- Automation & Robotics

- Testing, Inspection, and Certification (TIC) Market

Testing, Inspection, and Certification (TIC) Market Size, Share, and Growth Forecast 2026–2033

Testing, Inspection, and Certification (TIC) Market by Service Type (Testing, Inspection, Certification), Sourcing Type (In-House, Outsourced), Application (Environmental Services, Education, Government, Consumer Goods & Retail, Agriculture, Food, Chemicals, Infrastructure, Automotive, Others), and Regional Analysis for 2026–2033

Testing, Inspection, and Certification (TIC) Market Size and Trend Analysis

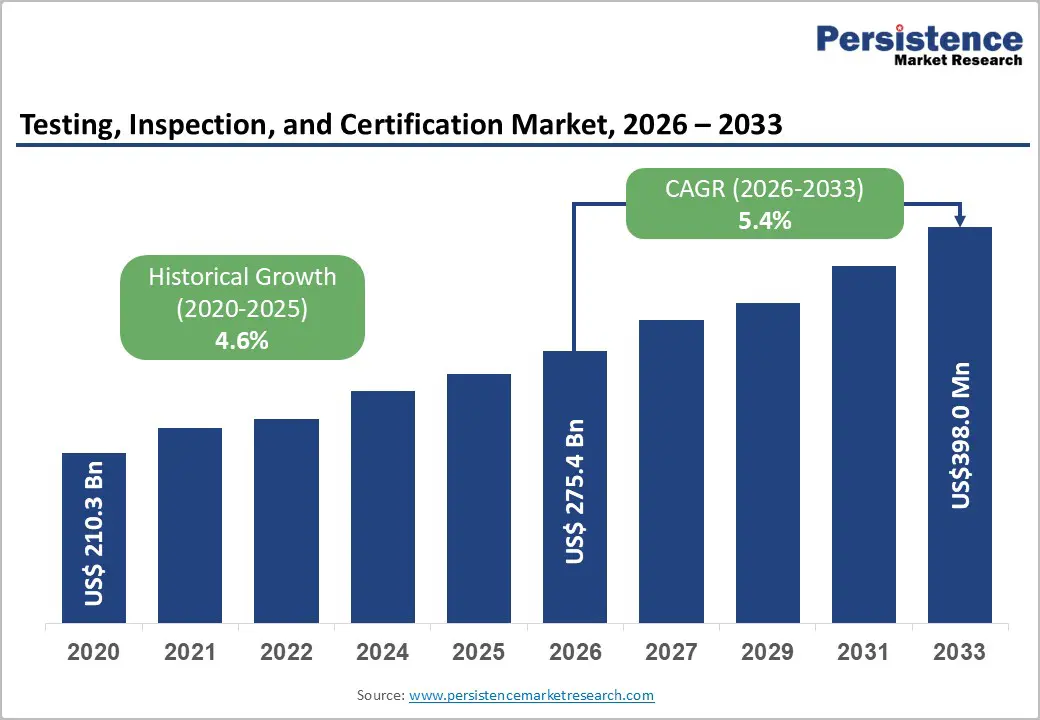

The global testing, inspection, and certification (TIC) market size is expected to be valued at approximately US$ 277.0 billion in 2026 and is projected to reach US$ 398.0 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. This growth is fundamentally driven by the proliferating complexity of global regulatory frameworks, the accelerating pace of international trade requiring third-party compliance verification, and rising consumer and industrial expectations for product safety, environmental conformilty, and supply chain transparency.

Stringent EU, U.S. FDA, and WTO Technical Barriers to Trade (TBT) Agreement compliance requirements are compelling manufacturers across food, chemicals, automotive, and consumer goods sectors to outsource quality assurance to accredited TIC providers creating structural, recurring demand that expands in line with global manufacturing output and trade volumes.

