Industry: IT and Telecommunication

Published Date: December-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 181

Report ID: PMRREP13330

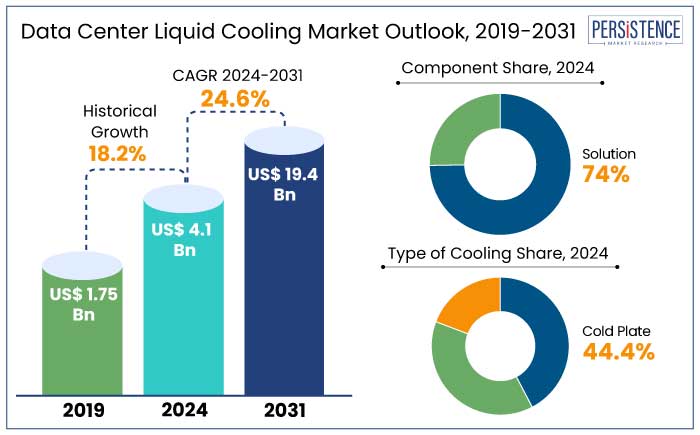

The data center liquid cooling market is estimated to increase from US$ 4.1 Bn in 2024 to US$ 19.4 Bn by 2031. The market is projected to record a CAGR of 24.6% during the forecast period from 2024 to 2031.

Data centers are being compelled to implement more sustainable processes due to strict laws and environmental concerns. When it comes to energy efficiency, liquid cooling is far superior to air cooling.

A recent study claims that liquid cooling systems can cut the amount of energy used for data center cooling by as much as 40%. Liquid immersion cooling has been tested by Microsoft and other companies for their Azure data centers, showing up to 15% more energy efficiency than conventional techniques.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Data Center Liquid Cooling Market Size (2024E) |

US$ 4.1 Bn |

|

Projected Market Value (2031F) |

US$ 19.4 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

24.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

18.2% |

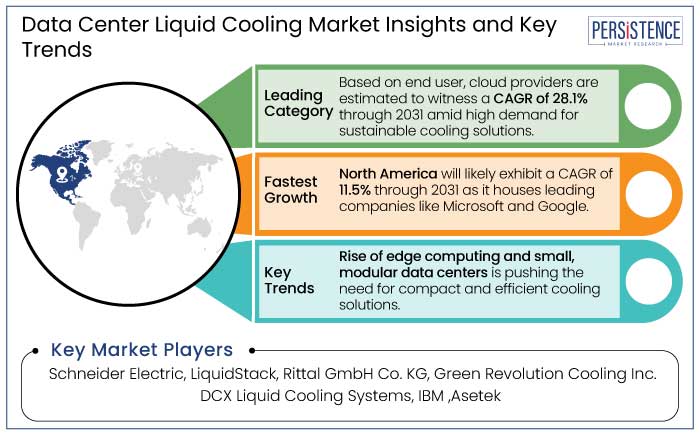

North America has consistently maintained a substantial data center liquid cooling market share, accounting for 30.9% in 2024. The U.S., with its thriving cloud computing sector, houses leading players such as Amazon Web Services, Google, and Microsoft. These generate immense data processing and storage needs, which require highly efficient cooling systems.

As these data centers scale up, traditional air-cooling methods struggle to maintain performance, making liquid cooling a more viable solution. Moreover, increasing reliance on AI, big data, and edge computing intensifies the need for unique cooling technologies. These can support the high heat loads of modern computing equipment.

North America is home to several hyperscale data centers that require cooling systems capable of operating continuously without downtime. These facilities, often owned by large tech companies, place a premium on reliability and efficiency, pushing demand for liquid cooling solutions.

Several U.S. states have implemented tax benefits and regulatory support to attract data center investments. These incentives encourage the construction of new facilities and the renovation of existing ones, especially as companies look to meet the high demand for data storage.

Cold plate liquid cooling continues to be the leading segment in the data center liquid cooling market, accounting for a significant 44.4% share in 2024. Cold plate cooling can directly cool the most heat-intensive components of a data center, such as CPUs and GPUs. Given the rising demands of High-Performance Computing (HPC), Artificial Intelligence (AI), and machine learning workloads, this precise thermal management has become essential.

Rising complexity and power consumption of servers have highlighted the limitations of air cooling. The data center industry is surging, driven by increased digitalization and cloud services. Hence, cold plate cooling technology is becoming increasingly viable.

As data centers rise, these systems can be adapted to new configurations without overhauls. This flexibility makes cold plate cooling a long-term solution that aligns with the growth and evolution of data centers, particularly as they accommodate new technologies like 5G and edge computing.

