Comprehensive Snapshot of Automatic Lubrication Systems Market Report Including Regional and Country Analysis in Brief.

Industry: Industrial Automation

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 130

Report ID: PMRREP31509

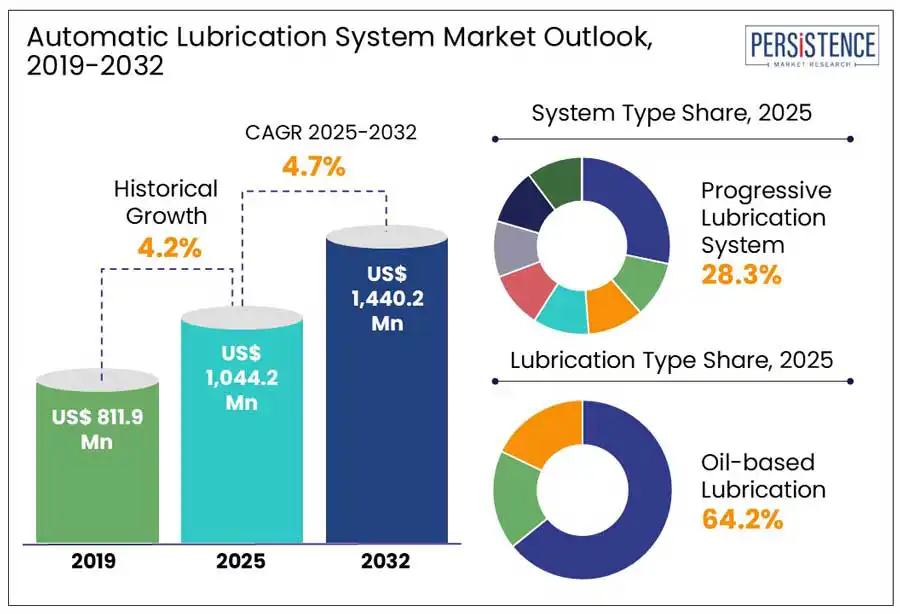

The global automatic lubrication systems market size is projected to value at US$ 1,044.2 Mn to accelerate at a CAGR of 4.7%, reaching a market valuation of US$ 1,440.2 Mn by the end of 2032. This growth is fueled by the increasing automation and the growing emphasis on minimizing machinery downtime across diverse industries including steel, manufacturing, transportation, mining, power, cement, construction, paper & printing, and agriculture.

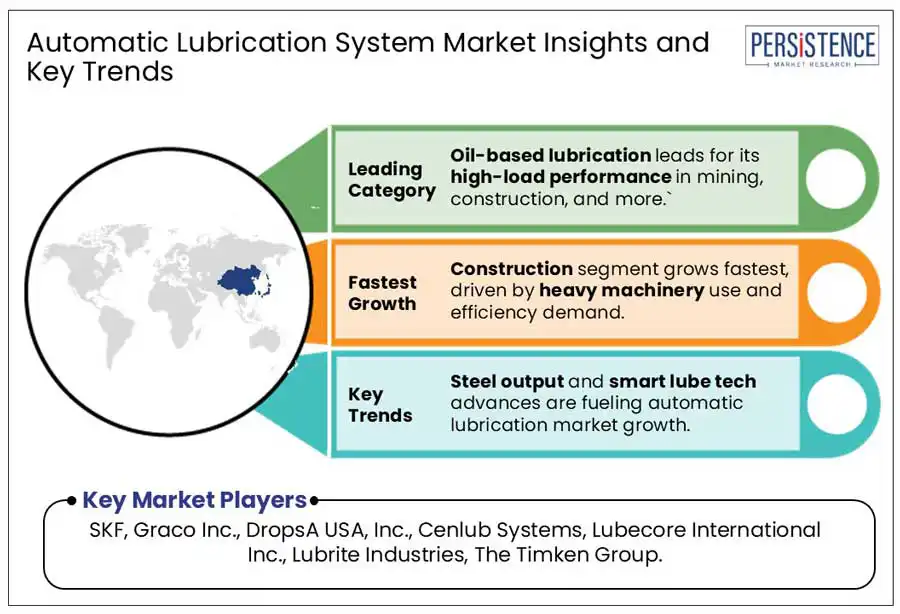

The mining sector, particularly in India, is on an upward trajectory with 1,319 reporting mines and significant reserves of coal, iron ore, and bauxite. Its role as a key supplier of raw materials to construction, automotive, and energy industries positions it as a vital End-user of advanced lubrication technology. In parallel, the steel industry remains a cornerstone of industrial development, with global crude steel output hitting 1.88 billion tonnes highlighting continuous operational requirements that benefit from automated lubrication processes.

