- Metalworking & Fabrication

- Underwater Welding Consumable Market

Underwater Welding Consumable Market Size, Share, and Growth Forecast 2026 - 2033

Underwater Welding Consumable Market by Types of Consumables (Electrode, Filler Metal, Flux), Welding Method (Wet, Dry, Hyperbaric), End Use (Oil and Gas Industry, Marine Infrastructure, Ship Repair and Maintenance), and Regional Analysis for 2026 - 2033

Underwater Welding Consumable Market Size and Trend Analysis

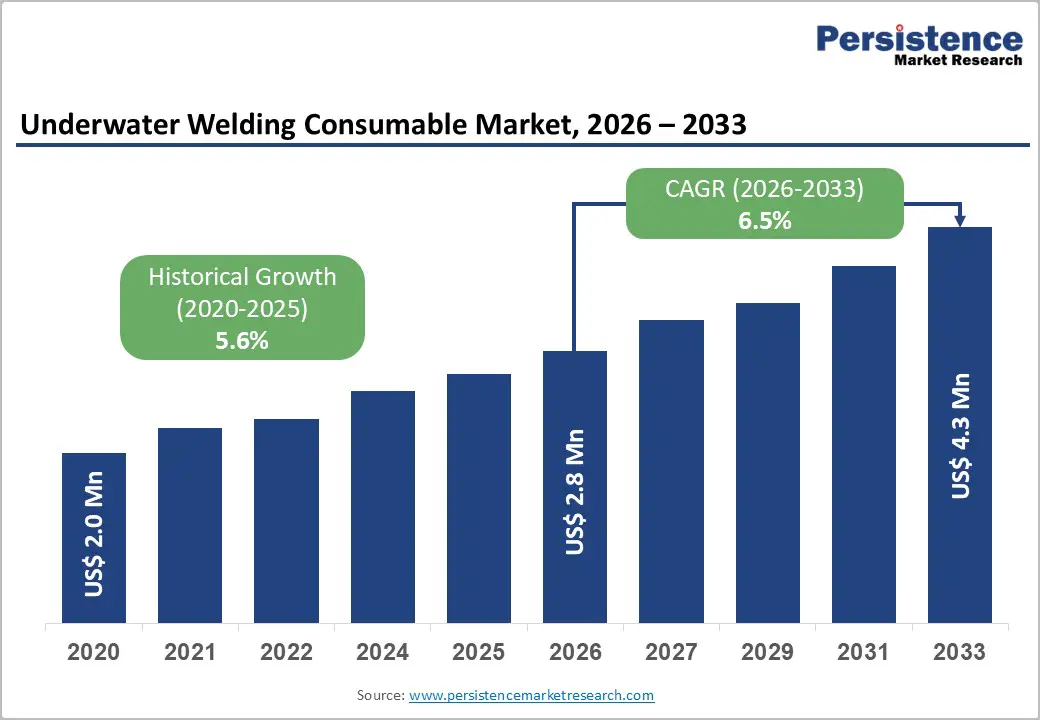

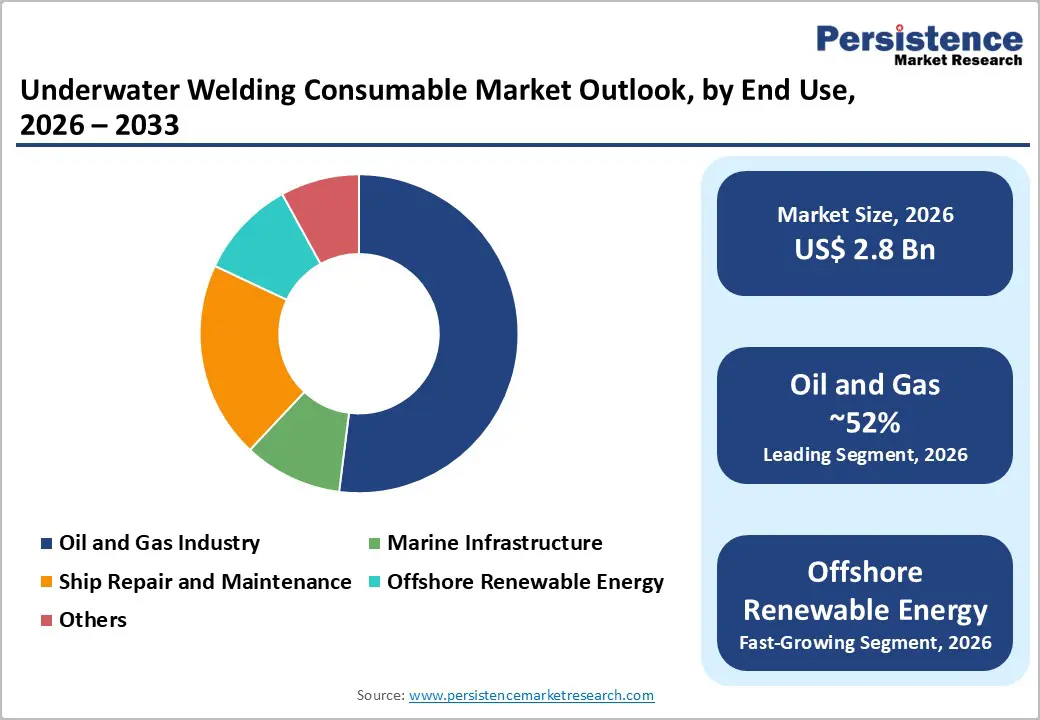

The global Underwater Welding Consumable Market size is valued at US$ 2.8 Bn in 2026 and is projected to reach US$ 4.3 Bn by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

This sustained growth is primarily driven by the accelerating global investment in offshore energy infrastructure spanning oil and gas, offshore wind, and subsea pipeline networks combined with the critical maintenance backlog accumulating across aging marine structures globally. Regulatory mandates from bodies such as the International Maritime Organization (IMO) and the American Bureau of Shipping (ABS) enforce structural integrity standards that necessitate periodic underwater welding for certification compliance, sustaining baseline consumable demand. frontiers.

