- Inks, Coatings, Adhesives & Sealants (ICAS)

- Waterproofing Chemicals Market

Waterproofing Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Waterproofing Chemicals Market by Product Type (Bitumen, PVC, EPDM, TPO, PTFE, Silicone, Others), Technology (Performed Membrane, Coatings & LAMs, Integral Systems), Application (Roofing & Walls, Floors & Basements, Waste & Water Management, Tunnel Liners, Others), and Regional Analysis, 2026 - 2033

Waterproofing Chemicals Market Size and Trend Analysis

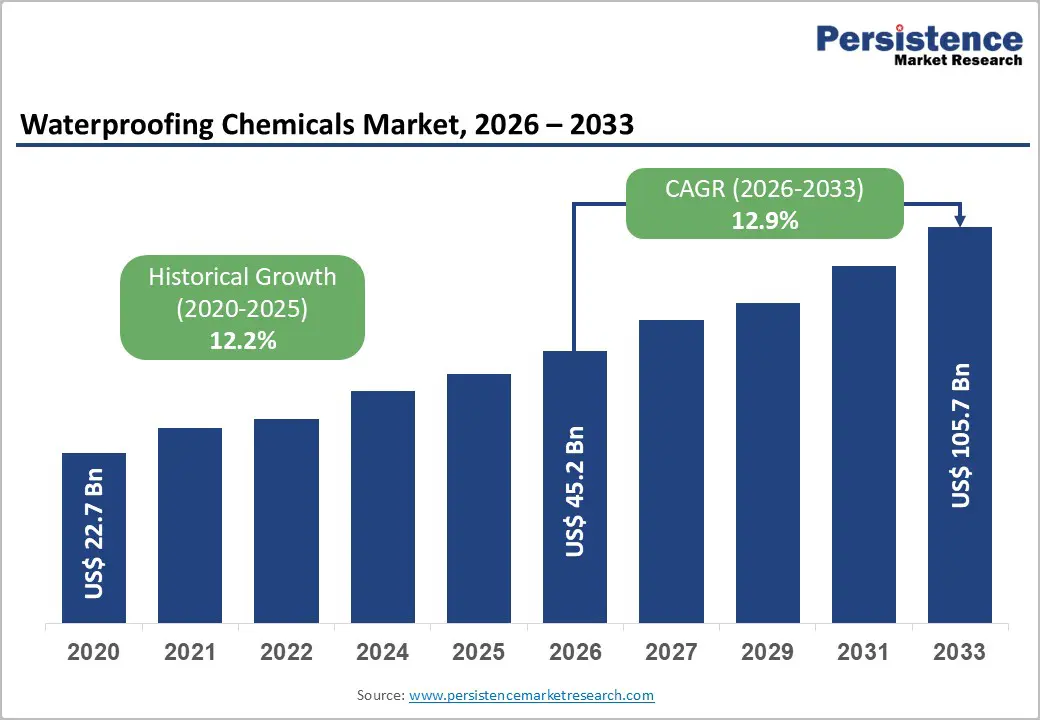

The global waterproofing chemicals market size is expected to be valued at US$ 45.2 billion in 2026 and projected to reach US$ 105.7 billion by 2033, growing at a CAGR of 12.9% between 2026 and 2033. This exceptional expansion is primarily driven by accelerating global construction activity, increasingly stringent building codes mandating waterproofing in new construction and renovation, and the growing urgency of climate-resilient infrastructure investment in the face of rising extreme weather events.

The market grew from US$ 22.7 billion in 2020 at a historical CAGR of 12.2%, underpinned by rapid urbanization in the Asia Pacific, infrastructure modernization in North America and Europe, and growing awareness of lifecycle cost benefits from waterproofing in construction projects across all regions.

Key Industry Highlights

- Leading Region: Asia Pacific leads with 37% market share in 2026, driven by China's massive construction output, India's PMAY and Smart Cities programs, and Southeast Asia's tropical climate, creating waterproofing demand across residential, commercial, and infrastructure construction segments.

- Fastest Growing Region: MEA is the fastest growing waterproofing chemicals region, with Saudi Arabia's Vision 2030 mega-projects, UAE's Net Zero 2050 green building drive, and AfDB's US$ 25 billion annual infrastructure investment collectively creating unprecedented demand for advanced waterproofing systems.

