- Biotechnology

- Urothelial Carcinoma Diagnostics Market

Urothelial Carcinoma Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Urothelial Carcinoma Diagnostics Market by Diagnostic Test Type (Cystoscopy, Urine Cytology, Urinary Biomarker Tests, Imaging Modalities, Others), Technology (Microscopy-Based Diagnostics, Fluorescence In Situ Hybridization [FISH], PCR-Based Molecular Diagnostics, Next-Generation Sequencing, Others), End-user (Hospitals, Specialty Urology Clinics, Cancer Centers, Diagnostic Laboratories, Ambulatory Surgical Centers, Others), and Regional Analysis, 2026 - 2033

Urothelial Carcinoma Diagnostics Market Size and Trend Analysis

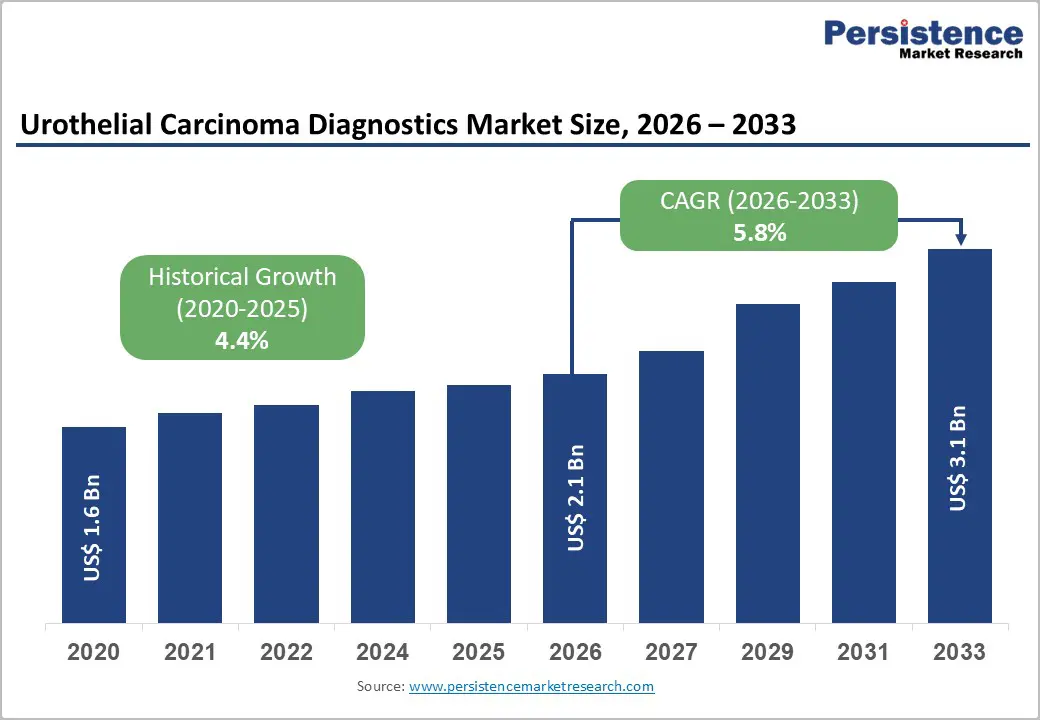

The global urothelial carcinoma diagnostics market size is expected to be valued at US$ 2.1 billion in 2026 and projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. This consistent and accelerating growth is driven by the rising global incidence of bladder cancer, urothelial carcinoma's most prevalent form, combined with growing clinical adoption of advanced molecular diagnostic technologies that enable earlier, more accurate, and less invasive disease detection and surveillance.

The World Health Organization's International Agency for Research on Cancer (IARC/GLOBOCAN) reported 614,000 new bladder cancer cases and 220,000 deaths globally in 2022, establishing it as the 10th most common cancer worldwide. Urothelial carcinoma's exceptionally high recurrence rate, 50-70% within five years of initial treatment per American Urological Association (AUA) guidelines creates a large and recurring surveillance testing market that structurally supports consistent diagnostic test volume.

Rapid innovation in urinary biomarker panels, next-generation sequencing (NGS)-based liquid biopsy diagnostics, and fluorescence-enhanced cystoscopy are further broadening the market's technology addressable landscape through the forecast period.

