- Biotechnology

- Cell Therapy Bioprocessing Market

Cell Therapy Bioprocessing Market Size, Share and Growth Forecast, 2026 - 2033

Cell Therapy Bioprocessing Market by Technology (Bioreactor, Centrifugation, Ultrasonic Lysis, Lyophilization, Genome Editing, Others), Indication (CVD, Oncology, Wound Healing, Orthopedic, Others), End User (Hospitals, Clinics, Diagnostic Centers, Regenerative Centers, Research Institutes), and Regional Analysis for 2026 - 2033

Cell Therapy Bioprocessing Market Share and Trends Analysis

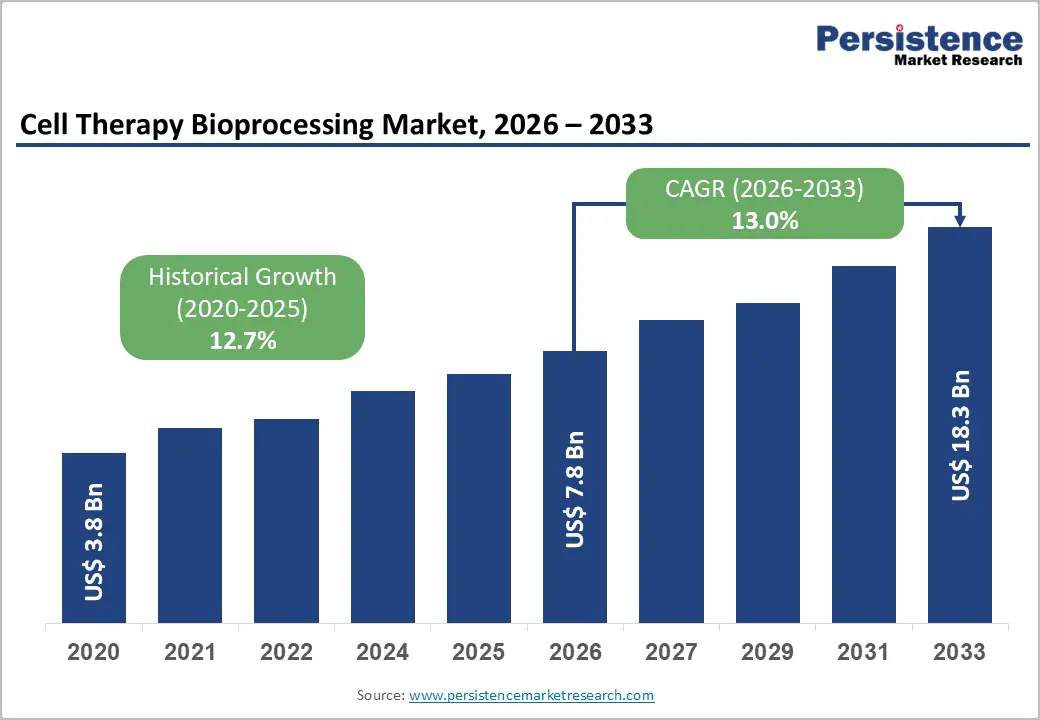

The global cell therapy bioprocessing market size is likely to be valued at US$ 7.8 billion in 2026 and is projected to reach US$18.3 billion by 2033, growing at a CAGR of 13% during the forecast period 2026-2033.

The market is growing due to increasing demand for advanced regenerative therapies driven by the high prevalence of chronic and genetic diseases. Industry trends toward personalized medicine and automated, scalable bioprocessing platforms are accelerating adoption, as these technologies improve product consistency, safety, and yield.

Key advantages, such as rapid cell expansion, closed-system processing, and efficient viral vector production, enhance therapeutic efficacy and reduce manufacturing risks. Additionally, the expansion of oncology, cardiovascular, and orthopedic treatment applications, coupled with emerging market growth, urbanization, and rising disposable incomes, is broadening patient access and driving global market expansion.

Key Industry Highlights

- Dominant Technologies: Bioreactors are set to lead with an estimated 30% revenue share in 2026, while genome editing is likely to be the fastest-growing, driven by rising demand for CAR-T and gene-modified therapies.

