- Marine

- Tugboat Market

Tugboat Market Size, Share, and Growth Forecast 2026 - 2033

Tugboat Market by Boat Type (Conventional Tug, Tractor Tug, Azimuthal Stern Drive (ASD) Tugs, Others), Engine Power (< 2,000 HP, 2,000–5,000 HP, 5,000–8,000 HP, > 8,000 HP), Service Type (Harbour Assistance, Towage & Salvage, Escort Services, Offshore Support, Ice-Breaking, Others), Fuel Type (ICE, Hybrid, Electric), and Regional Analysis for 2026 - 2033

Tugboat Market Size and Trend Analysis

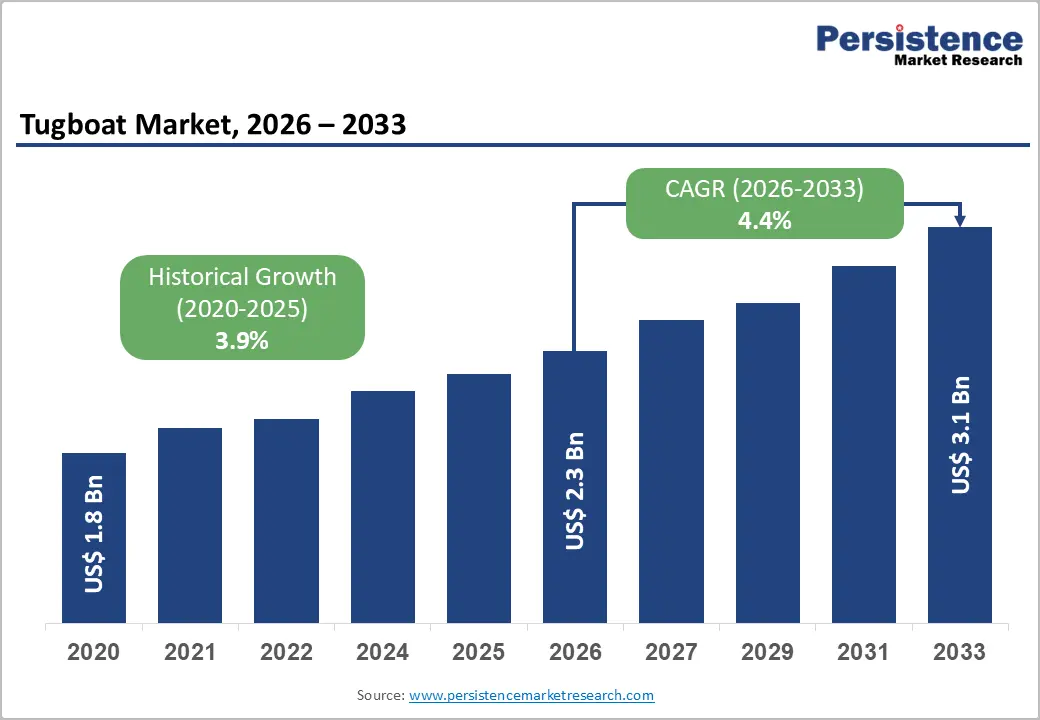

The global Tugboat market size is valued at US$ 2.3 Bn in 2026 and is projected to reach US$ 3.1 Bn by 2033, growing at a CAGR of 4.4% between 2026 and 2033. This consistent growth is driven by rising global seaborne trade volumes, large-scale port infrastructure modernization programs, and the expanding operational requirements of offshore energy industries, all of which increase demand for harbour assistance, escort, and offshore support tug services.

According to UNCTAD's Review of Maritime Transport 2025, global seaborne trade grew by 2.2% in 2024, with ton-miles expanding by 5.9% due to longer shipping routes, while UNCTAD projects maritime trade to grow at an average annual rate of 2.4% through 2025–2029, creating sustained fleet expansion and replacement demand for advanced tugboats at ports and offshore operations worldwide.