Key Highlights

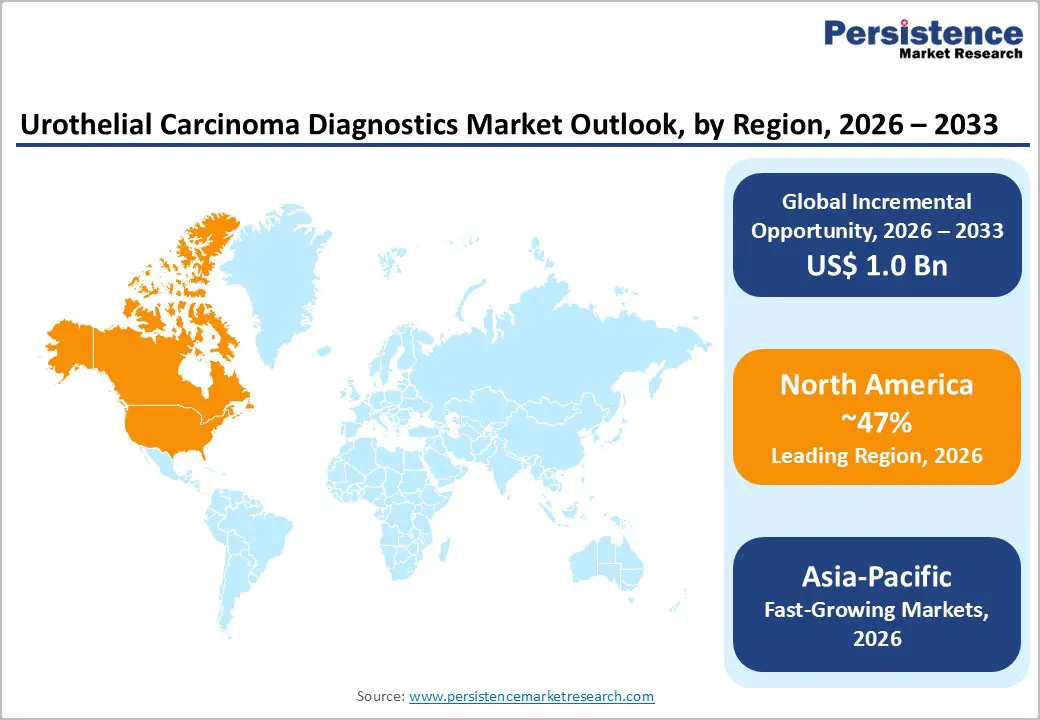

- Leading Region - North America: North America holds approximately 47% of global Urothelial Carcinoma Diagnostics market share in 2025, anchored by the U.S.'s 83,000 annual bladder cancer cases per American Cancer Society, Medicare reimbursement for UroVysion® and Cxbladder®, and the world's highest concentration of molecular diagnostic technology companies.

- Fastest Growing Region - Asia Pacific: Asia Pacific is the fastest-growing urothelial carcinoma diagnostics market, driven by China's 90,000+ annual bladder cancer cases per the National Cancer Center, Healthy China 2030 hospital infrastructure expansion, and growing molecular diagnostic adoption across Japan, India, and ASEAN oncology centers.