In the transportation and automotive segments, car sales surpassed 72 million units globally in 2023, registering nearly 10% growth from the prior year. Emerging markets such as India, which achieved record-high sales of 4.2 million units, are driving the need for high-performance manufacturing support systems. Infrastructure expansion in Asia and sub-Saharan Africa, along with India’s projected US$1 trillion annual construction output by 2030 is further amplifying demand for efficient lubrication solutions in heavy-duty machinery and industrial equipment.

Key Industry Highlights:

|

Global Market Attribute |

Details |

|

Automatic Lubrication Systems Market Size (2024A) |

US$ 997.3 Million |

|

Estimated Market Size (2025E) |

US$ 1,044.2 Million |

|

Projected Market Value (2032F) |

US$ 1,440.2 Million |

|

Value CAGR (2025 to 2032) |

4.7% |

|

Collective Share: Top 3 Countries (2025E) |

60 % |

The market growth is supported by the rising infrastructure investment and the adoption of smart lubrication systems across sectors such as construction, logistics, and agriculture. Focus on durability and cost-efficiency is likely to drive innovation in system design. In April 2024, CENLUB SYSTEMS introduced its MINO range of greasing systems, optimized for the ease of installation, improved uptime, and simplified maintenance in mobile equipment applications.

The growing scale and complexity of global steel manufacturing are intensifying the need for efficient machinery upkeep. As steel plants operate under high temperatures, heavy loads, and continuous production cycles, maintaining equipment reliability becomes essential. This drives the demand for advanced lubrication technologies that can operate with precision in extreme conditions, ensuring smooth performance and reduced downtime.

The initial high costs of purchasing, installing, and maintaining automatic lubrication systems is a significant barrier, particularly for small and medium-sized businesses with limited budgets. Despite the long-term benefits of these systems such as reduced downtime and operational costs, the substantial upfront financial commitment discourages many potential players. The ongoing maintenance costs also adds to the financial burden, making companies hesitant to invest in automation technologies. This factor is crucial in slowing down the widespread adoption of these systems.

Industrial lubrication is undergoing a significant shift, driven by strategic acquisitions and smart product innovations. A notable development occurred in August 2024, when SKF announced its acquisition of John Sample Group’s Lubrication and Flow Management units. This move strengthens SKF’s footprint in India and the rest of Southeast Asia, boosting its distribution capabilities and expanding its service network to meet the growing demand for machine reliability.

Companies are investing in product advancements that emphasize performance, longevity, and digital integration. Graco Inc.'s GCI™ Series injectors, launched in March 2023, offer double the lifespan of traditional components and reduce system downtime through easier replacements. Earlier, in January 2020, the launch of the GLC™ X controller and Auto Lube™ app marked a leap toward data-driven maintenance, enabling remote monitoring and smarter system adjustments. These innovations are enhancing system efficiency while reducing labor and operational costs.

Oil-based lubrication is projected to account for 64.2% share in 2032. Oil-based lubrication is preferred for several machinery applications. Oil-based lubrication comes with several advantages such as better-cooling properties, i.e., it carries away unwanted heat and does not contain thickeners so there is no risk of incompatible thickeners mixing. Due to its ability to remove impurities, oil is cleaner than grease and is also simpler to regulate the amount of lubricant used. The oil from lubrication systems can be easily changed without dismantling the machine hardware. Due to these factors, oil-based lubrication has a high potential for expanding in the coming years.

The series progressive lubrication systems are estimated to account for 28.3% revenue share by 2032. Series progressive systems facilitate continuous lubrication as long as the pump is in process condition. When the pump stops working, the pistons of the progressive metering device halts in their current position. After lubrication, the pistons resume working where the pumps left off. Other benefits include continuous lubrication, reliable monitoring and control, and effectiveness in harsh conditions. Therefore, the series progressive lubrication systems have become the most popular.

End-use industries present a mixed outlook. The construction sector has faced a prolonged downturn, with real investment dropping for the third straight year by 2.7% in 2023. Despite rising labor figures, issues such as rising material costs, policy uncertainty, and reduced residential construction orders have weighed on the market in the early 2025. In contrast, the transportation sector remains relatively more stable. Though total car sales dropped by 1.0% in 2024, truck sales rose 9.0%, and vehicle exports saw a 2.0% rise. The mix of hybrid and alternative powertrain vehicles also indicates a shift in mobility trends, which supports continued demand for lubrication systems in vehicle production and maintenance operations.

Germany expects to witness a CAGR of 3.2% by 2032 and account for a prominent share during the forecast period. This growth is driven by the strong foundation in machinery and equipment manufacturing as Germany is the foremost in Europe to adopt advanced automation systems across industrial sectors. Key industries such as automotive, metalworking, and general manufacturing has steadily integrated automatic lubrication systems to improve operational efficiency and reduce equipment downtime. These sectors are expected to continue anchoring demand for such solutions, supported by Germany’s emphasis on industrial innovation and engineering excellence.