Key Industry Highlights:

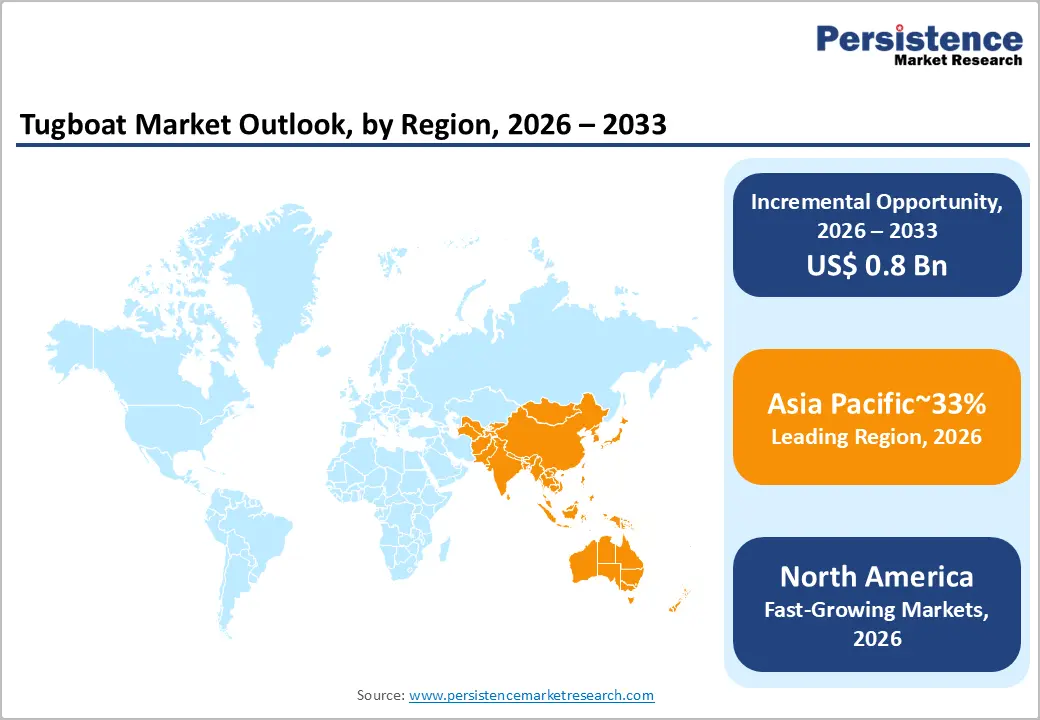

- Leading Region: Asia Pacific dominates the global Tugboat market, handling approximately 63% of global container trade per UNCTAD, with China's ports processing over 270 million TEUs annually and India's Sagarmala Programme allocating over US$ 10 billion in port-led development generating structural harbour tug demand.

- Fastest Growing Region: Asia Pacific is simultaneously the fastest-growing region, with India, Vietnam, Indonesia, and Malaysia rapidly expanding port infrastructure under government-backed programs, India's offshore Sagarmala investment pipeline, and China's Belt and Road Initiative driving port construction across the broader region through 2033.

