- Biotechnology

- Cell Harvesting System Market

Cell Harvesting System Market Size, Share and Growth Forecast, 2026 - 2033

Cell Harvesting System Market by Product (Manual Cell Harvesters, Automated Cell Harvesters), Application (Biopharmaceutical Application, Cell Therapy, Others), End-user (Hospitals, Biotech & Biopharma Companies), and Regional Analysis for 2026 - 2033

Cell Harvesting System Market Share and Trends Analysis

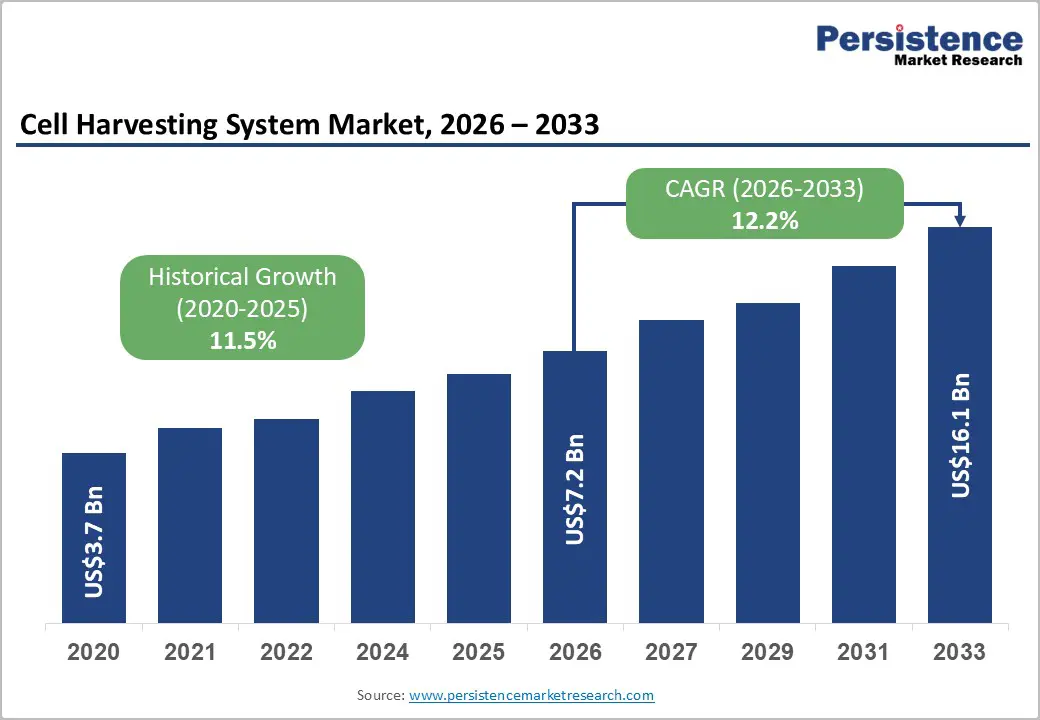

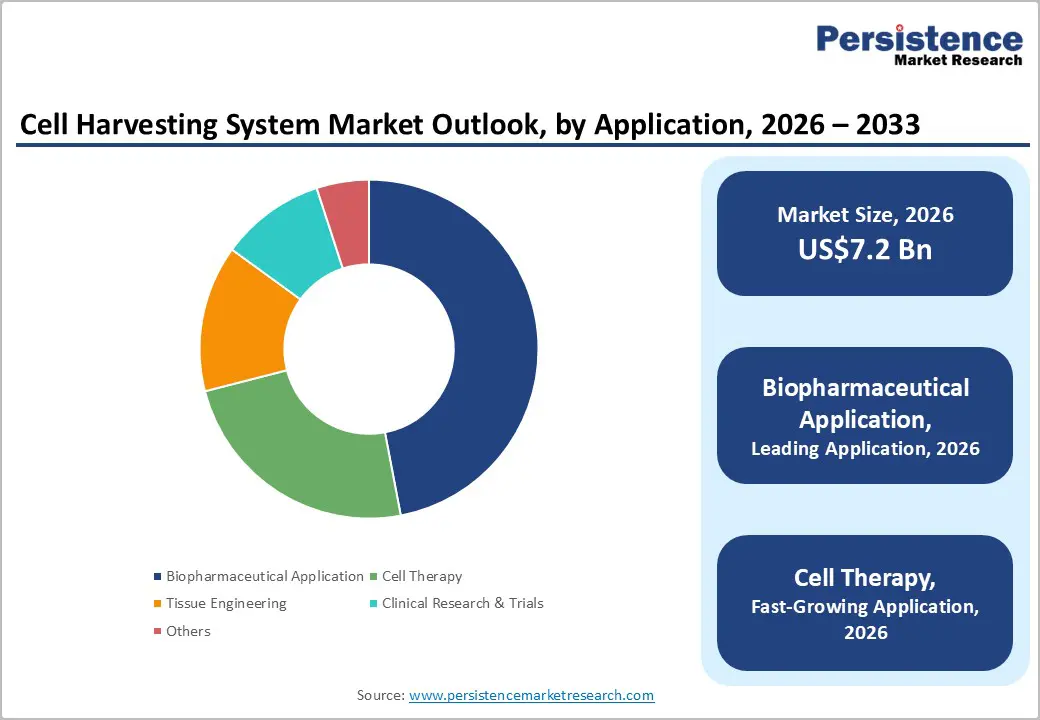

The global cell harvesting system market size is likely to be valued at US$7.2 billion in 2026 and is projected to reach US$16.1 billion by 2033, growing at a CAGR of 12.2% during the forecast period from 2026 to 2033, driven by the rising commercialization of cell therapy products, increasing biologics production capacity, and the transition toward automated closed-system bioprocessing workflows.

Regulatory emphasis on contamination control and process standardization is accelerating investments in advanced cell harvesting systems among biotech companies and hospitals. In parallel, expanding clinical pipelines for CAR-T therapy, stem cell therapy, and gene-modified biologics are strengthening long-term market demand.

Key Industry Highlights:

- Dominant Product Type: Automated cell harvesters are set to command around 64% of the revenue share in 2026, while manual cell harvesters continue to support small-scale research and pilot-stage bioprocessing applications due to lower operational costs.

- Leading Application: Biopharmaceutical applications are expected to lead with nearly a 47% share in 2026, while cell therapy is likely to register the fastest growth through 2033, supported by expanding CAR-T therapy commercialization and regenerative medicine investments.

- Dominant End-user: Biotech & biopharma companies are anticipated to account for approximately 61% of market revenue in 2026, whereas hospitals are projected to emerge as the fastest-growing end-user segment owing to rising adoption of clinical cell therapy procedures.

