- Biotechnology

- Stromal Vascular Fraction Market

Stromal Vascular Fraction Market Size, Share, and Growth Forecast, 2026 - 2033

Stromal Vascular Fraction Market by Product Type (SVF Aspiration Products, SVF Transfer Products, Others), Application (Cosmetic & Aesthetic Treatments, Orthopedic, Wound Healing, Others), and Regional Analysis for 2026 - 2033

Stromal Vascular Fraction Market Size and Trends Analysis

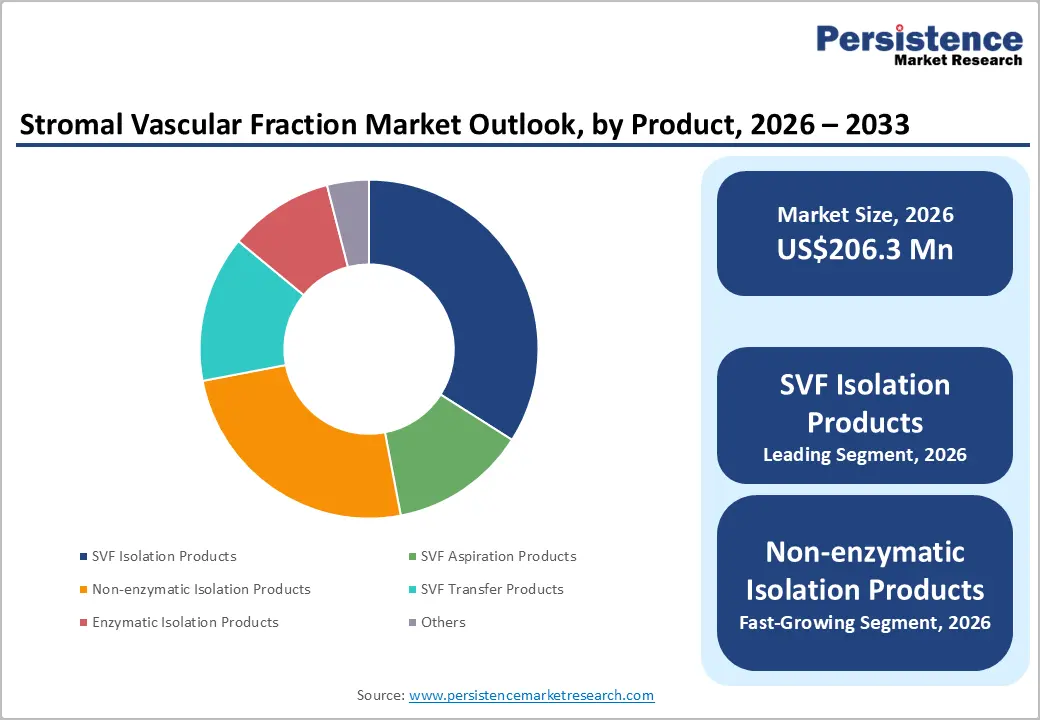

The global stromal vascular fraction market size is likely to be valued at US$206.3 million in 2026 and is expected to reach US$306.1 million by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by the expanding adoption of regenerative medicine, stem cell therapies, and minimally invasive autologous procedures in orthopedics, wound healing, and aesthetic medicine. SVF, derived from adipose tissue, contains adipose-derived stem cells, endothelial cells, and immune-regulating cells that support tissue repair, angiogenesis, and anti-inflammatory responses.

In 2025, the National Institutes of Health (NIH) highlighted increasing clinical interest in adipose-derived regenerative therapies for chronic wounds and ulcer management. They also estimate that chronic wounds affect nearly 10.5 million Medicare beneficiaries in the U.S., increasing demand for advanced regenerative treatments and cell-based therapies.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 46% in 2026, driven by strong U.S. leadership in regenerative medicine research, advanced biotechnology infrastructure, and increasing adoption of autologous cell-based therapies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding regenerative medicine infrastructure, rising medical tourism, and increasing adoption of stem cell-based therapies.

