Industry: IT and Telecommunication

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 189

Report ID: PMRREP35089

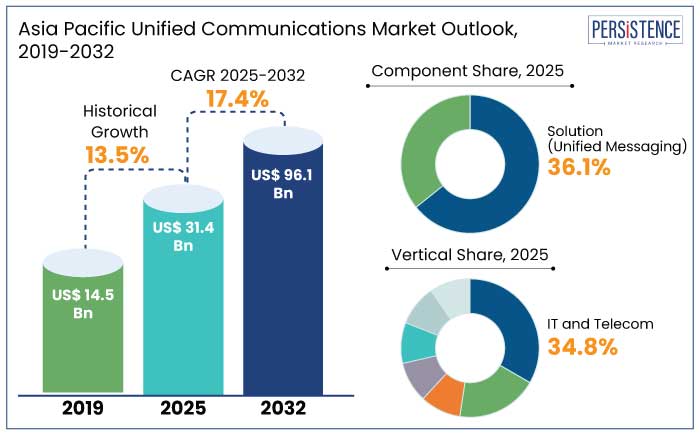

The Asia Pacific unified communications market is estimated to reach a size of US$ 31.4 Bn in 2025. The industry is anticipated to rise at a CAGR of 17.4% through the forecast period to attain a value of US$ 96.1 Bn by 2032.

As organizations prioritize scalability, cost-efficiency, and remote accessibility, the demand for cloud-hosted UC platforms is estimated to surge. The shift toward remote and hybrid work arrangements is anticipated to elevate the need for effective communication tools, further propelling growth.

Increasing investment in cloud infrastructure and the scalability offered by cloud-based UC solutions are significant contributors to market expansion. Artificial Intelligence (AI) powered features, including chatbots, automated transcription, and predictive analytics, are becoming integral to UC platforms.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Asia Pacific Unified Communications Market Size (2025E) |

US$ 31.4 Bn |

|

Projected Market Value (2032F) |

US$ 96.1 Bn |

|

Asia Pacific Market Growth Rate (CAGR 2025 to 2032) |

17.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

13.5% |

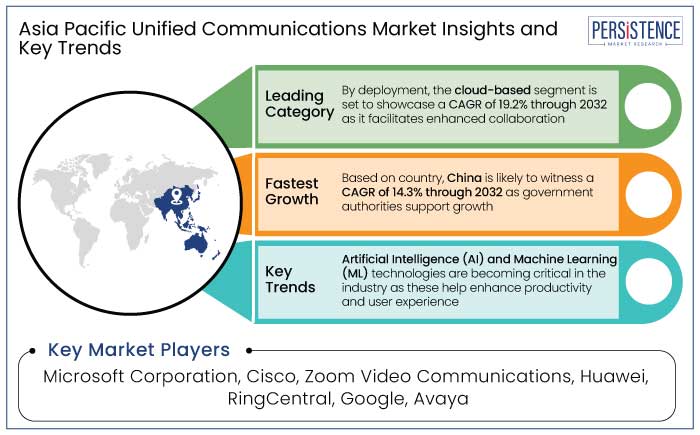

China has consistently maintained a substantial share and is projected to hold 41.8% in 2025 in the Asia Pacific unified communications industry. The country’s booming digital infrastructure, supported by government initiatives such as the Digital China program, creates an ecosystem that is conducive to UC adoption.

The program prioritizes the modernization of communication systems, including integrated telephony, messaging, and conferencing solutions. These are pivotal for businesses transitioning to hybrid and remote work models. The country's robust internet penetration and 5G rollout further enhance the adoption of UC technologies. For instance,

The developments enable seamless communication across large enterprises and SMEs alike. This infrastructure underpins UC solutions like Zoom, Microsoft Teams, and Huawei's enterprise communication tools?. Owing to the aforementioned factors, China is likely to witness a CAGR of 14.3% through 2032.

Unified messaging solution is predicted to hold a share of 36.1% in 2025. This solution has the ability to provide real-time and cross-platform communication, which is critical in the present fast-paced business environment. This communication mode enables employees to send and receive messages across multiple devices such as smartphones, tablets, and desktops, thereby enabling collaboration even in remote work setups.

As economies in Asia Pacific embrace digital transformation, businesses are recognizing the value of immediate communication solutions that enhance productivity and foster smoother interaction. In 2023, the enterprise sector contributed to a significant portion of the market owing to the need for unified communication tools that integrate voice, video, and messaging capabilities into one seamless experience?.

The tools have become indispensable in managing geographically dispersed teams and streamlining communication across various departments. This makes them particularly popular among businesses in countries like China and India. As these nations continue to push for digital infrastructure improvements, the demand for unified messaging is likely to witness further growth?.

The cloud-based segment is anticipated to witness a CAGR of 19.2% through 2032. Growth in the segment is driven by its flexibility, scalability, and cost-effectiveness. As organizations increasingly adopt cloud technology, the demand for cloud-based UC solutions continues to rise.