Key Industry Highlights:

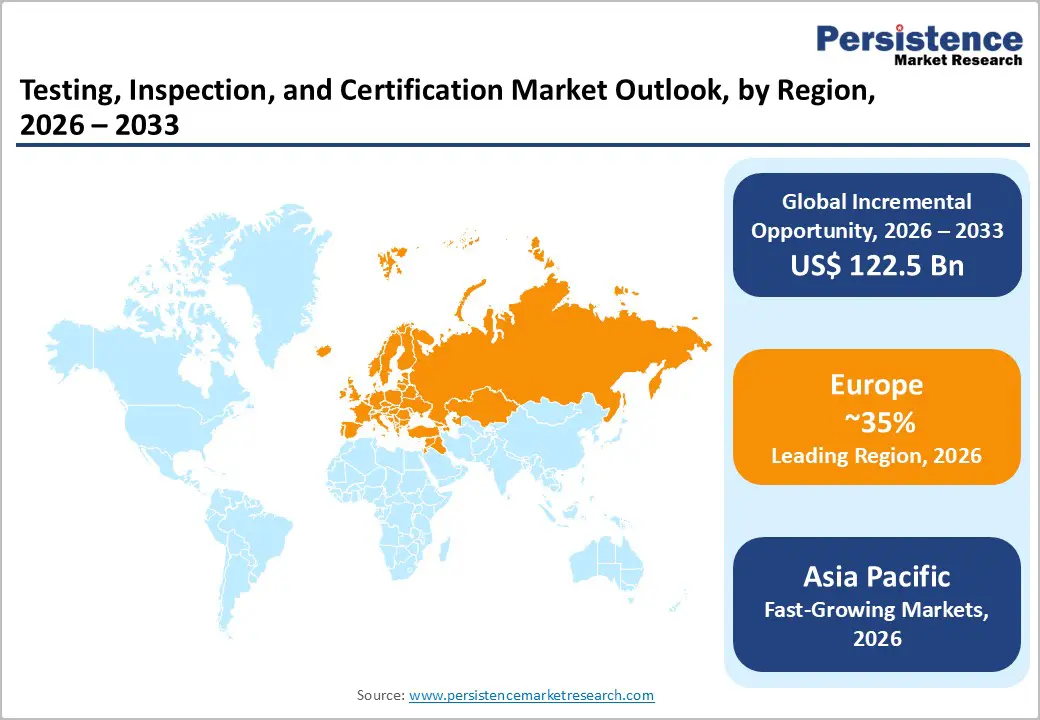

- Leading Region – Europe leads the global TIC market with the highest regulatory density globally, anchored by the EU CE Marking, REACH, and EU Green Deal frameworks that mandate accredited third-party conformity assessment across virtually all product categories and supply chain stages.

- Fast-Growing Market – Asia Pacific is the fastest-growing TIC region, driven by China's CCC mandatory certification expansion, India's BIS Act 2016 rollout, and ASEAN standards harmonization collectively creating unprecedented demand for accredited TIC services across the region's manufacturing export base.