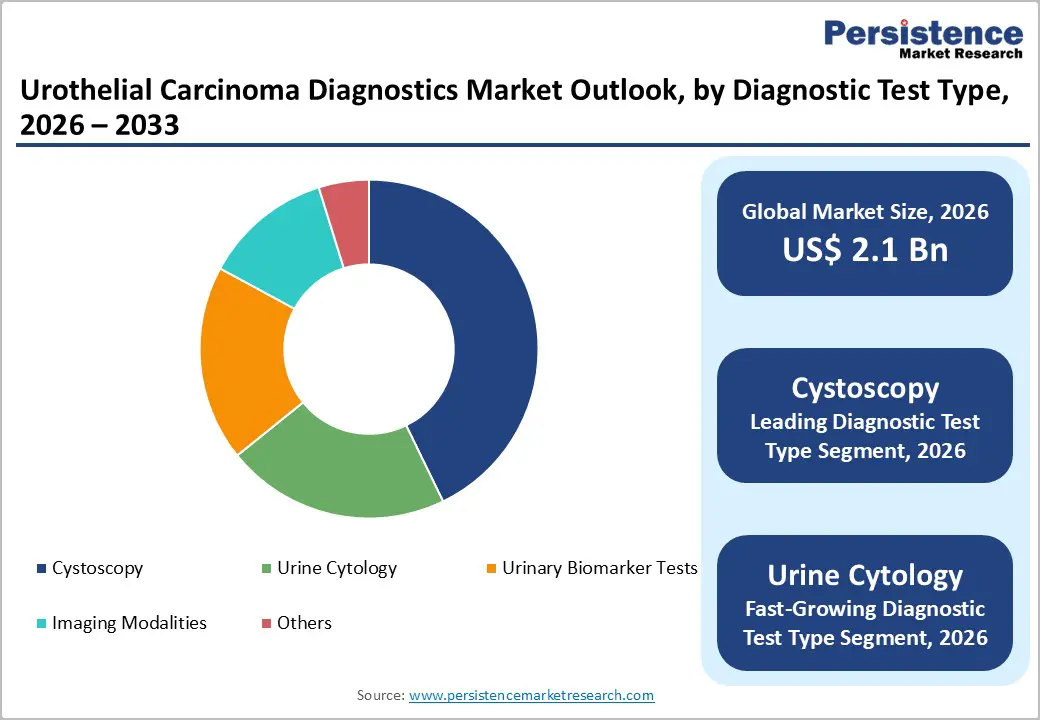

- Dominant Diagnostic Type - Cystoscopy: Cystoscopy leads the diagnostic test type category with approximately 43% share in 2026 endorsed by EAU and AUA as the definitive bladder cancer surveillance gold standard generating mandatory recurring test demand from the 50-70% NMIBC recurrence rate requiring biannual endoscopic surveillance.

- Fast-Growing Segment - Urinary Biomarker Tests: Urinary Biomarker Tests are the fastest-growing diagnostic test type, driven by FDA-cleared panels including Cxbladder® and UroVysion®, emerging urine ctDNA liquid biopsy platforms achieving >90% sensitivity for high-grade NMIBC, and growing clinician demand for non-invasive surveillance alternatives.

- Key Opportunity: Next-generation sequencing (NGS)-based urine ctDNA liquid biopsy represents the most transformative diagnostics opportunity with studies in European Urology and Nature Medicine demonstrating superior sensitivity and growing FDA Breakthrough Device Designation approvals accelerating commercial timelines for validated non-invasive surveillance platforms.

Market Dynamics

Drivers - Rising Global Bladder Cancer Incidence and Exceptionally High Recurrence Rates Sustaining Surveillance Demand

Urothelial carcinoma accounting for approximately 90-95% of all bladder cancers is among the most expensive cancers to manage per patient lifetime due to its high recurrence and mandatory long-term endoscopic surveillance. The IARC GLOBOCAN 2022 report confirmed 614,000 new bladder cancer diagnoses globally, with the United States alone reporting approximately 83,000 new cases per the American Cancer Society in 2023.

Critically, non-muscle-invasive bladder cancer (NMIBC) the predominant disease stage recurs in 50-70% of patients within five years, requiring biannual or quarterly cystoscopy and urine cytology surveillance per EAU (European Association of Urology) and AUA clinical guidelines. This mandatory, guideline-driven surveillance creates an enormous recurring diagnostic test market that is structurally independent of new incidence rates, providing durable demand floor for the global urothelial carcinoma diagnostics industry.

Technological Innovation in Liquid Biopsy and Molecular Urinary Biomarker Tests Expanding Diagnostic Landscape

Rapid technological advancement in molecular urinary biomarker testing including DNA-based liquid biopsy panels, protein biomarker multiplex assays, and next-generation sequencing (NGS) approaches is fundamentally expanding the diagnostic toolkit beyond conventional cystoscopy and urine cytology, driving the market's accelerating CAGR. Pacific Edge Limited's Cxbladder® test range FDA-cleared and Medicare-reimbursed uses a five-gene mRNA expression panel to detect urothelial carcinoma from voided urine with sensitivity superior to cytology alone.

Abbott Molecular's UroVysion® FISH test is FDA-approved for detection and surveillance of urothelial carcinoma recurrence. The FDA's Breakthrough Device Designation has been applied to several novel urinary biomarker diagnostic platforms, accelerating regulatory review timelines. The convergence of liquid biopsy innovation, increasing awareness of urinary biomarkers as non-invasive surveillance alternatives, and growing NGS adoption across cancer centers is compelling market expansion into higher-value molecular diagnostic segments.

Market Restraints

Low Sensitivity of Urine Cytology Limiting Standalone Diagnostic Utility

Despite being a cornerstone surveillance tool for urothelial carcinoma, urine cytology's well-documented sensitivity limitations restrain the diagnostic market from transitioning away from invasive cystoscopy as the gold standard reference. Multiple studies published in the Journal of Urology confirm that urine cytology sensitivity ranges from 20-40% for low-grade urothelial carcinoma insufficient for reliable disease exclusion necessitating cystoscopic confirmation in virtually all clinically suspicious cases. This fundamental limitation perpetuates cystoscopy's dominant market position while simultaneously suppressing cytology's ability to serve as a standalone surveillance tool, constraining market volume growth for non-invasive diagnostic pathways that could otherwise expand the addressable surveillance patient population beyond urology specialist settings.