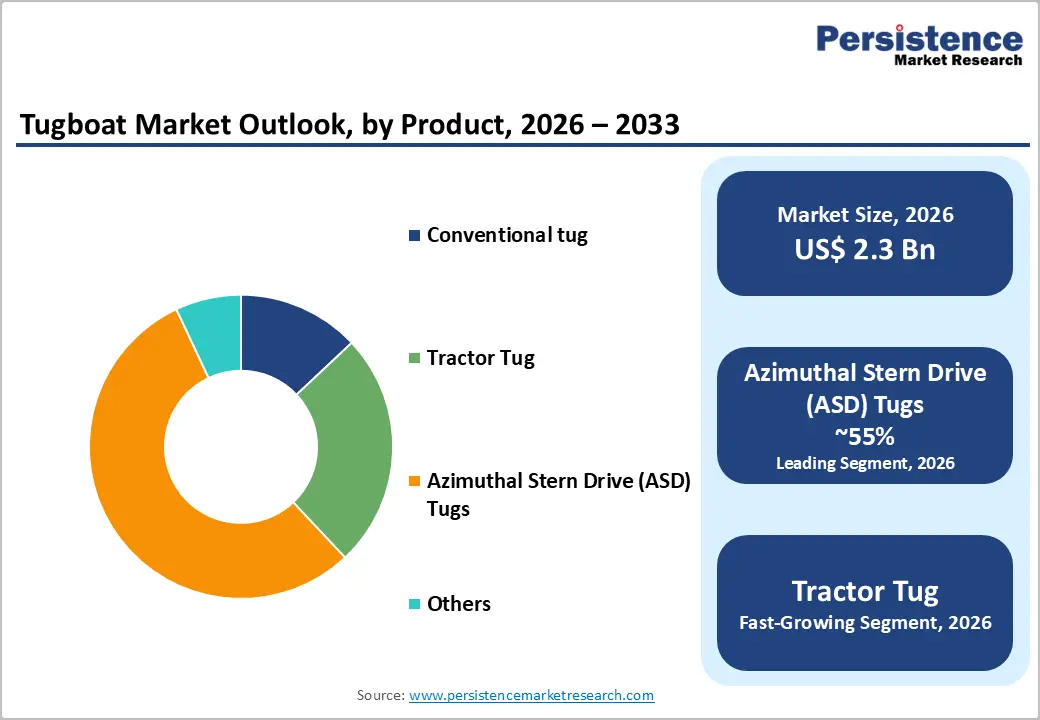

- Dominant Segment: Azimuthal Stern Drive (ASD) Tugs dominate the boat type category with approximately 55% of global Tugboat market revenue, favored for their 360-degree thruster maneuverability, superior bollard pull efficiency, and operational safety when handling ultra-large container vessels across the world's busiest container and bulk commodity ports.

- Fastest Growing Segment: The Electric and Hybrid fuel type segment is the fastest-growing category, driven by the IMO's 2050 net-zero target, EU Green Deal port mandates, and research confirming that electric tugboats reduce port CO2 emissions by up to 91.83% versus diesel fleets, prompting accelerating procurement by progressive port authorities in Norway, the Netherlands, Singapore, and South Korea.

- Key Market Opportunity: The offshore wind construction boom, with the EU targeting 120 GW by 2030 and BOEM leasing over 20 million acres of U.S. Atlantic offshore area, creates a high-value, long-duration demand opportunity for offshore support and anchor handling tug operators offering specialized wind farm construction and O&M tug services.

| Global Market Attributes | Key Insights |

|---|---|

|

Tugboat Market Size (2026E) |

US$ 2.3 Bn |

|

Market Value Forecast (2033F) |

US$ 3.1 Bn |

|

Projected Growth CAGR (2026–2033) |

4.4% |

|

Historical Market Growth (2020–2025) |

3.9% |

DRO Analysis

Drivers - Surging Global Seaborne Trade and Port Infrastructure Modernization Amplifying Tug Fleet Demand

The continuous expansion of global maritime trade is the most fundamental structural driver underpinning tugboat market growth, as every increase in port calls by commercial vessels generates direct demand for harbour assistance, berthing and unberthing support, and escort tug services. UNCTAD's Review of Maritime Transport 2025 confirmed seaborne trade growth of 2.2% in 2024, with a record of nearly 250,000 container ship port calls recorded in the second half of 2023 alone. The progressive deployment of ultra-large container vessels (ULCVs), with capacities exceeding 24,000 TEU, and megasize bulk carriers in the world's major ports requires more powerful and maneuverable tugs capable of managing these vessels in constrained harbour environments.

Ports across Asia, Europe, and North America are investing substantially in infrastructure deepening, terminal expansion, and berth modernization. The U.S. Army Corps of Engineers allocated US$ 2 billion for port improvement initiatives in 2024, directly stimulating demand for advanced ASD and tractor tugs at deepened berths. This combination of rising port call frequency, larger vessel deployment, and infrastructure investment creates a structurally expanding demand base for the global tugboat market through 2033.

Offshore Energy Sector Expansion Generating Growing Tug Support Service Demand

The rapid growth of both offshore oil and gas operations and the emerging offshore wind energy sector is generating substantial new demand streams for tugboats performing towing, anchor handling, platform support, and offshore construction assistance services. Oil & gas remains the primary offshore support demand sector, accounting for approximately 67% of offshore support vessel utilization in 2024. Simultaneously, the European Union's offshore wind expansion target of 120 GW installed by 2030, rising to 300 GW by 2050 from approximately 30 GW today, is creating large, persistent requirements for specialized tug and support vessel operations across the North Sea, Baltic Sea, and Atlantic development zones.

