- Specialty & Fine Chemicals

- Bio-succinic Acid Market

Bio-succinic Acid Market Size, Share, and Growth Forecast 2026 - 2033

Bio-succinic Acid Market by Raw Material (Corn, Sugarcane, Cassava, Biomass, Others), Application (Industrial Polymers/PBS, BDO, Polyester Polyols, Plasticizers, Alkyd Resins, Others), and Regional Analysis for 2026 - 2033

Bio-succinic Acid Market Size and Trend Analysis

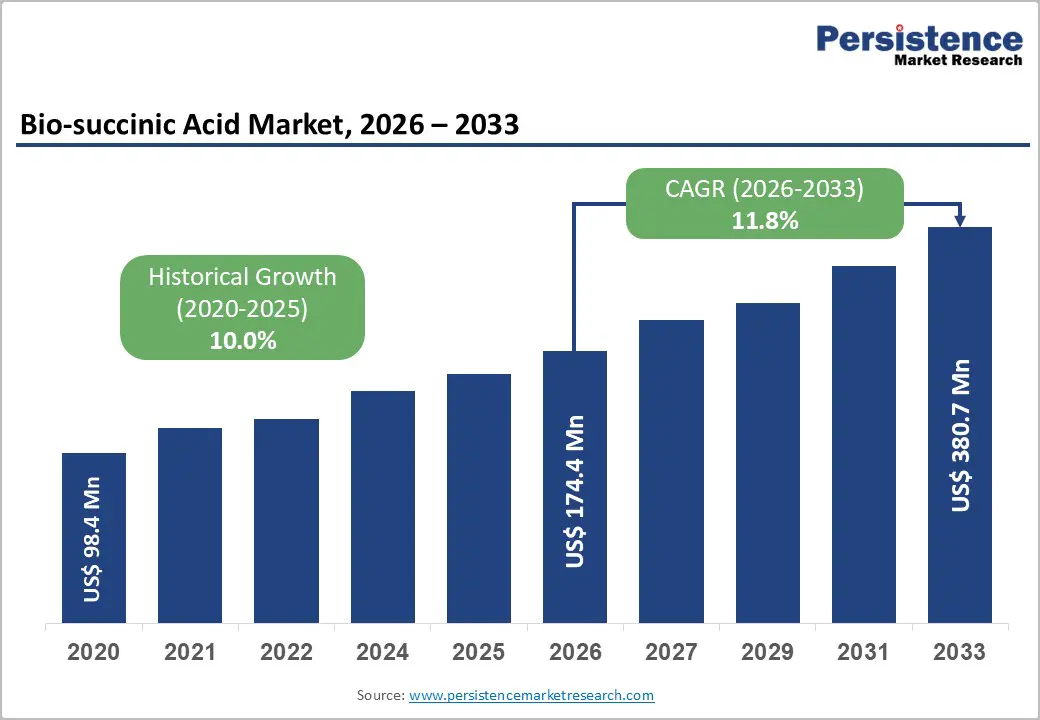

The global bio-succinic acid market size is expected to be valued at US$ 174.3 million in 2026 and is projected to reach US$ 380.7 million by 2033, growing at a CAGR of 11.8% between 2026 and 2033. This high-growth trajectory is driven by the global chemical industry's accelerating transition from petrochemical-derived succinic acid to bio-based alternatives, propelled by stringent regulatory frameworks targeting fossil-fuel-derived chemicals, brand owner corporate sustainability commitments, and the commercial scale-up of fermentation-based bio-succinic acid production, achieving cost-competitiveness with petrochemical routes.

Key Industry Highlights:

