dominance is attributed to its world-leading pharmaceutical and biotechnology R&D ecosystem, substantial NIH research funding, progressive FDA regulatory frameworks, and the headquarters concentration of leading cloud drug discovery platform providers.

Integration of generative AI and digital twins, increasing adoption by biotech startups and CROs, expansion in emerging markets, and growing demand for cloud platforms supporting precision medicine and biologics discovery.

Leading companies in the market include Schrödinger, Inc., Exscientia plc, Insilico Medicine Inc., Recursion Pharmaceuticals, Inc., Alphabet Inc. (Isomorphic Labs), Veeva Systems Inc., Oracle Corporation, IBM Corporation, Absci Corporation, and Dassault Systèmes SE, among others, competing through AI model innovation, strategic pharma partnerships, and global platform expansion.