- Pharmaceuticals

- Systemic Scleroderma Treatment Market

Systemic Scleroderma Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Systemic Scleroderma Treatment Market by Drug Class (Immunosuppressants, Corticosteroids, Endothelin Receptor Antagonists, Others), Route of Administration (Oral, Injectable, Topical), Distribution Channel (Hospital Pharmacies, Others), and Regional Analysis for 2026 - 2033

Systemic Scleroderma Treatment Market Share and Trends Analysis

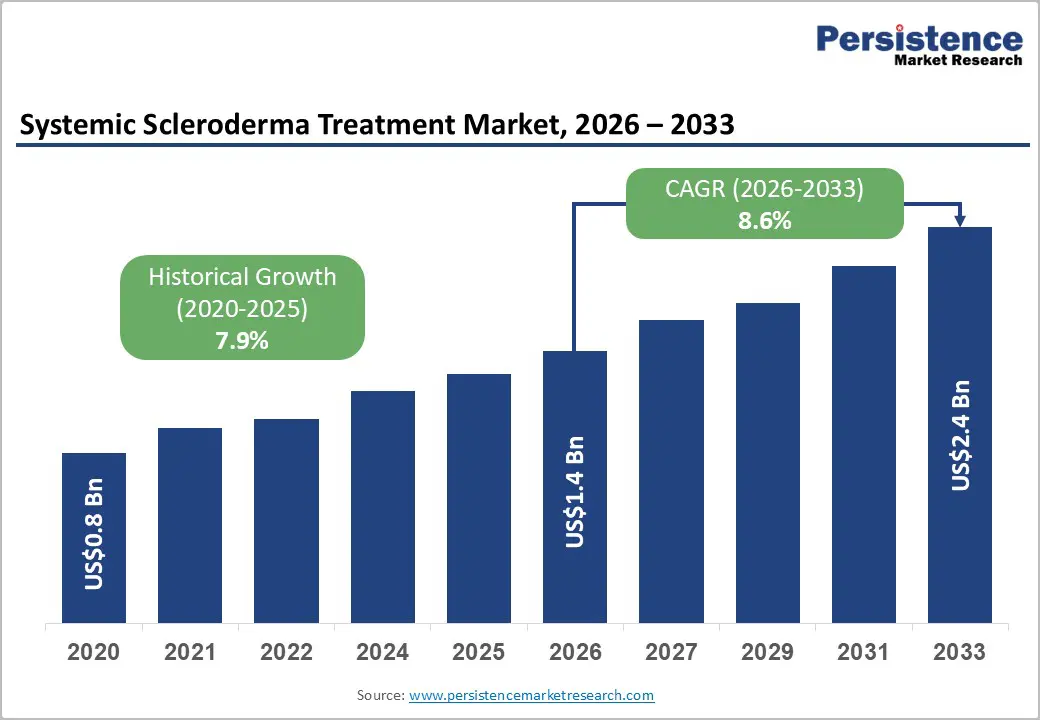

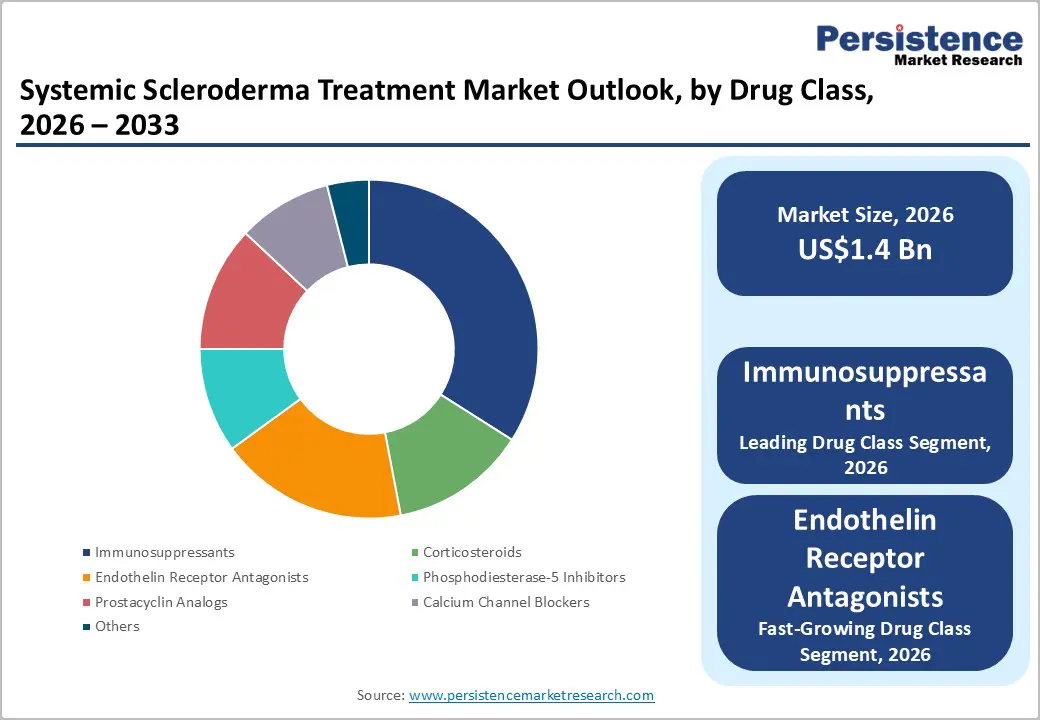

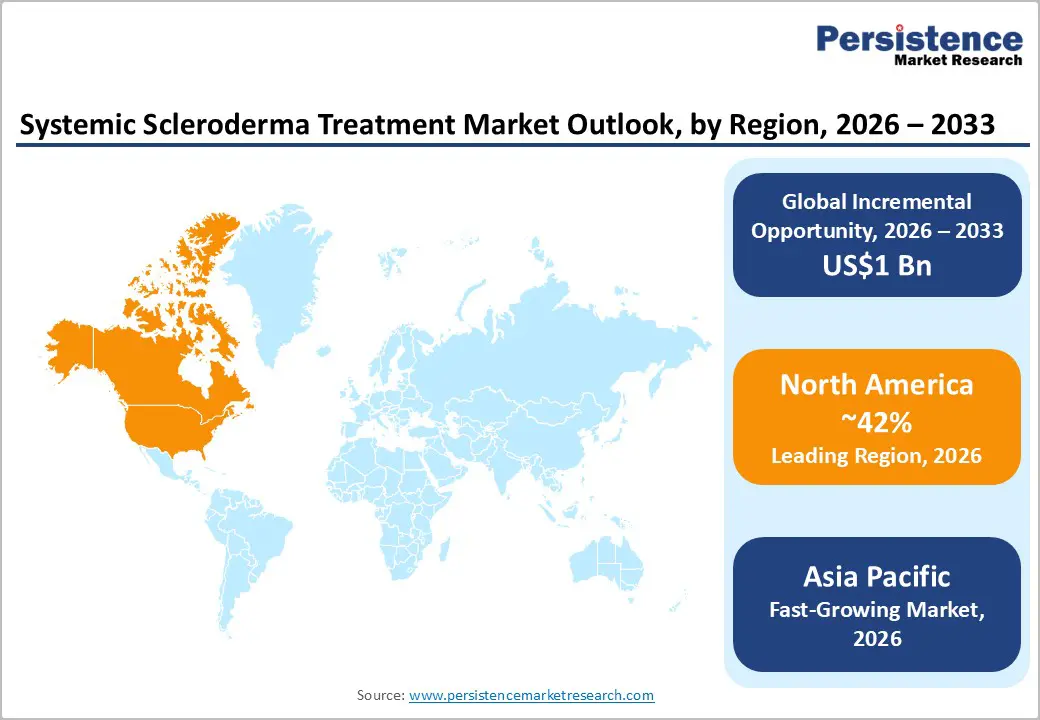

The global systemic scleroderma treatment market size is likely to be valued at US$1.4 billion in 2026 and is estimated to reach US$2.4 billion by 2033, growing at a CAGR of 8.6% during the forecast period 2026 - 2033, driven by expanding autoimmune disease diagnosis rates, increasing biologic therapy adoption, and rising investment in rare disease management infrastructure.