Key Market Highlights

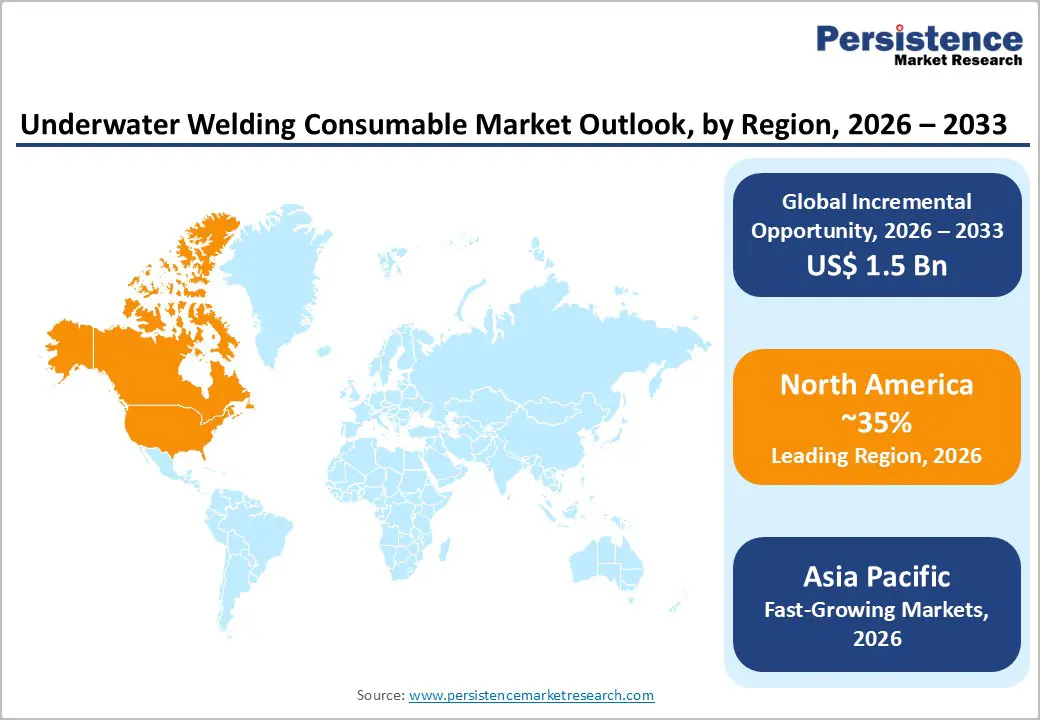

- Leading Region: North America leads the global Underwater Welding Consumable Market, holding approximately 28% revenue share, supported by the Gulf of Mexico's extensive aging offshore infrastructure, a strong regulatory framework under BSEE and ABS, and the procurement requirements of the U.S. Navy's expanding Pacific Fleet operations.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by China's offshore oil and gas expansion, South Korea's and Japan's world-leading shipbuilding volumes, and India's naval and port infrastructure programs under the Sagarmala Programmed and Project-75 India, collectively generating double-digit consumable demand growth.

- Dominant Segment: The Oil and Gas Industry end-use segment dominates with approximately 52% market revenue share, anchored by persistent maintenance demand from aging offshore platforms and pipelines in the Gulf of Mexico, North Sea, and Arabian Gulf that require regular certified underwater weld repairs.

- Fastest Growing Segment: The Offshore Renewable Energy end-use segment is the fastest-growing application, accelerated by the North Sea Investment Pact's commitment to 15 GW per year of offshore wind deployment and the expanding global fleet of offshore wind monopile foundations requiring specialized underwater welding consumables for installation and lifecycle maintenance.

- Key Market Opportunity: Hyperbaric and dry welding technology adoption in deepwater applications across the Gulf of Mexico, Brazil's pre-salt basin, and West African ultra-deepwater blocks represents the highest-value growth opportunity, as these methods require premium, tight-specification hydrogen-controlled electrodes and flux formulations commanding significant price premiums over standard wet welding materials.

| Key Insights | Details |

|---|---|

|

Underwater Welding Consumable Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2024) |

5.6% |

Market Dynamics

Market Growth Drivers

Aging Offshore Oil and Gas Infrastructure Generating Persistent Maintenance-Driven Demand

The global offshore oil and gas sector represents the single largest and most consistent source of demand for underwater welding consumables, sustained primarily by the accelerating maintenance and repair cycle for aging subsea infrastructure. Over 60% of subsea pipelines in the Gulf of Mexico currently exceed 30 years of service life, requiring frequent structural interventions including weld repair, cladding, and joint reinforcement to maintain pressure integrity and regulatory compliance. The International Energy Agency (IEA) estimates that global upstream oil and gas capital expenditure remained above US$ 500 Bn annually through 2024–2025, a significant proportion of which is directed toward offshore asset life extension programs. Platforms in the North Sea require an estimated 600–800 underwater welding operations annually per platform, owing to corrosion and fatigue damage from harsh saline environments.

Rapid Offshore Wind Farm Deployment Creating a High-Growth Adjacent End-Use Segment

The global offshore wind industry's accelerating expansion is creating a fast-growing and strategically significant new demand stream for underwater welding consumables, specifically for monopile foundation installation, array cable protection, subsea transition piece repair, and inter-array cable joint maintenance. At the January 2026 North Sea Summit in Hamburg, nine European nations including Germany, France, the United Kingdom, Denmark, and Belgium signed a landmark "Investment Pact for the North Seas" committing to deploy 15 GW of new offshore wind capacity annually between 2031 and 2040, targeting a cumulative 300 GW installed base by 2050. The Global Wind Energy Council (GWEC) reported installation of 10.8 GW of new offshore wind capacity in 2023 alone, with this figure expected to grow substantially through the forecast period.

