- Executive Summary

- Global Aluminum Anodizing Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Regulatory Landscape

- Service Adoption Analysis

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Aluminum Anodizing Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

- Global Aluminum Anodizing Market Outlook: Material Source

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Material Source, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- Secondary Aluminum

- Market Attractiveness Analysis: Material Source

- Global Aluminum Anodizing Market Outlook: Process Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Process Type, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Attractiveness Analysis: Process Type

- Global Aluminum Anodizing Market Outlook: Finish Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Finish Type, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Attractiveness Analysis: Finish Type

- Global Aluminum Anodizing Market Outlook: Application Area

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application Area, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- Market Attractiveness Analysis: Application Area

- Key Highlights

- Global Aluminum Anodizing Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Aluminum Anodizing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Material Source

- By Process Type

- By Finish Type

- By Application Area

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- Secondary Aluminum

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- Europe Aluminum Anodizing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Material Source

- By Process Type

- By Finish Type

- By Application Area

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- Secondary Aluminum

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- East Asia Aluminum Anodizing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Material Source

- By Process Type

- By Finish Type

- By Application Area

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- Secondary Aluminum

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- South Asia & Oceania Aluminum Anodizing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Material Source

- By Process Type

- By Finish Type

- By Application Area

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- We

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- Latin America Aluminum Anodizing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Material Source

- By Process Type

- By Finish Type

- By Application Area

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- Secondary Aluminum

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- Middle East & Africa Aluminum Anodizing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Material Source

- By Process Type

- By Finish Type

- By Application Area

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Material Source, 2026 - 2033

- Primary Aluminum

- Secondary Aluminum

- Market Size (US$ Bn) Analysis and Forecast, By Process Type, 2026 - 2033

- Sulfuring Acid

- Hard Anodizing

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Finish Type, 2026 - 2033

- Natural

- Dyed

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application Area, 2026 - 2033

- Structural Component

- EV. Enclosures

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Bodycote

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- Aalberts Surface Technologies

- Pioneer Metal Finishing

- Norsk Hydro

- Arconic

- Linetec

- Henkel

- Lorin Industries

- Techmetals Inc.

- SAF Southern Aluminum Finishing

- Alumet Inc.

- Saporito Finishing Co.

- Anoplate

- Alumeco Group

- Bonnell Aluminum

- Chicago Anodizing Company

- Others

- Bodycote

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Metals & Minerals

- Aluminum Anodizing Market

Aluminum Anodizing Market Size, Share, and Growth Forecast, 2026 - 2033

Aluminum Anodizing Market by Material Source (Primary Aluminum, Secondary Aluminum), Process Type (Sulfuric Acid, Others), Finish Type (Natural, Dyed, Others), Application Area (Structural Components, EV Enclosures, Others), and Regional Analysis 2026 - 2033