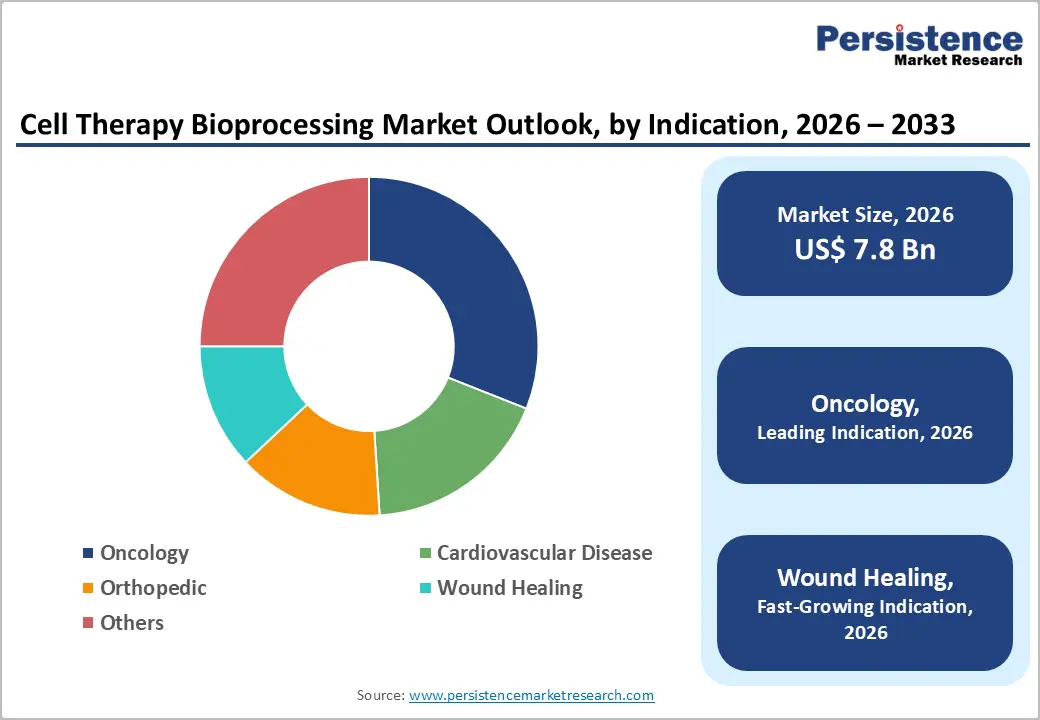

- Leading Indications: Oncology is expected to hold around 31% share in 2026, while wound healing is projected to be the fastest-growing segment, reflecting expanding adoption of regenerative therapies.

- Leading End Users: Research institutes are set to lead with 34% in 2026, while hospitals are likely the fastest-growing end users as on-site processing and clinical adoption increase.

