- Specialty & Fine Chemicals

- Organoaluminum Market

Organoaluminum Market Size, Share, and Growth Forecast, 2026 - 2033

Organoaluminum Market by Product Type (Trialkylaluminum, Alkylaluminum Halides, Alkylaluminum Hydrides), Application (Catalysts, Chemical Intermediates, Pharmaceuticals), End-user (Petrochemicals, Others), and Regional Analysis for 2026 - 2033

Organoaluminum Market Size and Trends Analysis

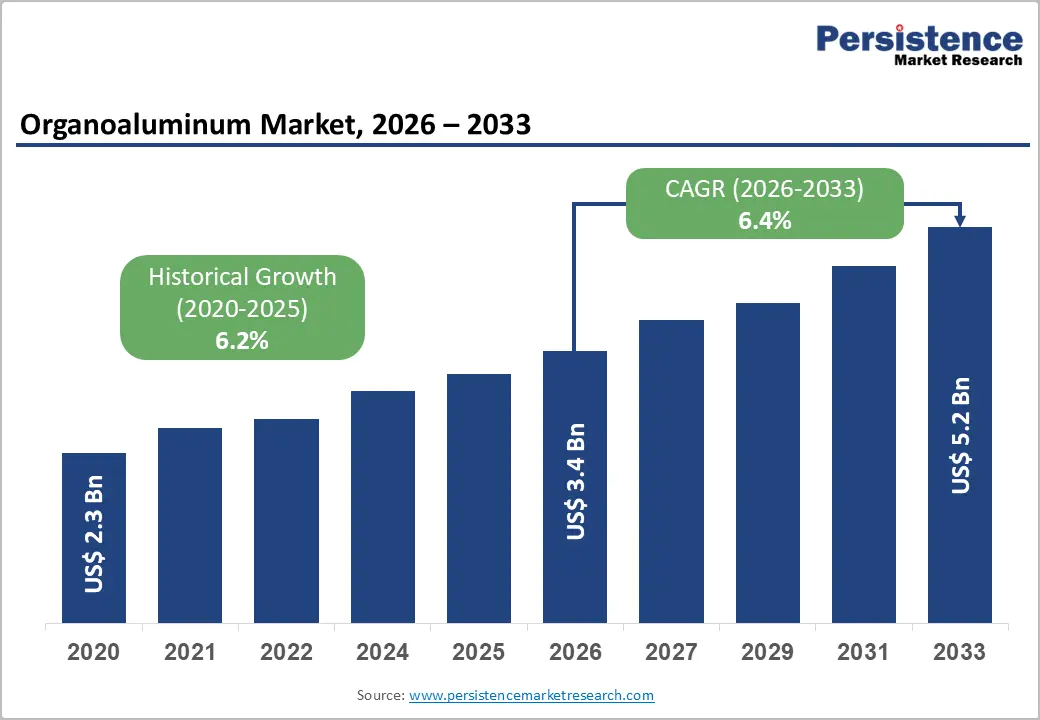

The global organoaluminum market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$5.2 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by the expansion of polyolefin production and increasing demand for catalysts, as organoaluminum compounds play a critical role as co-catalysts in Ziegler–Natta and metallocene systems widely used in petrochemical processes.

Insights from the International Energy Agency indicate that global aluminum-related industrial output surpassed 220 million metric tons in 2023, reflecting a steady growth alongside rising demand for polymers and advanced materials, particularly across energy transition and industrial end-use sectors.

