- Marine

- Vessel Mooring System Market

Vessel Mooring System Market Size, Share and Growth Forecast, 2026 - 2033

Vessel Mooring System Market by Types of Systems (Taut leg, Spread mooring, Semi taut, Dynamic positioning, Catenary, Single point mooring), Anchorage (Drag embedment anchors, Suction anchors, Vertical load anchors), Application (Tension leg platforms, FPSO, Semi-submersible platforms, FDPSO, SPAR platforms, FLNG, Others), and Regional Analysis for 2026 - 2033

Vessel Mooring System Market Share and Trends Analysis

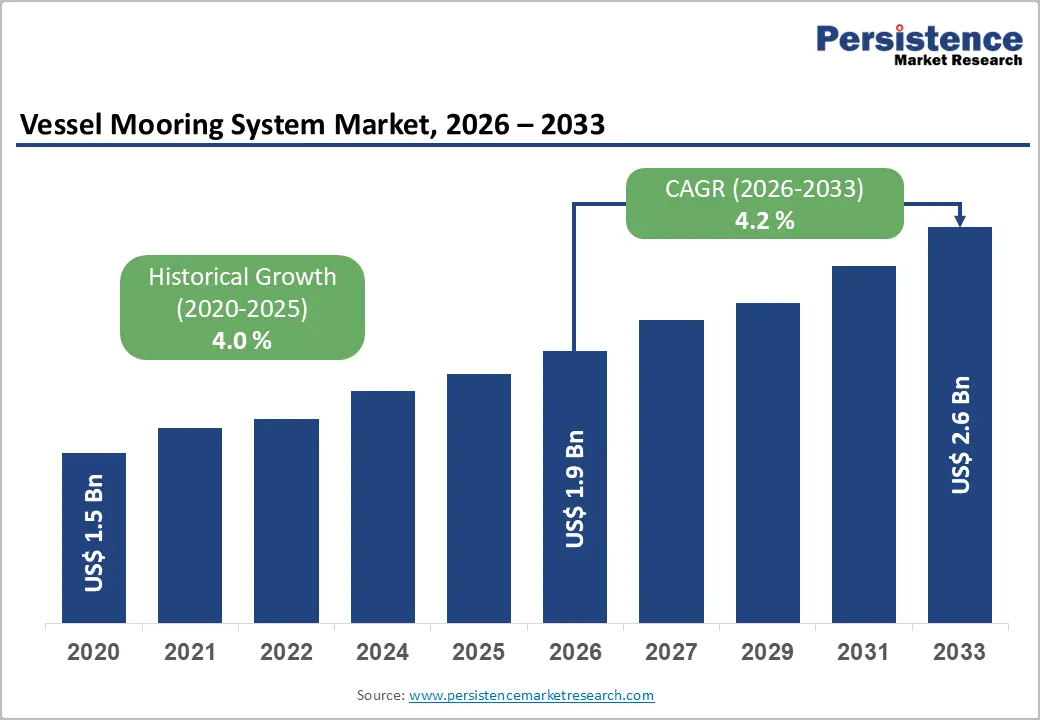

The global vessel mooring system market size is likely to be valued at US$ 1.9 billion in 2026 and is projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026-2033.

The vessel mooring system market is expanding due to rising offshore oil and gas exploration, rapid deployment of floating production units such as FPSOs (Floating Production Storage and Offloading), FLNGs (Floating Liquefied Natural Gas), SPARs (Single Point Anchor Reservoir), and floating offshore wind farms, all requiring advanced mooring and station-keeping solutions.

Technological innovation, digital monitoring, and regulatory pressure further drive demand, though the market remains capital-intensive and cyclical, closely tied to project sanction cycles and renewable-energy investment timelines.

Key Industry Highlights:

- Leading Application Segments: FPSO mooring systems command around 36% of the market in 2026, while FLNG platforms are the fastest-growing, underpinned by deepwater gas and floating-energy developments.

- Leading Mooring-Type Segment: Spread mooring systems hold around 43% of the market share in 2026.

