Industry: Healthcare

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 188

Report ID: PMRREP33182

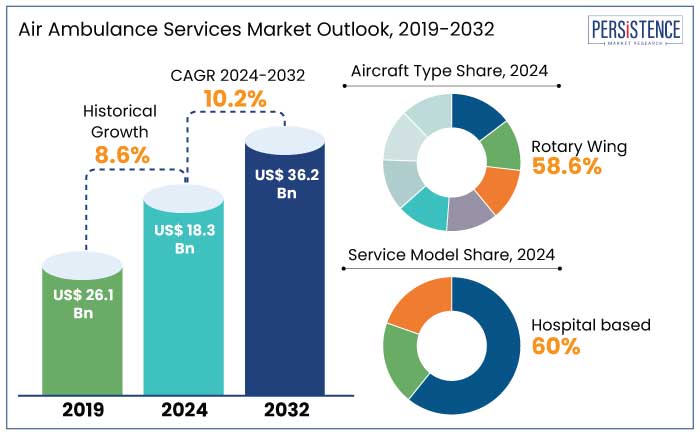

The air ambulance services market is estimated to increase from US$ 19.1 Bn in 2025 to US$ 37.1. Bn by 2032. The market is projected to record a CAGR of 10.2% during the forecast period from 2025 to 2032.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Air Ambulance Services Market Size (2025E) |

US$ 19.1 Bn |

|

Projected Market Value (2032F) |

US$ 37.1 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

10.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

8.6% |

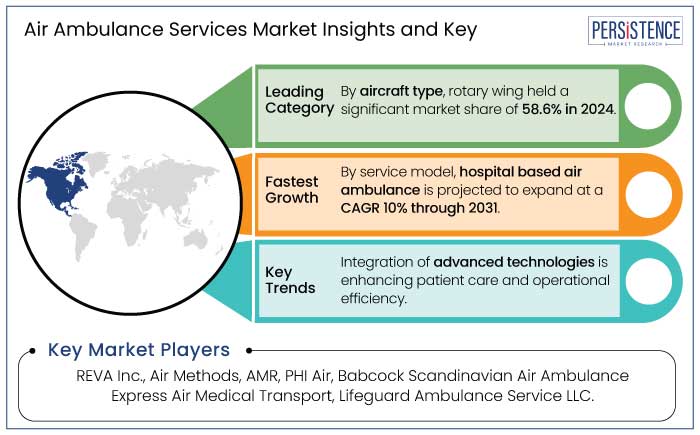

North America is estimated to hold a market share of 38% in 2025. The region continues to dominate the market recording a significant growth rate. The regional market growth is due to the presence of different air ambulance service providers. Another key driver for market growth is favorable reimbursement policies.

Increased public and healthcare sector awareness regarding the advantages of air ambulance services contributes to the regional market growth further. The presence of a well-established infrastructure for medical airplane transportation is anticipated to create new opportunities. In addition, favorable reimbursement policies and the emergence of various prominent service providers are projected to propel demand.

Rotary-wing aircraft, mainly helicopters are estimated to hold a market share of 58.9% in 2025 due to their ability to access remote areas and provide quick emergency response. Their vertical takeoff and landing capability allow direct transport from emergency sites to hospitals, ensuring rapid care, especially in urban inter-facility transfers.

Helicopters are also equipped with advanced medical technology, further solidifying their role in critical care transport. Fixed-wing aircraft, on the other hand, are preferred for long-distance travel due to their superior fuel capacity and ability to operate in adverse weather conditions.