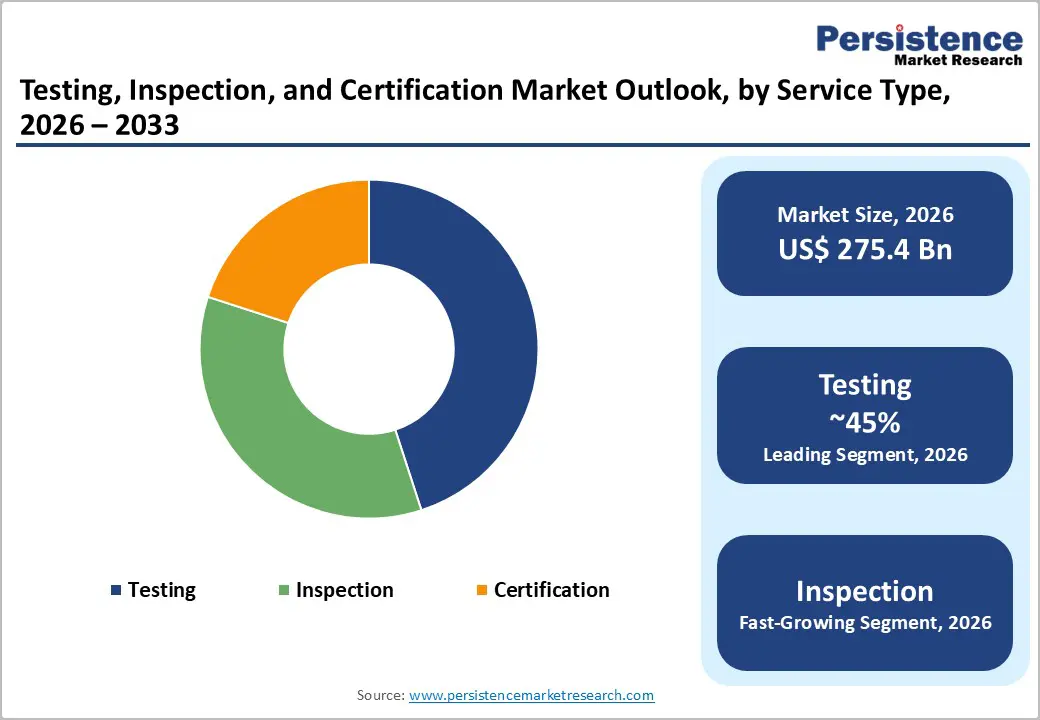

- Dominant Service Type – Testing led the service type category with 45% share in 2025, serving as the technical foundation for certification and inspection decisions across food, pharmaceutical, automotive, and consumer goods sectors worldwide under ISO/IEC 17025 accredited frameworks.

- Fastest Growing Segment – Automotive TIC is the fastest-growing application, propelled by EV battery safety testing per ISO 6469 and UN Regulation No. 100, ADAS sensor certification, and expanding EU General Safety Regulation mandates requiring comprehensive vehicle system conformity assessment.

- Key Opportunity: Digital TIC transformation including AI-powered defect detection, drone inspection, and blockchain-based digital certificates enables TIC providers to reduce delivery costs by 30–40% while expanding into remote and continuous monitoring applications, creating a premium, scalable service differentiation opportunity.

DRO Analysis

Drivers - Expanding Global Regulatory Complexity and Trade Compliance Requirements Are Structurally Driving TIC Outsourcing Demand

The progressive tightening and proliferation of national and international regulatory frameworks governing product safety, environmental performance, and quality management is the most consequential structural driver of TIC market demand. The World Trade Organization (WTO) administers the Technical Barriers to Trade (TBT) Agreement, under which member nations notified over 35,000 technical regulations since 2010, each representing a compliance verification requirement for exporters.

The European Union's regulatory framework encompassing the CE Marking Regulation, REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), RoHS Directive, and General Food Law Regulation (EC) 178/2002 obliges manufacturers serving EU markets to demonstrate certified compliance through accredited third-party testing and certification. The U.S. Consumer Product Safety Improvement Act (CPSIA) similarly mandates third-party testing for children's products sold in the U.S. market.

Global Food Safety Concerns and Stricter Regulatory Enforcement Are Generating Sustained Growth in Food and Agriculture TIC Services

Food safety testing and certification represent one of the largest and most rapidly expanding application segments within the TIC market, driven by intensifying regulatory enforcement, high-profile contamination incidents, and global consumers' rising demand for verified food provenance and quality. The WHO estimates that approximately 600 million people nearly 1 in 10 globally fall ill from contaminated food annually, generating sustained political and regulatory pressure for robust food testing infrastructure.

The Codex Alimentarius Commission (jointly administered by WHO and FAO) sets international food safety standards adopted by 188 member nations, and compliance verification through accredited laboratories is a prerequisite for participation in international food trade. The U.S. FDA Food Safety Modernization Act (FSMA) the most sweeping U.S. food safety reform in 70 years has significantly expanded mandatory testing and third-party auditing requirements across the food supply chain, amplifying demand for accredited TIC service providers with food-specific laboratory capabilities.

Restraints - High Capital Investment and Accreditation Costs Create Significant Barriers to Entry and Limit Market Participation

Establishing and maintaining accredited TIC operations requires substantial capital investment in laboratory infrastructure, precision analytical instruments, and reference materials with ISO/IEC 17025-accredited laboratory setup costs ranging from USD 500,000 to over USD 5 million depending on scope and specialization.

