- Hardware & Software IT Services

- Data Lake Market

Data Lake Market Size, Share, and Growth Forecast 2026 - 2033

Data Lake Market by Component (Solutions, Services), by Deployment (Cloud-Based, On-Premises, Hybrid, Multi-cloud), Industry (BFSI, IT & Telecom, Retail & E-Commerce, Healthcare, Manufacturing, Government, Media & Entertainment, Transportation & Logistics, Others), and Regional Analysis, 2026 - 2033

Data Lake Market Size and Trend Analysis

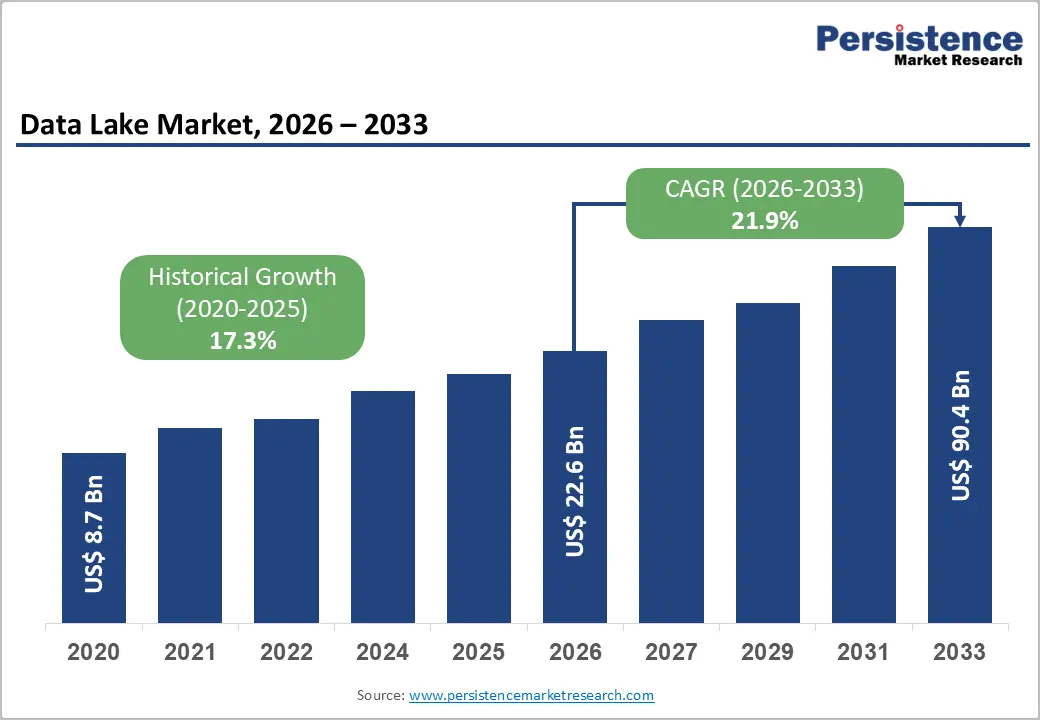

The global data lake market is expected to be valued at US$ 22.6 billion in 2026 and is projected to reach US$ 90.4 billion by 2033, growing at a CAGR of 21.9% between 2026 and 2033, due to the rapid scaling of enterprise AI and machine learning workloads, which require centralized, governed, and high-volume data repositories.

Organizations are increasingly shifting from traditional data warehouses to data lake architectures to handle structured and unstructured data on scale. Regulatory and governance frameworks, such as the U.S. NIST AI Risk Management framework which has pushed enterprises toward auditable and traceable datasets for AI deployment in regulated sectors. Rising data volumes from IoT, cloud migration, and real-time analytics are further intensifying the need for scalable data lake infrastructures.

Key Industry Highlights:

- Leading Offering: Solutions segment dominates with over 73% market share in 2026, valued at approximately US$ 16.50 billion, as enterprises prioritize unified platforms integrating storage, governance, analytics, security, and AI enablement.

- Leading Deployment: Cloud-based account for over 45% share in 2026, valued at more than US$ 10.17 billion, driven by elastic scalability, faster AI workload execution, and reduced infrastructure overhead.