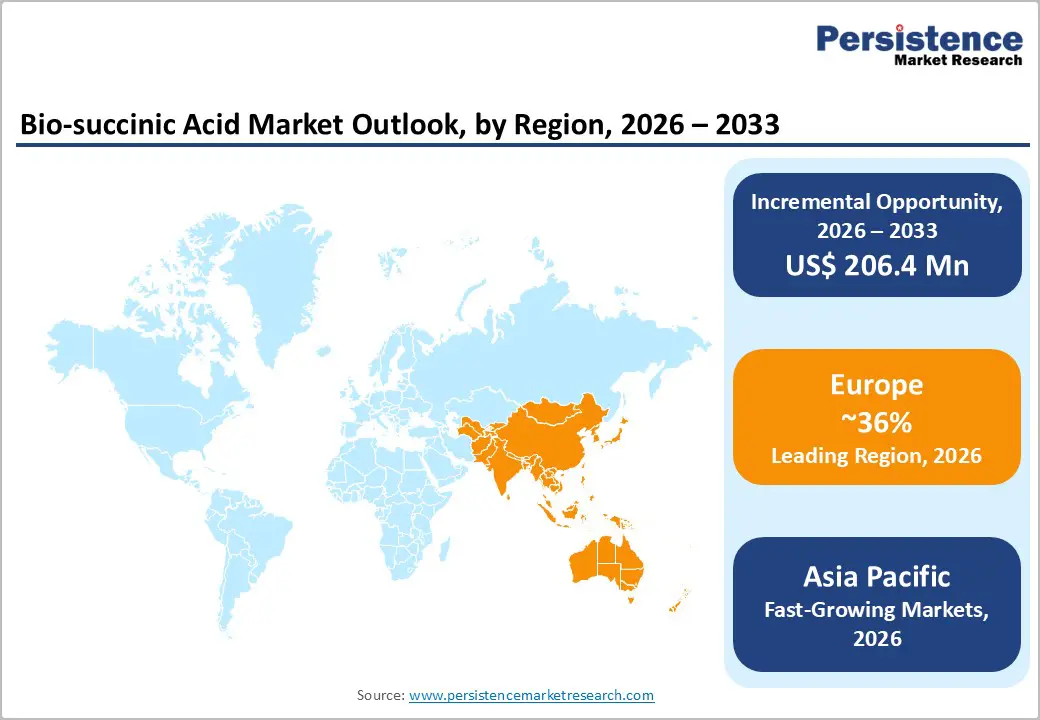

- Leading Region: Europe leads the global bio-succinic acid market, with 36% market share, driven by EU Bioeconomy Strategy mandates, and Single-Use Plastics Directive PBS packaging compliance requirements.

- Fastest Growing Region: Asia Pacific is the fastest growing national bio-succinic acid market, driven by India’s sugarcane feedstock cost advantages, Single-Use Plastics Prohibition Rules 2022 driving PBS demand, and growing fermentation-based chemical manufacturing investment building domestic bio-succinic acid supply capacity.