The ongoing costs of maintaining accreditation status including proficiency testing, calibration programs, and assessor fees paid to national accreditation bodies such as UKAS, DAkkS, and A2LA impose recurring overhead that constrains both new market entrants and smaller regional operators from competing with global majors in multi-accreditation, multi-sector service delivery.

Shortage of Qualified Technical Personnel Constrains Capacity Expansion and Service Quality Across TIC Providers

The TIC industry's dependence on highly trained chemists, engineers, auditors, and inspection specialists creates a systemic talent constraint that limits capacity expansion and can impair service quality in rapidly growing geographies. The International Accreditation Forum (IAF) and International Laboratory Accreditation Cooperation (ILAC) have both identified workforce development as a critical sector challenge in their published strategic plans.

In rapidly growing markets including India, Southeast Asia, and the Middle East, the mismatch between TIC demand growth and qualified personnel supply is creating delivery bottlenecks that Favor established global TIC operators with international deployment capabilities over local providers.

Opportunities - Digital Transformation of TIC Services Including AI-Powered Inspection and Blockchain Certification Is Opening a High-Growth Technology-Enabled Service Segment

The digitalization of testing, inspection, and certification processes represents the most transformative near-term opportunity for TIC service providers enabling remote inspection via drones and IoT-connected sensors, AI-driven defect detection in manufacturing quality control, and tamper-proof digital certificates anchored on blockchain platforms.

The International Electrotechnical Commission (IEC) has published technical guidance on digital conformity assessment, and leading TIC operators including SGS, Bureau Veritas, and Intertek have all publicly committed multi-year digital transformation investment programs aimed at automating laboratory workflows and developing cloud-based client compliance management portals. Drone-based infrastructure inspection is projected to reduce inspection costs by 30–40% while improving safety and data quality, per published pilot programs by TÜV Rheinland and DNV.

Asia Pacific's Manufacturing Expansion and Regulatory Alignment Are Creating the Fastest-Growing Regional Demand Base for TIC Services

Asia Pacific is the fastest-growing regional TIC market, propelled by the convergence of manufacturing output growth, progressive regulatory alignment with international standards, and rising domestic consumer expectations for product safety verification. China's State Administration for Market Regulation (SAMR) has significantly expanded mandatory product certification requirements under the China Compulsory Certification (CCC) scheme, encompassing an increasing range of product categories and requiring accredited third-party testing. India's Bureau of Indian Standards (BIS) is progressively implementing mandatory BIS Certification across electronics, chemicals, and food products under the BIS Act 2016, creating substantial new demand for accredited testing and certification services.

Category-wise Analysis

Service Type Insights

Testing leads the service type segment with approximately 45% market share in 2026, a dominance rooted in the universal, non-discretionary nature of analytical testing across virtually every regulated industry sector, from food and pharmaceutical to automotive and electronics and its position as the technical foundation upon which certification and inspection decisions are based.

The ISO/IEC 17025 international standard for laboratory competence is recognized in MLA agreements covering over 150 accreditation bodies globally through ILAC, establishing a technically harmonized framework that allows accredited laboratory testing results to be recognized across borders a structural enabler of international TIC outsourcing demand.

Sourcing Type Insights

Outsourced TIC services lead the sourcing type segment with approximately 62% market share in 2026, reflecting the structural reality that most manufacturers and commercial entities, particularly small and medium enterprises, cannot justify the capital investment, ongoing accreditation costs, and specialist personnel requirements of maintaining comprehensive in-house TIC capabilities across all applicable regulatory domains.

The outsourcing trend is reinforced by third-party independence requirements embedded in many regulatory frameworks: the EU CE Marking system requires involvement of Notified Bodies, independent third-party organizations designated by EU member states for most product categories, legally mandating outsourced certification rather than in-house self-declaration. The WTO TBT Agreement's emphasis on third-party conformity assessment further entrenches the outsourcing model in international trade contexts.