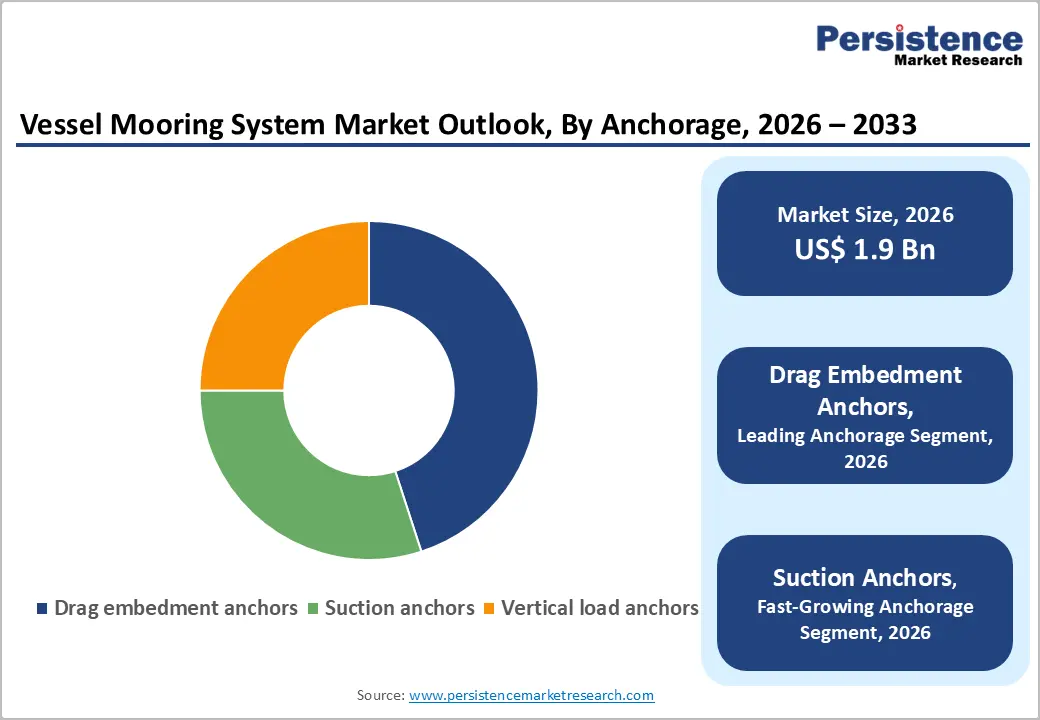

- Dominant Anchorage Types: Drag-embedment anchors lead with 45% share 2026, while suction anchors are the fastest-growing, especially in deepwater and ultra-deepwater projects.

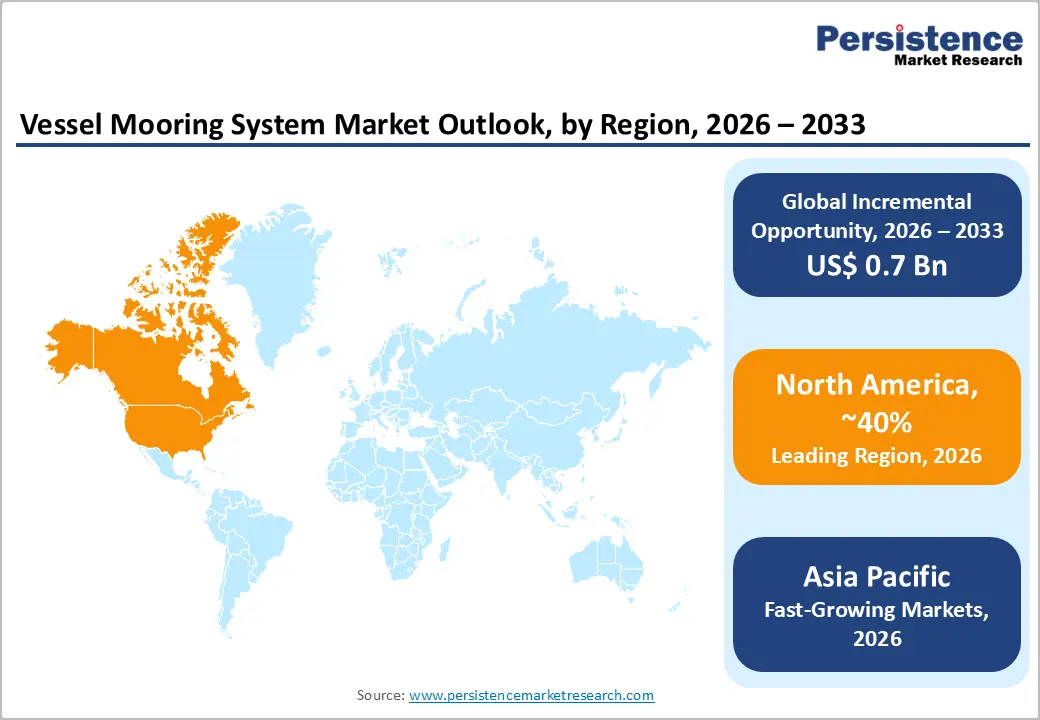

- Regional Leadership: North America leads with over 40% share in 2026, while Asia Pacific is the fastest-growing region, driven by new offshore oil and gas projects and rising floating-energy investments.

