Industry: Healthcare

Published Date: September-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 174

Report ID: PMRREP34797

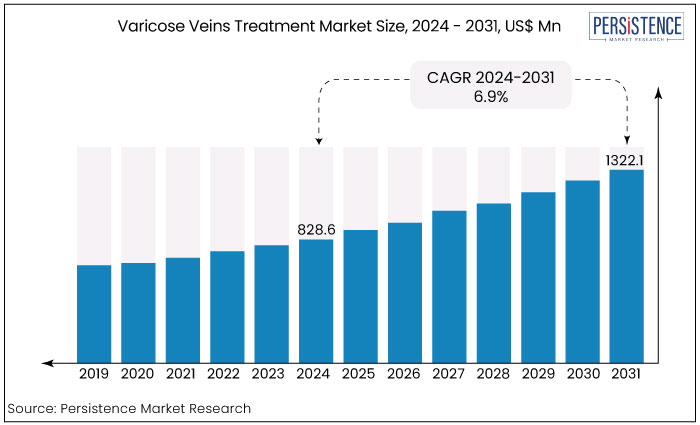

The varicose veins treatment market is estimated to increase from US$828.6 Mn in 2024 to US$1322.1 Mn by 2031. The market is projected to record a CAGR of 6.9% during the forecast period from 2024 to 2031. Increasing prevalence of lifestyle-related risk factors like obesity and sedentary lifestyles influences the market progress over the forecast period. North American is estimated to be the powerhouse for the market owing to its robust healthcare infrastructure.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Market Size (2024E) |

US$828.6 Mn |

|

Projected Market Value (2031F) |

US$1322.1 Mn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

6.9% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

6% |

|

Region |

Market Share in 2024 |

|

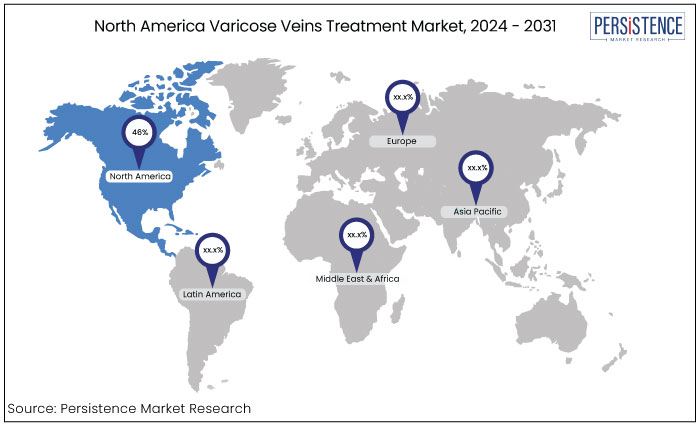

North America |

46% |

North America market is estimated to command with significant market share of 46% mostly results from a substantial patient demographic that is visually aware. Individuals are inclined to pursue cosmetic operations because of the apparent outcomes and safety.

The Society for Vascular Surgery, in collaboration with the American Venous Forum, has established clinical care recommendations for treating varicose veins in the United States. These guidelines include suggestions for treating chronic venous illnesses grounded in the grading system.

Assessing the severity of the ailment facilitates communication between care and insurance providers. A general physician can convey the severity when referring patients to vein specialists. Patients can be categorized into distinct groups according to their severity.

The validation of the safety and efficacy of laser treatments has diminished the stigma associated with cosmetic procedures and fostered social acceptance of laser treatments, particularly among men.

|

Category |

Market Share in 2024 |

|

Treatment - Sclerotherapy |

73% |

The varicose veins treatment market is divided into endovenous ablation, sclerotherapy, and surgical ligation. Among these, the sclerotherapy treatment dominates the market based on treatment.

The advantages of this treatment are less bruising and scarring, absence of sedation, shortened hospital stays, and uncomplicated follow-up treatments account for its predominant market share.

Medicare offers coverage for patients receiving sclerotherapy treatment in the United States. Numerous organizations including the British Association of Sclerotherapies (BAS) conduct annual activities to promote awareness and facilitate the acceptance of diverse treatments.