- Leading Product Type: SVF isolation products are projected to represent the leading product type in 2026, accounting for 48% of the revenue share, due to the increasing demand for efficient and standardized cell separation technologies.

- Leading Application: The orthopedic segment is anticipated to be the leading application type, accounting for over 39% of the revenue share in 2026, supported by growing adoption in osteoarthritis and musculoskeletal regenerative treatments.

- Key Opportunity: The key market opportunity in the stromal vascular fraction market lies in the growing integration of automated and non-enzymatic SVF processing technologies with personalized regenerative medicine for minimally invasive orthopedic, wound healing, and aesthetic therapies.

DRO Analysis

Driver - Rising Demand for Regenerative and Minimally Invasive Therapies in Orthopedics and Wound Healing

SVF contains adipose-derived stem cells, endothelial cells, and growth factors that support tissue repair, anti-inflammatory responses, and angiogenesis. The increasing prevalence of osteoarthritis, sports injuries, diabetic ulcers, and chronic wounds is accelerating clinical adoption of SVF-based procedures.

Patients and healthcare providers increasingly prefer minimally invasive autologous therapies that reduce hospitalization and recovery time compared to conventional surgeries. Technological improvements in isolation systems and point-of-care processing devices are also supporting treatment efficiency, reproducibility, and broader use across regenerative medicine clinics and hospitals.

Growing elderly populations worldwide are increasing demand for orthopedic regenerative procedures and advanced wound management solutions. According to NIH estimates, chronic wounds continue to affect millions of patients globally, creating a strong demand for cell-based regenerative therapies. SVF-based treatments are increasingly used for cartilage repair, tendon injuries, diabetic foot ulcers, and tissue regeneration because of their ability to promote natural healing.

Restraint - Regulatory Hurdles and Lack of Harmonized Guidelines

Regulatory agencies often classify enzymatically processed SVF as more than minimally manipulated, leading to stricter approval pathways and compliance requirements. Variations in regulatory frameworks across the U.S., Europe, and Asia Pacific create uncertainty for manufacturers and healthcare providers. Clinical translation becomes difficult because companies must meet varying safety, efficacy, and manufacturing standards across regions.

Limited long-term clinical evidence and concerns regarding standardization also affect physician confidence and market adoption of SVF-based therapies. Regulatory authorities continue emphasizing validated clinical data, reproducible processing methods, and controlled therapeutic outcomes before broader approvals can be granted. Smaller biotechnology companies often face financial and operational difficulties in conducting extensive clinical trials and maintaining regulatory compliance.

Opportunity - Technological Convergence with Automated Systems and Personalized Medicine

Automated isolation platforms improve cell extraction efficiency, sterility, reproducibility, and processing speed, making SVF therapies more suitable for clinical and hospital environments. Advances in closed-loop systems and point-of-care technologies reduce contamination risks while supporting standardized therapeutic outcomes. The increasing adoption of personalized medicine is also driving demand for autologous SVF therapies tailored to individual patients' conditions.

These technologies enable healthcare providers to develop targeted regenerative treatments for orthopedic disorders, chronic wounds, and aesthetic procedures while improving patient safety, convenience, and overall treatment effectiveness across the healthcare system. Growing investments in biotechnology innovation and regenerative medicine infrastructure are accelerating commercialization opportunities for advanced SVF technologies.

Companies are increasingly focusing on artificial intelligence-assisted cell processing, automated manufacturing platforms, and integrated regenerative treatment solutions to improve scalability and regulatory compliance. Personalized cell-based therapies are gaining traction because they reduce the risks of immune rejection and support patient-specific healing responses. Expanding partnerships between biotechnology firms, research institutes, and healthcare providers are strengthening clinical validation and technology development.

Category-wise Analysis

Product Type Insights

SVF isolation products are expected to lead, accounting for 48% of revenue in 2026. Its critical role in regenerative medicine workflows and adipose-derived stem cell processing. These products are widely used across hospitals, specialty clinics, and research laboratories for efficient extraction and purification of stromal vascular fraction cells. A notable example is Thermo Fisher Scientific Inc., which offers advanced cell isolation technologies and laboratory solutions that support regenerative medicine and stem cell research applications.