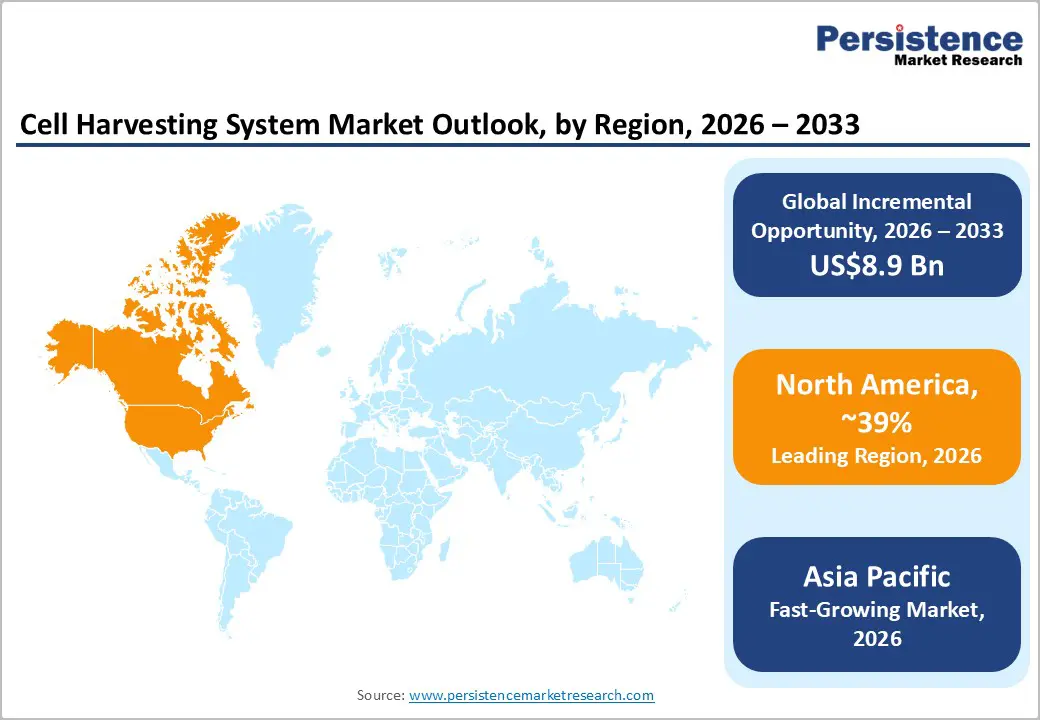

- Regional Leadership: North America is poised to dominate with an estimated 39% share in 2026, while Asia Pacific is expected to register the fastest growth through 2033, driven by expanding biopharmaceutical manufacturing investments and favorable regulatory reforms.

- Competitive Environment: Competitive dynamics include investments in automated closed-system bioprocessing technologies, expansion of regenerative medicine manufacturing facilities, strategic collaborations, and development of advanced contamination control solutions.

DRO Analysis

Driver - Rising Commercialization of Cell and Gene Therapies Accelerating Demand for Automated Cell Harvesting Systems

The rapid expansion of the global cell and gene therapy industry is significantly increasing demand for advanced cell harvesting technologies. According to the U.S. Food and Drug Administration (FDA), the agency expects to approve dozens of cell and gene therapies annually by the end of the decade, supported by a growing regenerative medicine pipeline. Data from the Alliance for Regenerative Medicine shows that more than 2,000 regenerative medicine clinical trials are currently active worldwide, with oncology-focused therapies accounting for a major share.

Automated cell harvesting systems are increasingly preferred due to their ability to reduce manual intervention, improve reproducibility, and support compliance with Good Manufacturing Practice (GMP) standards. Biopharmaceutical manufacturers are integrating closed-loop harvesting platforms into large-scale production workflows to improve efficiency and minimize contamination risk, particularly across North America and Europe, where ATMP manufacturing facilities continue to expand.

Restraint - High Capital Costs and Complex Validation Requirements Limiting Market Penetration

The adoption of advanced cell harvesting systems remains limited by high equipment costs and stringent validation requirements. Automated harvesting platforms require substantial investments in sterile processing infrastructure, integrated software systems, and skilled operator training. Small and mid-sized biotechnology companies often face financial constraints when scaling manufacturing operations, particularly during early-stage commercialization.

Regulatory compliance further increases operational complexity, as cell harvesting systems must meet GMP standards, sterility validation protocols, and process traceability requirements established by agencies such as the FDA and the European Medicines Agency (EMA). Validation procedures can prolong deployment timelines and increase implementation costs. In addition, customization requirements for different cell types and biologic products create interoperability challenges, particularly in emerging markets where bioprocessing infrastructure and technical expertise remain limited.

Opportunity - Expansion of Biopharmaceutical Manufacturing Capacity Creating New Revenue Opportunities

The global expansion of biologics manufacturing facilities is creating significant opportunities for cell harvesting system providers. Governments and private investors are increasing funding for domestic biopharmaceutical production to strengthen healthcare supply chain resilience. According to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), more than 12,700 medicines are currently under development globally, with biologics and advanced therapies representing a growing share of pipelines across oncology, immunology, and rare disease treatments.

Emerging markets in Asia Pacific are becoming attractive investment hubs due to lower manufacturing costs, supportive regulatory reforms, and expanding biotechnology ecosystems. Countries such as China, India, Singapore, and South Korea are investing heavily in biomanufacturing infrastructure and cell therapy facilities, increasing demand for scalable automated harvesting solutions. Advancements in single-use bioprocessing systems and AI-enabled monitoring technologies are also creating opportunities for next-generation harvesting platforms with enhanced process efficiency and contamination control.

Category-wise Analysis

Product Insights

Automated cell harvesters are projected to dominate the market with nearly a 64% share in 2026 and are expected to grow at a CAGR of 12.8% through 2033. Rising commercialization of CAR-T therapies, stem cell therapies, and biologics manufacturing is accelerating adoption of automated closed-system technologies due to improved sterility control, scalability, and batch consistency. Companies such as Thermo Fisher Scientific and Sartorius are expanding automated bioprocessing portfolios, while AI-enabled monitoring and single-use systems continue to strengthen demand.