The rising quantity of product approvals is further facilitating market expansion. Vascular Barcelona Devices (VB Devices) obtained CE mark clearance for the Varixio Pod Air, classified as a Class 1 medical equipment designed for automated foam creation for sclerotherapy of varicose veins.

|

Category |

Market Share in 2024 |

|

End User - Hospitals |

60% |

The varicose veins treatment market is divided into vein clinics, hospitals, and ambulatory care unit based on End User. Among these, hospitals to dominate the market accounting for 60% market share in 2024.

Hospitals are equipped with advanced medical infrastructure including diagnostic tools (e.g., Doppler ultrasound, MRI, and CT scans) and treatment equipment for both surgical and non-surgical procedures. These procedures include endovenous laser treatment (EVLT), radiofrequency ablation (RFA), and sclerotherapy.

The availability of sophisticated medical facilities ensures that patients receive precise diagnosis and tailored treatment for different severities of varicose veins making hospitals a one-stop solution for comprehensive care.

The combination of advanced technology, availability of specialists, multi-disciplinary care, ability to handle complex cases, and access to emergency and post-treatment care makes hospitals dominant End User segment in the market. Further, the vein clinics and ambulatory care centers are growing especially for less severe cases. Hospitals remain the preferred choice for comprehensive and high-risk treatments.

The transition to minimally invasive treatment methods, the accessibility of modern varicose vein treatment technologies, and the significant prevalence of varicose vein cases in North America and Europe are propelling market expansion. Additional growth factors encompass enhanced patient compliance and reliability, increasing healthcare expenditures, and the swift expansion of the aging population.

The scarcity of training for vascular surgeons, the elevated expenses associated with varicose vein treatment treatments, and the enactment of healthcare reforms in the U.S. are significant factors inhibiting market growth further.

Constraints related to uneven reimbursement for varicose vein treatment treatments and the sustainability of participants in the intensely competitive industry restrain market growth. The increasing prevalence of varicose veins globally is attributed to causes such as an aging population, sedentary lifestyles, obesity, and genetic predisposition. Consequently, intensifying the demand for better treatment alternatives. A variety of therapeutic techniques are available including minimally invasive procedures such as endogenous laser ablation, sclerotherapy, and radiofrequency ablation.

Before 2023, the varicose veins treatment market witnessed steady growth driven by the rising prevalence of venous diseases due to sedentary lifestyles, obesity, and aging populations. The increased adoption of minimally invasive procedures, such as endovenous laser treatment (EVLT), radiofrequency ablation (RFA), and sclerotherapy, further fueled market expansion.

The growing awareness of varicose vein-related complications and the availability of outpatient treatments also contributed to market growth. Technological advancements in laser treatments, foam sclerotherapy, and increasing healthcare, spending, particularly in developed helped the market to flourish.

The market is projected to expand at an accelerated pace post-2024, driven by advancements in treatment technologies such as improved non-invasive options and high precision tools. Also, increasing demand for cosmetic procedures and a huge focus on early treatment will propel the market further.

Emerging economies especially in Asia Pacific are likely to present new growth opportunities due to rising healthcare awareness and improving access to treatment. With the expansion of specialized vein clinics, the shift toward outpatient settings is expected to drive demand. Expanding insurance coverage for varicose vein treatments in several regions will boost market growth.

Rising Prevalence of Lifestyle-Related Risk Factors

The increasing prevalence of lifestyle-related risk factors such as sedentary behaviour, obesity, and prolonged standing or sitting is a significant driver for the varicose veins treatment market. Modern work environments where individuals spend extended hours sitting at desks or standing for long periods contribute to poor blood circulation leading to venous insufficiency. Additionally, rising obesity rates exert extra pressure on veins exacerbating the risk of varicose veins.

With an aging global population, these risk factors are compounded by the natural weakening of venous walls making the condition more common. As awareness of varicose veins increases, more patients are seeking treatments earlier in the progression of the disease. This growing patient pool combined with the emphasis on lifestyle management and preventive care continues to drive demand for both minimally invasive and surgical interventions in the market.