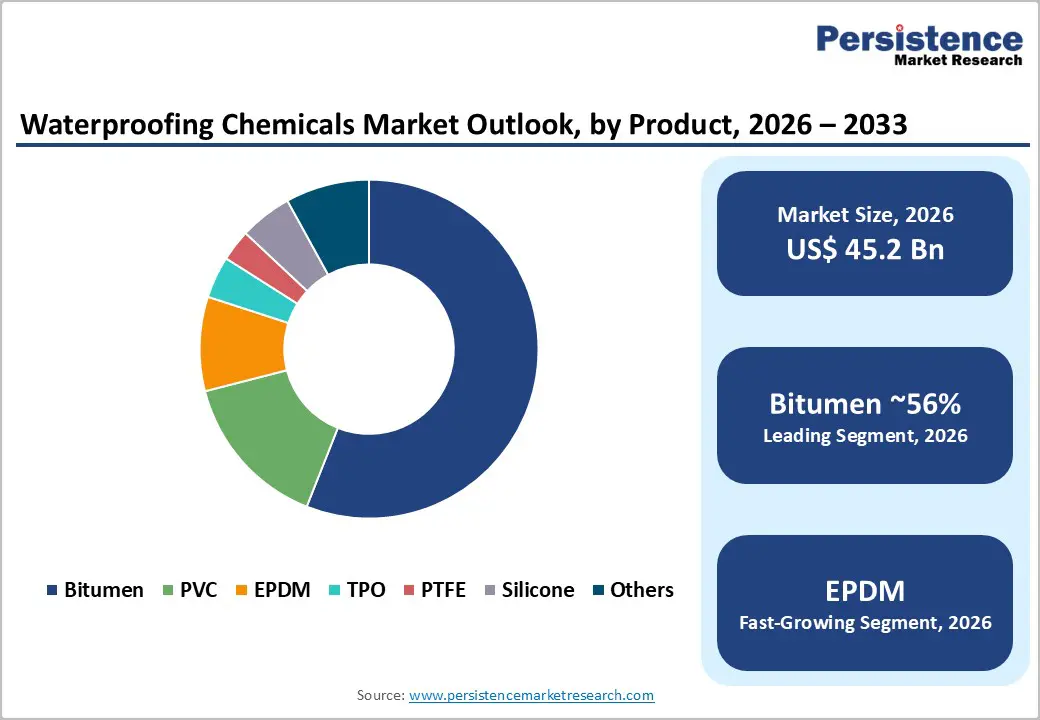

- Dominant Product Segment: Bitumen-based waterproofing products command 56% market share in 2026, anchored by their proven performance, cost-effectiveness, broad applicability across climates, and compatibility with torch-applied, self-adhered, and cold-applied installation methods in roofing and foundation applications.

- Fastest Growing Product Segment: EPDM membranes are the fastest growing product type at 14% CAGR (2026 - 2033), driven by 50+ year service life credentials, recyclability, compatibility with green roofing, and mandatory specification in LEED-certified and EU near-zero-energy buildings under EPBD recast mandates.

- Opportunity: The EU's target to retrofit 35 million buildings by 2030, combined with FEMA-driven flood-resilient construction mandates and IPCC-projected increases in extreme precipitation events, represents the highest-growth policy-driven demand opportunity for premium waterproofing systems globally.

DRO Analysis

Drivers - Rapid Urbanization and Expanding Global Construction Activity

The unprecedented scale of global urbanization is the foremost structural driver of waterproofing chemicals demand. According to the United Nations Department of Economic and Social Affairs (UN DESA), approximately 68% of the world's population is projected to live in urban areas by 2050, requiring massive investment in residential, commercial, and public infrastructure. The Global Infrastructure Hub, a G20 initiative, estimates that the world requires US$ 94 trillion in infrastructure investment through 2040 to meet current and projected needs.

Every new building, tunnel, bridge, and underground structure requires waterproofing solutions to protect structural integrity. India's Housing for All (PMAY) mission, targeting 20 million affordable homes, and China's continued urban housing expansion collectively create tens of billions of square meters of new waterproofed surface area annually, driving sustained primary demand growth.

Climate Change-Driven Demand for Building Envelope Protection and Flood Resilience

Intensifying climate-related events, including increased precipitation, flooding, and extreme temperature cycles, are compelling building owners, governments, and insurers to mandate higher standards of waterproofing in both new construction and existing building retrofit programs. The Intergovernmental Panel on Climate Change (IPCC) projects that extreme precipitation events will increase in frequency and intensity across most regions by mid-century.

In response, the European Union's Renovation Wave Strategy targets retrofitting 35 million buildings by 2030, with building envelope waterproofing being a core element. The U.S. Federal Emergency Management Agency (FEMA) has expanded flood-resilient construction guidelines that increasingly require waterproofing solutions in flood-prone zones, directly expanding the regulatory demand base for waterproofing chemicals across roofing, basement, and foundation applications.