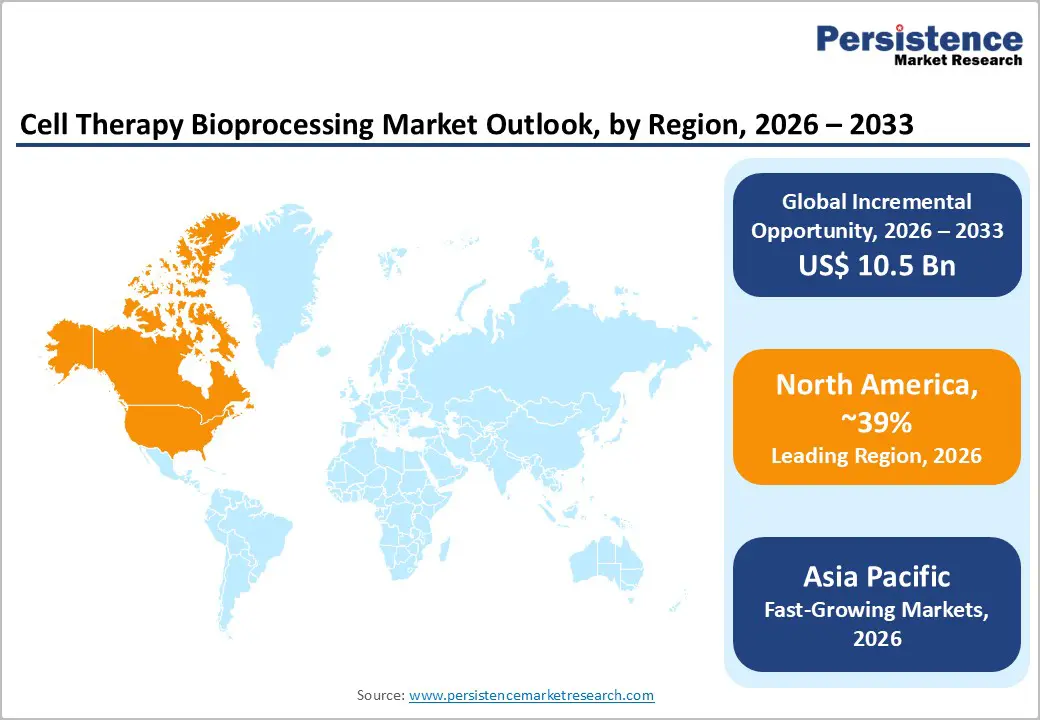

- Regional Leadership: North America is poised to dominate with 39% share in 2026; Asia Pacific is expected to register the fastest growth, driven by emerging market expansion and healthcare infrastructure development.

- Competitive Environment: Market growth is shaped by automation adoption, strategic partnerships, and global expansion, focusing on high-growth regions in the Asia Pacific and Europe.

| Key Insights | Details |

|---|---|

| Cell Therapy Bioprocessing Market Size (2026E) | US$ 7.8 Bn |

| Market Value Forecast (2033F) | US$ 18.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.7% |

DRO Analysis

Driver - Expansion of Cell Therapy Pipelines and Commercialization

The global ecosystem for advanced cell therapies, especially CAR-T, TCR-T, and allogeneic treatments, continues to deepen as more candidates progress through late-stage clinical evaluation toward market entry. Manufacturers are prioritizing scalable bioprocessing platforms that preserve product quality at commercial volumes while adhering to stringent quality standards. This shift heightens demand for bioreactors, viral vector production systems, and integrated automation to support robust throughput and reproducible outcomes. Commercialization momentum is also catalyzing investment in facility expansion and GMP-compliant infrastructure, creating a stronger pipeline-to-market pathway for complex therapies.

Supporting this trend, global biopharma firms and emerging players are expanding manufacturing capabilities to meet rising therapeutic demand. For example, Bharat Biotech established Nucelion Therapeutics in late 2025 to provide scalable process development and manufacturing services for advanced cell and gene therapies, in line with international regulatory standards, underscoring real-world expansion in production capacity. Additionally, FDA engagement on manufacturing approaches for novel therapies, such as feedback supporting scalable production systems for a tumor-targeting therapy’s clinical filing, reflects constructive regulatory interaction that smooths commercialization pathways.

Technological Advancements and Strategic Collaborations

Continuous innovation in automation, real-time bioprocess monitoring, closed processing systems, and single-use technologies is reshaping the cell therapy manufacturing landscape. These advancements streamline workflows, reduce contamination risks, and enable consistent, high-quality production outcomes from early development through commercial scale. Automated platforms that integrate steps such as cell isolation, expansion, and formulation provide the operational efficiency needed to manage complex, biologically sensitive processes without extensive manual intervention. These capabilities enhance consistency, reduce risk, and improve yield quality, all critical to meeting regulatory expectations.

The strategic collaborations and partnerships are accelerating technology adoption and addressing key manufacturing bottlenecks. In 2025, industry partnerships, such as technology alliances that improve gene-delivery efficiency and streamline cell-engineering workflows, illustrated how stakeholders are tackling core scalability and cost challenges. Further evidence of industry alignment is seen in regional distributor partnerships that expand access to high-quality, cGMP-compliant media and bioprocessing solutions into major markets such as China, broadening the practical adoption of advanced manufacturing platforms. These cooperative movements underscore how shared innovation and expanded technology access are enabling market growth beyond traditional research settings and into commercial manufacturing.

Restraint - High Capital and Operational Costs

Cell therapy bioprocessing requires substantial investment in specialized equipment, including bioreactors, viral vector production systems, and closed-system automation platforms. Establishing GMP-compliant facilities demands high upfront capital, which is prohibitive for smaller firms and emerging-market players. In addition, hiring and training skilled personnel adds to operational expenditure. The complexity of maintaining advanced systems increases both maintenance and consumable costs. High capital requirements limit the adoption of scalable manufacturing solutions. Consequently, the cost structure creates barriers to wider market penetration. These financial barriers also hinder rapid expansion into new geographic markets.