Offshore wind construction requires tugs for turbine foundation towing, cable-lay vessel support, platform positioning, and emergency response operations, with major wind developers including Ørsted, Vattenfall, and SSE Renewables contracting dedicated support fleets for long-duration operations and maintenance programs. Similarly, Petrobras's deepwater expansion in Brazil and Saudi Aramco's offshore operations in the Arabian Gulf are sustaining multi-year anchor handling and offshore supply tug service contracts, adding recurring revenue streams for global tug operators and builders.

Restraints - IMO Emissions Regulations Imposing Heavy Capital Compliance Costs on Tug Operators

The International Maritime Organization's (IMO) progressively tightening emissions framework, targeting a 40% reduction in CO2 intensity by 2030 and at least a 70% reduction by 2050 relative to 2008 levels, is imposing significant capital and operational compliance costs on tug operators, constraining fleet profitability and slowing new vessel procurement decisions. Tugboat operations contribute approximately 28% of total CO2 emissions from port activities.

Meeting IMO Tier III NO2 standards requires costly selective catalytic reduction (SCR) or exhaust gas recirculation (EGR) systems, while complying with Emission Control Area (ECA) sulfur limits necessitates low-sulfur fuel adoption or scrubber installation, each adding meaningful capital and operational expenditure per vessel. For smaller independent tug operators with constrained balance sheets, these compliance obligations can preclude fleet renewal entirely.

High Vessel Acquisition and Newbuild Costs Limiting Fleet Expansion for Smaller Operators

The capital-intensive nature of tugboat newbuilds, particularly for advanced ASD and hybrid-electric vessels equipped with modern propulsion and IMO Tier III-compliant engine configurations, poses a significant market access barrier for small and medium-sized tug operators in developing markets. A modern ASD tug with 80-tonne bollard pull, IMO Tier III engines, and fire-fighting capability, such as Sanmar's Deliçay Class delivered to H. Schramm Towage in 2025, requires multi-million dollar investment per unit.

Rising global steel and marine equipment costs, combined with constrained shipyard capacity, are extending delivery lead times and pushing newbuild prices higher. This financial barrier limits fleet modernization rates for second-tier operators, particularly in Latin America, Africa, and South Asia, suppressing addressable market growth in these regions.

Opportunities - Electric and Hybrid Tug Electrification: Regulatory Convergence Creating a Green Fleet Replacement Wave

The mandatory decarbonization of port operations under the IMO's 2050 net-zero strategy, the EU Green Deal, and national port sustainability mandates is creating a compelling and time-bound market opportunity for manufacturers developing electric and hybrid tugboat platforms. Research published in the journal Transportation Research Part D confirms that introducing electric tugboats can reduce total port CO2 emissions by up to 91.83% compared to a diesel-only fleet, a performance advantage that is convincing port authorities worldwide to mandate low-emission tug procurement in new service contracts. The IDTechEx report on Electric Boats and Ships 2024–2044 identifies batteries for pure electric tugboats as one of the clearest and most commercially viable near-term electrification pathways in maritime, given tugs' short-range operations and predictable duty cycles that favor high-cycle battery architectures.

Norway and the Netherlands are already leading the commercialization of hybrid and electric tugs in European ports, supported by the EU Innovation Fund and national maritime decarbonization subsidies. Shipbuilders including Damen Shipyards and Sanmar are actively developing IMO Tier III-compliant and hybrid tug designs to serve this growing green fleet replacement wave. Companies that secure first-mover positions in certified low-emission tug platforms will benefit from structural regulatory tailwinds and premium contract pricing through 2033 and beyond.

Offshore Wind Construction Boom: Anchor Handling and Towing Services in Fast-Growth Demand

The unprecedented acceleration of offshore wind development, particularly across the North Sea, U.S. East Coast, and Asia Pacific, is opening a high-growth, long-duration service opportunity for specialized anchor handling and offshore construction support tug operations. The EU's target of 120 GW of offshore wind by 2030, representing a fourfold capacity increase from today's approximately 30 GW installed, will require years of foundation installation, cable laying, turbine positioning, and platform commissioning activities, each requiring dedicated tug support. In the United States, the Bureau of Ocean Energy Management (BOEM) has leased over 20 million acres of offshore areas for wind development along the Atlantic and Gulf coasts, creating a multi-decade pipeline of offshore construction tug service demand.