Clinical emphasis on early intervention and organ protection continues to reshape treatment pathways across immunology and rheumatology care settings. Regulatory incentives for orphan diseases are accelerating pipeline activity and commercialization timelines for targeted therapies.

Key Industry Highlights:

- Leading Drug Class: Immunosuppressants are set to hold around 34% revenue share in 2026, driven by broad clinical adoption across diffuse and limited systemic sclerosis subtypes.

- Fastest-Growing Drug Class: Endothelin receptor antagonists are projected to be the fastest-growing segment, supported by rising diagnoses of scleroderma-associated pulmonary arterial hypertension.

- Leading Distribution Channel: Hospital pharmacies are estimated to hold roughly 47% revenue share in 2026, due to strong integration within specialty rheumatology and rare disease clinical care systems.

- Fastest-Growing Distribution Channel: Online pharmacies are forecast to record the fastest growth, driven by rising adoption of digital prescription fulfillment and remote chronic disease management platforms.

- Regional Leadership: North America is projected to capture roughly 42% of the market share in 2026, while Asia Pacific is forecast to record the fastest growth due to rapid healthcare modernization.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Boehringer Ingelheim and Roche leveraging pipeline depth, regulatory relationships, and specialty channel access to maintain competitive positioning.

- Innovation Trends: Advancement of antifibrotic biologics, TGF-beta pathway inhibitors, and digital health integration in scleroderma care are shaping long-term investment priorities across the forecast period.

DRO Analysis

Driver - Regulatory Incentives and Orphan Drug Programs Accelerating Therapeutic Innovation

Regulatory agencies are expanding orphan drug support programs for rare autoimmune diseases, leading pharmaceutical companies toward targeted research investments. Faster regulatory review timelines and exclusivity incentives are encouraging the development of therapies focused on fibrosis reduction, vascular stabilization, and immune pathway modulation. Clinical trial activity is increasing because treatment gaps remain significant for progressive organ complications.

The European Medicines Agency granted orphan designation for multiple systemic sclerosis therapies during 2024 and 2025, including iloprost and avenciguat development programs. Expansion of regulatory support is reducing commercialization risk for biotechnology companies. Investment in biologic platforms, inhaled vasodilators, and fibrosis-modifying therapies is strengthening clinical development pipelines and improving long-term treatment accessibility for severe disease populations.

Restraint - High Therapy Costs and Reimbursement Complexity

The cost burden associated with biologic and targeted systemic therapies remains a structural impediment to broad market penetration. Specialty drug pricing frequently exceeds reimbursement thresholds in lower-income healthcare systems. This compresses addressable volume and limits market scalability.

Complex prior authorization requirements and inconsistent payer coverage policies create unpredictable revenue cycles for manufacturers. Companies absorb patient assistance program costs to maintain formulary access. These dynamics erode net margins, particularly in price-sensitive markets.

Opportunity - Pipeline Expansion in Anti-fibrotic and Biologic Therapies

The treatment pipeline contains a substantial number of anti-fibrotic candidates targeting TGF-beta signaling and interleukin-mediated inflammation. Successful late-phase trial readouts for novel biologics represent a transformative growth pathway, as current standard-of-care options address symptoms rather than underlying disease mechanisms. Current therapies leave a significant disease modification gap that pipeline candidates are positioned to fill.

National Institutes of Health funding and European Commission Horizon programs are catalyzing academic-industry partnerships that accelerate candidate advancement. Companies achieving first-to-market status in mechanistically differentiated categories are positioned to capture premium pricing. Established formulary positions across major health systems will follow for those clearing regulatory milestones.