Restraints - Volatile Raw Material Prices and Supply Chain Disruptions

The waterproofing chemicals industry is significantly exposed to petrochemical feedstock price volatility, as bitumen, PVC, TPO, and EPDM-based products all derive from petroleum-based precursors. Crude oil price fluctuations, which have varied by over 50% year-on-year in recent periods, directly impact production costs, compressing margins for manufacturers.

Supply chain disruptions witnessed during 2020-2022, including logistics bottlenecks and feedstock shortages, caused average selling price increases of 15-25% across multiple product categories, deterring demand from cost-sensitive construction segments and slowing project commencement in emerging markets where budget constraints are tightest.

Skilled Labor Shortages and Application Quality Variability

The performance of waterproofing systems is critically dependent on correct application, and the global construction industry faces an acute skilled labor shortage. The U.S. Bureau of Labor Statistics has consistently reported construction labor shortage rates of 300,000-400,000 unfilled positions annually in recent years.

Improper application of waterproofing membranes, including insufficient surface preparation, lap joint errors, and inadequate curing, is a leading cause of waterproofing failures that erode confidence in product performance, increase warranty claims, and slow specification of premium waterproofing systems among risk-averse developers and contractors.

Opportunities - EPDM Membranes Driven by Sustainability and Green Building Mandates will Provide Lucrative Growth Opportunities

EPDM (Ethylene Propylene Diene Monomer) rubber waterproofing membranes represent the fastest growing product segment at a projected CAGR of 14% (2026 - 2033), driven by their exceptional durability (50+ year service life), recyclability, and compatibility with green roofing systems. The U.S. Green Building Council (USGBC) reports that LEED-certified buildings increasingly specify EPDM for low-slope and cool roof applications due to its high solar reflectance and energy efficiency credentials.

The EU's Energy Performance of Buildings Directive (EPBD) recast mandating near-zero-energy buildings (NZEBs) is driving specification of high-performance, long-life waterproofing systems in both new construction and renovation. Manufacturers, including Carlisle Companies Inc. and Soprema Group are expanding EPDM product lines to capture this premium, sustainability-driven demand growth.

Middle East & Africa: Fastest Growing Region Through Mega-Infrastructure and Climate Adaptation Investment

The Middle East & Africa region presents the highest growth opportunity in the global waterproofing chemicals market over the forecast period, fueled by unprecedented infrastructure investment and climate adaptation urgency. Saudi Arabia's Vision 2030 includes NEOM, The Line, and other mega-projects collectively requiring millions of square meters of advanced waterproofing solutions for underground structures, tunnels, and infrastructure. The UAE's Net Zero 2050 Strategic Initiative is driving green building construction with high-performance waterproofing specifications.

In Africa, the African Development Bank (AfDB) is channeling US$ 25 billion annually into infrastructure development, with water management and flood-resilient construction being priority areas requiring waterproofing chemicals at scale. Regional market participants such as Fosroc International Ltd are actively expanding their MEA distribution and technical support networks to capitalize on this accelerating demand.

Category-wise Analysis

Product Type Insights

Bitumen-based waterproofing products dominate the product type segment with approximately 56% market share in 2026, reflecting their long-established track record, broad applicability, and cost-effectiveness across roofing, foundation, and underground waterproofing applications. Modified bitumen membranes, reinforced with SBS (Styrene-Butadiene-Styrene) or APP (Atactic Polypropylene) polymers, offer significantly improved flexibility, thermal resistance, and service life compared to traditional unmodified bitumen.

According to ASTM International standards widely referenced in construction specifications, bitumen membranes deliver proven moisture resistance in both hot and cold climates. Their compatibility with torch-applied, self-adhered, and cold-applied installation methods makes them the most versatile product type across varied construction environments globally, particularly in Asia Pacific and the Middle East where bitumen raw material supply chains are well-established.

Technology Insights

Preformed membrane systems hold the leading technology position, accounting for approximately 52% market share in 2026. Preformed membranes, encompassing bituminous, EPDM, PVC, and TPO sheet systems, are preferred in demanding commercial and industrial applications due to their consistent factory-controlled thickness, predictable performance characteristics, and suitability for third-party quality certification under standards including EN 13707 (European Standard for reinforced bitumen membranes) and ASTM D4637 (Standard for EPDM membranes).

Their use in flat and low-slope roofing, the dominant waterproofing application globally, is entrenched across North America, Europe, and increasingly Asia Pacific, where large commercial roofing projects regularly specify preformed membrane systems due to their long-term performance warranties of 20-30 years offered by leading manufacturers.