They carry more medical equipment and personnel, making them ideal for extended transports. Common models include Learjet 31, King Air 200, and Pilatus PC-12. This segment has seen growth, driven by increasing medical tourism. Leading companies in both sectors include REVA Inc., PHI, AirMed International, and Scandinavian Air Ambulance.

|

Hospital-based air ambulance services are estimated to dominate the market with a CAGR of 10% and to account for a 61% of the market share due to their strong integration with hospital networks. Managed by or affiliated with leading hospitals, these services provide direct access to specialized medical teams and equipment, ensuring high-quality care during transit. Their centralized operations improve coordination and response times, making them essential for emergencies like trauma and cardiac care. Growing hospital investments in advanced fleets and critical care systems further reinforce their leading market position. |

Domestic air ambulance services maintained dominance in the market and to exhibit a share of 58.4% in 2025 due to the high demand for emergency medical transport and inter-facility patient transfers within national boundaries. These services are critical for reaching patients in rural, suburban, and urban areas where timely medical care can mean the difference between life and death.

Domestic operations are more accessible and cost-effective compared to international services, making them the preferred choice for both healthcare providers and patients. Additionally, rotary-wing aircraft, commonly used in domestic services, allow for direct scene responses and hospital transfers, further boosting their utility.

As the need for rapid medical response grows, particularly in emergencies or underserved areas, domestic services continue to be the backbone of the air ambulance industry, driving their market dominance.

The air ambulance services market has experienced significant growth, driven by advancements in medical technology, the rising demand for rapid emergency response, and the need for access to specialized care, particularly in rural and remote areas. Advanced medical equipment, such as ventilators, defibrillators, and telemedicine systems, has been integrated into air ambulances, improving patient care during transport.

Hospital-based services, which account for the largest market share, are increasingly in demand for inter-facility transfers, ensuring critical care during transport. Rotary-wing aircraft, like helicopters, are especially valuable for accessing hard-to-reach locations, as demonstrated by services like CareFlight in Australia, which provides medical transport to underserved regions.

International air ambulance services are expanding, primarily for patient repatriations and non-emergency medical transfers. Insurance companies are also including air ambulance coverage, making these services more accessible. These trends are reshaping the market, improving the efficiency and availability of air medical transport globally.

The air ambulance services market has experienced steady historical growth, driven by increasing demand for rapid medical response, advancements in aviation and medical technologies, and the need for improved access to healthcare in remote areas. Initially, air ambulances were primarily used for emergency response in difficult-to-reach locations, but over time, they have evolved into critical components of healthcare systems,

Technological advancements, such as the integration of telemedicine and advanced medical equipment onboard, have further enhanced the quality of care during transport, contributing to the market expansion. The rise in hospital-based services has also bolstered growth, as hospitals increasingly invest in their own air ambulance fleets to ensure timely patient transfers.

The market is poised for continued growth, driven by increasing demand for both domestic and international air medical services, advancements in aircraft technology, and the expansion of insurance coverage. As healthcare providers continue to invest in faster and efficient air transport solutions, the future of the air ambulance services market looks promising, with great accessibility and improved patient outcomes on the horizon.

Increasing Healthcare Expenditure to Boost Market Growth

Increasing healthcare expenditure is a significant driver for the air ambulance services market growth globally. According to the World Health Organization’s 2023 global health expenditure report, global health spending reached a record high of US$ 9.8 trillion in 2021, accounting for 10.3% of global GDP.

The distribution of this spending remains highly unequal, with low-income countries struggling to allocate sufficient funds for healthcare, despite external aid. The COVID-19 pandemic further underscored the importance of strong healthcare systems, leading to increased investments in healthcare infrastructure, especially in emerging markets.

In high-income countries, per capita healthcare spending is significantly higher, which supports the growth of advanced medical services, including air ambulance services. The growing focus on improving healthcare infrastructure, along with increasing investments in medical transport services, is expected to significantly boost the market globally through 2032.

Supportive Government Initiatives & High Spending on Healthcare Research and Development

Supportive government initiatives and increased spending on healthcare research and development are significant drivers of the air ambulance services market. Governments around the world are recognizing the need for advanced emergency medical services and are investing significantly in air ambulance systems to ensure rapid and effective patient transport.

In the United States, for example, government programs such as Medicare and Medicaid help cover the cost of air ambulance services, making them more accessible to a larger population. In Europe, countries like Germany and the UK have invested in improving their air ambulance fleets and infrastructure to better serve their populations, particularly in remote or underserved areas.