Aluminum Anodizing Market Size and Trends Analysis

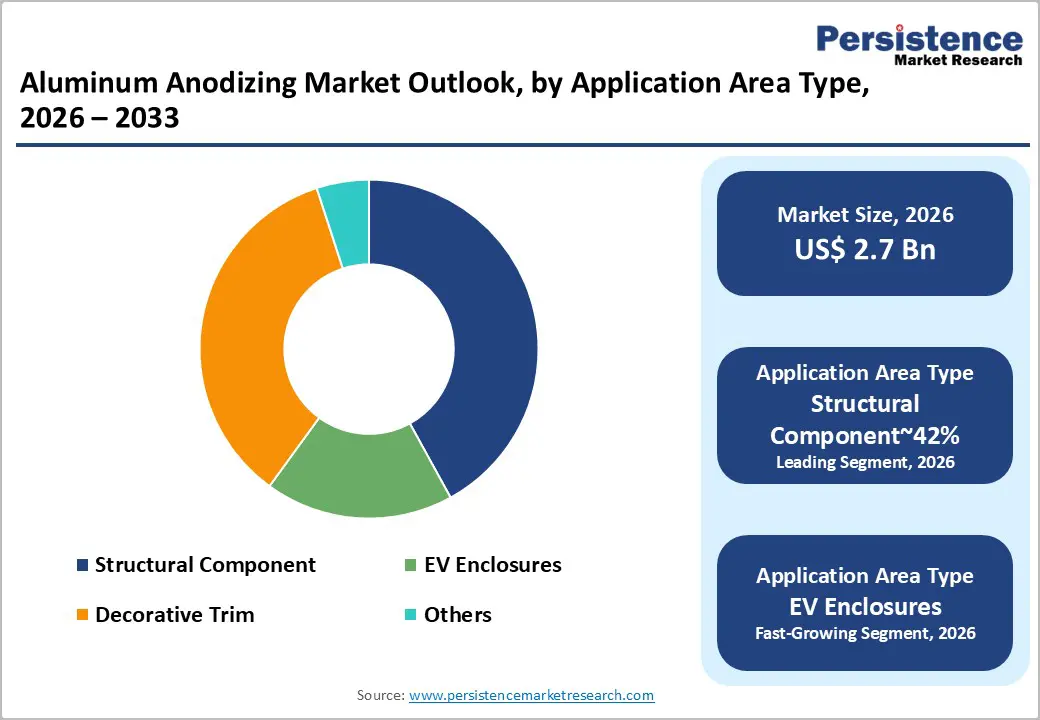

The global aluminum anodizing market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$3.8 billion by 2033, growing at a CAGR of 5.0% during the forecast period from 2026 to 2033, driven by the rising demand in automotive lightweighting and EV components, alongside construction sector expansion.

Asia Pacific, driven by manufacturing hubs in China and India. Additionally, escalating global ESG compliance pressures compel manufacturers to adopt anodized secondary aluminum over heavier alternatives. By leveraging sulfuric acid and hard anodizing techniques, industries achieve critical structural longevity, ensuring a sustained market trajectory.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to lead due to large-scale aluminum production capacity, capturing approximately 48% of the global market share in 2026, strong downstream manufacturing ecosystems, and high infrastructure and automotive demand.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest due to expanding EV manufacturing, renewable energy infrastructure, and rapid industrialization across China, India, and Southeast Asia.

- Leading Material Source: Primary aluminum is expected to lead through consistent quality standards by 69% market share in 2026, large-scale industrial throughput, and suitability for structural and high-performance anodized applications.

- Leading Application Area: Structural components are expected to lead through large-scale deployment in construction with 42% market share in 2026, transportation, and industrial equipment manufacturing.

| Key Insights | Details |

|---|---|

| Aluminum Anodizing Market Size (2026E) | US$2.7 Bn |

| Market Value Forecast (2033F) | US$3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Accelerating Automotive Lightweighting and EV Battery Enclosures

The global transition toward electric mobility is structurally accelerating aluminum anodizing demand. Electric vehicle architectures prioritize lightweight materials to optimize energy efficiency. Aluminum substitution reduces structural mass compared with conventional steel assemblies. Weight reduction directly enhances battery range and overall drivetrain performance. Anodizing provides dielectric insulation essential for high-voltage battery enclosures. The process also enhances corrosion resistance across chassis and structural components. These performance requirements elevate anodizing from decorative treatment to functional necessity. Consequently, demand concentrates around high-specification hard-coat applications supporting safety compliance.

The EV scaling reconfigures substrate and coating specifications. Thermal management requirements intensify surface engineering standards across enclosure systems. Regulatory scrutiny over electrical isolation reinforces certified anodizing performance benchmarks. Material selection increasingly integrates surface treatment compatibility during component design. This integration embeds anodizing earlier within automotive engineering workflows. Cost structures shift toward energy-intensive, precision-controlled processing environments. Higher specification coatings support margin differentiation through performance validation. Collectively, electrification structurally repositions anodizing within advanced mobility supply chains.

Aerospace Fleet Expansion and Modernization Initiatives

The global commercial aviation rebound directly strengthens aluminum anodizing demand structures. Aircraft modernization programs actively prioritize lightweight yet mechanically durable structural alloys. OEMs and tier suppliers specify anodized aluminum for fuselage skins and airframe subassemblies. Engineers apply controlled surface treatments to enhance fatigue resistance under cyclic pressurization loads. Operators confront extreme atmospheric exposure that necessitates advanced corrosion and wear mitigation strategies. Anodizing engineers form regulated oxide layers that ensure dimensional stability and microstructural integrity. These engineered properties satisfy stringent aerospace qualification protocols and compliance audits. Consequently, aerospace primes structure long-cycle procurement pipelines around high-specification finishing services.

Across the aerospace value chain, manufacturers enforce premium processing standards. Defense authorities codify coating thickness and performance under military-grade specifications. Regulators impose certification regimes that elevate compliance costs and entry barriers. Process engineers deploy advanced chemistries to increase hardness without substrate degradation. Quality teams institutionalize validation protocols that intensify documentation and traceability requirements. Thus, fleet expansion and defense procurement sustain innovation in high-performance anodizing technologies.