The large data centers (more than 10,000 sq. feet) segment has established a substantial lead, commanding an impressive 59.3% market share in terms of value in 2024. These facilities handle massive volumes of data processing. Hence, they require efficient cooling methods to ensure the reliability and longevity of critical infrastructure.

Data center operators strive to manage increasing data traffic, particularly from cloud computing, big data analytics, and AI workloads. Cooling solutions must keep up with the high thermal loads generated by high-density equipment.

Increasing density of servers and processors in these large facilities necessitates novel cooling systems to prevent overheating and ensure business continuity. For example,

The trend toward ‘green’ or sustainable data centers also plays a critical role in the adoption of liquid cooling technologies. As large data centers aim to reduce carbon footprint and improve energy efficiency, liquid cooling offers a significant advantage over traditional methods.

Cloud providers in the data center liquid cooling market are projected to rise at a CAGR of 28.1% through 2031. As cloud services become central to global computing infrastructure, need for efficient, scalable, and environmentally sustainable cooling solutions has surged. It is positioning liquid cooling technologies, such as immersion and direct-to-chip cooling, as the preferred choice.

Cloud providers, especially hyperscale data centers, are embracing liquid cooling to address the increasing power densities and operational demands of modern computing. These data centers host large-scale services, such as AI, machine learning, and blockchain. These generate significant heat due to high-performance processors and dense server configurations.

As the market rises, cloud providers face growing infrastructure demands, further driving the need for efficient cooling technologies. These help ensure the longevity and optimal performance of their data centers. This is particularly evident in regions with high ambient temperatures, where liquid cooling offers substantial benefits over air cooling.

Data center liquid cooling refers to unique cooling technologies used to manage the heat produced by high-density IT equipment, such as servers in data centers. Unlike traditional air-cooling methods that use air-conditioning systems, liquid cooling directly transfers heat away from the components using fluids, offering greater efficiency and precision. Liquid cooling also contributes to sustainability goals by utilizing less water compared to air-cooled systems and reducing the carbon footprint of data centers.

As the need for edge computing grows, liquid cooling is being increasingly adopted in edge data centers. These small-scale data centers often face space and energy constraints, making air cooling less efficient.

Liquid cooling systems are ideal in this context, as they take up less space, are more energy-efficient, and provide better cooling for high-performance servers in remote locations. Modular liquid cooling systems are gaining popularity because of their flexibility and scalability.

The systems can be easily extended as the data center grows. The modular approach also allows data centers to quickly deploy new cooling solutions when adding high-density workloads or specific cooling needs, without overhauls of existing infrastructure.

Cloud service providers, with their vast and booming infrastructure, are further adopting liquid cooling solutions. Need for energy efficiency and high-performance computing in cloud environments has led to the implementation of novel cooling systems.

As liquid cooling solutions mature, there is a rising emphasis on standardizing technologies and ideal practices across the industry. Industry groups, such as the Open Compute Project (OCP), are working to establish standards for liquid cooling systems. They are set to ensure that these solutions are compatible with a wide range of hardware and operational requirements.

The rise of edge computing and the shift toward hyper-efficient infrastructure have spurred investments in innovative cooling technologies. Liquid cooling, especially direct-to-chip (D2C) cooling, has become a preferred solution for cooling high-performance servers and specialized IT hardware. This is due to its superior heat transfer capabilities compared to air cooling.

Innovations in closed-loop cooling systems and immersion cooling have helped reduce operational costs, which has attracted more enterprises to adopt liquid cooling. The market recorded historical growth at a CAGR of 18.2%, indicating steady expansion from 2019 to 2023.

The data center liquid cooling market is projected to surge at a CAGR of 24.6% in the forecast period. The need for data centers to handle increasing data volumes, especially with the integration of AI, 5G, and machine learning, will likely drive demand for efficient solutions.

As these technologies evolve, data centers are set to become more compact, powerful, and energy intensive. These are set to necessitate novel cooling systems that can manage high heat loads and reduce energy consumption. New developments in refrigerant fluids, cooling materials, and high-performance heat exchangers will likely improve the efficiency and scalability of liquid cooling solutions.

Rising Demand for High-performance Computing to Propel Growth

High-Performance Computing (HPC) applications in fields like artificial intelligence, climate modeling, and scientific simulations have become more data intensive. Hence, traditional air-cooling systems struggle to effectively dissipate the increasing heat.

The challenge is driving data center operators to adopt liquid cooling technologies. These are particularly advantageous for HPC workloads as they remove heat more efficiently than air, enabling high computing densities. For instance,

Real-world implementations like NREL's show the scalability of liquid cooling systems in addressing the rising thermal demands of HPC systems.

Urgent Need for Energy Efficiency and Sustainability to Augment Demand

Data centers, which power the digital infrastructure of the world, consume a vast amount of energy. In fact, cooling systems alone account for up to 40% to 50% of the energy consumed by traditional data centers.