Key Industry Highlights:

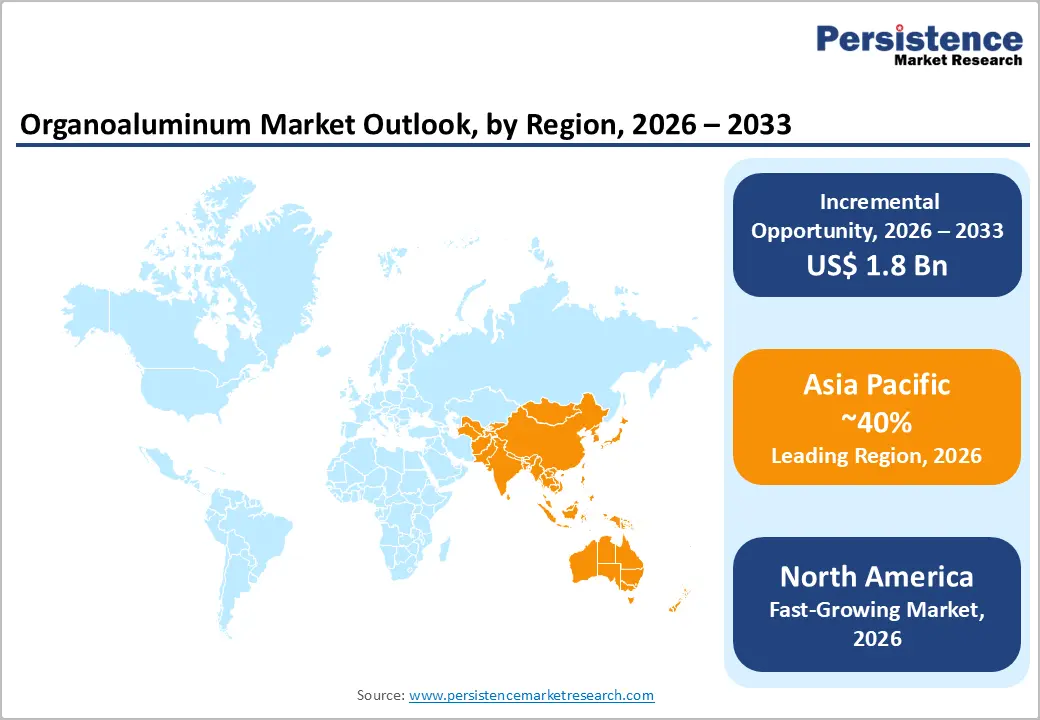

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by large-scale manufacturing growth and increasing catalyst demand.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by strong petrochemical activity in the U.S. and aerospace-linked demand in Canada.