Market Restraints

Acute Skilled Labor Shortage in the Certified Underwater Welding Profession

The global underwater welding industry faces a structural human capital deficit that materially constrains the rate of consumable consumption growth relative to available project demand. Underwater welding is among the most technically demanding and hazardous skilled trades, requiring simultaneous commercial diving certification, proficiency in wet and dry welding techniques, and knowledge of high-pressure physiology. In the United Kingdom, a 2025 report by ORE Catapult warned that approximately 50% of the 2023 certified welding workforce is expected to have retired by 2027, while offshore wind and nuclear sectors are simultaneously intensifying demand. This skills gap creates project execution delays, limits the rate at which new offshore infrastructure contracts can be serviced, and in turn suppresses the volume throughput of consumables per project cycle.

High Operational Costs and Safety Hazards Associated with Wet Welding Environments

Underwater welding operations involve substantially higher cost structures than topside equivalents, owing to saturation diving logistics, hyperbaric chamber deployment, specialized equipment rental, and stringent safety protocols mandated by OSHA and IMO standards. The fatality rate for commercial underwater welders is estimated at approximately 40 times that of conventional topside welders, imposing significant insurance, compliance, and liability costs on contractors. These combined operational cost premiums which can inflate per-project welding expenditure by 300–500% relative to surface alternatives restrict the adoption of underwater welding in cost-sensitive segments such as small port infrastructure, coastal civil engineering, and developing market offshore projects, thereby limiting the addressable consumable market.

Market Opportunities

Hyperbaric Welding Technology Adoption Unlocking Premium Consumable Demand in Deep-Water Applications

The continued commercial maturation of hyperbaric (dry) welding technology represents one of the most significant growth opportunities for premium-tier consumable manufacturers in the Underwater Welding Consumable Market. Unlike wet welding which produces welds susceptible to hydrogen-induced cracking due to direct water contact, hyperbaric welding encloses the weld zone within a pressurized, water-free habitat, enabling weld quality equivalent or superior to surface standards. This technique is increasingly mandated by operators in deepwater applications exceeding 100 m and for critical structural joints on floating production storage and offloading (FPSO) vessels, where weld failure consequences are catastrophic. Hyperbaric welding requires highly specialized consumables, including hydrogen-controlled flux-coated electrodes, precision filler metals with tight alloy composition tolerances, and flux formulations engineered for stability at pressures exceeding 10 bars, all which command substantial price premiums over standard wet welding materials.

Naval and Defence Sector Procurement Presenting a Stable, High-Value Demand Channel

Government naval procurement programs represent an underappreciated but structurally growing demand channel for underwater welding consumables, particularly for high-specification electrodes certified to military and defence standards. The U.S. Navy's expanded Pacific Fleet operations have driven a 22% growth in underwater welding consumable procurement since 2020, with NATO submarine support ships now mandated to carry electrodes capable of delivering structural welds at depths of 500 m, requiring proprietary flux formulations that prevent porosity at extreme hydrostatic pressures. South Korea's 2024 destroyer maintenance program reportedly utilized 18 tons of underwater electrodes for hull and propulsion system repairs, illustrating the substantial unit volumes generated by a single naval maintenance cycle.

Category-wise Insights

Types of Consumables Analysis

The Electrode segment is the dominant product category in the global Underwater Welding Consumable Market, accounting for approximately 48% of total revenue share. Electrodes encompassing waterproof-coated shielded metal arc welding (SMAW) rods specifically engineered for underwater applications are the consumable of first choice for wet welding operations across offshore oil and gas maintenance, ship hull repair, and marine infrastructure projects due to their unmatched portability, compatibility with a wide range of ferrous base materials, and straightforward handling by certified commercial divers. Advances in flux coating technology are progressively enhancing arc stability, reducing hydrogen-induced cracking susceptibility, and improving deposition rates in the electrode segment, strengthening its competitive position against wire-based alternatives.