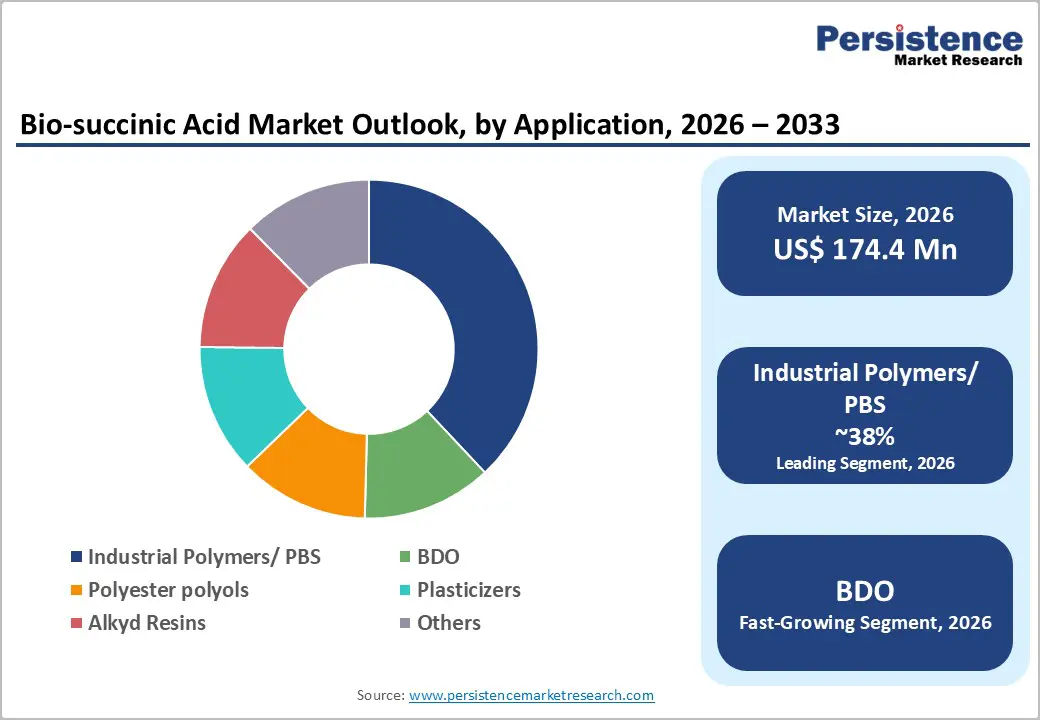

- Dominant Segment: PBS and industrial polymers hold 38% application market share in 2025, driven by European Bioplastics Association-documented double-digit PBS growth, EU Single-Use Plastics Directive compliance creating mandatory PBS packaging adoption, and each PBS tonne consuming 0.4-0.5 tonnes of bio-succinic acid as direct feedstock.

- Fastest Growing Segment: Bio-BDO production is the fastest growing application, driven by DOE-documented 70% GHG reduction versus petrochemical BDO, Genomatica's commercial bio-BDO technology platform, and Mitsubishi Chemical and BASF downstream polymer programs creating premium-priced pull-through demand for bio-succinic acid feedstock.

- Key Opportunity: Roquette's pharmaceutical-certified bio-succinic acid program and DOE-documented 70% lifecycle GHG savings for bio-BDO demonstrate that premium pharmaceutical and engineering polymer applications can command 30-50% price premiums over commodity PBS, making these high-value applications the highest-margin growth frontier for bio-succinic acid producers through 2033.

DRO Analysis

Drivers - EU Bioeconomy Strategy Mandating Bio-Based Transitions

Regulatory mandates across Europe and growing policy pressure globally are creating structural demand floors for bio-succinic acid by restricting petroleum-derived chemical equivalents and providing certification advantages for bio-based alternatives. The European Commission's Bioeconomy Strategy and the EU Green Deal explicitly target the substitution of fossil-fuel-derived chemicals with bio-based alternatives as a core decarbonization pathway for the chemical industry.

The EU's REACH regulation and evolving restrictions on petroleum-derived chemical components in food contact materials and packaging are progressively expanding the regulatory space in which bio-succinic acid's renewable origin provides compliance advantages. Brand owner commitments under programs including the Zero Discharge of Hazardous Chemicals initiative and the Ellen MacArthur Foundation's New Plastics Economy are additionally driving chemical buyers to prefer bio-based feedstocks, including bio-succinic acid for polyester polyol and PBS polymer applications, that carry documented renewable content credentials.

Growing Demand for Biodegradable PBS Polymers in Packaging and Agricultural Films

The most commercially significant demand catalyst for bio-succinic acid is the rapidly expanding adoption of polybutylene succinate (PBS), a biodegradable polymer produced by reacting bio-succinic acid with bio-butanediol, across food packaging, agricultural mulch film, and single-use item applications. The European Bioplastics Association) documents consistent double-digit growth in global bioplastics production capacity, with PBS among the fastest-growing biodegradable polymer categories.

The EU's Single-Use Plastics Directive (2019/904) has created regulatory demand for compostable and biodegradable alternatives to conventional plastics in food service and packaging, directly benefiting PBS and the bio-succinic acid supply chain that underpins it. Agricultural applications, particularly biodegradable mulch films that eliminate plastic recovery costs after crop harvest, are generating volume demand from precision agriculture programs in Europe and Japan, where plastic film pollution has become a regulatory priority.

Restraints - Higher Production Costs Relative to Petroleum-Derived Succinic Acid Constraining Adoption

Despite significant fermentation technology improvements, bio-succinic acid still commands a cost premium of approximately 20-40% above petroleum-derived succinic acid in most market conditions, creating resistance to specification change among price-sensitive industrial buyers who do not receive a sufficient sustainability price premium to offset the input cost differential. The U.S. Department of Energy (DOE)) has identified succinic acid as a top-12 bio-based chemical building block with high commercial potential, but achieving full cost parity with petrochemical routes remains dependent on feedstock cost optimization, fermentation yield improvement, and downstream purification efficiency, all areas requiring continued capital investment that constrains rapid margin expansion for producers.

Feedstock Price Volatility and Agricultural Commodity Market Exposure

Bio-succinic acid's dependence on agricultural feedstocks, corn starch, sugarcane molasses, and cassava glucose as primary carbon sources for fermentation, exposes production economics to agricultural commodity price cycles that can be as volatile as petrochemical feedstock markets. The FAO's food commodity price index has documented 30-60% agricultural commodity price swings between cycle extremes, directly impacting bio-succinic acid production cost and margin predictability. In periods of elevated agricultural commodity prices, such as the 2021-2022 food price spike documented by FAO, the cost premium of bio-succinic acid versus petroleum-derived alternatives can widen to economically prohibitive levels, stalling conversion projects and complicating multi-year offtake contract pricing.