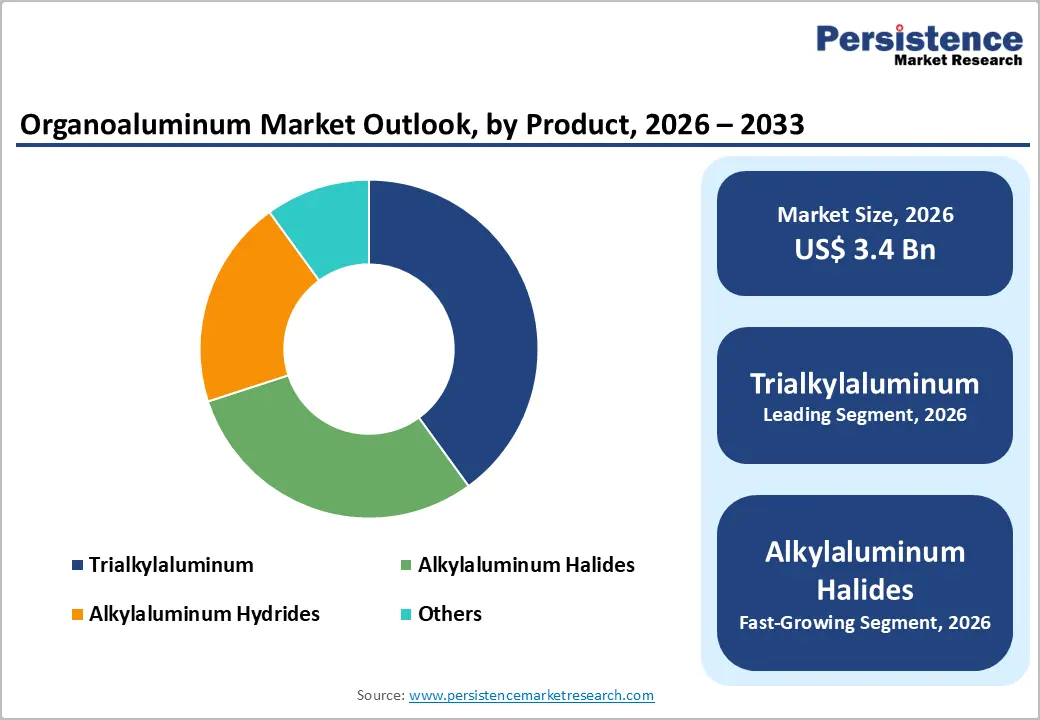

- Leading Product Type: Trialkylaluminum is projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by high reactivity in polymerization catalysts and strong use in olefin processing.

- Leading Application: Catalysts are anticipated to be the leading application, accounting for over 55% of the revenue share in 2026, supported by extensive use in Ziegler-Natta systems and rising demand from polymer manufacturing.

- Key Opportunity: Driven by expanding demand for advanced polyolefin catalysts, high-purity organometallics in pharmaceuticals, and sustainable high-efficiency chemical manufacturing technologies across end-use industries.

DRO Analysis

Driver - Expanding Pharmaceutical Synthesis Applications

Their strong reducing properties and controlled reactivity make them valuable in API (active pharmaceutical ingredient) production and intermediate synthesis. Growing demand for advanced therapeutics, precision medicines, and high-purity compounds has significantly increased reliance on organoaluminum chemistry. Pharmaceutical manufacturers are increasingly adopting organometallic routes to improve yield efficiency, reaction selectivity, and cost-effectiveness.

WHO Essential Medicines List expansion and growing biosimilar approvals are elevating demand for precision synthesis reagents, positioning organoaluminum compounds as strategically important inputs in regulated pharmaceutical supply chains globally.

Organoaluminum compounds support scalable pharmaceutical manufacturing processes, particularly in producing chiral intermediates and specialty molecules. Their role in facilitating selective bond formation improves synthesis efficiency and reduces by-product formation, aligning with modern pharmaceutical quality standards.

Restraint - Stringent Regulatory Compliance for Pyrophoric Compounds

Trialkylaluminum compounds are classified as highly pyrophoric substances under the Globally Harmonized System (GHS) of Classification, imposing significant regulatory compliance burdens on transportation, storage, and handling operations. OSHA (U.S.) and REACH (EU) mandate specialized containment infrastructure, trained personnel, and dedicated supply chain protocols.

These requirements substantially increase operational overhead for mid-tier manufacturers, limiting market participation to well-capitalized players with established safety systems and constraining supply network scalability in emerging markets and across new geographies. Companies must invest heavily in specialized storage infrastructure, safety systems, and trained personnel to ensure safe handling.

Opportunity - Green Chemistry and Sustainable Synthesis Initiatives

Manufacturers are increasingly focusing on reducing environmental impact by developing cleaner catalytic processes and improving reaction efficiency. Organoaluminum compounds play a key role in enabling atom-economical reactions and minimizing waste generation in polymer and fine chemical production.

The European Green Deal and U.S. Inflation Reduction Act (IRA) incentivize investments in cleaner industrial chemistry. Governments and regulatory bodies are promoting sustainable manufacturing practices, encouraging companies to invest in eco-friendly chemical solutions. This is particularly relevant in polymer production, where demand for low-emission and recyclable materials is increasing.

Organoaluminum compounds play a key role in enabling atom-economical reactions and minimizing waste generation in polymer and fine chemical production. Growing emphasis on sustainability in the petrochemical and pharmaceutical industries is encouraging the shift toward more environmentally responsible production technologies. Advancements in catalyst design and process optimization are supporting the development of more energy-efficient and less hazardous organoaluminum formulations.

Category-wise Analysis

Product Type Insights

Trialkylaluminum is expected to lead the organoaluminum market, accounting for approximately 45% of revenue in 2026, driven by its extensive use in polymerization catalysts for olefin production. Its high reactivity and strong alkylating ability make it essential in Ziegler-Natta and metallocene catalyst systems, which are widely used in producing polyethylene and polypropylene. A notable example includes triethylaluminum, which is extensively used in large-scale polyethylene production facilities operated by major petrochemical companies.