Barrier Analysis - Escalating Energy Intensity and Cost Structure Volatility

Aluminum anodizing remains inherently energy-intensive due to continuous electrochemical processing requirements. Aluminum anodizing operations consume substantial energy through continuous electrochemical conversion cycles. Engineers operate rectifiers, cooling baths, and current stabilization systems that require uninterrupted power delivery. Utilities across major industrial economies continue to raise electricity tariffs, inflating operating expenditure. Energy inputs now represent a significant proportion of total metal finishing conversion costs. Such tariff volatility destabilizes predictable pricing mechanisms within long-term contract manufacturing frameworks. Independent surface finishing firms experience intensified margin compression under fluctuating utility expenses. Producers struggle to pass incremental costs through price-sensitive downstream sectors. This structural imbalance erodes competitive positioning across fragmented and regionally dispersed processing networks.

Persistent energy inflation reshapes geographic competitiveness dynamics. Jurisdictions with subsidized grids secure structural cost advantages in anodizing operations. Corporate strategists redirect capital toward regions offering tariff stability and fiscal incentives. Smaller standalone facilities absorb disproportionate exposure to input price volatility. Smaller non-integrated facilities face disproportionate exposure to input volatility. Firms pursue consolidation strategies to capture scale efficiencies and risk mitigation. Consequently, overhead instability restricts capacity expansion and suppresses overall industry profitability.

Aggressive Regulatory Phase-outs of Chromic Acid

Environmental regulators, including the U.S. Environmental Protection Agency and the European Chemicals Agency under REACH mandates, are actively phasing out hexavalent chromium due to its carcinogenic risk profile. Authorization regimes impose stringent compliance thresholds and documentation obligations. Aerospace programs historically favored chromic acid for corrosion reliability. Legacy specifications embedded these treatments within certified manufacturing standards. Tightening oversight now subjects such processes to prolonged approval cycles. Regulatory scrutiny elevates administrative burden across finishing facilities. Uncertainty surrounding renewals disrupts long-term production planning stability. These constraints structurally challenge continuity within aerospace-qualified supply chains.

Transition toward boric, sulfuric, and alternative chemistries requires capital reinvestment. Process substitution demands extensive requalification and fatigue performance validation. Engineering workflows must be redesigned to maintain certification equivalence. Personnel retraining becomes necessary to uphold revised quality protocols. Equipment retrofitting increases fixed cost exposure for compliant facilities. Material compatibility assessments extend program lead times significantly. Supply chains confront temporary disruption during transitional qualification phases. Collectively, regulatory phase-outs reconfigure competitive dynamics across aerospace surface treatment markets.

Opportunity Analysis - Integration of Secondary and Recycled Aluminum

Escalating ESG mandates present a highly actionable opportunity to develop specialized anodizing processes tailored for recycled aluminum alloys. Automotive and electronics manufacturers increasingly prioritize low-emission and recycled material sourcing strategies. Sustainability mandates compel procurement teams to integrate secondary aluminum into supply portfolios. Metallurgical impurity variability destabilizes conventional anodizing bath chemistry equilibrium. Trace elements such as iron and silicon disrupt oxide layer uniformity and optical consistency. Traditional sulfuric acid chemistries frequently generate uneven coloration and surface defect formation. These process inconsistencies constrain full-scale substitution within premium automotive and consumer electronics applications.

Engineers, therefore, intensify research into adaptive electrochemical controls and alloy-specific parameter optimization. Sustained process innovation also becomes indispensable for economically viable circular material integration. Specialized chemistries engineered for recycled substrates unlock differentiated and higher-margin value pools. Adaptive bath formulations improve tolerance to compositional variability across secondary alloys. Advanced process control systems enhance defect mitigation and coating uniformity. European Union circular economy frameworks accelerate institutionalized recycled content adoption. Procurement teams increasingly embed carbon accounting into supplier qualification metrics. Thus, impurity-resilient anodizing platforms expand the addressable market for sustainable finishing solutions.

Biocompatible Titanium and Aluminum Medical Devices

The convergence of advanced healthcare and metallurgical technology creates profound unmet needs in medical device manufacturing. Anodized aluminum and titanium substrates form stable oxide barriers that resist physiological corrosion. Medical engineers specify these passivated surfaces to withstand repeated autoclaving and chemical sterilant exposure. Manufacturers leverage anodic coloration to enhance surgical instrument identification and procedural traceability. Orthopedic designers engineer controlled surface morphology to improve osseointegration and wear resistance. Device producers rely on micro-structured oxide layers to optimize biocompatibility and mechanical durability. Hospitals increasingly demand reusable instruments that maintain coating integrity under aggressive sterilization cycles. Global demographic aging accelerates procedural volumes across advanced and emerging healthcare systems.

