Industry: Healthcare

Published Date: February-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 221

Report ID: PMRREP22912

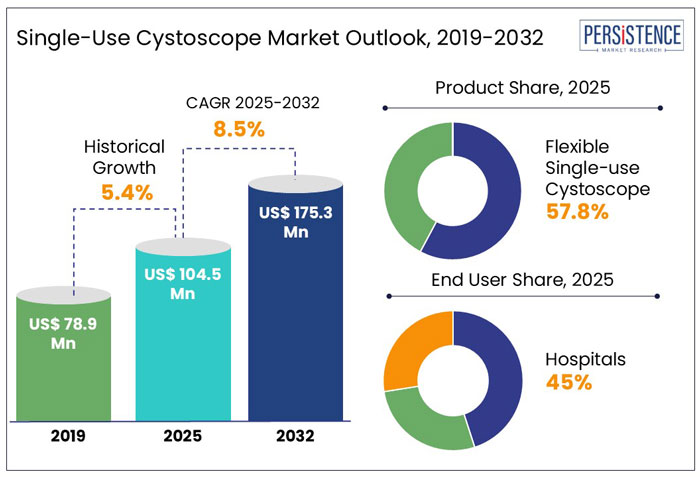

The global single-use cystoscope market size is projected to rise from US$ 104.5 Mn in 2025 to 175.3 Mn in 2032. The market is anticipated to exhibit a considerable CAGR of 8.5% during the forecast period from 2025 to 2032.

|

Market Size (2025) |

US$ 104.5 Million |

|

Projected Market Value (2032) |

US$ 175.3 Million |

|

Global Market Growth Rate (2025 – 2032) |

8.5% CAGR |

|

Market Share of Top 5 Countries (2024) |

58.1% |

According to Persistence Market Research, the single-use cystoscope market is experiencing significant growth, driven by increasing demand for minimally invasive procedures, rising prevalence of urological disorders, and advancements in medical technology. Unlike reusable cystoscopes, single-use cystoscopes eliminate the need for sterilization, reduce cross-contamination risks, and offer cost-effectiveness in certain healthcare settings.

The single-use cystoscope market has grown steadily in recent years, owing to a greater emphasis on infection control, developments in disposable medical devices, and the rising prevalence of urological illnesses. Historically, the market was quite small, with reusable cystoscopes dominating the business because to their long-term cost savings. However, worries about hospital-acquired infections (HAIs) and the high costs of sterilisation and maintenance have resulted in a trend towards disposable options. Over the last decade, single-use cystoscopes have gained popularity, particularly in outpatient settings and smaller healthcare facilities with limited sterilisation infrastructure.

The market is likely to grow further, owing to technical advancements in visualisation, material durability, and cost efficiency. The expanding use of minimally invasive diagnostic methods, together with the rising incidence of bladder cancer and urinary tract infections, will drive up demand. Furthermore, governmental support for infection control and a preference for single-use medical tools in some locations are projected to promote market growth. Despite obstacles such as cost concerns and competition from reusable alternatives, the estimate predicts a strong expansion of the single-use cystoscope market, particularly in industrialized healthcare systems and emerging economies investing in sophisticated medical infrastructure.

The rising prevalence of urinary tract conditions such as bladder cancer, urinary strictures, and recurrent urinary tract infections (UTIs) is driving the demand for cystoscopic procedures. Single-use cystoscopes are gaining traction due to their ability to provide high-definition visualization, improved maneuverability, and enhanced diagnostic accuracy without the risk of cross-contamination. As hospitals and urology clinics focus on early disease detection, single-use cystoscopes offer an efficient alternative to reusable counterparts, eliminating the need for complex reprocessing while ensuring sterility.

A recent example highlighting this trend is the increasing adoption of single-use cystoscopes in the U.S. and Europe following the rise in hospital-acquired infections (HAIs).

Additionally, the increasing geriatric population, which is more susceptible to urological disorders, is further fueling market growth. With advancements in optics and minimally invasive technology, single-use cystoscopes are becoming a preferred choice, widening the scope for early and precise urinary tract diagnostics.

“High Per-Procedure Cost Compared to Reusable Cystoscopes”

While single-use cystoscopes eliminate the expenses associated with sterilization, reprocessing, and potential cross-contamination, their higher per-unit cost poses a significant financial challenge for healthcare providers. Hospitals and urology clinics performing a high volume of cystoscopic procedures may find the recurring expenditure on disposable cystoscopes unsustainable compared to reusable models, which, despite requiring cleaning and maintenance, offer long-term cost-effectiveness. In cost-sensitive markets such as India and parts of Latin America, budget constraints in public healthcare systems further restrict the widespread adoption of single-use cystoscopes.