- Fast-Growing Deployment: Multi-cloud architectures are the fastest-growing segment, supported by rising concerns around vendor lock-in, data sovereignty regulations, and demand for cross-provider interoperability enabled by open table formats.

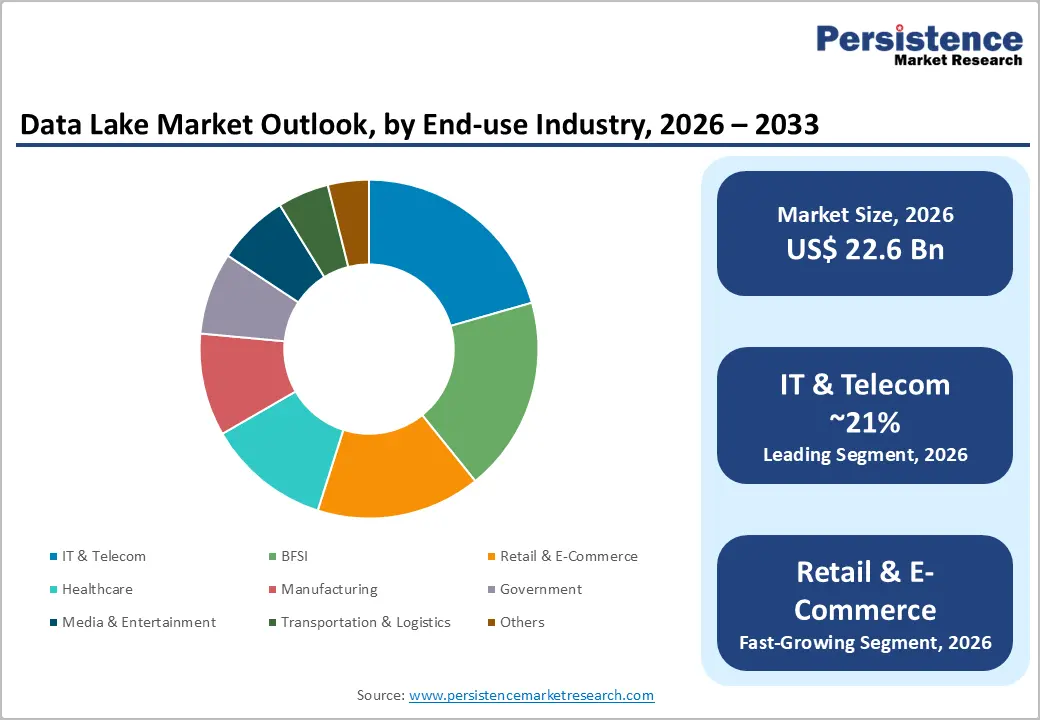

- Leading Industry: IT & Telecom holds over 21% market share in 2026, valued at more than US$ 4.75 billion, driven by high-volume network telemetry, 5G workloads, cybersecurity logs, and real-time analytics needs.