Application Insights

Food application leads the application segment with approximately 20% share in 2026, anchored by the global food industry's non-negotiable requirement for continuous safety testing and certification across production, processing, and import/export stages driven by the Codex Alimentarius international food standards framework, EU Food Law Regulation (EC) 178/2002, U.S. FDA FSMA, and equivalent national food safety legislation in over 100 countries.

Food TIC services encompass microbiological testing, pesticide residue analysis, allergen verification, nutritional labelling compliance, and supply chain auditing each representing a discrete, recurring service revenue stream for TIC providers with accredited food laboratory capabilities. The WHO's estimate that contaminated food causes 420,000 deaths annually globally sustains the political priority of food safety enforcement, creating regulatory tailwinds for TIC demand that are effectively decoupled from broader economic cycles.

Regional Analysis

North America Testing, Inspection, and Certification (TIC) Market Trends & Analysis

North America is a mature and deeply regulated TIC market, anchored by the U.S. FDA, EPA, CPSC, and OSHA regulatory ecosystems that mandate third-party testing and certification across food, pharmaceuticals, consumer products, and environmental monitoring. The U.S. National Institute of Standards and Technology (NIST) coordinates the national measurement infrastructure that underpins accredited laboratory performance. Growing demand from EV testing, cybersecurity certification, and FSMA food safety auditing is the primary growth catalyst, with TIC providers investing heavily in EV battery testing laboratories and digital inspection platforms to serve these fast-emerging segments.

U.S. Testing, Inspection, and Certification (TIC) Market Size

The United States commands approximately 82% of the North American TIC market, anchored by the world's most extensive network of federal regulatory mandates and the density of its manufacturing, food processing, pharmaceutical, and energy sectors. The FDA's expanded FSMA enforcement, EPA environmental testing requirements, and CPSC consumer product certification obligations generate deep, multi-sector TIC demand.

Europe Testing, Inspection, and Certification (TIC) Market Trends, Drivers, & Insights

Europe is the world's most comprehensively regulated TIC market, shaped by the EU CE Marking framework, REACH, RoHS, GDPR, and the expanding EU Green Deal regulatory agenda that is progressively adding sustainability performance testing and supply chain due diligence certification requirements. The European cooperation for Accreditation (EA) and its MLA agreement ensure mutual recognition across EU member state accreditation bodies, facilitating cross-border TIC service delivery. Germany and the UK host the world's densest concentrations of accredited TIC organizations globally, and the region's large industrial and chemical manufacturing base sustains consistent high-value TIC demand.

Germany Testing, Inspection, and Certification (TIC) Market Size

Germany holds approximately 23% of the European TIC market, reflecting its position as the EU's largest economy and manufacturing base home to world-leading automotive, chemical, pharmaceutical, and engineering sectors that are intensive users of accredited testing and certification services. TÜV Rheinland, TÜV SÜD, DEKRA, and DIN CERTCO are globally recognized TIC organizations headquartered in Germany, further anchoring the country's technical leadership and export influence in international TIC service delivery.

U.K. Testing, Inspection, and Certification (TIC) Market Size

The United Kingdom accounts for approximately 15% of the European TIC market. The UK Accreditation Service (UKAS) the sole national accreditation body oversees over 10,000 accredited organizations covering laboratories, inspection bodies, and certification bodies across all regulated sectors. Post-Brexit, the UK's UKCA marking scheme has created parallel certification requirements to EU CE marking for products sold in Great Britain, generating additional third-party conformity assessment demand that benefits UKAS-accredited TIC providers.

France Testing, Inspection, and Certification (TIC) Market Size

France represents approximately 13% of the European TIC market. Bureau Veritas, one of the world's three largest TIC organizations, is headquartered in Paris and contributes significantly to France's strong market position. France's large agri-food sector, advanced nuclear energy industry, and active government infrastructure inspection programs generate diverse, high-value TIC demand across food safety, energy, and civil engineering testing and certification.