Damen Shipyards has capitalized on this trend, securing orders for ASD tugboats for ports in New Zealand and contracting 13 new ASD tugs for Edison Chouest Offshore, one of the most significant newbuild orders in the U.S. offshore support market in recent years. Tug operators that invest in versatile, high-bollard-pull offshore support vessels certified for offshore wind construction operations are positioned to capture premium day-rate contracts from major energy developers through the 2026–2033 forecast horizon.

Category-wise Analysis

Boat Type Insights

Azimuthal Stern Drive (ASD) Tugs are the leading boat type segment, commanding approximately 55% of total global Tugboat market revenue. ASD tugs derive their market dominance from their 360-degree rotating azimuth thruster propulsion system, which delivers unmatched omnidirectional maneuverability, higher bollard pull efficiency, and superior operational safety compared to conventional tug configurations, making them the preferred platform across high-traffic commercial ports, offshore support operations, and escort service applications.

As container ships and bulk carriers have grown progressively larger over the past decade, ASD tugs' precision control capability has become an operational necessity for safe berthing in confined harbour channels. The ASD tug segment recorded a global market valuation of US$ 1.2 Bn in 2024, with leading shipbuilders Damen Shipyards and Sanmar Shipyards dominating the orderbook. In Q3 2025, Damen Shipyards secured fresh orders for ASD 2312 design tugs, featuring IMO Tier III-compliant propulsion, for Port Marlborough in New Zealand, reflecting the sustained global preference for ASD configurations in port modernization programs.

Engine Power Insights

The 5,000–8,000 HP engine power segment leads the market, accounting for approximately 37% of total global revenue. This mid-to-high power range is the dominant configuration for commercial harbour assistance and offshore support operations, where adequate bollard pull, typically in the 60–100 tonne range for port applications and above 100 tonnes for offshore anchor handling, requires diesel engines in the 5,000–8,000 HP output bracket.

The widespread adoption of Caterpillar, MaK (Caterpillar Marine), MTU, and Wärtsilä main engines in this power class, combined with Kongsberg and Rolls-Royce Marine azimuth thrusters, reflects the segment's alignment with commercial port requirements. Sanmar's Deliçay Class vessels, fitted with Caterpillar 'E' series engines and Kongsberg thrusters achieving 80-tonne bollard pull, are representative of this segment's commercial mainstream. Growing demand for high-power tugs capable of safely handling ultra-large container vessels (ULCVs) is further reinforcing this engine power band's market leadership.

Service Type Insights

Harbour Assistance is the leading service type segment, accounting for approximately 40% of total global Tugboat market revenue. This segment encompasses all tug operations supporting the berthing, unberthing, and in-port maneuvering of commercial vessels, the single most frequently demanded tug service globally given the volume and frequency of vessel calls at commercial terminals. According to UNCTAD's Review of Maritime Transport 2024, nearly 250,000 container ship port calls were recorded in the second half of 2023 alone, with the Asia Pacific region handling 63% of global container trade and generating the highest absolute volume of harbour tug service demand.

The progressive deployment of ultra-large container vessels (ULCVs) and Very Large Crude Carriers (VLCCs), whose sheer size requires mandatory minimum tug escort and berthing assistance irrespective of weather conditions, is embedding harbour assistance as a structurally non-discretionary demand category in port operations contracts globally, sustaining this segment's dominant revenue position through 2033.

Fuel Type Insights

ICE (Internal Combustion Engine) tugboats constitute the dominant fuel type segment, accounting for approximately 70% of total global Tugboat market revenue. The near-universal prevalence of diesel-powered ICE propulsion in the existing global tug fleet, which numbers several thousand vessels, and the high capital cost of full fleet electrification or hybrid retrofitting sustain ICE's dominant commercial position across the 2026–2033 forecast period.

Conventional diesel engines, particularly IMO Tier III-compliant configurations from Caterpillar, Wärtsilä, and MTU, remain the most commercially viable solution for operators in markets where shore power charging infrastructure for electric tugs is unavailable, which includes the majority of ports in Africa, Southeast Asia, and Latin America. While hybrid and electric tugs are growing in absolute deployment volume, driven by ports in Europe and East Asia, the ICE segment will retain dominant market share throughout the forecast period as fleet replacement cycles are extended by asset longevity and capital constraints among smaller operators.