Application Insights

Roofing & walls represent the leading application segment, accounting for approximately 45% of total waterproofing chemicals market share in 2026. The global commercial and residential roofing market constitutes one of the largest surface areas requiring waterproofing protection, with tens of billions of square meters of roof area replaced or renovated globally each year. According to the National Roofing Contractors Association (NRCA), the U.S. commercial roofing market alone processes billions of square feet of waterproofing membrane annually.

Growing adoption of green roofs, mandated or incentivized in cities including Paris, Toronto, and Singapore, which require high-performance root-resistant waterproofing underlays, further reinforces roofing's position as the dominant application segment through the forecast period.

Regional Insights

Asia Pacific leads the global waterproofing chemicals market with approximately 37% market share in 2026, while Middle East & Africa (MEA) is the fastest growing region, projected to record the highest CAGR over 2026 - 2033, driven by mega-infrastructure projects, climate adaptation investment, and rapid urbanization across both sub-regions.

North America Waterproofing Chemicals Market Trends and Insights

North America is a mature, innovation-driven waterproofing chemicals market characterized by strong adoption of high-performance membranes and liquid-applied systems in commercial roofing, infrastructure renewal, and green building construction. The U.S. Infrastructure Investment and Jobs Act allocating US$ 1.2 trillion is driving significant waterproofing demand for bridges, tunnels, and water management infrastructure. Sustainability certifications and energy-efficient cool roofing specifications are elevating EPDM and TPO adoption.

U.S. Waterproofing Chemicals Market Size

The United States accounts for approximately 76% of North American waterproofing chemicals market revenue in 2026. Driven by aging infrastructure requiring waterproofing rehabilitation, active commercial construction, and LEED green building adoption, the U.S. market is the largest single national waterproofing market outside Asia. Leading players including GAF Materials Corporation, Carlisle Companies Inc., and GCP Applied Technologies, have strong domestic market positions.

Europe Waterproofing Chemicals Market Trends and Insights

Europe represents a technically advanced waterproofing chemicals market driven by rigorous building standards, ambitious building renovation programs, and a strong tradition of performance-specified membrane systems. The EU Renovation Wave Strategy targeting 35 million building retrofits by 2030 is a structural growth driver. Sustainability-certified waterproofing systems compliant with CE marking and ETA (European Technical Assessment) requirements dominate specifications across commercial and residential segments.

Germany Waterproofing Chemicals Market Size

Germany holds approximately 22% of the European waterproofing chemicals market in 2026. As Europe's largest construction economy, Germany's Gebäudeenergiegesetz (GEG) building energy law mandating high-performance building envelopes drives specification of advanced waterproofing systems. Companies including Sika AG, Schomburg GmbH & Co. KG, and Kemper System maintain strong domestic market presences serving both new construction and renovation applications.

U.K. Waterproofing Chemicals Market Size

The United Kingdom accounts for approximately 14% of European waterproofing chemicals market revenue in 2026. The UK Building Regulations Part C (Site Preparation and Resistance to Contaminants and Moisture) mandates waterproofing compliance in new construction. Active commercial roofing, basement waterproofing for urban development, and infrastructure waterproofing for HS2 tunnel construction sustain strong and growing market demand.

France Waterproofing Chemicals Market Size

France contributes approximately 12% of European waterproofing chemicals market revenue in 2026. France's RE2020 building standards for energy and environmental performance drive waterproofing specification upgrades in new construction. Paris's green roof mandate, requiring vegetated or solar roofs on new commercial buildings under Grenelle II law provisions, specifically drives demand for root-resistant, high-performance waterproofing membranes in the roofing application segment.

Asia Pacific Waterproofing Chemicals Market Trends and Insights

Asia Pacific leads global waterproofing chemicals consumption, driven by the unparalleled scale of construction activity in China, India, and Southeast Asia. China accounts for approximately 42% of the Asia Pacific demand, with its massive residential construction sector, including ongoing urban renewal programs replacing aging building stock, consuming enormous quantities of bitumen and polymer-modified waterproofing products. India and Southeast Asia are the fastest-growing sub-regional markets within Asia Pacific, driven by infrastructure investment programs and rapid urbanization.

India Waterproofing Chemicals Market Size

India represents approximately 18% of Asia Pacific waterproofing chemicals market revenue in 2026. The Pradhan Mantri Awas Yojana (PMAY) housing program, Smart Cities Mission infrastructure development, and large-scale commercial construction in metropolitan areas drive strong growth. Pidilite Industries Limited and Asian Paints Ltd. are key domestic market participants with extensive distribution networks serving both professional contractors and DIY consumers.