- Emerging High-Growth Opportunities: Floating offshore wind and offshore aquaculture represent key opportunities, with thousands of new mooring lines and anchors projected over the next decade.

DRO Analysis

Offshore Energy Expansion in Deepwater and Floating Renewables

The deepwater and ultra-deepwater oil and gas sector remains the largest end-user of vessel mooring systems, accounting for over 50% of demand in the offshore mooring market. Rising project sanctions in the Gulf of Mexico, West Africa, and Southeast Asia are driving large-scale FPSO and FPU developments, each requiring multiple mooring lines supported by drag-embedment or suction anchors in water depths exceeding 1,500 meters. With global upstream oil and gas investments stabilizing at a multi-hundred-billion-dollar annual scale, this pipeline provides a durable base for vessel mooring system manufacturers and service providers.

Floating offshore wind is emerging as the fastest-growing segment, with tens of thousands of turbines planned globally over the next decade, each relying on array-based mooring systems with catenary or semi-taut configurations and drag-embedment or suction anchors. Projects such as Hywind Scotland and Hywind Tampen, along with large leasing rounds like ScotWind, are driving multi-gigawatt portfolios of floating wind farms, each requiring thousands of mooring lines and anchors over extended lifetimes.

Supportive policies, such as the EU’s Green Deal and national offshore wind mandates, are accelerating investment in floating mooring R&D, synthetic-rope-based systems, and standardized layouts. These expansions of deepwater oil and gas and floating renewables create a unified, long-term driver for the vessel mooring system market, sustaining multi-year demand across traditional offshore energy and next-generation floating platforms

Capital-Intensive Nature and Cyclical Project Environment

The vessel mooring system market is highly capital-intensive, with mooring systems for large FPSOs or FLNGs typically representing 5–10% of total project CAPEX. Deepwater developments require specialized anchors, long-length synthetic or chain-wire combinations, and engineered installation campaigns, all of which drive up upfront costs and extend lead times. This exposure to high upfront engineering and equipment spend makes mooring systems particularly sensitive to oil-price volatility and macroeconomic uncertainty.

Over the 2020–2025 period, fluctuations in crude-oil prices and bouts of global economic stress have repeatedly led operators to delay or re-scope offshore projects, compressing demand for new mooring systems and testing margins and utilization rates for mooring-system providers. The hesitancy to commit to new FIDs during periods of price weakness or financial tightening underscores the cyclical nature of the market and limits the ability of mooring-system suppliers to secure long-term, stable backlogs.

Technical Complexity and Harsh-Environment Constraints

Operating in deepwater and ultra-deepwater environments imposes extreme technical and environmental constraints, where currents, waves, and wind can exceed 100-year storm conditions over a platform’s lifetime. This demands high-integrity mooring designs capable of resisting fatigue failure, anchor drag, or riser clash, yet any design or installation shortfall can trigger off-station events, production downtime, and environmental incidents. Such failures invite regulatory scrutiny and liability risk, discouraging cost-cutting in critical mooring components.

In addition, deepwater and remote offshore sites face logistical bottlenecks, including a limited pool of specialized anchor-handling vessels, deepwater installation contractors, and certified suppliers. Can these constraints lead to supply-chain delays and schedule slippage, increasing project risk and pushing up costs? The combination of technical complexity, harsh-environment exposure, and constrained logistics raises the barrier to entry for smaller players and reinforces the dominance of established, integrated mooring-system providers in the market.

Opportunities - Expansion of Floating LNG, Floating Production Units, and New Energy-Linked Mooring Niches

The FLNG and floating production unit market offers a high-value opportunity for vessel mooring system vendors, with 4–6 new FLNG projects expected to reach FID by 2025–2026. Each FLNG unit typically requires 8–16 mooring lines and a permanent, weather-resistant mooring system, often deployed in deepwater or ultra-deepwater locations. As Cedar FLNG, Delfin FLNG, and similar projects move forward, the associated mooring-system spend is expected to scale with platform size and operational complexity, supporting long-term revenue for mooring system integrators, anchor manufacturers, and installation contractors. Policy-driven global gas-demand growth and liquefaction-capacity expansion, especially in Southeast Asia, West Africa, and the Americas, further strengthen this opportunity across floating-energy platforms.