Manual cell harvesters continue to maintain relevance across research laboratories, academic institutions, and pilot-scale therapeutic production settings due to lower capital costs and operational flexibility. However, the segment is witnessing slower growth as regulatory focus on contamination control and scalable manufacturing increasingly encourages end users to shift toward automated harvesting platforms.

Application Insights

Biopharmaceutical applications are expected to account for approximately 47% of global market revenue in 2026, supported by rising production of monoclonal antibodies, recombinant proteins, vaccines, and biosimilars. Pharmaceutical companies are expanding biologics manufacturing infrastructure globally to improve production efficiency and meet growing demand for precision therapeutics and advanced biologic drugs.

Cell therapy is projected to emerge as the fastest-growing application segment, registering an estimated CAGR of 12.5% through 2033. Increasing approvals for advanced therapy medicinal products (ATMPs), growing regenerative medicine research, and expanding CAR-T therapy pipelines are accelerating demand for high-precision harvesting systems capable of preserving cell integrity and viability.

End-user Insights

Biotech & biopharma companies are anticipated to hold nearly 61% of global market revenue in 2026, driven by rising investments in biologics production, regenerative medicine, and commercial-scale cell therapy manufacturing. Expansion of contract development and manufacturing organizations (CDMOs) and increasing adoption of automated bioprocessing technologies are further strengthening segment growth.

Hospitals are expected to register the fastest growth during the forecast period, expanding at an estimated CAGR of 12.9% through 2033. Increasing use of cell therapy procedures in oncology, hematology, and orthopedic treatments is encouraging hospitals to establish dedicated regenerative medicine and cell processing facilities, particularly across advanced healthcare systems.

Regional Analysis

North America Cell Harvesting System Market Trends

North America is expected to account for nearly 39% of the global cell harvesting system market share in 2026, driven by advanced biologics manufacturing infrastructure, rising cell therapy approvals, and increasing adoption of automated bioprocessing technologies. The region benefits from strong healthcare investments, established GMP-compliant production facilities, and growing collaboration between biotechnology firms and research institutions. Increasing investments in regenerative medicine and single-use bioprocessing systems continue to strengthen regional market expansion.

U.S. Cell Harvesting System Market Trends

The U.S. is projected to contribute approximately 82% of the North America market share, supported by its leadership in biologics manufacturing and regenerative medicine commercialization. The FDA has stated that it expects to approve nearly 10 to 20 cell and gene therapies annually, accelerating demand for automated harvesting platforms and scalable GMP-compliant manufacturing systems. In addition, recent manufacturing expansions by companies such as Thermo Fisher Scientific and Cytiva are further strengthening the country’s advanced bioprocessing ecosystem.

Canada Cell Harvesting System Market Trends

Canada is estimated to account for nearly 18% of the regional market share in 2026, driven by increasing investments in stem cell research and translational medicine infrastructure. The country invested more than US$1.5 billion through healthcare innovation and regenerative medicine initiatives, while collaborations between universities and biotechnology companies continue to strengthen domestic cell therapy research capabilities. Rising adoption of automated bioprocessing technologies across academic medical centers and contract manufacturing facilities is also supporting market growth.

Europe Cell Harvesting System Market Trends

Europe represents a significant share of the global cell harvesting system market, supported by expanding ATMP development, harmonized regulatory frameworks, and increasing investments in biologics manufacturing. The region continues to witness strong adoption of automation technologies and regenerative medicine solutions, particularly across Germany, the U.K., France, and Spain. Regulatory support from the European Medicines Agency (EMA) is further encouraging the expansion of advanced therapy manufacturing capabilities across the region.

Germany Cell Harvesting System Market Trends

Germany is expected to account for approximately 27% of the Europe market share in 2026, supported by its strong bioprocess engineering sector and leadership in laboratory automation technologies. Companies such as Sartorius AG and Merck KGaA are expanding automated bioprocessing and life sciences manufacturing facilities to improve contamination control, manufacturing efficiency, and biologics production scalability. Continued investments in regenerative medicine infrastructure and biotechnology research programs are further strengthening market demand.