Welding Method Analysis

The Wet Welding method commands the leading revenue share in the global Underwater Welding Consumable Market, representing approximately 52% of total demand. Wet welding's dominance is rooted in its operational flexibility, comparatively low setup cost, and applicability to the broadest range of shallow to medium-depth maintenance tasks that constitute most global underwater welding activity by project count. The technique requires no pressurized habitat infrastructure, allowing certified commercial divers to execute repairs directly at the weld site using waterproof electrodes without logistical mobilization delays. This simplicity makes wet welding the method of choice for routine ship repair, port infrastructure maintenance, and emergency offshore pipeline interventions where speed of response and cost efficiency are the primary criteria.

End Use Analysis

The Oil and Gas Industry segment holds the dominant position in the global Underwater Welding Consumable Market, accounting for approximately 52% of total end-use revenue share in 2024, as reported in available industry analyses. This leadership reflects the sector's unparalleled intensity of subsea welding requirements: offshore platforms, subsea pipelines, riser systems, and export flow lines all require regular structural assessment and weld repair to comply with certification standards imposed by regulatory bodies including the American Bureau of Shipping (ABS), Bureau Veritas (BV), and Det Norske Veritas (DNV). Deepwater exploration activities in the Gulf of Mexico, North Sea, Brazil's Santos Basin, and the Arabian Gulf generate persistent consumable demand for electrode and filler metal grades capable of delivering certified welds in high-salinity, high-pressure environments.

Regional Insights

North America

North America is the global leading region in the Underwater Welding Consumable Market, holding approximately 28% of market revenue, underpinned by the largest concentration of active offshore oil and gas infrastructure in the Gulf of Mexico and a highly developed regulatory ecosystem administered by the U.S. Coast Guard, OSHA, Bureau of Safety and Environmental Enforcement (BSEE), and American Bureau of Shipping (ABS). The region is home to the global headquarters of key consumable suppliers including Lincoln Electric and Broco Ranking, whose R&D investments continue to advance the performance frontier of waterproof electrode and flux technology for deepwater applications.

Concurrently, the nascent U.S. offshore wind market with over 40 GW of projects currently in various stages of development or permitting along the Atlantic and Gulf Coasts is emerging as a supplemental demand driver for marine welding consumables. The U.S. Department of Energy (DOE) and the Bureau of Ocean Energy Management (BOEM) continue to issue new offshore wind leases and advance the development of accompanying port and installation infrastructure, creating an incremental demand pipeline for specialized underwater welding solutions beyond the sector's established oil and gas base.

Europe

Europe represents the second largest and among the most strategically evolving regional markets for underwater welding consumables, driven by the coexistence of mature North Sea oil and gas asset maintenance requirements and the world's most advanced offshore wind development program. Germany, Norway, the United Kingdom, and the Netherlands are central to regional consumption, with the North Sea alone hosting thousands of aging offshore platforms and thousands of kilometers of subsea pipelines requiring regular certified weld repair.

Voestalpine Böhler Welding of Austria and ESAB, with significant European operations, are investing in advanced alloy electrode and filler metal development aligned with the increasingly stringent weld quality requirements of offshore wind monopile and jacket foundation construction. France and Spain are developing Atlantic Coast offshore wind zones that will require substantial subsea installation and maintenance welding capacity, further broadening the regional consumption base beyond the established North Sea geography.

Asia Pacific

Asia Pacific is the fastest-growing regional market for the Underwater Welding Consumable Market, projected to register the highest regional CAGR, driven by the world's largest and most active shipbuilding industry, rapid offshore energy development, and large-scale marine infrastructure investment across China, Japan, South Korea, and ASEAN nations. China leads regional consumption, with its extensive coastal and offshore energy development programs, including substantial subsea pipeline network expansion in the South China Sea, generating high-volume demand for electrodes and filler metals.

South Korea, as a global leader in naval vessel and commercial ship construction through Hyundai Heavy Industries, Samsung Heavy Industries, and DSME, generates substantial per-annum volumes of ship repair and drydock welding consumable demand with South Korea's 2024 destroyer maintenance program alone consuming 18 tons of underwater electrodes. India is emerging as a significant new demand center, with government-backed port modernization under the Sagarmala Programmed, naval expansion under Project-75 India, and offshore oil and gas development by ONGC in the Arabian Sea collectively creating a rapidly maturing underwater welding consumable market.