Opportunities - PBS Bioplastics for Packaging: Fastest Growing Application at Above-Market CAGR

PBS bioplastics are bio-succinic acid’s fastest-growing use, boosted by regulations and sustainability commitments expanding mainstream packaging demand. The European Bioplastics Association documents PBS production capacity growing at double-digit annual rates across Europe, while Japan's Ministry of Economy, Trade and Industry (METI) has established a bioplastics market promotion strategy targeting significant domestic bioplastics adoption by 2030.

BASF's Ecoflex and Mitsubishi Chemical's GS Plan PBS grades are gaining commercial traction in flexible food packaging certification programs. Each ton of PBS produced consumes approximately 0.4-0.5 tons of succinic acid, making PBS capacity expansion a direct and proportional demand multiplier for bio-succinic acid producers.

High-Value Derivative Application Expanding Total Addressable Market

Bio-based butanediol (BDO), produced by hydrogenating bio-succinic acid, represents a high-value derivative that extends bio-succinic acid's addressable market into BDO's much larger downstream applications, including THF (tetrahydrofuran), PBT engineering plastics, and spandex/elastane fibers. The bio-BDO market is growing rapidly as a major BDO consumer, including BASF and Mitsubishi Chemical, which pursue bio-based feedstock transitions for their downstream polymer programs.

Genomatica's commercial bio-BDO technology, producing BDO from sugar via fermentation through a succinic acid intermediate, has been commercialized through partnerships with Novamont and Versalis. The DOE estimates that bio-based BDO can reduce greenhouse gas emissions by 70% versus petrochemical BDO on a lifecycle basis, a differentiator that enables bio-BDO and its bio-succinic acid feedstock to command premium pricing from sustainability-committed polymer producers globally.

Category-wise Analysis

Raw Material Insights

Corn is the dominant raw material for bio-succinic acid fermentation, accounting for approximately 42% market share in 2025. Corn starch, hydrolyzed to glucose as the primary fermentation carbon source, provides the highest-quality, most consistent, and most commercially scalable feedstock for bio-succinic acid fermentation processes, making it the preferred specification for established producers in North America and Europe, where corn supply chains are well-developed and glucose quality is consistent.

BASF SE's and Corbion's bio-succinic acid programs rely on corn glucose from established North American and European agricultural supply chains. The USDA documents corn as the world's most produced cereal grain at over 1.2 billion tons annually, ensuring a supply scale for bio-succinic acid fermentation. Sugarcane is the fastest-growing raw material segment, particularly in Brazil and India, where lower feedstock costs drive competitive fermentation economics versus corn-based production.

Application Insights

Industrial Polymers/PBS (polybutylene succinate) dominates the application segment, accounting for approximately 38% share in 2025. PBS is the commercially most significant downstream application for bio-succinic acid, combining the polymer's biodegradable credentials with broad processing compatibility across existing plastics manufacturing infrastructure.

PBS is a leading growth engine for bio-succinic acid because it’s biodegradable and fits packaging and agricultural films. Regulations (e.g., single-use plastics limits) and brand sustainability targets are accelerating adoption. As PBS capacity expands, demand rises directly since PBS production consumes significant succinic acid per tonne.

Regional Insights

North America Bio-succinic Acid Market Trends & Analysis

North America is a technically advanced bio-succinic acid market characterized by strong R&D infrastructure, mature corn-based fermentation feedstock supply chains, and growing demand from the sustainable packaging and bio-based chemicals transition programs of major consumer goods companies. The U.S. Department of Energy (DOE) has designated succinic acid among its top 12 bio-based chemical building blocks with the highest commercial potential, sustaining federal research support for bio-succinic acid fermentation technology improvement.

Growing PBS packaging adoption from CPG companies under brand sustainability commitments is driving commercial-scale bio-succinic acid procurement growth.

U.S. Bio-succinic Acid Market Size

The United States accounts for approximately 74% of the North American bio-succinic acid market revenue in 2025. U.S. demand is anchored by the DOE's bio-based chemicals technology program, growing PBS packaging adoption by major food companies under sustainability commitments, and the emerging bio-BDO commercialization pathway via Genomatica's technology platform.