Precision micro-anodizing capabilities also become embedded within critical medical device manufacturing workflows. The stringent certification frameworks elevate operational and validation requirements. Medical-grade anodizing facilities implement controlled environments and statistically validated process parameters. Manufacturers comply with quality systems such as ISO 13485 to ensure regulatory conformity. Cleanroom integration and electrolyte purity management reshape capital allocation priorities. Regulatory agencies enforce traceability from substrate sourcing through final surface finishing. Higher compliance thresholds ultimately sustain differentiated pricing and resilient segment profitability.

Category-wise Analysis

Material Type Insights

Primary aluminum is expected to lead, accounting for approximately 69% share in 2026, supported by its superior alloy purity and predictable electrochemical behavior across industrial finishing lines. Consistent substrate composition enables uniform oxide layer formation, minimizing rejection rates in high-volume automotive and aerospace workflows. Sulfuric acid anodizing processes particularly benefit from metallurgical stability, supporting dimensional control and coating integrity.

Defense and commercial aviation programs rely heavily on primary metal to satisfy stringent performance and safety specifications. Its established supply chains and qualification history reduce operational risks for tier suppliers. Continuous coil anodizing platforms deployed by Lorin Industries further reinforce throughput efficiency using primary rolls. Upstream suppliers including Rio Tinto and Norsk Hydro, anchor quality benchmarks for anodizing-grade sheet, sustaining ecosystem lock-in and structured procurement models.

Secondary aluminum is expected to be the fastest-growing segment, driven by intensifying ESG (Environmental, Social, & Governance) mandates and lifecycle carbon reduction targets across mobility and electronics sectors. Automotive manufacturers increasingly integrate recycled substrates to align with sustainability reporting frameworks and procurement decarbonization goals. Historically, impurity variability constrained anodic consistency and aesthetic outcomes.

Advanced pre-treatment chemistries and adaptive bath formulations now mitigate alloy heterogeneity challenges. Strategic investments by Novelis and Constellium in anodizing-quality recycled sheet accelerate qualification within premium applications. As hybrid billet engineering and low-carbon branding mature, secondary substrates increasingly embed within enterprise sustainability frameworks, reshaping material sourcing economics across the anodizing ecosystem. Process control innovations improve coating uniformity and reduce defect incidence in recycled inputs. As circular economy policies strengthen and cost efficiencies improve, secondary aluminum integration accelerates across value chains, positioning this segment for sustained expansion relative to conventional primary sourcing.

Application Area insights

Structural components are anticipated to lead, accounting for approximately 42% share in 2026, anchored by sustained infrastructure investment and aerospace manufacturing intensity. Extruded beams, load-bearing profiles, and transport frameworks utilize anodized alloys to maximize strength-to-weight efficiency and long-term corrosion immunity. Structural engineers specify anodized finishes to extend service life under cyclic loading and harsh environmental exposure.

Manufacturers align these applications with architectural performance codes and aerospace hard-coat specifications to ensure qualification continuity. Such compliance regimes elevate technical entry barriers and reinforce disciplined supplier approval processes. Prime contractors consequently embed certified finishers within repeat procurement and multi-year structural programs. Continuous coil anodizing platforms operated by Lorin Industries enable scalable throughput for architectural and transportation substrates. Similarly, hard-coat process specialization at Aalberts Surface Technologies underpins high-performance structural and aerospace assemblies. Integrated building systems from Norsk Hydro further embed anodized extrusions within global construction ecosystems, sustaining predictable demand across long-duration assets.

EV battery enclosures are expected to be the fastest-growing segment, propelled by accelerating electric mobility adoption and escalating thermal management requirements. Electric vehicle battery housings incorporate dielectric anodic layers to mitigate short-circuit risk while preserving lightweight structural rigidity. Design engineers specify electrically insulating oxide coatings to isolate high-voltage modules from conductive chassis components. Manufacturers must balance dielectric strength with minimal mass addition to maintain vehicle efficiency targets.