Regional Analysis

North America Tugboat Trends & Insights

The United States is the largest individual national market for tugboats in North America, underpinned by one of the world's most extensive port and inland waterway networks, a large active commercial tug fleet, and significant publicly funded port infrastructure investment. The U.S. Army Corps of Engineers allocated US$ 2 billion for port improvement initiatives in 2024, directly expanding harbour infrastructure that requires tug support services. BOEM's active offshore wind leasing program, covering over 20 million acres of U.S. Atlantic and Gulf Coast offshore areas, is simultaneously expanding the demand base for offshore support and anchor handling tug services. The Jones Act (Merchant Marine Act of 1920) mandates U.S.-built, -owned, and -crewed vessels for domestic waterway operations, creating a structurally protected domestic market for U.S. shipbuilders including Eastern Shipbuilding Group, Nichols Brothers Boat Builders, and Washburn & Doughty Associates.

Crowley Maritime Corporation, one of the largest U.S. tug operators, and Edison Chouest Offshore have both placed significant newbuild orders with Damen Shipyards for ASD tugs featuring IMO Tier III-compliant propulsion in 2025. Canada contributes Arctic ice-breaking tug demand, with the Canadian Coast Guard expanding its icebreaker and escort tug fleet for Arctic Sovereignty and Northern shipping route support programs. Combined, North America represents one of the highest-value regional markets for both conventional harbour and offshore support tugboats, with sustained investment in fleet modernization and green tug technology adoption.

Europe Tugboat Trends & Insights

Europe is the world's most innovation-driven tugboat region, at the vanguard of hybrid and zero-emission tug development, driven by the European Union's Green Deal, FuelEU Maritime regulation, and the IMO's decarbonization targets. Norway and the Netherlands, home to globally leading naval architects and tug operators, have pioneered hybrid electric tug deployments in their ports, with Kongsberg, Wärtsilä, and Robert Allan Ltd. developing the propulsion and design architectures adopted by mainstream builders, including Damen Shipyards and Sanmar. The North Sea's vast offshore wind construction program, with the UK, Germany, Denmark, and the Netherlands collectively targeting over 80 GW of offshore wind by 2030, is generating enormous sustained demand for offshore support tugs.

Germany's harbour tug activity is sustained by major commercial ports in Hamburg, Bremen, and Kiel, with operators including H. Schramm Towage, which contracted a new twin Z-drive tractor tug from Sanmar at TugTechnology 2025 in Antwerp, continuously modernizing their fleets. Spain's Barcelona and Valencia terminals and France's Le Havre and Marseille ports are expanding capacity under TEN-T (Trans-European Transport Networks) infrastructure programs, stimulating replacement tug procurement. Europe's combination of strict emission regulations, offshore energy expansion, and well-capitalized port operators makes it the world's leading market for technology-advanced, low-emission tugboat innovation and commercial deployment through 2033.

Asia Pacific Tugboat Trends & Insights

Asia Pacific is the world's largest regional tugboat market by volume and the fastest-growing by growth rate, driven by the region's dominant share of global container trade, approximately 63% per UNCTAD, and massive investments in port capacity expansion across China, India, Singapore, and Southeast Asia. China's Belt and Road Initiative (BRI) is financing port infrastructure projects across Southeast Asia, South Asia, and Africa, indirectly generating demand for tug fleets at newly constructed and expanded terminals. China's domestic ports, which handled over 270 million TEUs in 2023, collectively represent the world's highest absolute volume of harbour tug service demand, with COSCO Shipping Heavy Industry and domestic builders producing large numbers of ASD tugs annually.

India's Cochin Shipyard Limited, a listed government enterprise, is actively expanding its tug construction capacity and has received multiple domestic orders for harbour tugs from Indian Port Trust bodies under the Sagarmala Programme, which has allocated over US$ 10 billion for port-led development nationwide. Singapore, as the world's busiest transshipment hub, operates a large fleet of advanced harbour tugs and has become a test bed for electric and LNG-powered tug technologies. Japan's Mitsui O.S.K. Lines (MOL Group) has invested in hybrid tug development for domestic port operations. ASEAN nations including Vietnam, Indonesia, Malaysia, and the Philippines are expanding port infrastructure rapidly, with government-backed programs creating new tug procurement pipelines throughout the 2026–2033 period.