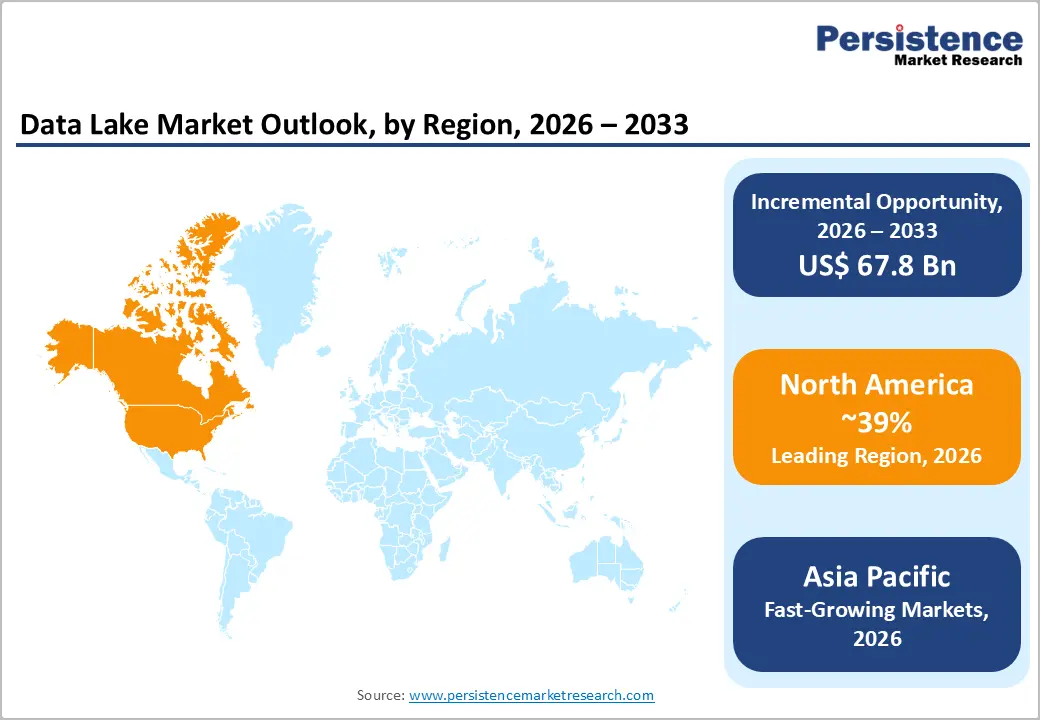

- Leading Region: North America dominates with over 39% market share in 2026, valued at approximately US$ 8.81 billion, supported by hyperscaler concentration, strong AI adoption, and enterprise modernization programs.

- Fast-Growing Market: Asia Pacific is the fast-growing market with a positive CAGR driven by 5G expansion, cloud migration, and large-scale digital economy initiatives across China, India, and Southeast Asia.

Market Dynamics

Drivers - Generative AI Model Training Pipelines Demanding Centralised Raw-Data Repositories

Enterprises building proprietary large language models and multimodal AI applications require petabyte-scale, schema-flexible storage that only data lake architectures cost-effectively provide, forcing immediate capital allocation toward lake modernisation.

The European Union's AI Act, formally adopted in May 2024, requires organisations deploying high-risk AI systems to maintain auditable data lineage, a compliance obligation that Databricks addressed directly through its Unity Catalog governance layer released in 2023, which integrates metadata management natively within the lakehouse. Every enterprise pursuing AI model development will treat the data lake not as optional infrastructure but as a regulatory and operational prerequisite, compressing the adoption decision cycle.

5G Network Rollout Generating Machine-Scale Telemetry That Overwhelms Conventional Databases

Telecom operators deploying 5G infrastructure are generating network telemetry, call detail records, and IoT sensor streams at volumes that relational databases cannot ingest without prohibitive cost, redirecting capital toward scalable lake architectures purpose-built for unstructured and semi-structured data. According to GSMA Intelligence, total number of 5G connections globally surpassed 2.7 billion, and Nokia deployed its Network as Code platform in 2024 to expose telemetry APIs directly to enterprise data lake pipelines.

As operator-driven data monetization strategies mature through 2027, telemetry lakes will evolve into commercial data products, expanding the total addressable market well beyond internal analytics use cases.

Market Restraints

Data Governance Fragmentation Inflating Total Cost of Ownership Across Multi-Jurisdictional Deployments

Inconsistent data residency laws across jurisdictions force organizations to replicate governance tooling, access controls, and audit trails in each sovereign cloud region, adding an estimated 20-40% premium to multi-region data lake operating costs compared to single-region deployments. The General Data Protection Regulation (GDPR) in the European Union, together with divergent national implementations of data localization in Brazil, LGPD, and India DPDP Act 2023, creates compliance overhead that disproportionately penalizes mid-market firms lacking dedicated data governance teams, slowing procurement decisions by an estimated six to twelve months.

Skills Scarcity in Data Engineering Compressing Deployment Velocity

The structural shortage of qualified data engineers professionals capable of building ingestion pipelines, maintaining Delta Lake or Apache Iceberg table formats, and tuning query performance limits how quickly organizations operationalize data lake investments after purchase. The U.S. Bureau of Labor Statistics projects that demand for data science and related occupations will grow 36% by 2033, the fastest of any occupation category tracked, yet supply from university programmes is expanding at less than a third of that pace, creating a widening talent gap.