These elevated expenses also increase the final price of therapies, limiting access in cost-sensitive regions. CAR-T treatments, for example, continue to exceed half a million dollars per patient in 2026, including hospitalization and supportive care costs. Small and mid-sized developers may defer investment due to insufficient financial resources. High operating costs reduce potential return on investment for new market entrants. The financial burden may slow infrastructure expansion. This challenge remains a major constraint to industry growth. Rising global demand further emphasizes the need for cost-efficient production solutions.

Complex Regulatory and Quality Compliance Requirements

Cell therapy manufacturing is regulated by strict frameworks to ensure patient safety and therapeutic efficacy. Requirements vary across regions for viral vector handling, sterility, and genetically modified cells, complicating approvals. Extensive validation, quality audits, and documentation are mandatory before clinical or commercial deployment. Compliance increases operational costs and extends production timelines. Firms must invest in monitoring systems and trained quality teams. The regulatory burden can slow the scaling of advanced manufacturing processes. Managing evolving international standards adds further operational challenges and uncertainty.

Regulatory uncertainty remains a significant challenge. In early 2026, stakeholders highlighted inconsistencies in FDA approvals for rare disease therapies, with additional clinical requirements delaying product entry. These variations increase the cost of compliance and reduce flexibility in manufacturing. Firms must navigate overlapping regional standards, prolonging time to market. Operational bottlenecks and higher overhead deter investment in novel therapies. Such regulatory constraints continue to restrain market expansion and commercialization. Clearer regulatory guidance could mitigate delays, but it remains limited in some regions.

Opportunities - Growth in Emerging Therapeutic Indications and Strategic Innovation

Cell therapies are expanding into high-value non-oncology areas such as cardiovascular disease, wound healing, orthopedics, and rare genetic disorders, generating demand for diversified bioprocessing platforms that support complex manufacturing needs. These emerging indications create new revenue streams as developers require scalable systems capable of handling diverse cell types, tailored quality controls, and specialized production workflows. This therapeutic diversification elevates clinical relevance and market potential for advanced bioprocessing ecosystems. Advancing these areas enhances long-term growth prospects as patient populations expand and unmet medical needs persist.

In 2026, regulatory developments, such as the U.S. FDA’s increased flexibility on cell and gene therapy requirements, have reduced certain barriers to innovation, enabling developers to pursue broader therapeutic targets with streamlined compliance procedures. This regulatory adjustment supports faster advancement of new modalities, encouraging investment in platforms that address evolving clinical needs across indications. As a result, bioprocessing technologies with adaptability and throughput advantages are better positioned to capture opportunities in growing therapeutic segments and drive future industry expansion.

Regional Expansion, Investment Momentum and Digital Innovation Platforms

The Asia Pacific region is emerging as a dynamic growth market for cell therapies and bioprocessing infrastructure, supported by government initiatives to attract biotech investment and foster local manufacturing ecosystems. For example, AstraZeneca announced plans to build a dedicated cell therapy manufacturing base and innovation center in Shanghai, reflecting increased pharma investment to develop end-to-end capabilities in key Asian markets and accelerate regional access. These developments expand infrastructure, deepen technical expertise, and drive competitive differentiation for bioprocessing technologies.

In addition, major biopharma players are making substantial innovation-oriented investments, such as Johnson & Johnson’s US$ 1 billion facility in Pennsylvania to support future manufacturing capacity and bolster advanced therapy production capabilities. Such capital commitments signal confidence in long-term demand for next-generation therapies and support ecosystem expansion. Concurrently, biotechnology hubs such as Hyderabad’s BioAsia initiative highlight the public sector's emphasis on moving from manufacturing to innovation, with significant investment pledges. Combined with rising adoption of digital process monitoring, AI-enabled platforms, and automation integration, these trends position the market to leverage innovation-driven efficiencies and broaden adoption across regions.

Category-wise Analysis

Technology Insights

Bioreactor technologies are set to remain the dominant technology in cell therapy bioprocessing, with an estimated 30% market share in 2026, owing to their broad application in cell expansion, culture, and large-scale production. Single-use, automated, and scalable systems reduce contamination risk and streamline workflows, supporting higher throughput with reproducible quality. Manufacturers are integrating real-time monitoring and closed systems for enhanced control and regulatory compliance. In 2026, Cellares secured $257 M in Series D funding to build Smart Factories with automated bioreactor platforms capable of supporting hundreds of thousands of treatments annually. This investment underscores industry confidence in scalable, GMP-compliant bioreactor manufacturing for complex commercial therapies. Adoption is also driven by increasing clinical and commercial demand, making bioreactors central to modern cell therapy infrastructure.