As energy costs rise and demand for sustainable operations intensifies, operators are turning to liquid cooling solutions to mitigate these issues. Liquid coolants, with their high thermal conductivity, are far more efficient at transferring heat away from IT equipment, enabling superior power densities in small spaces. This results in significant energy savings by reducing the need for excessive air circulation. It is both energy-intensive and less effective in cooling high-density servers?.

Liquid cooling also directly contributes to sustainability efforts by improving the efficiency of data center operations. Various systems incorporate heat recovery capabilities. The excess heat generated by servers is often repurposed for heating or even used in nearby residential or commercial buildings. This reduces reliance on traditional heating methods, further lowering energy consumption and associated carbon emissions.

Increasing Need for Specialized Equipment to Hamper Demand

Integration of liquid cooling systems into an existing data center setup requires careful planning due to the constant structural and operational changes. Unlike traditional air-cooling systems, liquid cooling demands specialized equipment such as liquid-to-liquid heat exchangers, pumps, and novel piping systems. These help in significantly altering the layout and operational dynamics of a facility. For example,

Potential Risk of Equipment Damage to Hinder Sales

Liquid cooling technologies, such as immersion and direct-to-chip cooling, offer significant benefits in terms of energy efficiency and performance. However, they can introduce new risks, particularly those associated with leaks or system failures.

A small leak in a liquid-cooling loop can have catastrophic consequences, leading to downtime, damaged equipment, and costly repairs. Without proper leak monitoring, even a minor fluid escape can go undetected, causing prolonged exposure of equipment to moisture. This accelerates corrosion or may lead to short circuits. For instance,

Integration with Renewable Energy to Create Fresh Growth Prospects

Data centers are increasingly becoming power-hungry and require efficient energy management. The combination of liquid cooling systems and renewable energy offers substantial opportunities for improving operational efficiency and sustainability.

As more data centers migrate toward sustainable energy solutions like solar and wind, liquid cooling technologies, such as direct-on-chip waterless, two-phase systems, are becoming essential. These cooling solutions can handle high thermal loads, enhancing data center capacity without excessive reliance on energy-intensive air conditioning systems.

Integrating renewable energy with liquid cooling further improves energy efficiency by repurposing waste heat. As data centers operate on green energy sources like solar and wind, excess heat generated by these facilities can be used for heating nearby buildings.

The holistic approach not only reduces the carbon footprint but also boosts the energy performance of data centers. The U.S. Department of Energy has highlighted such practices, where waste heat from servers is effectively reused, contributing to energy conservation.

Innovations in Coolant Technologies to Open the Door to Success

Demand for High-Performance Computing (HPC) is rising, driven by Artificial Intelligence (AI), machine learning, and expansion of 5G networks. Traditional air-cooling systems are struggling to keep pace with the increasing thermal output of IT equipment.

Liquid cooling solutions, by directly cooling heat-generating components, offer superior thermal management capabilities. These further help in addressing both performance and reliability issues in modern data centers.

The trend toward high rack densities exacerbates the problem. Techniques like direct-to-chip (DtC) cooling and immersion cooling allow operators to manage heat with high precision. These systems are not only more energy-efficient but also reduce the need for large air conditioning systems, significantly lowering operational costs.

Liquid cooling technologies can also lower the total cost of cooling by reducing both capital expenditures (CapEx) and operational expenses (OpEx). For example,

Data centers that adopt liquid cooling technologies further report significant reductions in their Power Usage Effectiveness (PUE) and carbon emissions. These factors make the systems a crucial component of sustainability efforts.

Companies are developing next-generation cooling technologies that offer high energy efficiency and low environmental impact. They are also forming alliances with data center operators and cloud service providers to integrate their liquid cooling technologies into existing infrastructure.

Such collaborations enable vendors to tap into new markets and drive broader adoption of liquid cooling solutions. Additionally, a few vendors are partnering with hardware manufacturers to optimize their cooling solutions for specific data center hardware. They are ensuring a tailored approach that enhances performance and energy efficiency.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Component

By Type of Cooling

By Data Center Size

By End User

By Region

To know more about delivery timeline for this report Contact Sales

The market is estimated to increase from US$ 4.1 Bn in 2024 to US$ 19.4 Bn by 2031.

Rising demand for energy-efficient and sustainable cooling solutions is anticipated to fuel the industry.

Schneider Electric, LiquidStack, Rittal GmbH Co. KG, and Green Revolution Cooling Inc. are a few leading players.

The market is projected to record a CAGR of 24.6% from 2024 to 2031.

A prominent opportunity is the adoption of immersion cooling for high-density computing applications, such as AI and machine learning, which generate significant heat.