High Cost of Advanced Molecular Diagnostic Tests and Limited Reimbursement Coverage

Next-generation sequencing (NGS) and advanced molecular biomarker tests for urothelial carcinoma diagnosis and surveillance carry significantly higher per-test costs than conventional cytology or cystoscopy procedure charges, with reimbursement coverage remaining limited and variable across markets. In the United States, Centers for Medicare & Medicaid Services (CMS) coverage for molecular urothelial carcinoma biomarker tests beyond the UroVysion® FISH test and Cxbladder® panel varies by local coverage determination, creating geographic reimbursement gaps.

In Europe and Asia Pacific, NGS-based bladder cancer diagnostics face even more limited payer acceptance, restricting adoption to tertiary academic cancer centers and limiting broader clinical diffusion despite compelling clinical evidence.

Market Opportunities

Next-Generation Sequencing (NGS) and ctDNA Liquid Biopsy as the Transformative High-Growth Technology

Next-Generation Sequencing (NGS) applied to cell-free tumor DNA (ctDNA) in urine represents the most transformative technological opportunity in the Urothelial Carcinoma Diagnostics market, with the potential to fundamentally redefine non-invasive surveillance paradigms. Urine-based ctDNA liquid biopsy offers the unique advantage of directly sampling the urinary tract's liquid interface with the bladder tumor microenvironment, achieving high tumor DNA concentrations in voided urine samples.

Published studies in Nature Medicine and European Urology have demonstrated that urine ctDNA panels can detect urothelial carcinoma recurrence with sensitivity exceeding 90% in high-grade NMIBC. Companies including Nonacus Limited (with its Cell3™ Target urine ctDNA panel) and Illumina platform-based NGS assay developers are actively commercializing this opportunity. As FDA regulatory pathways for liquid biopsy diagnostics continue to evolve including the agency's Oncology Center of Excellence initiatives urine NGS-based carcinoma diagnostics are positioned for substantial market share expansion in the forecast period.

Asia Pacific Market Expansion Driven by Rising Cancer Incidence and Diagnostic Infrastructure Investment

Asia Pacific presents an exceptional Urothelial Carcinoma Diagnostics growth opportunity, as the region's large population base, rapidly rising bladder cancer incidence, and expanding diagnostic infrastructure investment create a large and underpenetrated addressable market. China, where the National Cancer Center of China reports bladder cancer as one of the most prevalent urological malignancies, is investing heavily in oncology diagnostic infrastructure through national cancer screening programs and hospital network expansion under the Healthy China 2030 initiative. Japan's National Cancer Center Hospital operates among

Asia's urothelial carcinoma diagnostic programs and India's massive oncology patient volume generate growing demand for advanced diagnostic tools as private hospital infrastructure expands. KDx Diagnostics Inc. and Sysmex Corporation are among the companies actively positioning advanced urinary diagnostic platforms for Asia Pacific market penetration, supporting the region's fastest-growing trajectory through 2033.

Category-wise Analysis

Diagnostic Test Type Insights

Cystoscopy dominates the Urothelial Carcinoma Diagnostics market by diagnostic test type, commanding approximately 43% of total market share in 2026. Cystoscopy's market leadership reflects its clinical status as the definitive gold standard for urothelial carcinoma detection, confirmation, and surveillance, endorsed by both EAU and AUA clinical guidelines as the primary diagnostic and surveillance tool for NMIBC. Despite its invasive nature, cystoscopy's unmatched sensitivity for bladder lesion visualization including advanced techniques such as Photodynamic Diagnosis (PDD/Blue Light Cystoscopy) and its simultaneous diagnostic and biopsy/resection capability, make it clinically irreplaceable.

Olympus Corporation and Karl Storz are major cystoscope technology suppliers globally. The adoption of flexible cystoscopy in office-based and ambulatory settings, improving patient tolerability, and blue-light fluorescence-enhanced cystoscopy platforms are driving technology premiumization within this dominant segment.