New entrants without established partner networks face 12-to-18-month implementation timelines that erode projected ROI and increase competitive disadvantage against incumbents with embedded professional services relationships.

Opportunities - Healthcare Interoperability Mandates Opening a Greenfield Lake Deployment Wave

Healthcare interoperability mandates under the 21st Century Cures Act, and the ONC Cures Act Final Rule are creating a strong growth opportunity for the data lake market in healthcare. These regulations are driving health systems, payers, and life sciences firms to consolidate fragmented clinical, claims, genomic, and real-world evidence data into unified, cloud-based data lake architectures. This shift is increasing demand for FHIR-enabled ingestion layers and scalable storage systems capable of handling large, diverse healthcare datasets for analytics and AI use cases.

Platforms such as Microsoft Azure Health Data Services are enabling this transition by providing interoperable data integration frameworks that connect directly with enterprise data lakes. Interoperability mandates are creating significant opportunities for healthcare data lakes, accelerating cloud adoption, and enterprise-wide data modernization.

Industrial IoT in Smart Manufacturing: Creating Edge-to-Lake Data Pipelines at Scale

Industrial IoT in smart manufacturing is enabling large-scale edge-to-cloud data architectures where continuous sensor streams from production lines are ingested via industrial protocols such as OPC UA and processed through edge gateways before being consolidated into cloud data lakes or lakehouse platforms for predictive maintenance, quality optimization, and throughput analytics. Vendors such as Siemens, along with hyperscalers such as AWS and Microsoft Azure, are enabling integrated but heterogeneous edge-to-cloud stacks rather than fully standardized pipelines.

Interoperability is driven through a fragmented ecosystem led by OPC Foundation standards for machine connectivity and Linux Foundation initiatives such as LF Edge, rather than a single governing body. Enterprise deployments increasingly rely on hybrid architectures combining edge computing, streaming middleware, and centralized analytics layers. This creates a scalable but integration-intensive market opportunity for system integrators and industrial software platform providers.

Category-wise Analysis

Component Insights

The Solutions segment accounts for more than 73% of the global data lake market in 2026, equivalent to US$ 16.50 billion, reflecting enterprise preference for unified platforms that combine storage, governance, analytics, security, and AI enablement within a single environment. Organizations increasingly require scalable architectures capable of ingesting structured, semi-structured, and unstructured data in real time without creating fragmented data silos. Enterprises also prioritize solutions with embedded compliance, encryption, and access-control capabilities to address tightening data governance mandates.

Services are growing at a significant rate due to the increasing complexity of enterprise data modernization initiatives and the shortage of in-house cloud data engineering expertise. Organizations require consulting, migration, integration, and managed services to transition legacy warehouses and fragmented databases into scalable lakehouse environments. The demand is particularly strong for implementation services that enable interoperability across multi-cloud ecosystems and hybrid IT infrastructures. As AI adoption expands, businesses increasingly depend on external specialists for data pipeline orchestration, model-ready data preparation, and compliance-driven architecture customization.

Deployment Insights

Cloud-based segment accounts for over 45% share in 2026, reaching more than US$10.17 billion, due to the operational flexibility and elastic scalability that cloud-native architectures uniquely provide at enterprise workload volumes. Organizations increasingly prefer cloud deployments because they eliminate large upfront infrastructure investments while enabling rapid expansion of storage and compute capacity according to data growth.

Cloud environments also support faster AI experimentation, real-time analytics, and cross-regional collaboration through centralized access to massive datasets. Enterprises are prioritizing cloud-based data lakes to improve disaster recovery, automate software updates, and reduce infrastructure maintenance complexity.

Multi-cloud deployments are accelerating due to rising enterprise concerns regarding vendor lock-in, regulatory sovereignty requirements, and business continuity risks. Large organizations increasingly distribute data workloads across multiple cloud providers to optimize performance, pricing flexibility, and geographic compliance obligations. Multi-cloud architectures also allow enterprises to leverage specialized capabilities from different hyperscalers, such as AI processing, advanced analytics, or high-performance storage.