High spending on healthcare research and development is driving innovation in air ambulance technologies. Advances in telemedicine, medical equipment, and aircraft design are allowing air ambulances to offer highly specialized care while transporting patients. This is particularly important in regions like China and India, where government investment in healthcare infrastructure is enhancing air ambulance services.

High Operational Costs of Air Ambulance Services

High operational costs are a significant restraint for the air ambulance services market. Air ambulance transports, including both rotary-wing (helicopter) and fixed-wing (airplane) services, incur substantial expenses due to factors like fuel, maintenance, medical equipment, staffing, and insurance.

In 2017, the median cost for a rotary-wing transport was $36,400, and for fixed-wing services, it was $40,600, making air ambulance transport one of the most expensive healthcare services.

Furthermore, the Airline Deregulation Act of 1978 prevents states from regulating air carriers’ prices, including those for air ambulance services, resulting in price variability and financial challenges for both providers and patients.

Many privately insured patients face significant out-of-pocket expenses despite insurance coverage as insurance may not fully cover these high costs. The combination of these high operational costs and inconsistent reimbursement policies creates a key barrier to expanding access to air ambulance services, limiting market growth.

Insurance and Reimbursement Barriers in the Air Ambulance Services Market

Insurance coverage and reimbursement issues are significant restraint for the air ambulance services market. Air ambulance transports, both rotary-wing (RW) and fixed-wing (FW), are typically covered by private insurance, Medicare, and Medicaid only when ground ambulance transportation is deemed inappropriate.

Insurance payers often make the determination of medical necessity retroactively, particularly in emergency situations, leading to the risk of surprise balance billing. This situation arises because air ambulance providers typically do not inquire about insurance before services are rendered.

The cost of air ambulance services includes both fixed charges and variable charges based on mileage, with additional adjustments for geographic location. For example, the median price for RW transport was $36,400, and for FW transport, it was $40,600 in 2017. However, public programs like Medicare reimburse at significantly lower rates. In 2016, the median Medicare reimbursement for rotary-wing aircraft was only $4,814.

Although Medicare and Medicaid enrollees cannot be balance-billed, the low reimbursement rates and potential for out-of-pocket expenses create financial strain, hindering market growth.

Expanding in Untapped Regions Presents Growth Opportunities

Expanding into untapped regions presents a significant opportunity for growth in the air ambulance market. Many rural, remote, and underserved areas, particularly in developing countries or regions with limited access to advanced medical care, remain under-served by air ambulance services.

As healthcare infrastructure improves and demand for emergency medical services rises globally, there is a growing need for timely and efficient air transport, especially in emergencies where ground transportation may not be viable. For example, in regions like sub-Saharan Africa and parts of Southeast Asia, air ambulance services can drastically reduce response times and improve patient outcomes in critical situations.

Companies that establish a presence in these areas can leverage advancements in both rotary-wing and fixed-wing aircraft, offering specialized services for trauma, cardiac, and other emergency medical needs. Additionally, governmental support and funding for healthcare infrastructure in these regions further boost the potential for air ambulance operators to expand their services, tapping into previously underserved markets.

The air ambulance services market is competitive, with leading players like REVA Inc., PHI Air Medical, and AirMed International leading the sector. These companies offer advanced medical equipment and rapid emergency response.

Regional players, such as Scandinavian Air Ambulance, are expanding, focusing on specialized services like pediatric and cardiac transport. Geographic expansion into underserved areas further boosts competition, allowing companies to capture greater market share.

Recent Developments in the Air Ambulance Services Market

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Aircraft Type

By Service Model

By Service Type

By Region

To know more about delivery timeline for this report Contact Sales

The market is estimated to increase from US$ 19.1 Bn in 2025 to US$ 37.1 Bn by 2032.

The industry is propelled by increasing demand for rapid emergency medical transport.

Some of the leading industry players in the market are REVA Inc., PHI Air Medical, and AirMed International.

The market is projected to record a CAGR of 10.2% through 2032.

A prominent opportunity in the market is expanding into underserved and remote regions.