Category-wise Analysis

Drug Class Insights

Immunosuppressants are anticipated to secure around 34% of the systemic scleroderma treatment market share in 2026, reflecting their foundational role in modulating aberrant immune activation. Methotrexate and mycophenolate mofetil represent widely prescribed agents within this category. Established clinical evidence, broad physician familiarity, and generic availability drive consistent utilization, making this the structurally dominant drug class.

Endothelin receptor antagonists are expected to be the fastest-growing segment, propelled by increasing diagnoses of scleroderma-associated pulmonary arterial hypertension. Bosentan, a first-in-class endothelin receptor antagonist, established the clinical rationale for this category. Growing recognition of vascular manifestations as a primary driver of morbidity is accelerating prescribing in specialist and community rheumatology settings.

Route of Administration Insights

Oral is poised to dominate with a forecast market share of over 58% in 2026, powered by patient preference for self-administered regimens. Oral mycophenolate mofetil, widely used in clinical practice, exemplifies the category strength. Ease of dispensing through retail and hospital pharmacies reinforces oral route dominance across all major treatment geographies.

Injectables are estimated to be the fastest-growing segment, fueled by the expansion of biologic therapies requiring subcutaneous or intravenous administration for optimal bioavailability. Tocilizumab, an injectable IL-6 receptor inhibitor approved for scleroderma-associated interstitial lung disease, illustrates the segment trajectory. Investment in home-infusion services and pre-filled syringe formats is reducing administration barriers and supporting broader adoption.

Distribution Channel Insights

Hospital pharmacies are likely to be the leading segment with a projected 47% of the systemic scleroderma treatment market share in 2026, due to the concentration of specialty drug dispensing within tertiary care centers. Major academic medical centers such as Johns Hopkins Hospital serve as high-volume dispensing hubs for complex biologic regimens. Physician proximity and insurance billing infrastructure embedded within hospital systems reinforce channel dominance.

Online pharmacies are anticipated to be the fastest-growing segment, fueled by the rising adoption of digital prescription fulfillment platforms among chronic disease patients. Specialty online pharmacy operators offering adherence support programs are gaining traction among scleroderma patients managing long-term oral maintenance regimens. Regulatory approvals for digital pharmacy licensing are accelerating channel legitimacy and reimbursement eligibility.

Regional Insights

North America Systemic Scleroderma Treatment Market Trends

North America is expected to lead with an estimated 42% of the systemic scleroderma treatment market share in 2026, supported by a mature rheumatology infrastructure and robust rare disease policy frameworks. The U.S. orphan drug ecosystem continues to attract disproportionate pipeline investment.

U.S. Systemic Scleroderma Treatment Market Insights

The U.S. is projected to account for the majority of North American revenue, driven by the presence of Boehringer Ingelheim and Roche in active scleroderma development programs. Reimbursement coverage under Medicare Part D specialty tiers is expected to broaden as value-based contracting frameworks gain traction.

Canada Systemic Scleroderma Treatment Market Insights

Canada is forecast to demonstrate steady growth, supported by Health Canada's expedited review pathways for rare disease therapies. The Scleroderma Society of Canada has been active in patient registry development, generating real-world evidence datasets expected to support label expansion submissions.

Europe Systemic Scleroderma Treatment Market Trends

Europe represents a major commercial hub driven by expanding government funding for rare autoimmune disease research and standardized clinical management guidelines across regional health systems. Integrated healthcare models facilitate long-term patient monitoring and consistent therapeutic adherence.

Germany Systemic Scleroderma Treatment Market Insights

Germany is expected to dominate continental revenue due to robust industrial pharmaceutical manufacturing infrastructure and rapid integration of novel therapeutics into statutory health insurance catalogs. Corporate research hubs operated by Boehringer Ingelheim advance local anti-fibrotic drug development.