Beyond oil and gas, floating offshore wind and offshore aquaculture expand mooring demand, with floating wind projects requiring standardized, cost-optimized mooring layouts and developers targeting 2025–2030 as commercialization windows. Norway’s planned multi-gigawatt floating wind pipelines will demand thousands of mooring lines and anchors, creating a multi-billion-dollar cumulative opportunity over the next decade. Offshore aquaculture is shifting into deeper and more exposed waters; these projects are already generating new mooring demand and encouraging providers to develop specialized offshore aquaculture solutions.

Category-wise Analysis

System Type

Within mooring-type segmentation, spread mooring systems are likely to be the leading segment, accounting for around 43% of the offshore mooring systems market by revenue. These systems typically use 6–10 lines arranged around a vessel or platform to deliver stable, omnidirectional station-keeping and are widely deployed on FPSOs, semi-submersibles, and mobile offshore drilling units. Their proven reliability, long design life (20–30 years), and adaptability from shallow to ultra-deepwater have entrenched them as the core go-to configuration across the vessel mooring system market.

Dynamic positioning (DP-enabled mooring layouts) is anticipated as the fastest-growing segment, driven by deepwater drilling and FPSO campaigns that require real-time, anchor-light positioning in cyclone-prone waters and ultra-deep basins. A North Sea drilling program led by Equinor-linked drillships has rolled out next-generation DP-C services, combining AI-based weather-adaptive station-keeping and remote-monitoring hubs to cut fuel burn and improve safety. These deployments illustrate how DP-augmented mooring is becoming standard on premium FPSOs and ultra-deepwater drillships.

Anchorage Insights

Drag-embedment anchors (DEAs) are expected to be the leading anchorage type, contributing approximately 45% of revenue in the offshore mooring systems market. DEAs are dragged along the seabed until they embed at depths of about 1–2 meters, leveraging soil resistance to deliver holding capacities often 30–50 times their own weight, making them cost-effective and widely deployable across a range of seabed conditions. They are commonly used on mobile offshore drilling units, semi-submersibles, and shallow-to-mid-depth FPSOs, where ease of installation and re-deployment are critical.

Suction anchors are projected to be the fastest-growing anchorage segment, expanding at a higher rate than vertical load or traditional drag anchors, particularly in deepwater and ultra-deepwater projects. Large-diameter suction piles, with diameters up to 10 meters and heights of 35 meters, provide high-capacity, low-drag solutions with a minimal seabed footprint. In 2026, a deepwater Gulf of Mexico gas FPSO and a West Africa ultradeep project both adopted clustered suction-pile arrays as part of zero-seabed-drilling mooring schemes, aligned with stricter decommissioning and environmental rules.

Regional Analysis

North America Vessel Mooring System Market Trends

North America is expected to be the leading regional market for vessel mooring systems, accounting for over 40% of global offshore mooring systems revenue. The region’s strength comes from the United States Gulf of Mexico, which hosts high-value deepwater FPSO and FPU developments such as BP’s Kaskida, Tiber-Guadalupe, and Woodside’s Trion project, each requiring million-dollar mooring systems. The U.S. offshore regulatory framework, enforced by the Bureau of Safety and Environmental Enforcement (BSEE) and the U.S. Coast Guard, mandates safety-case-based design, risk-based inspections, and strict environmental controls, driving demand for advanced, high-integrity mooring solutions.

North America also hosts a dense innovation ecosystem, where major oil and gas operators, EPCs, and mooring-system integrators collaborate on next-generation technologies such as digital twins, real-time mooring monitoring, and synthetic-rope-based systems. This ecosystem is increasingly extending into floating offshore wind, with Gulf of Maine and Central Atlantic lease auctions creating a forward pipeline of mooring-system demand once commercial farms are deployed, reinforcing the region’s long-term structural advantage in the vessel mooring system market.

Europe Vessel Mooring System Market Trends

Europe is a mature, highly regulated offshore mooring systems market, with Germany, the U.K., France, and Spain jointly driving demand from deepwater gas and floating wind projects. The North Sea, particularly the UK and Norwegian sectors, remains a core hub for FPSO and FLNG operations, while Norway’s floating wind projects are pioneering floating-wind mooring standards tailored to harsh, high-latitude environments. European regulatory bodies such as the European Maritime Safety Agency (EMSA) and national offshore authorities enforce strict safety and environmental regimes, which incentivize operators to upgrade legacy mooring systems to modern, monitored layouts.