Europe Bio-succinic Acid Market Trends, Drivers & Insights

Europe is the world's most advanced regulatory environment for bio-based chemicals, making it the highest-priority market for bio-succinic acid commercial development. The EU Bioeconomy Strategy, EU Green Deal, and Single-Use Plastics Directive collectively create the world's most supportive policy framework for bio-succinic acid adoption across PBS packaging, polyester polyols, and bio-BDO applications.

Germany Bio-succinic Acid Market Size

Germany holds approximately 26% of the European bio-succinic acid market revenue in 2025. BASF SE's Ludwigshafen operations and Germany's world-class chemical industry, encompassing polyester, polyurethane, and polymer manufacturers, generate substantial bio-succinic acid procurement for PBS and polyester polyol applications. Germany's Circular Economy Act is accelerating bio-based chemical specification.

U.K. Bio-succinic Acid Market Size

The United Kingdom represents approximately 12% of the European bio-succinic acid market revenue in 2025. The UK's active sustainable packaging regulatory push, including the Plastic Packaging Tax, incentivizing recycled and biodegradable content, is driving PBS packaging adoption from UK-based food manufacturers. UK CAGR is projected at approximately 11.5% through 2033.

France Bio-succinic Acid Market Size

France accounts for approximately 14% of the European bio-succinic acid market revenue in 2025. Roquette Frères, headquartered in Lestrem, is a major bio-succinic acid producer serving European market demand from its integrated starch-to-bio-chemical production platform. France's AGEC anti-waste law mandating compostable packaging expansion is driving PBS demand.

Asia Pacific Bio-succinic Acid Market Drivers & Analysis

Asia Pacific is the fastest-growing bio-succinic acid market globally, driven by China's expanding bio-based chemicals manufacturing capability, Japan's METI bioplastics promotion strategy, and India's growing fermentation-based chemical industry. China accounts for approximately 44% of Asia Pacific bio-succinic acid demand, with domestic producers including Anhui Sunsing Chemicals serving growing domestic PBS polymer demand from China's packaging industry, transitioning away from conventional plastics under China's plastic ban regulations. Japan's sophisticated bioplastics market and South Korea's advanced chemical sector are additional regional growth drivers.

China Bio-succinic Acid Market Size

China holds approximately 44% of the Asia Pacific bio-succinic acid market revenue in 2025. Anhui Sunsing Chemicals is a major Chinese bio-succinic acid producer serving domestic PBS polymer manufacturers. China's Action Plan on Plastic Pollution Control, banning single-use plastics in key sectors, is directly driving PBS and bio-succinic acid demand growth.

India Bio-succinic Acid Market Size

India represents approximately 11% of the Asia Pacific bio-succinic acid market revenue in 2025. India's sugarcane industry, one of the world's largest, provides cost-competitive fermentation feedstock for bio-succinic acid production, creating competitive supply chain advantages. India's Single-Use Plastics Prohibition Rules 2022 are driving bioplastics demand, including PBS.

Japan Bio-succinic Acid Market Size

Japan contributes approximately 12% of the Asia Pacific bio-succinic acid market revenue in 2025. Japan's advanced bioplastics sector, with Mitsubishi Chemical's GS Pla PBS and Nippon Shokubai's bio-based chemical programs, and METI's bioplastics promotion strategy targeting 2 million tons of bioplastics adoption by 2030 sustain growing bio-succinic acid demand.

Competitive Landscape

The global bio-succinic acid market exhibits a moderately consolidated competitive structure, with a limited number of vertically integrated chemical companies and specialized bio-based chemical producers controlling most of the commercial production capacity. Emerging strategic trends include joint ventures between fermentation technology specialists and commodity chemical companies, bio-succinic acid co-production with other bio-based platform chemicals sharing fermentation infrastructure, and development of second-generation lignocellulosic biomass feedstocks to further reduce production costs.

Key Developments

- August 2022: Technip Energies announces the purchase of Biosuccinium® technology from DSM, adding a technology solution to its growing Sustainable Chemicals portfolio.

- October 2024: Mitsubishi Chemical Corporation expanded its GS Plan PBS biopolymer production capacity in Japan, consuming additional bio-succinic acid volumes to serve growing PBS flexible packaging demand from Japanese food manufacturers under METI's bioplastics promotion program.