Open data formats and interoperable lake house technologies are enabling easier cross-cloud data mobility, making multi-cloud strategies more commercially viable and operationally efficient.

Industry Insights

IT & Telecom segment accounts for over 21% of the global data lake market in 2026, reaching over US$ 4.75 billion, driven by the massive growth of network traffic, connected devices, and real-time operational data generation. Telecom operators increasingly require scalable data lake architectures to process subscriber analytics, network performance metrics, cybersecurity logs, and 5G traffic data at extremely high velocity. The sector’s growing investment in edge computing and IoT ecosystems is further intensifying demand for centralized, low-latency data management platforms. Telecom companies prioritize data lakes for fraud detection, automated service assurance, and monetization of customer usage insights.

Retail & E-Commerce is the fast-growing end-use segment, propelled by the increasing dependence on real-time consumer intelligence, omnichannel operations, and AI-powered personalization strategies.

Retailers are deploying data lakes to consolidate customer transactions, browsing behavior, inventory data, logistics information, and social sentiment into unified analytical environments. The rapid expansion of digital commerce and same-day delivery models is generating unprecedented data volumes requiring scalable and cost-efficient storage architectures. Businesses are also leveraging data lakes for dynamic pricing, demand forecasting, recommendation engines, and supply chain optimization.

Regional Insights

North America Data Lake Market Trends and Insights

North America accounts for over 39.0% of the global data lake market in 2026, representing approximately US$ 8.81 billion, underpinned by the region’s dense concentration of hyperscale cloud providers, Fortune 500 enterprises, and early adoption of enterprise AI workloads that require scalable, governed data architectures. Strong venture capital investment in data infrastructure startups further reinforces ecosystem maturity, while the regulatory environment continues to encourage structured data governance and compliance-driven modernization.

The United States represents the core of this regional leadership, accounting for approximately 87.0% of the North America data lake market in 2026, equivalent to approximately US$ 7.67 billion, driven by financial services, technology firms, and regulated industries investing heavily in data platform modernization. Compliance frameworks such as requirements enforced by the U.S. Securities and Exchange Commission support robust data retention and auditability expectations, reinforcing the adoption of enterprise data lake architectures.

Federal AI governance initiatives under the Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence are accelerating demand among government contractors and regulated enterprises, further strengthening the U.S. position within the regional market.

Europe Data Lake Market Trends and Insights

Europe accounts for more than 27.0% of the global data lake market in 2026, valued at approximately US$ 6.10 billion, influenced by regulatory frameworks such as GDPR and the EU Data Act, which together increase compliance requirements around data access, portability, and cross-platform interoperability. Germany's data lake market represents over 22.0% of the Europe regional market in 2026, equating to approximately US$ 1.34 billion, driven by export-oriented manufacturing and Industry 4.0 adoption, where data lakes are integrated with platforms such as SAP S/4HANA for real-time production and supply chain analytics.

Sovereign data infrastructure initiatives such as Gaia-X, supported by multi-billion-euro public investment commitments, are shaping enterprise preferences toward compliant and federated cloud architectures.

The United Kingdom data lake market is valued at approximately US$ 1.22 billion in 2026, led by financial services adoption in London. Regulatory pressure from the Financial Conduct Authority (FCA), particularly its push toward machine-readable and API-based regulatory reporting, is a key demand driver for governed data lake architecture. Post-Brexit data adequacy arrangements with the EU further reinforce the need for strong data governance, lineage tracking, and residency-aware architectures.

France data lake market value is expected to cross over US$ 850 million, supported by state-backed digital transformation initiatives under France 2030 and sovereign cloud mandates requiring migration of public-sector analytics workloads to compliant domestic infrastructure, creating sustained enterprise and government demand for secure data lake platforms.

Asia Pacific Data Lake Market Trends and Insights

Asia Pacific accounts for approximately 25% of the global data lake market in 2026, representing US$ 5.65 billion, and is the fastest-growing region at a CAGR of 26.4%, due to large-scale 5G network densification, accelerated cloud migration across enterprises, and strong digital economy initiatives. Hyperscaler expansion and regional cloud availability zones are reducing latency and improving cost efficiency, enabling broader mid-market adoption of data lake platforms.