Non-enzymatic isolation products are likely to represent the fastest-growing segment, supported by increasing preference for minimally manipulated cell processing techniques and improved regulatory acceptance. Mechanical isolation methods are gaining traction because they avoid enzymatic digestion processes while supporting safer and faster clinical applications. For instance, GID Group Inc. is recognized for developing automated adipose tissue processing and regenerative cell therapy technologies for clinical and surgical applications.

Application Insights

The orthopedic segment is projected to lead the market, capturing around 39% of the revenue share in 2026, supported by the rising prevalence of osteoarthritis, sports injuries, and degenerative musculoskeletal disorders worldwide. SVF therapies are increasingly utilized in orthopedic regenerative medicine because adipose-derived stem cells and growth factors support cartilage repair, tissue regeneration, and anti-inflammatory responses. For example, Cytori Therapeutics Inc. has developed regenerative cell therapy technologies focused on orthopedic and soft-tissue repair applications in the regenerative medicine industry.

Cosmetic & aesthetic treatments are likely to be the fastest-growing application, due to increasing demand for minimally invasive regenerative aesthetic procedures. SVF-based therapies are widely used in fat grafting, facial rejuvenation, skin regeneration, scar treatment, and hair restoration procedures for their regenerative and anti-aging properties. A notable example is Kerastem Technologies LLC, which focuses on regenerative hair restoration solutions using adipose-derived cell-based technologies for aesthetic applications.

Regional Insights

North America Stromal Vascular Fraction Market Trends

North America is anticipated to be the leading region, accounting for 46% in 2026, supported by advanced regenerative medicine infrastructure, strong biotechnology investments, and rising adoption of minimally invasive cell-based therapies. The increasing prevalence of osteoarthritis, chronic wounds, and sports injuries continues to support demand for adipose-derived regenerative treatments across the region. For instance, Lonza Group AG supports North American regenerative medicine companies through advanced cell therapy manufacturing solutions.

U.S. Stromal Vascular Fraction Market Trends

The U.S. dominates the regional market, driven by strong regenerative medicine research and high healthcare expenditure. The increasing prevalence of musculoskeletal disorders and chronic wounds is driving demand for adipose-derived regenerative therapies. Hospitals and orthopedic clinics are increasingly adopting minimally invasive SVF procedures for joint repair and tissue regeneration. Recent developments in automated cell isolation technologies are improving treatment reproducibility and safety standards.

Canada Stromal Vascular Fraction Market Trends

Canada is a significant market for stromal vascular fraction, supported by expanding biotechnology research and supportive healthcare innovation programs. The increasing aging population and rising incidence of orthopedic disorders are contributing to higher demand for minimally invasive regenerative treatments. Canadian healthcare institutions are focusing on stem cell research and advanced biologic therapies for tissue repair applications. Recent investments in cell therapy infrastructure and laboratory automation are supporting clinical adoption of SVF technologies.

Europe Stromal Vascular Fraction Market Trends

Europe is likely to be a significant market for stromal vascular fraction in 2026, driven by strong regenerative medicine research, rising healthcare investments, and growing demand for biologic orthopedic treatments. The region is witnessing rising adoption of adipose-derived stem cell therapies in wound healing, tissue engineering, and aesthetic medicine. For example, Human Med AG, which develops regenerative medical technologies and adipose tissue processing systems used in autologous cell therapy applications across Europe.

U.K. Stromal Vascular Fraction Market Trends

The U.K. is a significant market for stromal vascular fraction, supported by rising interest in personalized medicine and regenerative healthcare technologies. Orthopedic clinics and aesthetic treatment centers are increasingly using adipose-derived regenerative procedures for tissue repair and cosmetic enhancement. Recent healthcare innovation initiatives are supporting clinical research in stem cell therapies and advanced biologic treatments.