- September 2024: Mitsubishi Corporation and ExxonMobil Corporation signed a Project Framework Agreement for Mitsubishi Corporation's participation in ExxonMobil's facility in Baytown, Texas, which is expected to produce virtually carbon-free hydrogen with approximately 98% of CO2 removed, as well as low-carbon ammonia.

Top Companies in the Bio-succinic Acid Market

- BASF SE (Ludwigshafen, Germany) is the world's largest chemical company and a pioneer in bio-succinic acid commercialization, having developed the BioAmber bio-succinic acid joint venture program and retaining active bio-based chemical R&D investment. BASF's downstream integration into PBS polymers (Ecoflex) and polyester polyols creates a vertically integrated demand pathway for bio-succinic acid, and its global chemical distribution network provides the broadest commercial reach for bio-succinic acid applications.

- Corbion N.V. (Amsterdam, Netherlands) is a specialized bio-based chemical producer with established commercial bio-succinic acid production capabilities serving European industrial buyers. Corbion's expertise in fermentation-based chemistry, leveraging its lactic acid fermentation technology heritage, gives it a competitive manufacturing efficiency advantage. Its focus on serving PBS polymer producers and specialty chemical applications positions it as the leading dedicated bio-succinic acid commercial supplier in Europe.

- Mitsubishi Chemical Corporation (Tokyo, Japan) is the world's leading PBS biopolymer producer through its GS Plan brand, making it simultaneously the world's largest single commercial consumer of bio-succinic acid for polymer production. Its vertically integrated position, from bio-succinic acid procurement through PBS polymerization and compound development, gives it unmatched commercial insight into downstream PBS market development and supply chain security requirements for bio-succinic acid quality and consistency.

Companies Covered in Bio-succinic Acid Market

- BASF SE

- DSM (dsm-firmenich)

- Anhui Sunsing Chemicals

- Kawasaki Kasei Chemicals

- Mitsubishi Chemical Corporation

- Technip Energies N.V.

- Roquette Freres

- BioAmber Inc.

- Nippon Shokubai Co. Ltd.

- Corbion N.V.

- Genomatica Inc.

- PTT Global Chemical

Frequently Asked Questions

The global bio-succinic acid market is projected to reach US$ 380.7 million by 2033, growing from an estimated US$ 174.3 million in 2026 at a CAGR of 11.8%. This high-growth trajectory reflects escalating demand for PBS biodegradable polymers, EU bioeconomy regulatory mandates, bio-BDO commercialization, and the progressive achievement of cost competitiveness with petroleum-derived succinic acid alternatives globally.

Primary drivers include the EU Bioeconomy Strategy and Single-Use Plastics Directive (2019/904), creating mandatory biodegradable polymer adoption requirements, with PBS, consuming 0.4-0.5 tonnes of bio-succinic acid per tonne, among the primary compliance solutions.

Industrial Polymers/PBS leads with approximately 38% application market share in 2025, driven by the European Bioplastics Association-documented double-digit PBS capacity growth, EU SUPD compliance driving PBS packaging specification, and Mitsubishi Chemical's GS Pla PBS polymer, the world's largest single PBS commercial program, as the largest institutional bio-succinic acid buyer.

Europe leads with approximately 38% market share in 2025, anchored by EU Bioeconomy Strategy mandates, EU Green Deal, and Single-Use Plastics Directive regulatory frameworks. Asia Pacific, particularly India at 13.5% CAGR and China at 12.8% CAGR, is the fastest growing region, driven by plastic ban regulations and sugarcane-based low-cost fermentation economics.

The highest-value opportunity lies at the convergence of pharmaceutical-certified bio-succinic acid excipients, pioneered by Roquette's pharmaceutical supply program, and bio-BDO high-value derivatives commanding 30-50% price premiums over commodity PBS applications. Genomatica's commercial bio-BDO technology and DOE's 70% lifecycle GHG savings documentation create a compelling premium market case. India's sugarcane cost advantage at 13.5% CAGR additionally represents the highest-growth greenfield production location for bio-succinic acid capacity investment through 2033.

Key companies include BASF SE, Corbion N.V., Roquette Freres, Mitsubishi Chemical, Nippon Shokubai, Anhui Sunsing Chemicals, Genomatica, DSM, Kawasaki Kasei Chemicals, and PTT Global Chemical.