Cloud-based solutions facilitate enhanced collaboration, integration of communication tools, and remote management of operations. These are the key components of the current hybrid work environment, thereby fostering demand. Unlike traditional on-premises UC systems, cloud-based solutions offer a pay-as-you-go model that provides financial flexibility and reduces the total cost of ownership.

Cloud-based UC solutions are well-suited to the expanding remote and hybrid work models. Businesses are focusing on providing employees with flexible work arrangements and access to productivity tools, which are abundant in cloud-based UC offerings.

For instance, platforms such as Webex and Microsoft Teams are incorporating generative AI capabilities to enhance team collaboration and communication, making cloud solutions even more attractive. These platforms enable seamless communication and collaboration across geographical boundaries, mitigating latency issues and ensuring consistent connectivity among dispersed teams.

The IT and telecom segment is anticipated to hold a share of 34.8% in 2025. Technological innovations and increasing reliance on digital communication solutions are key drives of growth. The widespread adoption of cutting-edge technologies, such as 5G, IoT, and cloud computing, has greatly enhanced UC systems.

Telecom providers play a central role in deploying the necessary infrastructure required for seamless communication services, a critical component for businesses in the current landscape of remote work and decentralized teams. The escalating demand for enhanced collaboration tools within the IT and telecom sectors is responsible for fostering expansion.

Businesses in these industries are implementing UC solutions to streamline operations, improve customer service, and enhance internal communications. The integration of mobile devices, video conferencing, and collaboration platforms enables employees across diverse locations to interact effortlessly. These further boosts productivity and decreases operational costs.

Prominent telecommunications companies such as China Mobile and Bharti Airtel have been at the forefront of advancing mobile and internet technologies, facilitating the broad adoption of UC solutions among enterprises. This widespread technological adoption supports the sector's leading position in the market.

Unified communications (UC) integrate various communication tools and services into a single, cohesive system to streamline and enhance communication and collaboration within organizations. It combines real-time communication methods like voice calls, video conferencing, and instant messaging with non-real-time methods like email, voicemail, and SMS. This enables users to switch seamlessly between different communication channels. UC systems often leverage cloud technology, allowing access from multiple devices, including smartphones, tablets, and desktop computers, ensuring connectivity regardless of location.

There is a strong emphasis on integrating artificial intelligence (AI) and machine learning (ML) into UC platforms. AI-powered features such as virtual assistants, automatic transcription, sentiment analysis, and predictive analytics are gaining popularity.

The capabilities enhance productivity, optimize communication processes, and provide valuable insights into business operations. AI integration is particularly beneficial in industries like customer service, where real-time assistance and data analysis can enhance customer experience.

Organizations are looking for solutions that not only offer communication and collaboration features but also integrate with enterprise resource planning (ERP), customer relationship management (CRM), and productivity applications. This integration helps to streamline workflows, reduce silos, and improve overall operational efficiency. Platforms like Microsoft Teams, Slack, and Zoom have responded to this demand by offering deeper integrations with third-party business applications, creating unified environments for workers.

The Asia Pacific unified communications market growth was robust at a CAGR of 13.5% during the historical period. Rise of remote work, spurred by the COVID-19 pandemic, accelerated the adoption of unified communications. As cloud-based and hybrid solutions are being highly sought after owing to their flexibility, scalability, and cost-efficiency.

Sectors like banking, finance, healthcare, and education in countries like India, China, and Japan are increasingly leveraging UC solutions to improve collaboration, enhance customer service, and streamline internal communications. The adoption of UC tools by SMEs also witnessed growth, as these solutions enabled smaller businesses to compete with larger counterparts by providing them access to high-quality communication tools.

Growth in the forecast period is anticipated to be driven by the ongoing shift toward 5G technology to provide enhanced bandwidth and decreased latency, fueling the demand for high-quality unified communications services. This is further anticipated to support industries like healthcare, education, and IT and telecom in adopting sophisticated UC tools. Increasing focus on customer experience and personalized communication is likely to drive UC adoption as businesses look to offer responsive and efficient service through multi-channel communication platforms.

Rapid Development of Cloud Infrastructure to Foster Demand

Cloud infrastructure provides the backbone for scalable, reliable, and flexible communication platforms, enabling organizations to integrate diverse tools such as voice, video, messaging, and collaboration applications into unified ecosystems. With Asia Pacific holding 37% of the world's cloud data centers, it holds a massive potential for UC adoption, especially as businesses in the region seek to enhance agility and support remote and hybrid work models.

Government authorities across the region are fostering cloud development, directly boosting UC adoption. For instance, Singapore's Smart Nation initiative encourages the digitization of communication frameworks, while India's Digital India program prioritizes cloud services for public and private sector modernization.

The COVID-19 pandemic acted as a catalyst, with businesses adopting Desktop-as-a-Service (DaaS) and other cloud-enabled communication tools to support remote work. Unified Communications-as-a-Service (UCaaS) saw substantial growth as organizations sought to maintain operational continuity.