India automatic lubrication systems market is poised for solid growth at a projected CAGR of 5.2%, by 2032 backed by rising demand from sectors such as construction, mining, and steel. India's construction sector, with a GVA of US$ 179.5 billion in FY25, is benefiting from a 11.1% rise in capital expenditure, driving increased use of heavy machinery and construction equipment. These machines rely heavily on automatic lubrication systems to ensure continuous operation and minimize downtime in high-load environments such as road building, real estate, and warehousing.

In the mining and steel industries, robust output continues to fuel demand for high-performance lubrication systems. India’s coal production reached 104.43 MT in January 2025, while crude steel production stood at 84.95 MT between April and December FY25. With iron ore output rising 3% YoY to 182.6 MMT and the steel sector expanding at 14% annually, the intense use of excavators, crushers, and transport vehicles necessitates efficient lubrication to maintain productivity and reduce equipment wear making automatic systems a critical component in these end-use markets.

The U.S. automatic lubrication systems market is expected to witness a CAGR of 3.4% during the forecast period. The country’s dominance in global manufacturing and automation, along with strict federal regulations and a high demand for advanced operational efficiency, drives market adoption. The construction industry, in particular, is a major end-user contributing nearly $2.2 trillion in annual spending and employing over eight million people as of 2024. With over 919,000 construction establishments and sustained growth in equipment-heavy segments like residential and infrastructure development, the demand for automatic lubrication systems is expected to remain strong.

The global automatic lubrication systems market is moderately consolidated with global and regional companies competing through a mix of innovation, acquisitions, and localized product development. Leading players are focusing on integrating advanced technologies such as remote monitoring, app-based control, and enhanced injector designs to improve system efficiency and reduce downtime. This focus on automation and smart capabilities highlights a broader industry shift toward predictive maintenance and cost optimization.

Manufacturers are strengthening their presence in emerging markets like India and Southeast Asia by expanding distribution networks and offering solutions suited to harsh operating environments across industries such as mining, construction, and transportation. Regional players are competing by offering robust, affordable, and easy-to-install systems that cater to the specific demands of local users, while global companies are leveraging strategic acquisitions and product portfolio enhancements to consolidate their market positions and address diverse end-use applications.

For instance, in August 2024, SKF acquired John Sample Group’s Lubrication and Flow Management businesses to strengthen its foothold in India and Southeast Asia. This move enhances SKF’s customer reach, service capabilities, and distribution network in the growing market.

|

Attribute |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2024 |

|

Market Analysis |

USD Million for Value, Units for Volume |

|

Key Regions Covered |

|

|

Key Countries Covered |

U.S., Canada, Mexico, Brazil, Argentina, Germany, Italy, France, Nordics, U.K., Spain, BENELUX, Russia, Central Asia, Baltics, Turkey, South Africa, Gulf Cooperation Council Countries, Northern Africa, Japan, China, South Korea, India, ASEAN, Australia & New Zealand |

|

Key Countries Covered |

|

The supply chain for automatic lubrication systems has improved over the past several years as a result of an increase in acquisitions and growth operations. Prominent manufacturers of automatic lubrication systems are focusing on business expansion through mergers & acquisitions, partnerships, and contracts to further strengthen their market presence in regional and global markets, and new product launches to enhance their product portfolios in lubrication systems.

|

Attribute |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2024 |

|

Market Analysis |

USD Million for Value, Units for Volume |

|

Key Regions Covered |

|

|

Key Countries Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon Request |

By Lubrication Type

By System Type

By End-use

By Region:

To know more about delivery timeline for this report Contact Sales

The global market is projected to value at US$ 1,044.2 Million in 2025.

The market is poised to witness a CAGR of 4.7% from 2025 to 2032.

Driven by strategic acquisitions and smart innovations, manufacturers are reshaping the landscape of intelligent lubrication technologies. Companies are investing in advanced, data-enabled systems that enhance uptime, reduce maintenance, and support Industry 4.0 initiatives across sectors.

The series progressive lubrication systems are projected to hold a 31.3% share in 2025, driven by rising demand for flexible, on-site crushing solutions. Their cost-efficiency and ability to reduce material transportation are key growth factors.

Integration of IoT and Industry 4.0 and Rapid Expansion of Industrial Infrastructure in Emerging Economies are the key opportunities in the market, driven by the increasing need for real-time monitoring, predictive maintenance, and the growing demand for automation across heavy industries in developing regions.

The leading players include SKF, Graco Inc., DropsA USA, Inc., Cenlub Systems, Lubecore International Inc., Lubrite Industries, The Timken Group.