China data lake market is expected to cross the US$ 2.15 billion value by 2026, supported by long-term digital infrastructure planning under national strategies that prioritize big data systems, cloud computing, and industrial digitalization across banking, telecom, and energy sectors. Domestic platforms such as Alibaba Cloud and Huawei Cloud are increasingly preferred due to data sovereignty requirements and evolving compliance frameworks.

Japan is valued at approximately US$ 1.02 billion, driven by government-led digital transformation initiatives and enterprise modernization programs. The Digital Agency of Japan is advancing cross-ministerial data integration, while manufacturers are deploying cloud-based data lake architectures to support smart factory and Industry 4.0 use cases.

The India data lake market is expected to grow at a high rate, supported by the India Stack ecosystem, including UPI and Account Aggregator frameworks, which are generating large-scale structured and unstructured data flows requiring scalable lake architectures.

Competitive Landscape

The global data lake market is partially concentrated, platform-led competitive ecosystem rather than an oligopoly. Competition is shifting from storage cost advantages to ecosystem depth, metadata governance, and unified analytics capabilities. A key battleground is the integration of native AI/ML services, open table formats, and real-time processing layers. The emergence of the lakehouse architecture is blurring the traditional boundary between data lakes and warehouses. Vendors increasingly differentiate on query performance, scalability, and seamless access to raw and semi-structured data without heavy ETL dependence.

Key Developments:

- In May 2026, SAP agreed to acquire Dremio to strengthen its SAP Business Data Cloud and unify SAP and non-SAP data on a single open platform for enterprise AI. The acquisition will integrate Dremio’s lakehouse technology to improve scalability, performance, and data access, helping organizations run AI and analytics workloads more efficiently.

- In April 2025: Huawei showcased its AI Data Lake Solution at the IDI Forum 2025, designed to unify enterprise data storage, management, and AI processing on a single platform. The solution aims to help organizations efficiently handle massive volumes of multi-format data for AI model training and analytics. It focuses on improving data accessibility, performance, and scalability, enabling enterprises to build and deploy AI applications more effectively using a centralized data lake architecture.

Companies Covered in Data Lake Market

- Amazon.com, Inc.

- Microsoft Corporation

- Alphabet Inc. (Google Cloud LLC)

- Databricks, Inc.

- Snowflake Inc.

- IBM

- Oracle Corporation

- Cloudera, Inc.

- SAP SE

- Teradata Corporation

- Informatica Inc.

- Dremio Corporation

- Starburst Data, Inc.

- Dell Technologies Inc.

- Others

Frequently Asked Questions

The global data lake market is valued at US$ 22.6 Billion in 2026 and is projected to reach US$ 90.4 Billion by 2033, expanding at a CAGR of 21.9% due to enterprise demand for AI-ready, scalable, and compliant data infrastructure.

The growth is driven by rising adoption of generative AI, which requires centralized, high-volume training data systems. Regulatory mandates like the EU AI Act and expanding 5G-driven data generation are increasing demand for governed data lakes.

Solutions segment dominates with over 73% share in 2026, due to demand for integrated ingestion, storage, governance, and analytics platforms. Enterprises prefer unified platforms over standalone tools because of higher efficiency and strong vendor lock-in.

North America dominates the global data lake market with a 39.0% share in 2026, equivalent to US$ 8.81 Billion, supported by strong AI adoption and advanced enterprise data ecosystems. Regulatory compliance requirements and hyperscale dominance further reinforce its leadership position.

The key opportunity lies in healthcare data interoperability, especially FHIR-compliant data lake solutions. Vendors offering secure, compliant, and pre-built clinical data models capture early enterprise adoption before hyperscale commoditization.

Leading players include Amazon.com, Inc., Microsoft Corporation , Alphabet Inc. (Google Cloud LLC), Databricks, Inc., Snowflake Inc., IBM, Oracle Corporation, Cloudera, Inc., SAP SE and Others.