Technology Insights

Microscopy-based diagnostics represents the leading technology segment in the Urothelial Carcinoma Diagnostics market, accounting for approximately 42% of technology revenue in 2026. This category encompasses both conventional light microscopy-based urine cytology and advanced fluorescence microscopy techniques, including photodynamic diagnosis during cystoscopy, that collectively dominate diagnostic volumes across hospital and laboratory settings globally. Urine cytology remains universally recommended as an adjunct to cystoscopy in standard NMIBC surveillance protocols per AUA and EAU guidelines, generating high-volume recurring test procurement at relatively low per-test costs.

The updated Paris System for Reporting Urinary Cytology (TPS) published in 2022, has standardized cytopathology reporting for urothelial carcinoma, reducing inter-laboratory variability and reinforcing cytology's institutional position as the standard adjunctive surveillance technology alongside cystoscopy globally.

End-user Insights

Hospitals represent the leading end-user segment in the Urothelial Carcinoma Diagnostics market, accounting for approximately 48% of the total share in 2026. Hospitals' dominance reflects their role as the primary setting for complex urothelial carcinoma diagnosis, initial cystoscopy, transurethral resection of bladder tumor (TURBT) biopsy, and high-grade disease workup, which require full inpatient or day-surgical hospital infrastructure. Major academic medical centers with dedicated urological oncology programs, including institutions affiliated with the National Comprehensive Cancer Network (NCCN) are the highest-volume procurement sites for advanced cystoscopy systems, FISH testing reagents, and emerging molecular diagnostic platforms.

Hospital-based urology departments also drive clinical trial participation that validates novel diagnostic technologies, creating institutional preference for first-mover adoption of innovative urothelial carcinoma diagnostic tools that subsequently drive broader market adoption.

Regional Insights

North America Urothelial Carcinoma Diagnostics Market Trends and Insights

North America accounted for approximately 47% of the global urothelial carcinoma diagnostics market in 2026, supported by advanced cancer diagnostic infrastructure, favorable reimbursement, and high adoption of molecular urine tests and fluorescence-based assays. Strong clinical adherence to bladder cancer surveillance guidelines and rapid commercialization of novel biomarker platforms continue to sustain regional leadership.

U.S. Urothelial Carcinoma Diagnostics Market Trends and Insights

The U.S. represented nearly 89.2% of the North American market in 2026. The incidences of high bladder cancer, widespread use of UroVysion FISH and Cxbladder, and robust adoption of next-generation sequencing and liquid biopsy technologies at leading cancer centers. Continued FDA Breakthrough Device designations and broad Medicare reimbursement are accelerating the commercialization of advanced urine-based diagnostic assays.

Canada Urothelial Carcinoma Diagnostics Market Trends and Insights

Canada accounted for an estimated 8.1% of the regional market in 2026 and is projected to expand at a CAGR of 8.6% in the forecast period. Growth is supported by universal healthcare coverage, evidence-based surveillance practices, and increasing integration of non-invasive urinary biomarker assays in tertiary hospitals. National cancer centers are also expanding access to molecular diagnostics for recurrence monitoring and treatment planning.

Europe Urothelial Carcinoma Diagnostics Market Trends and Insights

Europe held approximately 28.4% of the global urothelial carcinoma diagnostics market in 2026, driven by strong adoption of EAU guideline-based diagnostics, broad availability of blue-light cystoscopy, and increasing use of CE-marked urinary biomarkers under the EU IVDR framework.

Germany Urothelial Carcinoma Diagnostics Market Trends and Insights

Germany is likely to capture around 23.7% of the European market in 2026. The country benefits from extensive hospital urology networks, high procedural volumes, and early adoption of advanced cystoscopy and molecular diagnostics. University hospitals are actively validating AI-assisted pathology and urine biomarker platforms to improve diagnostic sensitivity.

UK Urothelial Carcinoma Diagnostics Market Trends and Insights

UK is likely to represent approximately 15.4% of the regional market and is forecast to reach a CAGR of 8.9% in the coming years. NICE-driven technology assessments and increasing use of urine biomarker tests are supporting market expansion across NHS oncology centers. Ongoing investments in genomic medicine and centralized pathology networks are further strengthening diagnostic capabilities.

Asia Pacific Urothelial Carcinoma Diagnostics Market Insights

Asia Pacific accounted for an estimated 18.9% of the global urothelial carcinoma diagnostics market in 2026 and is projected to register the fastest regional CAGR of 10.8% in the forecast period. Growth is fueled by expanding oncology infrastructure, increasing bladder cancer incidence, and improving access to molecular diagnostics across major economies.