Europe also benefits from regulatory harmonization under the EU Offshore Safety Directive and associated environmental frameworks, which support cross-border collaboration on mooring standards, inspection protocols, and decommissioning practices. This harmonization enables scalable, reusable mooring-system designs that can be adapted across North Sea, Mediterranean, and Atlantic projects, improving operational reliability and reducing engineering costs. The region’s combination of mature deepwater activity, growing ambitions for floating wind, and policy-driven safety upgrades positions Europe as a stable, high-value segment of the vessel mooring system market.

Asia Pacific Vessel Mooring System Market Trends

Is Asia Pacific projected to be the fastest-growing regional market for vessel mooring systems, expanding at a higher growth rate in the forecast period? The region is driven by new offshore oil and gas discoveries in the South China Sea, India, and Southeast Asia, alongside China’s and ASEAN’s floating-energy ambitions, which are reshaping deepwater investment patterns. China’s national oil companies, including CNOOC, are investing USD 17–19 billion annually in offshore projects, many of which involve deepwater FPSO developments that require advanced, multi-line mooring systems.

In Southeast Asia, Petronas’s Kasawari gas field and related projects are driving new demand for mooring systems, supported by regional manufacturing hubs in Malaysia, Singapore, and South Korea. Asia Pacific’s manufacturing advantages, including cost-competitive fabrication, skilled engineering workforces, and integrated shipbuilding and offshore-supply chains, position the region as a strategic production center for anchors, chains, connectors, and mooring-system components.

This ecosystem supports both domestic FPSO and FLNG deployments and export-oriented mooring-system packages for global floating-energy projects, amplifying Asia Pacific’s role in the global vessel mooring system value chain and cementing its status as the primary growth engine of the regional landscape.

Competitive Landscape

The vessel mooring system market is moderately consolidated, with a small group of global integrators capturing over half of total revenue. Leading players such as TechnipFMC, Aker Solutions, NOV, Delmar, MacGregor, and SBM Offshore dominate high-value deepwater projects through proven designs, operator relationships, and technology leadership in synthetic mooring lines, advanced anchors, and digital monitoring. Their integrated offerings for FPSOs, FLNGs, SPARs, and drilling units give them strong bidding power and long-term visibility.

Regional and niche suppliers focus on shallow-water terminals, marginal-field FPSOs, and emerging areas like offshore aquaculture and floating wind. Barriers such as stringent environmental regulations and safety standards constrain new entrants, but digitalization enables software firms to enter via mooring-health monitoring and analytics platforms. Market consolidation is expected to grow as global leaders acquire specialist anchor and monitoring providers while deepening technology-driven partnerships.

Key Developments

- In April 2026, CoreMarine and Jumbo Offshore are installing soft-yoke (SSY) mooring systems for the Hilli Episeyo and MKII FLNG units in Argentina’s Golfo San Matías, marking the country’s first SSY-FLNG project

- In January 2026, Qingdao Port in China debuted Trelleborg’s AutoMoor system, a fully automated ship-mooring solution that replaces manual mooring by automatically deploying and securing mooring lines with remote control and sensors.

Companies Covered in Vessel Mooring System Market

- TechnipFMC

- Aker Solutions

- NOV

- Delmar Systems

- MacGregor

- Nabrawind

- SBM Offshore

- GustoMSC

- BW Offshore

- Exponent

- Sea麒国际 (Sea Queen International)

- Hyundai Heavy Industries

- Daewoo Shipbuilding & Marine Engineering

- Samsung Heavy Industries

- China Offshore Oil Engineering

Frequently Asked Questions

The global vessel mooring system market is projected to reach US$ 1.9 billion in 2026.

Rising deepwater and floating‑energy projects, including FPSOs, FLNGs, and floating offshore wind, drive demand for advanced vessel mooring systems.

The market is poised to grow at a CAGR of 4.2% from 2026 to 2033.

Expanding FLNG, SPAR, and floating‑offshore wind developments and offshore aquaculture expansion present major growth opportunities.

TechnipFMC, Aker Solutions, NOV (National Oilwell Varco), Delmar Systems, MacGregor, SBM Offshore, GustoMSC, BW Offshore, and Hyundai Heavy Industries are key players in the market.