U.K. Systemic Scleroderma Treatment Market Insights

The U.K. market is likely to experience significant gains because of centralized National Health Service procurement strategies and structured clinical trials conducted via the National Institute for Health and Care Research. Streamlined regulatory evaluation pathways under updated domestic frameworks accelerate patient access to advanced monoclonal antibodies.

Asia Pacific Systemic Scleroderma Treatment Market Trends

Asia Pacific is forecast to be the fastest-growing market for systemic scleroderma treatment, stimulated by rapid healthcare infrastructure modernization, rising medical awareness, and expanding public reimbursement insurance frameworks. Growing economic development allows regional populations to access premium global therapeutic choices. Local regulatory agencies accelerate approval timelines for internationally validated orphan drugs to address significant unmet medical needs.

Japan Systemic Scleroderma Treatment Market Insights

Japan is expected to lead regional market expansion, due to an aging demographic profile and favorable pricing designations for innovative orphan therapies from the Ministry of Health, Labour and Welfare. Domestic entities, including Chugai Pharmaceutical and Kyowa Kirin, actively expand specialized autoimmune portfolios. High-density urban clinical networks facilitate rapid commercial distribution of newly approved injectable treatments.

China Systemic Scleroderma Treatment Market Insights

The China market is anticipated to record rapid growth driven by proactive government initiatives to expand the National Reimbursement Drug List inclusions and rising diagnostic rates across tier-one cities. Strategic manufacturing collaborations between international biotechnology organizations and domestic producers lower local distribution costs.

Competitive Landscape

The global systemic scleroderma treatment market is moderately fragmented, with innovation-driven companies competing across disease manifestation-specific segments. Key participants include Boehringer Ingelheim, Roche, Actelion Pharmaceuticals (Johnson & Johnson), United Therapeutics, and Gilead Sciences, each maintaining differentiated positions across pulmonary, fibrotic, and vascular treatment categories.

Competitive differentiation is achieved through pipeline depth, label breadth, and established payer relationships. Biosimilar entry into the immunosuppressant segment is introducing cost-based competition at the commodity tier. Branded innovators are concentrating investments in first-in-class biologics that command sustained pricing power and reimbursement preference.

Key Industry Developments:

- In October 2025, Island Rheumatology and Osteoporosis highlighted advancements in antifibrotic therapies, biologics, and stem cell transplantation for systemic sclerosis, reinforcing momentum toward personalized and multidisciplinary treatment strategies for systemic scleroderma patients.

- In March 2025, Vanderbilt University Medical Center received renewed designation from the National Scleroderma Foundation for its systemic sclerosis research and treatment program, reinforcing advancement in multidisciplinary care and personalized treatment development for Systemic Scleroderma patients.

Companies Covered in Systemic Scleroderma Treatment Market

- Boehringer Ingelheim International GmbH

- F. Hoffmann-La Roche Ltd

- Actelion Pharmaceuticals Ltd (Johnson & Johnson)

- United Therapeutics Corporation

- Gilead Sciences Inc.

- Bristol-Myers Squibb Company

- Pfizer Inc.

- AbbVie Inc.

- GlaxoSmithKline plc

- Sanofi S.A.

- Corbus Pharmaceuticals Holdings Inc.

- ChemoCentryx Inc. (Amgen)

- Bayer AG

- Merck KGaA

- Arena Pharmaceuticals (Pfizer)

Frequently Asked Questions

The global systemic scleroderma treatment market is projected to reach US$1.4 billion in 2026.

The rising prevalence of autoimmune disorders and increasing adoption of targeted biologics and antifibrotic therapies are driving the systemic scleroderma treatment market.

The systemic scleroderma treatment market is poised to witness a CAGR of 8.6% from 2026 to 2033.

Expansion of precision medicine, biologic therapy development, and digital autoimmune care infrastructure is creating key growth opportunities in the systemic scleroderma treatment market.

Some of the key market players include Boehringer Ingelheim, Roche, Actelion Pharmaceuticals (Johnson & Johnson), United Therapeutics, and Gilead Sciences.