China Urothelial Carcinoma Diagnostics Market Trends and Insights

China held approximately 39.8% of the Asia Pacific market in 2026. Government investment in tertiary hospitals and increasing adoption of FISH and PCR-based diagnostics are accelerating market growth. Domestic manufacturers are also expanding affordable urinary biomarker offerings for large public hospital systems.

Japan Urothelial Carcinoma Diagnostics Market Trends and Insights

Japan accounted for about 24.6% of the regional market in 2026. Strong domestic participation from companies such as Sysmex and Olympus, combined with advanced hospital infrastructure, supports continued uptake of cystoscopy and molecular testing platforms. PMDA-regulated approvals and strong reimbursement coverage continue to encourage adoption of high-precision diagnostic technologies.

Competitive Landscape

The urothelial carcinoma diagnostics market is moderately fragmented, with large global diagnostics companies Roche Holding, Thermo Fisher Scientific, Illumina, Danaher (Cepheid), and Agilent Technologies competing on molecular and NGS platform breadth alongside specialized urothelial carcinoma diagnostic companies including Pacific Edge Limited (Cxbladder®), Abbott Molecular (UroVysion®), IDL Biotech (AroCell), and Nonacus Limited. Cystoscopy system leadership is held by Olympus Corporation and Philips.

Key differentiators include FDA clearance, EAU/AUA guideline inclusion, payer reimbursement status, and clinical evidence publication depth. Emerging business model trends include liquid biopsy-as-a-service models, centralized reference laboratory partnerships, and companion diagnostic co-development with immunotherapy drug manufacturers for biomarker-stratified treatment.

Key Developments

- In April 2026, Celltrion announced that the U.S. Food and Drug Administration granted Fast Track designation to CT-P71 for the treatment of patients with locally advanced or metastatic urothelial carcinoma.

- In November 2024, Roche received FDA approval for its PATHWAY® anti-HER2/neu (4B5) Rabbit Monoclonal Primary Antibody test, making it the first FDA-approved companion diagnostic for assessing HER2-positive status in biliary tract cancer patients. This expansion allows for identifying patients eligible for treatment with Jazz Pharmaceuticals' ZIIHERA®.

- In August 2024, Illumina, a leading DNA sequencing and array-based technology company, received FDA approval for its TruSight™ Oncology Comprehensive test and its first two companion diagnostic indications.

Companies Covered in Urothelial Carcinoma Diagnostics Market

- Roche Holding

- Illumina, Inc.

- IDL Biotech AB (AroCell)

- Agilent Technologies, Inc.

- Olympus Corporation

- Koninklijke Philips N.V.

- Abbott Molecular (Abbott Laboratories)

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific Inc.

- Danaher Corporation (Cepheid)

- GE HealthCare Technologies Inc.

- Pacific Edge Limited

- Nonacus Limited

- KDx Diagnostics Inc.

- Sysmex Corporation

- Others

Frequently Asked Questions

The global urothelial carcinoma diagnostics market is projected to be valued at US$ 2.1 billion in 2026, growing from US$ 1.6 billion in 2020 at a historical CAGR of 4.4% (2020-2025), and is forecast to reach US$ 3.1 billion by 2033, expanding at a CAGR of 5.8% through the forecast period.

Rising global incidence of bladder and upper tract urothelial carcinoma, coupled with increasing adoption of non-invasive urine biomarker and molecular diagnostic tests for early detection and recurrence monitoring.

North America leads the global urothelial carcinoma diagnostics market with approximately 47% of market share in 2025. The region's dominance is driven by the U.S.'s 83,000 annual bladder cancer cases per the American Cancer Society, established Medicare reimbursement pathways for Cxbladder® and UroVysion® diagnostic tests, and the highest global concentration of molecular liquid biopsy and urothelial carcinoma diagnostic technology innovators.

Development and commercialization of highly sensitive AI-enabled liquid biopsy and next-generation sequencing assays for personalized diagnosis, surveillance, and companion diagnostics in urothelial carcinoma.

The urothelial carcinoma diagnostics market features global leaders including Roche Holding, Illumina Inc., Abbott Molecular (UroVysion®), Pacific Edge Limited (Cxbladder®), Thermo Fisher Scientific, Danaher Corporation (Cepheid), Olympus Corporation, Agilent Technologies, Sysmex Corporation, Nonacus Limited (Cell3™ Target), IDL Biotech AB (AroCell), KDx Diagnostics, and GE HealthCare Technologies, competing on FDA clearance, EAU/AUA guideline inclusion, reimbursement coverage, and clinical evidence depth.