Alkylaluminum halides are likely to represent the fastest-growing segment, supported by increasing demand in pharmaceutical intermediates and specialty chemical synthesis, with strong process selectivity and stability. Pharmaceutical manufacturers are increasingly using these compounds to improve yield and purity in complex drug molecule synthesis. For example, aluminum-based halide reagents are used in the synthesis of advanced intermediates for active pharmaceutical ingredients.

Application Insights

Catalysts are projected to lead the market, capturing around 55% of the revenue share in 2026, supported by their critical role in petrochemical polymerization processes. Organoaluminum compounds act as co-catalysts in Ziegler-Natta and metallocene systems, enabling efficient production of polyolefins such as polyethylene and polypropylene. A notable example includes, in industrial polyethylene manufacturing plants, trialkylaluminum compounds are widely used to activate titanium-based catalyst systems.

Chemical intermediates are likely to be the fastest-growing application, driven by increasing demand in pharmaceutical synthesis and specialty chemical production, where organoaluminum compounds are used for selective organic transformations. These intermediates are essential in producing complex molecular structures with high efficiency and purity. For example, organoaluminum reagents are used in the synthesis of fine chemical intermediates for antiviral and oncology drug pipelines, where precision and yield optimization are critical.

End-user Insights

The petrochemical industry is expected to lead the organoaluminum market, accounting for approximately 50% of revenue in 2026, driven by its extensive use in polymer production and catalytic processes. Organoaluminum compounds play a vital role in enabling large-scale production of polyolefins through advanced catalyst systems, ensuring high efficiency and product consistency. For instance, in major polyethylene production complexes, organoaluminum compounds are used to activate catalyst systems that produce high-density polyethylene used in packaging films and industrial containers.

Pharmaceuticals are likely to represent the fastest-growing segment, supported by increasing demand for advanced drug synthesis and high-purity chemical intermediates. Organoaluminum compounds are widely used in pharmaceutical manufacturing due to their efficiency in facilitating complex organic reactions and improving synthesis selectivity. For example, organoaluminum reagents are used in the synthesis of specialty intermediates for cardiovascular and oncology drugs, where precision and controlled reaction pathways are essential.

Regional Insights

North America Organoaluminum Market Trends

North America is likely to be the fastest-growing region, driven by strong demand from petrochemicals, polymer production, and specialty chemical synthesis. The rising focus on process efficiency and low-emission chemical manufacturing is encouraging the adoption of high-purity organoaluminum compounds. Companies such as Albemarle Corporation advance catalyst innovation through organometallic solutions for polyolefin production.

U.S. Organoaluminum Market Trends

The U.S. dominates the regional market, driven by strong petrochemical capacity expansion along the Gulf Coast, with increasing investments in polyethylene and polypropylene production facilities. Growth is supported by increasing demand for high-performance polymers in packaging, automotive, and industrial applications. The U.S. is also witnessing a shift toward energy-efficient and low-emission chemical production processes.

Canada Organoaluminum Market Trends

Canada is a significant market for organoaluminum, supported by aerospace materials, specialty chemicals, and industrial applications. The country is increasingly focusing on high-value chemical production and advanced material development. Recent developments include growing investments in sustainable chemical manufacturing and cleaner production technologies aimed at reducing environmental impact.

Europe Organoaluminum Market Trends

Europe is likely to be a significant market for organoaluminum in 2026, due to catalysts used in polymer production, pharmaceutical synthesis, and specialty chemical applications. Growth is supported by increasing R&D investments in advanced materials and precision chemicals. Companies such as BASF SE develop advanced catalyst systems and organometallic solutions that enhance polymerization efficiency and specialty chemical production in Europe.