Next-generation high-voltage architectures operating above 800 volts amplify insulation performance requirements. These systems subject enclosures to sustained electrical stress, thermal cycling, and coolant exposure. Accordingly, producers increasingly deploy hard-coat anodizing processes that deliver high breakdown voltage and abrasion resistance. Alloy innovations from Constellium and specialized finishing expansions by Aalberts Surface Technologies are aligning capacity with large-format enclosure designs. As automotive suppliers integrate dedicated EV finishing lines, anodized battery systems increasingly anchor next-generation drivetrain safety and performance standards.

Regional Insights

Asia Pacific Aluminum Anodizing Market Trends

Asia Pacific is expected to remain the leading and fastest-growing regional market, accounting for approximately 48% of global aluminum anodizing demand in 2026, anchored by its unparalleled manufacturing scale and vertically integrated metals ecosystem. The region is positioned to dominate volume throughput across consumer electronics, electric mobility, architectural systems, and industrial machinery, supported by dense supplier clusters, cost-competitive labor structures, and proximity to downstream OEM assembly hubs.

Expanding electric vehicle production corridors, rapid urban infrastructure buildout, and sustained export-oriented electronics manufacturing are expected to reinforce high-capacity Type II and hard-coat anodizing utilization. Policy frameworks across major economies are anticipated to gradually tighten environmental oversight while preserving industrial competitiveness, accelerating automation, effluent treatment upgrades, and chrome-free process transitions. The regional competitive structure is likely to remain fragmented at the mid-tier while consolidating at the top, as large integrated aluminum producers and automotive suppliers internalize finishing capabilities to secure quality control, cost predictability, and supply continuity.

China is expected to function as the structural anchor of regional momentum, shaping pricing dynamics, capacity expansion, and technology adoption across Asia Pacific. National industrial policy is anticipated to prioritize electric vehicle scaling, advanced manufacturing digitization, and green metallurgy, driving investment in large-format anodizing lines tailored for battery enclosures and structural extrusions.

Domestic OEMs and multinational suppliers are projected to expand captive finishing operations near automotive and electronics clusters, reinforcing localized supply chains and reducing export dependency risks. As China advances chrome-free chemistries, plasma electrolytic oxidation, and data-driven quality control systems, regional vendors are expected to align with higher-specification standards, strengthening Asia Pacific’s position as the primary global production and innovation hub for aluminum anodizing applications.

North America Aluminum Anodizing Market Trends

North America is expected to remain a structurally stable and mature market, with demand anchored in aerospace, defense, advanced automotive, and high-specification industrial applications rather than volume-driven expansion. The region is positioned to sustain steady replacement cycles and compliance-led upgrades, supported by deep engineering capabilities, vertically integrated OEM ecosystems, and strong institutional procurement frameworks.

Aerospace and defense programs are anticipated to reinforce demand for MIL-spec hard-coat and precision anodizing, while localized electric vehicle supply chain build-outs are expected to expand the requirement for dielectric and corrosion-resistant coatings in battery enclosures and lightweight structural systems. The competitive environment is likely to remain consolidated, favoring NADCAP-accredited and defense-qualified Tier-1 finishers capable of sustaining rigorous audit, traceability, and fatigue-performance standards.

The U.S. is expected to function as the primary regional anchor, shaping technology direction, regulatory alignment, and capital deployment across North America. Federal environmental enforcement is anticipated to accelerate the transition from legacy chromic acid processes toward boric-sulfuric acid anodizing and other compliant systems, reinforcing investment in automation, digital bath monitoring, and zero-discharge platforms. Defense modernization initiatives and commercial aircraft production programs are projected to sustain high-margin contracts for certified surface treatment providers, strengthening barriers to entry. Automotive OEMs are likely to expand domestic anodizing capacity in parallel with EV platform scaling, prioritizing lightweight structural components and thermally resilient enclosures.

Europe Aluminum Anodizing Market Trends

Europe is expected to remain a mature market, with demand anchored in premium automotive engineering, commercial aerospace production, and sustainability-driven architectural applications. The region is positioned to emphasize performance optimization, regulatory compliance, and lifecycle decarbonization rather than large-scale capacity expansion. Extreme lightweighting strategies across OEMs such as BMW, Mercedes-Benz, and Volkswagen are expected to reinforce demand for high-specification hard anodizing in structural and chassis components.

Aerospace programs led by Airbus are projected to sustain premium MIL-compliant surface treatments for fuselage assemblies and interior systems. Regulatory harmonization under REACH is anticipated to continue reshaping process chemistry, accelerating the phase-out of chromic acid systems and driving investment in eco-efficient alternatives. Elevated energy costs are likely to sustain operational pressure, favoring technologically advanced operators with automated, closed-loop anodizing infrastructure and integrated recycling capabilities.