Competitive Landscape

The global Underwater Welding Consumable Market is moderately consolidated at the premium and specification-grade product tier, where a handful of established multinational manufacturers including ESAB, Lincoln Electric, Voestalpine Böhler Welding, and Kobe Steel, Ltd. command significant market share through proprietary flux chemistry, decades of offshore project references, and certification compliance across DNV, ABS, BV, and Lloyd's Register approval regimes. At the standard and regional tier, the market is more fragmented, with Asian manufacturers such as Tianjin Golden Bridge Welding Materials Group, Kiswel Ltd., and Kobelco Welding of America competing on price competitiveness and regional distribution depth.

Key Market Developments

- In October 2024, Broco Rankin announced its acquisition of Ready Welder Corporation, a company specializing in portable welding products. This acquisition enhances Broco Rankin’s portfolio, particularly in the underwater welding sector, by incorporating the ReadyWelder II, a battery-powered welder designed for remote applications.

- In January 2024, ESAB Corporation, based in the U.S., launched a new line of underwater welding consumables aimed at the oil and gas industry. This innovation enhances welding efficiency and durability in extreme conditions, solidifying ESAB’s leadership in the underwater welding market.

- In March 2023, U.S.-based Lincoln Electric Holdings, Inc. extended its product portfolio with the introduction of high-performance underwater welding electrodes. This new range is designed for deep-sea applications, offering improved corrosion resistance and structural integrity.

Companies Covered in Underwater Welding Consumable Market

- Broco Ranking

- ESAB (Elektriska Svetsnings-Aktiebolaget)

- Lincoln Electric

- Air Liquide Welding

- Kobelco Welding of America

- Sandvik AB

- Voestalpine Böhler Welding

- Tianjin Golden Bridge Welding Materials Group

- Kiswel Ltd.

- Arcon Welding Equipment

- Gedik Welding

- Kobe Steel Ltd. Other Key Players

Frequently Asked Questions

The global Underwater Welding Consumable Market is valued at US$ 2.8 Bn in 2026 and is projected to reach US$ 4.3 Bn by 2033, expanding at a CAGR of 6.5% over the forecast period. The market registered a historical growth rate of 5.6% CAGR between 2020 and 2025, supported by consistent demand from offshore oil and gas maintenance and ship repair sectors.

The primary demand drivers are the critical maintenance and repair requirements of aging offshore oil and gas infrastructure with over 60% of Gulf of Mexico subsea pipelines exceeding 30 years of service combined with the accelerating global deployment of offshore wind farms, particularly following the North Sea Investment Pact's commitment to 300 GW of offshore wind by 2050.

The Oil and Gas Industry segment leads the market with approximately 52% of total end-use revenue share, driven by the extensive and persistent requirement for subsea pipeline maintenance, offshore platform structural repair, and riser system interventions. Regulatory certification mandates from ABS, DNV, and Bureau Veritas enforce compliance-based maintenance cycles that generate non-discretionary consumable demand regardless of commodity price fluctuations.

North America holds the dominant regional position in the Underwater Welding Consumable Market, accounting for approximately 28% of global revenue, underpinned by the Gulf of Mexico's vast offshore infrastructure base, a stringent regulatory environment under BSEE and U.S. Coast Guard oversight, and the procurement scale of the U.S. Navy's expanding Pacific and Atlantic Fleet operations requiring defence-grade underwater welding materials.

The leading companies in the global Underwater Welding Consumable Market include ESAB Lincoln Electric, Voestalpine Böhler Welding, Kobe Steel, Ltd., Kobelco Welding of America, Air Liquide Welding, Sandvik AB, Tianjin Golden Bridge Welding Materials Group, Kiswel Ltd., Broco Ranking, Arcon Welding Equipment, and Gedik Welding, among others.