U.K. Organoaluminum Market Trends

In the U.K., the organoaluminum market is driven by strong pharmaceutical innovation, specialty chemical production, and robust R&D activities. The country is increasingly focusing on advanced catalyst development and high-value chemical synthesis applications. Recent trends include a growing shift toward sustainable manufacturing practices and rising investments in environmentally friendly chemical processes.

Germany Organoaluminum Market Trends

Germany dominates the regional market, driven by strong chemical manufacturing capabilities and advanced industrial infrastructure. The country is a major hub for high-performance polymer production and catalyst development, with a strong focus on green chemistry and sustainable industrial processes. Germany is also strengthening its position in specialty chemicals and industrial polymers.

Asia Pacific Organoaluminum Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by rapid industrialization, expanding petrochemical capacity, and strong demand for polymer production across developing economies. Growth is supported by cost-effective manufacturing bases and the strong expansion of chemical production hubs. A key example includes China Petroleum & Chemical Corporation (Sinopec), which extensively uses organoaluminum-based catalyst systems in large-scale polyethylene and polypropylene production.

China Organoaluminum Market Trends

China dominates the regional market, driven by massive petrochemical capacity, strong government-backed industrial expansion, and rising polymer demand. The country is a leader in polyethylene and polypropylene production, heavily relying on advanced catalyst systems. China is also investing in high-efficiency chemical manufacturing technologies and next-generation polymerization processes.

India Organoaluminum Market Trends

India is a significant market, supported by rapid growth in petrochemical plants, pharmaceutical manufacturing, and packaging industries. The country is witnessing a strong expansion in domestic chemical production to reduce import dependency and enhance self-reliance. Recent developments include new refinery and polymer projects, along with increasing investments in specialty chemicals and industrial materials.

Competitive Landscape

The global organoaluminum market exhibits a moderately fragmented structure, driven by strong demand from polyolefin catalysts, pharmaceutical synthesis, and specialty chemical applications. The industry is dominated by large multinational chemical companies with advanced production capabilities, proprietary catalyst technologies, and integrated supply chains that ensure high product purity and consistent performance in sensitive polymerization processes.

With key leaders including Albemarle Corporation, BASF SE, Nouryon, AkzoNobel N.V., Evonik Industries AG, LANXESS AG, Mitsui Chemicals Inc., and Gulbrandsen Chemicals, the market is characterized by strong R&D investment and long-term supply contracts with petrochemical and polymer manufacturers. These companies maintain competitive advantages through vertical integration.

Key Industry Developments:

- In April 2025, LANXESS completed the sale of its remaining polymer business, fully transitioning into a pure specialty chemicals company. This strategic shift strengthens its focus on chemical intermediates, additives, and catalyst-related materials, aligning with growing demand from the petrochemical and advanced materials industries.

- In August 2025, Albemarle Corporation announced an enhanced organizational structure aimed at improving agility, operational efficiency, and alignment with its market-led growth strategy. The restructuring integrates key functions such as manufacturing, supply chain, capital management, and resource optimization under a more unified leadership model.

Companies Covered in Organoaluminum Market

- Albemarle Corporation

- AkzoNobel N.V.

- BASF SE

- LANXESS AG

- Mitsui Chemicals Inc.

- Nouryon

- Evonik Industries AG

- Chemtura Corporation

- Gulbrandsen Chemicals

- Sasol Limited

- WeylChem International GmbH

- Huntsman Corporation

- Momentive Performance Materials Inc.

Frequently Asked Questions

The global organoaluminum market is projected to reach US$3.4 billion in 2026.

Rising demand for polyolefin catalysts and expanding applications in petrochemical polymerization, pharmaceuticals, and specialty chemical synthesis drive the organoaluminum market.

The organoaluminum market is expected to grow at a CAGR of 6.4% from 2026 to 2033.

Expansion in high-performance polymer production, growing pharmaceutical intermediate synthesis, and increasing adoption of advanced catalyst technologies in sustainable chemical manufacturing.

Albemarle Corporation, AkzoNobel N.V., BASF SE, LANXESS AG, Mitsui Chemicals Inc, and Nouryon are the leading players.