Germany is expected to function as the regional anchor, shaping innovation standards, supplier qualification protocols, and sustainability integration across Europe. Industrial clusters surrounding automotive and aerospace manufacturing are projected to intensify collaboration between OEMs and specialized surface engineering firms such as Aalberts Surface Technologies and Bodycote, reinforcing high-barrier certification ecosystems. Vertically integrated aluminum producers, including Norsk Hydro, are expected to advance circular economy initiatives by scaling anodizing solutions tailored for secondary alloys, aligning with the coordinated industrial strategy. This strategy is set to preserve Europe’s premium positioning, characterized by technological refinement, regulatory stringency, and sustainability-led competitive differentiation.

Competitive Landscape

The global aluminum anodizing market exhibits moderate consolidation at the upper tier, led by globally certified surface engineering specialists such as Bodycote, Pioneer Metal Finishing, and Linetec. While overall market share remains distributed, influence at the premium end is driven less by scale and more by certification depth, aerospace and defense approvals, and the ability to execute high-specification hard-coat and MIL-compliant anodizing programs. In aerospace and advanced automotive applications, NADCAP accreditation and OEM-qualified process controls create significant entry barriers, concentrating high-value contracts among a limited pool of validated providers.

Architectural and decorative anodizing, by contrast, remains more price-competitive and regionally fragmented, with smaller operators competing on throughput efficiency and proximity to extrusion and fabrication hubs. Competitive advantage increasingly depends on regulatory credibility, metallurgical expertise, and integrated service portfolios spanning pretreatment, anodizing, sealing, and quality analytics. Larger groups leverage multi-site networks aligned with aerospace and EV manufacturing corridors, while regional specialists focus on niche industrial and medical applications. Ongoing consolidation, automation adoption, and digital bath monitoring are expected to further standardize operations and reinforce compliance resilience.

Key Industry Developments:

- In February 2026, Novelis Inc. provided a major update on its Oswego hot mill, projecting a restart late in the second quarter of 2026 following fire-related delays. Restoring this facility is critical to stabilizing the North American automotive aluminum sheet supply chain, which heavily relies on this site for anodizable products.

- In December 2025, Constellium SE launched new aluminum finishing lines at its German plant to capture growing high-value application demand. These lines are specifically designed to address the tightening technical specifications required by European automotive and industrial OEMs.

- In August 2025, Henkel Adhesive Technologies launched Bonderite M-AD 2000A, a new additive for the anodizing process. This additive allows anodizing baths to operate at temperatures up to 24°C (up from 18-20°C), reducing cooling energy, lowering sulfuric acid use by 25%, and shortening process times by 15%.

Companies Covered in Aluminum Anodizing Market

- Bodycote

- Aalberts Surface Technologies

- Pioneer Metal Finishing

- Norsk Hydro

- Arconic

- Linetec

- Henkel

- Lorin Industries

- Techmetals Inc.

- SAF Southern Aluminum Finishing

- Alumet Inc.

- Saporito Finishing Co.

- Anoplate

- Alumeco Group

- Bonnell Aluminum

- Chicago Anodizing Company

Frequently Asked Questions

The global aluminum anodizing market is projected to be valued at US$2.7 billion in 2026 and is expected to reach US$3.8 billion by 2033, driven by accelerating electric vehicle production, aerospace fleet modernization, and expanding architectural demand for corrosion-resistant structural components.

Electric vehicle architectures increasingly rely on lightweight aluminum structures to enhance range and thermal efficiency. Anodizing provides dielectric insulation for high-voltage battery enclosures, improves corrosion resistance under thermal cycling, and supports compliance with evolving electrical safety regulations, thereby embedding surface treatment earlier in automotive design workflows.

The aluminum anodizing market is forecast to grow at a CAGR of 5.0% from 2026 to 2033, reflecting steady expansion across automotive lightweighting, aerospace structural applications, and sustainability-driven substitution of heavier metallic alternatives.

Asia Pacific is the leading regional market, accounting for approximately 48% share, supported by vertically integrated aluminum production, high-volume consumer electronics manufacturing, expanding EV supply chains, and sustained infrastructure development across China and India.

The aluminum anodizing market is moderately consolidated at the upper tier, with key players including Bodycote, Aalberts Surface Technologies, Pioneer Metal Finishing, Norsk Hydro, Arconic, and Linetec. These companies compete through certification depth, aerospace and automotive qualification portfolios, vertically integrated capabilities, and investment in automated, environmentally compliant anodizing systems.