Germany Stromal Vascular Fraction Market Trends

Germany dominates the regional market due to its strong biotechnology infrastructure and advanced regenerative medicine research activities. The country has a growing aging population, increasing demand for orthopedic regenerative treatments, and chronic wound management solutions. German hospitals and specialty clinics are increasingly adopting autologous cell-based therapies for musculoskeletal and aesthetic applications.

Asia Pacific Stromal Vascular Fraction Market Trends

The Asia Pacific region is expected to emerge as the fastest-growing market for stromal vascular fraction in 2026, driven by expanding healthcare infrastructure, rising medical tourism, and increasing investments in regenerative medicine technologies. Growing demand for minimally invasive orthopedic, wound healing, and cosmetic procedures utilizing adipose-derived stem cell therapies is further supporting regional market growth. For instance, Stempeutics Research Pvt. Ltd. is actively developing stem cell-based regenerative therapies and advanced cell processing technologies for a range of therapeutic applications.

China Stromal Vascular Fraction Market Trends

China dominates the regional market, supported by strong government support for biotechnology and regenerative medicine innovation. The increasing prevalence of orthopedic disorders, diabetes, and chronic wounds is driving demand for advanced regenerative therapies. Hospitals and research institutes are expanding clinical studies involving adipose-derived stem cells and tissue regeneration technologies. Recent investments in biotechnology parks and cell therapy manufacturing facilities are strengthening the country’s regenerative healthcare ecosystem.

India Stromal Vascular Fraction Market Trends

India represents a significant market for stromal vascular fraction, driven by growing awareness of regenerative medicine and rising medical tourism activities. Orthopedic clinics and aesthetic centers across the country are increasingly adopting adipose-derived regenerative procedures for joint disorders, wound healing, and cosmetic applications. In addition, the increasing prevalence of diabetes and chronic wounds is fueling demand for advanced biologic treatment solutions.

Competitive Landscape

The global stromal vascular fraction market exhibits a moderately fragmented structure, driven by increasing investments in regenerative medicine, adipose-derived stem cell therapies, and automated cell processing technologies. Growing clinical adoption across orthopedics, wound healing, and aesthetic medicine is intensifying competition among biotechnology firms, medical device manufacturers, and regenerative therapy developers.

With key leaders, including GE HealthCare, Thermo Fisher Scientific Inc., Lonza Group AG, GID Group, Inc., and Stempeutics Research Pvt. Ltd., the competitive landscape is characterized by strong emphasis on product innovation, clinical research, and expansion strategies. These players compete through automated SVF isolation technologies, advanced regenerative medicine platforms, strategic partnerships, and investment in clinical trials targeting orthopedic, cardiovascular, and aesthetic applications.

Key Industry Developments:

- In February 2026, Mesoblast Limited reported strong commercial progress for its FDA-approved mesenchymal stromal cell product RYONCIL®, highlighting expanding adoption of regenerative cell therapies and increasing clinical momentum in the stromal vascular fraction market.

Companies Covered in Stromal Vascular Fraction Market

- Cytori Therapeutics, Inc.

- GE HealthCare

- Thermo Fisher Scientific Inc.

- Lonza Group AG

- Stempeutics Research Pvt. Ltd.

- Intelligent Cell Processing Ltd.

- Human Med AG

- Medikan International Inc.

- GID Group, Inc.

- Kerastem Technologies LLC

Frequently Asked Questions

The stromal vascular fraction market is projected to reach US$206.3 million in 2026.

The stromal vascular fraction market is driven by rising demand for regenerative and minimally invasive therapies in orthopedics, wound healing, and aesthetic medicine, along with growing adoption of adipose-derived stem cell technologies.

The stromal vascular fraction market is expected to grow at a CAGR of 5.8% from 2026 to 2033.

Key market opportunities in the stromal vascular fraction market include expanding adoption of automated SVF isolation systems, growing personalized regenerative medicine applications, and increasing use of adipose-derived cell therapies in orthopedics, wound healing, and aesthetic treatments.

Cytori Therapeutics, Inc., GE HealthCare, Thermo Fisher Scientific Inc., and Lonza Group AG are the leading players.