Genome editing is poised for rapid expansion, driven by engineered therapies such as CAR T and TCR T that require precise genetic modification and specialized infrastructure. CRISPR-based editing and viral delivery platforms enable customization and high therapeutic efficacy across multiple indications. In December 2025, the FDA approved Waskyra for Wiskott-Aldrich syndrome, the first gene therapy of its kind, signaling regulatory confidence and accelerating clinical adoption. This milestone underscores the importance of advanced bioprocessing infrastructure to ensure the safe and reproducible delivery of gene-edited therapies at scale. Investment in automated, high-throughput vector production facilities is increasing, as biopharma seeks to meet rising global demand. These technologies are also enabling innovation in next-generation therapies, strengthening their strategic relevance.

Indication Insights

Oncology is expected to continue to lead with an estimated 31% share in 2026, supported by multiple CAR T approvals and a growing pipeline of cancer cell therapies. High levels of R&D and clinical validation drive strong demand for reliable, reproducible bioprocessing solutions that meet stringent regulatory standards. FDA approval of Waskyra reinforced confidence in complex cell and gene therapies, highlighting the importance of advanced manufacturing platforms in oncology. Automated, high-throughput production facilities are increasingly deployed to ensure consistent quality, reduce human error, and improve efficiency. The oncology segment also benefits from sustained investment in innovation, including next-generation immune cell therapies and personalized medicine approaches. Growing global cancer incidence and focus on novel immunotherapies continue to drive adoption and revenue leadership.

Wound healing is emerging as a high-growth area, driven by rising demand for regenerative solutions and tissue repair as populations age. These applications require specialized bioprocessing workflows, including precise cell preparation, tissue scaffolding, and functional quality control. In 2026, advanced stem-cell-derived tissue platforms were developed to improve skin regeneration and musculoskeletal repair, reflecting industry focus on non-oncology regenerative applications.

Expanding clinical trials, supportive regulatory guidance, and growing healthcare infrastructure amplify the potential for adoption. Investment in scalable and automated manufacturing platforms enhances reproducibility, lowers operational risk, and accelerates commercial readiness. Combined with rising global awareness of regenerative medicine benefits, these segments are poised for rapid market penetration.

Regional Insights

North America Cell Therapy Bioprocessing Market Trends

North America is expected to maintain its position as the largest market, with an estimated 38-40% share in 2026, driven by strong R&D ecosystems, extensive clinical trial activity, and mature healthcare infrastructure. Regulatory clarity from the U.S. FDA supports advanced therapy manufacturing, encouraging innovation in bioprocessing platforms and high-throughput production. Investment in automation, closed systems, and GMP-compliant facilities continues to expand, supporting both clinical and commercial-scale therapies. High disease prevalence, strong public and private funding, and a dense network of biotech and pharmaceutical players further reinforce leadership.

BlueRock Therapeutics opened a new state-of-the-art cell therapy manufacturing facility in Massachusetts, designed to scale autologous and allogeneic products while integrating advanced automated processing systems. Additionally, Atara Biotherapeutics partnered with Northwell Health in 2026 to co-develop a regenerative medicine manufacturing site in New York, focusing on T-cell therapies for hematological conditions. These initiatives illustrate the region’s continued strategic investment in capacity, innovation, and collaborative networks, solidifying North America’s leadership in cell therapy bioprocessing.

Europe Cell Therapy Bioprocessing Market Trends

Europe remains a key region in the global cell therapy bioprocessing market, supported by harmonized regulatory frameworks and active public-sector engagement in advanced therapy development. The European Medicines Agency (EMA) and the European Commission maintain a joint Action Plan for advanced therapy medicinal products (ATMPs) to streamline regulatory procedures, harmonize quality standards, and foster competitiveness for cell and gene therapy manufacturers. This regulatory infrastructure enhances predictability for clinical development and manufacturing, encouraging investments in automated processing and robust quality systems across European biotech clusters. Collaborative networks across Germany, the U.K., France, and Spain further strengthen the region’s capacity for clinical translation and commercial readiness.