U.K. Cell Harvesting System Market Trends

U.K. is projected to hold around 23% of the regional market, driven by strong cell therapy commercialization activity and translational medicine research. The country has emerged as a major CAR-T therapy development hub through initiatives such as the Cell and Gene Therapy Catapult program, while increasing NHS adoption of advanced therapies continues to support demand for automated harvesting technologies. Expansion of commercial-scale ATMP manufacturing centers is also accelerating market growth.

Asia Pacific Cell Harvesting System Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing regional market during the forecast period, supported by expanding biopharmaceutical manufacturing capacity, lower operational costs, and increasing government investments in biotechnology infrastructure. Rising clinical trial activity, favorable regulatory reforms, and rapid growth in biosimilar production are encouraging global manufacturers to establish regional production facilities. The region is also benefiting from expanding contract manufacturing and regenerative medicine research activities.

China Cell Harvesting System Market Trends

China is expected to contribute nearly 38% of the Asia Pacific market, supported by aggressive investments in biologics manufacturing and regenerative medicine research. The country accounted for more than 30% of global cell therapy clinical trials in recent years, supported by government-backed expansion of large-scale biomanufacturing parks and domestic biologics production facilities. This rapid industrial expansion is significantly increasing demand for automated harvesting systems and scalable bioprocessing technologies.

Japan Cell Harvesting System Market Trends

Japan is projected to account for approximately 19% of the regional market, driven by its leadership in stem cell research and regenerative medicine commercialization. The Pharmaceuticals and Medical Devices Agency (PMDA) introduced accelerated approval pathways for regenerative medicine products under the Regenerative Medicine Promotion Act, encouraging wider adoption of automated bioprocessing technologies across biotechnology companies and healthcare institutions. Increasing investments in precision medicine and research collaborations continue to strengthen Japan’s role in advanced therapy manufacturing.

Competitive Landscape

The global cell harvesting system market is moderately consolidated, with leading companies such as Thermo Fisher Scientific, Sartorius AG, Danaher Corporation (Cytiva), and Merck KGaA accounting for a significant share of global revenue. These players leverage strong biopharmaceutical manufacturing networks, integrated bioprocessing portfolios, and advanced automation technologies to maintain competitive positioning. Companies are increasingly investing in closed-system processing, single-use bioprocessing, AI-enabled monitoring, and contamination control technologies to support growing demand from biologics and cell therapy manufacturers.

Meanwhile, companies such as Miltenyi Biotec, Terumo BCT, and Lonza are strengthening market presence through expertise in cell therapy manufacturing and regenerative medicine applications. Regulatory compliance requirements, GMP validation standards, and complex system integration continue to create barriers for new entrants. However, rising adoption of digital bioprocessing and modular manufacturing platforms is enabling emerging technology providers to compete through automation software, process analytics, and customized cell processing solutions.

Key Industry Developments:

- In October 2025, Teijin Limited and Cell Therapies Pty Ltd signed a strategic collaboration agreement to expand cell and gene therapy manufacturing infrastructure across Japan and Asia Pacific.

- In January 2025, Cytiva partnered with Cellular Origins to integrate robotic manufacturing with automated cell therapy production platforms, enabling scalable industrial manufacturing for cell and gene therapies.

Companies Covered in Cell Harvesting System Market

- Thermo Fisher Scientific Inc.

- Sartorius AG

- Danaher Corporation

- Merck KGaA

- Terumo BCT, Inc.

- Fresenius Kabi AG

- Lonza Group AG

- Eppendorf SE

- Getinge AB

- Miltenyi Biotec

- GE HealthCare

- Becton, Dickinson and Company

- Bio-Rad Laboratories, Inc.

- STEMCELL Technologies

- Asahi Kasei Medical Co., Ltd.

Frequently Asked Questions

The global cell harvesting system market is projected to reach US$7.2 billion in 2026.

Rising commercialization of cell therapies, expanding biologics manufacturing, and growing demand for automated bioprocessing technologies drive the cell harvesting system market.

The cell harvesting system market is expected to grow at a CAGR of 12.2% from 2026 to 2033.

Growth opportunities lie in regenerative medicine expansion, biologics manufacturing investments, and adoption of automated closed-system harvesting technologies.

Thermo Fisher Scientific, Sartorius AG, Danaher Corporation (Cytiva), Merck KGaA, and Lonza are key players in the market.