Asia Pacific Testing, Inspection, and Certification (TIC) Market Drivers & Analysis

Asia Pacific is the fastest-growing regional TIC market, propelled by manufacturing expansion, progressive regulatory development, and rising quality expectations across China, India, Japan, and Southeast Asia. China is the region's largest and most consequential TIC market, with the State Administration for Market Regulation (SAMR) overseeing the China National Accreditation Service (CNAS) and the mandatory CCC scheme that covers over 100 product categories, generating enormous domestic testing and certification demand that is served by both Chinese state-affiliated TIC organizations and international majors with Chinese laboratory operations.

China Testing, Inspection, and Certification (TIC) Market Size

China holds approximately 38% of the Asia Pacific TIC market, driven by the scale of its manufacturing output as the world's largest goods exporter and the SAMR's expanding CCC mandatory certification coverage. China's rapidly growing EV industry, food safety enforcement priorities under GB standards, and increasing consumer product quality expectations are all generating above-market TIC demand growth.

India Testing, Inspection, and Certification (TIC) Market Size

India holds approximately 14% of the Asia Pacific TIC market and is among the region's fastest-growing country markets. BIS's progressive mandatory certification expansion under the BIS Act 2016 covering electronics, chemicals, food, and construction materials is creating large-scale new demand for accredited testing and certification services. India's ambition to become a USD 5 trillion economy is generating significant infrastructure, pharmaceutical, and export-oriented manufacturing TIC demand.

Japan Testing, Inspection, and Certification (TIC) Market Size

Japan accounts for approximately 16% of the Asia Pacific TIC market. Japan's precision manufacturing industries, automotive, electronics, and industrial equipment generate high-value, technically demanding testing and certification requirements governed by JIS (Japanese Industrial Standards) and PSE (Product Safety Electrical Appliance & Material) regulations. JQA (Japan Quality Assurance Organization) and JICQA are major domestic TIC organizations serving Japan's export-intensive manufacturing base.

Competitive Landscape

The global TIC market is moderately consolidated at the premium international service tier, with SGS SA, Bureau Veritas, and Intertek Group collectively holding an estimated 25–30% of global TIC revenue a share sustained by their multi-sector accreditation portfolios, global laboratory networks spanning over 100 countries, and long-term framework agreements with multinational corporations and government regulatory authorities.

The market rewards both scale, enabling the breadth of accreditations required to serve multinational clients consistently and sector-specific technical depth. Strategic themes among leaders include digital laboratory automation investment, drone and IoT-enabled remote inspection platform development, and targeted acquisitions of specialty TIC firms in high-growth sectors including EV battery testing, cybersecurity certification, and sustainability assurance.

Key Developments:

- In December 2025, UL Solutions, a division of UL LLC, signed a memorandum of understanding with Saudi Electricity Company to advance fire protection and life safety standards in Saudi Arabia. The collaboration focuses on training, testing, and certification to enhance public safety and strengthen fire prevention across the energy sector.

- In April 2025, Nordic Inspekt Group finalized the NOK 41.2 million acquisition of Test partner Gruppen, enhancing Nordic coverage in materials testing and welding certification.

Global Testing, Inspection, and Certification (TIC) Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 210.3 Bn |

|

Current Market Value (2026) |

US$ 275.4 Bn |

|

Projected Market Value (2033) |

US$ 398.0 Bn |

|

CAGR (2026-2033) |

5.4% |

|

Leading Region |

Europe 35% share |

|

Dominant Application |

Food, 22% share |

|

Top-ranking Product |

Testing, 45% |

|

Incremental Opportunity |

US$ 122.5 Bn |

Companies Covered in Testing, Inspection, and Certification (TIC) Market

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- TÜV Rheinland Group

- TÜV SÜD AG

- DNV (Det Norske Veritas)

- DEKRA SE

- Eurofins Scientific SE

- Applus+ Services SA

- Element Materials Technology

- National Technical Systems (NTS)

- ALS Limited

- MISTRAS Group Inc.

- Exova Group

- UFI Filters

Frequently Asked Questions

The market size is set to reach US$ 393 Bn by 2032.

TIC, or testing, inspection and certification, is an independent sector that offers conformity assessment services for regulatory or good practice purposes.

In 2025, North America is set to hold a market share of 17.8%.

In 2025, the market is estimated to be valued at US$ 269.1 Bn.