Advancements in Minimally Invasive Treatments

Technological advancements in minimally invasive procedures have revolutionized the varicose veins treatment market. Treatments like endovenous laser therapy (EVLT), radiofrequency ablation (RFA), and foam sclerotherapy are becoming more popular. The popularity is due to their effectiveness, short recovery times, and reduced risks compared to traditional surgeries like vein stripping. These non-surgical options are performed in outpatient settings, which make them convenient for patients and lower healthcare costs.

As these treatments become more refined, their success rates are improving further encouraging their adoption. Patients are increasingly drawn to these options due to their minimal scarring, quick recovery, and few complications. Physicians and healthcare providers also prefer these methods for their precision, ease of use, and ability to treat a larger number of patients efficiently.

The shift toward advanced minimally invasive procedures are a key growth driver attracting both patients and healthcare systems to adopt new technologies in the varicose veins treatment landscape.

High Treatment Costs and Limited Reimbursement

One of the primary restraints for the varicose veins treatment market is the high cost of treatments, particularly for minimally invasive procedures like endovenous laser therapy (EVLT) and radiofrequency ablation (RFA). These advanced treatments can be expensive and are not always covered by insurance.

In many cases, insurance providers classify varicose vein treatments as cosmetic limiting reimbursement options for patients unless the condition is deemed medically necessary due to complications like ulcers or severe pain. The cost barrier reduces accessibility especially for patients in lower-income brackets or in regions with inadequate insurance coverage.

The financial burden discourages some patients from seeking early intervention leading to untreated cases or reliance on cheap, less effective treatments. As a result, the high out-of-pocket costs for patients remain a significant factor limiting the market growth particularly in developing regions.

Lack of Awareness in Emerging Markets

Another significant growth restraint is the lack of awareness regarding varicose veins and their potential complications in emerging markets. In many developing countries, varicose veins are often perceived as a purely cosmetic issue rather than a medical condition requiring treatment. As a result, patients may delay seeking care leading to more advanced stages of venous disease that require complex and costly interventions.

There is often a shortage of specialized healthcare providers and clinics equipped to diagnose and treat varicose veins in these regions. This lack of medical infrastructure and knowledge about modern treatment options hampers market growth further. The gap in education and infrastructure significantly limits the adoption of varicose vein treatments in emerging markets posing a challenge to global market expansion.

Expansion of Non-Invasive and Outpatient Procedures

One of the most transformative opportunities in the varicose veins treatment market is the expansion of non-invasive and outpatient procedures. With advancements in technologies such as endovenous laser therapy (EVLT), radiofrequency ablation (RFA), and sclerotherapy, patients can now undergo treatments that require minimal recovery time and fewer complications. The above procedures can often be performed in outpatient settings like vein clinics or ambulatory care centers, making them more accessible and convenient. This

Shift away from traditional surgeries, which were often invasive and required hospitalization represents a key opportunity for both healthcare providers and patients. The growth of these outpatient procedures opens new markets in regions where access to hospital-based care is limited or where patients prefer fast and cost-effective treatments.

As technology continues to improve, the success rates and efficiency of non-invasive methods are expected to attract more patients driving market growth and expanding treatment options globally.

The competitive landscape of the varicose veins treatment market is characterized by a mix of established medical device companies and specialized vein treatment providers. Key players operating in the market are Medtronic, AngioDynamics, Biolitec AG, Merit Medical Systems, and Alma Lasers

Leading players dominate the market with advanced technologies like endovenous laser therapy (EVLT), radiofrequency ablation (RFA), and sclerotherapy systems. Also, specialized vein clinics, such as USA Vein Clinics and Vein Clinics of America are gaining significant market share by offering outpatient treatments with high patient satisfaction.

Market competition is driven by technological innovations, product launches, and expanding treatment offerings. Regional players are also growing particularly in emerging markets, as healthcare access improves and awareness of varicose vein treatments increases globally.

Recent Industry Developments in the Varicose Veins Treatment Market

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Million for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Treatment

By End User

By Region

To know more about delivery timeline for this report Contact Sales

Increasing incidences of lifestyle-related risk factors remains a key driver for market growth.

Hospitals to dominate the market accounting for 60% market share in 2024.

North America holds the largest market share.

A key opportunity lies in the expansion of non-invasive and outpatient procedures.

Medtronic, Teleflex Incorporated, Sciton, Inc., are some of the top key players in the market.