Competitive Landscape

The global Tugboat market exhibits a moderately fragmented competitive structure, with a small number of globally dominant shipbuilders, led by Damen Shipyards and Sanmar Shipyards, competing alongside a large number of regional and national builders and operators. Key competitive differentiators include bollard pull capacity, propulsion technology (ASD vs. tractor vs. conventional), IMO Tier III compliance, and low-emission propulsion options.

Market leaders compete on proprietary tug designs developed in partnership with specialist naval architects, Robert Allan Ltd., Wartsila Ship Design, and Damen's in-house team, combined with after-sale service, spare parts networks, and financial structuring for fleet renewal contracts. Emerging competitive trends include outcome-based service contracts (per port call pricing), hybrid-electric vessel leasing, and remote monitoring of tug operations through digital fleet management platforms.

Key Developments:

- June 2025, Sanmar Shipyards secured a new order from German tug operator H. Schramm Towage for a Deliçay Class twin Z-drive tractor tug, achieving 80-tonne bollard pull and fitted with IMO Tier III-compliant Caterpillar engines and Kongsberg thrusters, at the TugTechnology 2025 conference in Antwerp.

- Q3 2025, Damen Shipyards secured multiple orders for ASD 2312 design tugboats, featuring IMO Tier III-compliant propulsion, for Port Marlborough in New Zealand and for offshore operator Edison Chouest Offshore, reflecting sustained newbuild demand globally.

- In 2025, Global tugboat newbuild deliveries reached a strong multi-year high, with leading shipyards building vessels equipped with emission-reducing technologies as fleet owners globally expanded fleets to meet rising port call volumes, offshore wind construction demand, and IMO Tier III emissions compliance requirements.

Companies Covered in Tugboat Market

- Damen Shipyards Group

- Sanmar Shipyards

- Ranger Tugs

- ODC Marine

- Gladding-Hearn

- MERRÉ

- Norfolk Tug Company

- SYM Naval

- Crowley Maritime Corporation

- Cochin Shipyard Limited

- Cheoy Lee Shipyards Ltd

- mol Group

- Eastern Shipbuilding Group

- Nichols Brothers Boat Builders

- Washburn & Doughty Associates

Frequently Asked Questions

The global Tugboat market is valued at US$ 2.3 Bn in 2026 and is projected to reach US$ 3.1 Bn by 2033, growing at a CAGR of 4.4% during the forecast period. The market is supported by UNCTAD's confirmed 2.2% growth in global seaborne trade in 2024, projected to continue at 2.4% annually through 2025–2029, driving sustained harbour tug fleet expansion at ports worldwide.

The two primary demand drivers are: (1) rising global seaborne trade and port infrastructure investment, with the U.S. Army Corps of Engineers allocating US$ 2 billion for port improvements in 2024, increasing harbour tug service demand; and (2) the offshore energy sector expansion, particularly the EU's offshore wind target of 120 GW by 2030, creating sustained anchor handling and construction tug service demand across the North Sea and beyond.

Azimuthal Stern Drive (ASD) Tugs lead the Boat Type category with approximately 55% of global market revenue. Their 360-degree rotating propulsion system delivers unmatched maneuverability for berthing and unberthing ultra-large container vessels and VLCCs. Damen Shipyards secured new ASD 2312 orders for Port Marlborough, New Zealand in Q3 2025, and Sanmar built its seventh ASD-design tug for H. Schramm Towage in 2025.

Asia Pacific leads the global Tugboat market, driven by the region's 63% share of global container trade per UNCTAD, China's ports processing over 270 million TEUs annually, and India's Sagarmala Programme's over US$ 10 billion port investment allocation. The region simultaneously generates the highest volume of harbour tug service demand and is the fastest-growing market for new tug procurement through 2033.

The most significant opportunity is the offshore wind construction boom: the EU's target of 120 GW of offshore wind capacity by 2030, a fourfold increase from today, combined with BOEM's over 20 million acres of U.S. Atlantic offshore leasing, creates a multi-decade, high-value pipeline for specialized anchor handling, towing, and offshore support tug services, with leading operators and builders already securing dedicated long-term contracts with major energy developers.