Hybrid and multi-cloud models are gaining traction, with over 50% of critical workloads anticipated to run on private and public clouds. This trend creates fertile ground for UC providers to offer tailored solutions that align with these infrastructures.

Widespread Adoption of Smartphones and Mobile Internet to Push Demand

Unique mobile subscriber penetration reached 63% of the population and exceeded 1.8 billion individuals in 2023. Hence, Asia Pacific demonstrates strong potential for sustained growth in the integrated communication services segment.

The growth corresponds to a CAGR of 2.1%, with smartphones accounting for 78% of mobile connections. This figure is projected to rise to 94% by 2030, underscoring the pivotal role of mobile technology in revolutionizing business and personal communication practices.

Asia Pacific's robust e-commerce and digital payment ecosystems. In markets like China, mobile-first strategies dominate, with integrated communication tools, assisting businesses to improve consumer engagement and streamline operations. For example,

Resistance to Change May Negatively Affect the Market

Several businesses in Asia Pacific, particularly SMEs, are hesitant to transition from legacy communication systems to integrated UC platforms. This reluctance is driven by concerns over implementation costs, disruptions during the migration process, and uncertainty about the return on investment.

In several countries in the region, hierarchical organizational structures and traditional work practices often hinder the acceptance of modern collaboration tools. Employees and decision-makers accustomed to face-to-face interactions or traditional telephony systems resist transitioning to cloud-based or integrated solutions. They cite a preference for familiar methods over innovative, technology-driven approaches. For example,

Japan-based companies often cite cultural preferences for in-person meetings and high sensitivity to data privacy as key factors inhibiting the uptake of digital communication tools.

Rollout of 5G Networks to Create Novel Opportunities

With the region's rising 5G coverage, businesses and government sectors are increasingly relying on 5G technology to enhance communication efficiency, support remote collaboration, and improve service delivery. 5G's high capacity facilitates better data streaming, faster video conferencing, and real-time collaboration tools, which are essential for companies transitioning to cloud-based and hybrid work models.

For instance, 5G is transforming the UC landscape through the deployment of private 5G networks at locations like Hong Kong International Airport and Bangkok's Krung Thep Aphiwat Central Terminal. These networks boast enhanced operational efficiency and safety through high-definition video surveillance, improved customer service, and more reliable, real-time communications.

In Singapore, the successful use of 5G during major sporting events demonstrated the network's ability to prioritize mobile traffic, ensuring uninterrupted mobile streaming even in high-density environments. The use of 5G is accelerating digital transformation in various industries, such as manufacturing, logistics, and healthcare. In Thailand, auto parts manufacturer Somboon Advance Technology utilizes 5G for robotic monitoring of production lines, thereby improving productivity and safety.

Growth of E-learning Platforms to Forge New Avenues

As the need for efficient and scalable communication tools has surged, educational institutions, businesses, and governments are embracing digital transformation. The expansion of e-learning platforms, combined with remote working and online collaboration, has created ample opportunities for UC providers to integrate novel solutions in their offerings.

The shift toward e-learning has led to greater reliance on cloud-based unified communications, enabling educational institutions to deliver live lectures, webinars, and collaborative projects to students, regardless of geographical constraints. The push for digitalization and smart education initiatives by governments is accelerating the adoption of these technologies, opening new opportunities for UC companies.

Tools like instant messaging, video conferencing, and cloud collaboration platforms have become indispensable in education, as institutions increasingly rely on them to manage the large volume of remote learners. This demand for robust, secure, and scalable solutions extends to virtual classrooms, exam monitoring, and interactive learning environments. The rapid adoption of these tools in educational settings is also influencing other sectors where UC tools facilitate seamless communication between businesses and their clients.

Companies in the Asia Pacific unified communications industry are continuously developing unique UC solutions that integrate communication tools into one seamless platform. Companies like Zoom Video Communications and Microsoft Teams have capitalized on this trend by enhancing their software with artificial intelligence (AI) and machine learning to provide smarter, more efficient communication experiences.

Innovations such as virtual meetings with immersive features, real-time transcription, and enhanced security measures are key competitive differentiators in the market. UC providers are focusing on improving the user experience by making their platforms more intuitive, user-friendly, and customizable.

Recent Developments in the Asia Pacific Unified Communications Market

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Country Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Component

By Deployment

By Enterprise Size

By Vertical

By Country

To know more about delivery timeline for this report Contact Sales

The market is estimated to reach a size of US$ 96.1 Bn by 2032.

The industry is propelled by growing adoption of cloud-based solutions, increasing demand for remote and hybrid work models, and surging mobile workforce.

Microsoft Corporation, Cisco, Zoom Video Communications, Huawei, RingCentral, and Google are few of the leading industry players.

The market is projected to record a CAGR of 17.4% during the forecast period.

A prominent opportunity lies in increasing investments in UC technologies, such as cloud-based solutions, AI-powered collaboration tools, and unique cybersecurity features.