Several noteworthy developments highlighted Europe’s forward momentum. The Annual ATMP Development & Manufacturing Conference in Vienna (April 2026) focused on practical strategies for scaling GMP manufacturing, automation integration, and technology transfer from lab to large-scale production, reinforcing the region’s role as a hub for bioprocess innovation and knowledge exchange.

Additionally, the Advanced Therapies Europe Investment Summit 2026 has been positioned as a key platform connecting European biotech innovators with strategic investors and partners, accelerating capital flows into bioprocessing infrastructure and next-generation cell therapy programs. These initiatives demonstrate Europe’s commitment to aligning regulatory support, manufacturing excellence, and strategic investment to advance the cell therapy value chain.

Asia Pacific Cell Therapy Bioprocessing Market Trends

Asia Pacific is projected to be the fastest-growing region for cell therapy bioprocessing, driven by expanding healthcare investment, rising clinical activity, and growing government support. China, Japan, South Korea, India, and Southeast Asian nations are increasing capacity through regulatory facilitation and strategic funding, making the region attractive for both domestic developers and multinational biopharma players.

Lower manufacturing costs and the ability to scale capacity appeal to companies seeking cost-efficient, high-quality production bases outside traditional markets. Broadening patient population and strong commitments to innovation further expand long-term demand for advanced therapies and associated bioprocessing infrastructure.

Cell Therapies and ENCell signed an APAC strategic partnership in late 2025 to expand GMP manufacturing and process development across Korea, Australia, and broader Asia-Pacific markets, a move aimed at accelerating access to next-generation cell and gene therapies. Additionally, the Asia Pacific Cell & Gene Therapy Excellence Awards 2026 and Cell & Gene Therapy World Asia 2026 events spotlighted regional innovation leaders and manufacturing readiness strategies, reflecting growing investment and collaboration in scalable production platforms. These initiatives demonstrate Asia Pacific’s rapid evolution into a dynamic hub for cell therapy bioprocessing innovation and capacity-building.

Competitive Landscape

The global cell therapy bioprocessing market is moderately consolidated, with key players such as Lonza, Miltenyi Biotec, Thermo Fisher Scientific, GE Healthcare, and Sartorius holding a substantial market presence. These companies leverage deep expertise across bioreactors, viral vector production, and automation platforms, while maintaining robust regulatory compliance and quality standards. Heavy investment in R&D enables technological leadership in scalable manufacturing, closed systems, and digital process monitoring, ensuring reproducibility and efficiency in commercial and clinical-scale cell therapy production.

Smaller and regional competitors, including Cellares, Cellgenix, and Hitachi Chemical, focus on niche applications such as autologous cell therapies, genome editing, and emerging therapeutic indications. High capital requirements, GMP compliance, and complex integration remain barriers for new entrants, but the rise of digital platforms and automation solutions enables participation through real-time monitoring, analytics, and process optimization. Strategic acquisitions, partnerships, and technology collaborations continue to shape competitive dynamics, allowing market leaders to expand capabilities and geographic reach while supporting innovation across specialized segments.

Key Developments:

- In May 2025, BMS announced a $40 billion investment to expand R&D, manufacturing, and AI-driven operations, enhancing domestic cell therapy production and advanced bioprocessing infrastructure.

- In March 2025, Astellas and Yaskawa established Cellafa Bioscience to integrate robotic automation into cell therapy manufacturing, improving precision, scalability, and technology access for startups and academic institutions.

Companies Covered in Cell Therapy Bioprocessing Market

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Danaher Corporation

- Sartorius Stedim Biotech

- Lonza Group AG

- Charles River Laboratories

- STEMCELL Technologies

- PromoCell GmbH

- RoosterBio, Inc.

- Bio techne Corporation

Frequently Asked Questions

The cell therapy bioprocessing market is projected to reach US$ 7.8 billion in 2026.

Rising clinical pipelines, automation adoption, and growing therapy approvals drive the market.

The cell therapy bioprocessing market is expected to grow steadily from 2026 to 2033.

Expansion in emerging indications and Asia Pacific offer significant growth potential.

Top companies include Lonza, Miltenyi Biotec, Thermo Fisher Scientific, GE Healthcare, and Sartorius.