Japan Waterproofing Chemicals Market Size

Japan contributes approximately 9% of Asia Pacific waterproofing chemicals market revenue in 2026. Japan's seismically active geography and typhoon exposure drive stringent building waterproofing requirements in both residential and infrastructure construction. The country's aging building stock, with approximately 6 million buildings over 30 years old per Ministry of Land, Infrastructure, Transport and Tourism (MLIT) data, creates a substantial renovation-driven waterproofing demand base.

Southeast Asia Waterproofing Chemicals Market Size

Southeast Asia represents approximately 15% of Asia Pacific waterproofing chemicals market revenue in 2026. Indonesia, Vietnam, Thailand, and Malaysia are experiencing rapid construction growth driven by urbanization and infrastructure investment. High tropical rainfall and humidity, with annual precipitation exceeding 2,000-3,000 mm in major markets, makes waterproofing a critical and non-negotiable construction requirement, sustaining strong demand across residential, commercial, and infrastructure segments.

Competitive Landscape

The global waterproofing chemicals market exhibits a moderately consolidated competitive structure, with multinational chemical and construction materials companies including Sika AG, BASF SE, Mapei S.p.A., and Henkel AG & Co. KGaA competing alongside specialized regional players. Leading competitors differentiate through comprehensive product portfolios spanning all technology types, extensive technical support networks, and strong project specification relationships with architects, engineers, and building owners.

R&D investment is focused on sustainable formulations, including bio-based polymers and low VOC coatings, and digital application tools. Emerging trends include integrated waterproofing-plus-insulation systems and circular economy approaches enabling membrane recycling. Acquisitions and regional capacity expansion are primary inorganic growth strategies as players seek to capture Asia Pacific and MEA growth opportunities.

Key Developments

- In February 2025, Sika AG completed the expansion of its waterproofing production facility in India, increasing local manufacturing capacity for SikaTop and Sikalastic product lines to serve accelerating residential and infrastructure waterproofing demand across South Asia.

- In September 2024, BASF SE launched its next-generation MasterSeal waterproofing coating range formulated with reduced VOC content and enhanced UV stability, targeting green building certification requirements in commercial roofing and façade applications across European markets.

- In April 2023, Mapei S.p.A. inaugurated a new technical center in the UAE dedicated to waterproofing and construction chemicals R&D, reinforcing its strategic expansion in the Middle East market ahead of Saudi Arabia Vision 2030 construction activity acceleration.

Waterproofing Chemicals Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 22.7 Billion |

| Current Market Value (2026) | US$ 45.2 Billion |

| Projected Market Value (2033) | US$ 105.7 Billion |

| CAGR (2026 - 2033) | 12.9% |

| Leading Region | Asia Pacific, 37% market share (2025) |

| Dominant Category - Product Type | Bitumen-Based, 56% market share (2025) |

| Top-Ranking Category - Technology | Preformed Membrane, 52% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 60.5 Billion |

Companies Covered in Waterproofing Chemicals Market

- Sika AG

- BASF SE

- GCP Applied Technologies

- Mapei S.p.A.

- Fosroc International Ltd

- Pidilite Industries Limited

- RPM International Inc.

- Carlisle Companies Inc.

- W.R. Grace & Co.

- GAF Materials Corporation

- Soprema Group

- Kemper System

- Schomburg GmbH & Co. KG

- Henkel AG & Co. KGaA

- Asian Paints Ltd.

Frequently Asked Questions

The global waterproofing chemicals market is projected to reach US$ 45.2 billion in 2026, up from US$ 22.7 billion in 2020. The market is forecast to expand further to US$ 105.7 billion by 2033, growing at a CAGR of 12.9%.

Key demand drivers include rapid global urbanization, with UN DESA projecting 68% urban population by 2050, requiring US$ 94 trillion in global infrastructure investment per the Global Infrastructure Hub.

Asia Pacific leads with approximately 37% market share in 2026, anchored by China's massive urban construction activity, accounting for 42% of Asia Pacific demand, and India's government-backed housing programs including PMAY targeting 20 million homes.

The greatest opportunity lies in EPDM membranes, the fastest growing product type at 14% CAGR through 2033, driven by green building mandates and LEED certification requirements.

Leading companies include Sika AG, BASF SE, Mapei S.p.A., Henkel AG & Co. KGaA, GCP Applied Technologies, Fosroc International Ltd, Carlisle Companies Inc., GAF Materials Corporation, Soprema Group, RPM International Inc., Pidilite Industries Limited, and Asian Paints Ltd..