A recent example highlighting this issue is the financial debate surrounding the adoption of disposable cystoscopes in U.S. hospitals in 2023. A study published in Urology Practice analyzed cost differentials and found that single-use cystoscopes, although beneficial in reducing infection risks, increased procedural costs by up to 50% compared to reprocessed reusable alternatives over an annual cycle. The study emphasized that while hospitals with lower procedural volumes could benefit from disposables due to reduced sterilization infrastructure needs, high-volume centers faced significant financial strain. Consequently, many healthcare systems are evaluating hybrid models—reserving single-use cystoscopes for high-risk patients while maintaining reusable devices for standard procedures—to balance cost and infection control priorities.

Why is the U.S. Market Booming?

“Increased Cystoscope Use in Finding Out Curable Causes of Recurrent UTIs”

Recurrent urinary tract infections (UTIs) affect millions of individuals globally, particularly women and older adults, leading to repeated antibiotic treatments and potential complications such as kidney infections. Identifying and addressing curable causes—such as bladder stones, strictures, or tumors—requires detailed visualization of the urinary tract, making cystoscopy a critical diagnostic tool. Traditional reusable cystoscopes, however, pose infection risks due to inadequate reprocessing, leading to an increased shift towards single-use cystoscopes that offer sterility and reduced contamination concerns.

Clinical studies have also highlighted that disposable cystoscopes improve workflow efficiency, allowing for quicker turnaround times in busy urology departments. Additionally, with rising antimicrobial resistance concerns, physicians are emphasizing precise diagnostics over empirical antibiotic use, further boosting demand for single-use cystoscopes. As awareness of curable causes of recurrent UTIs grows, the market for single-use cystoscopes is expected to expand, particularly in regions prioritizing infection control and patient safety in outpatient urology procedures.

Will the U.K. Be a Lucrative Market for Single-use Cystoscope Market?

“High Bladder Cancer Rate and Its High-Cost Need Cystoscope for Cancer Early Detection”

The U.K. market held about 5.6% of the global market share in 2024, and it is anticipated to expand due to the use of cystoscopes for early detection of bladder cancer.

In the U.K., bladder cancer treatment is expensive; hence, it is anticipated to expand the global market of single-use cystoscopes for early cancer detection.

Which Type of Product is Driving Demand Within the Global Market?

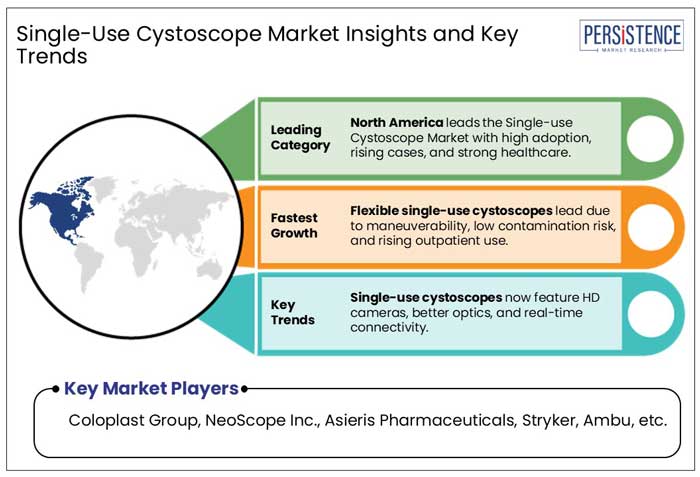

“More Clinical Utilization of Flexible Video Single-Use Cystoscope Over Other Single-Use Cystoscope”

Flexible video single-use cystoscopes allow urologists and physicians to see the urethra and bladder more clearly due to camera lenses and lower irrigation fluid flow in flexible cystoscopies. Flexible cystoscopy can be performed while the patient is awake. Thus, flexible cystoscopes are patient-friendly, less invasive and easy to use, propelling the flexible single-use cystoscope sector forward.

Which End User is Helping to Expand the Global Market?

“Various Cystoscopy Procedures Need to be done in the Hospitals by Skilled Health Workers”

Cystoscopy is primarily performed in hospitals because trained medical professionals or doctors can remove foreign bodies like bladder stones from the bladder using the proper surgical techniques.

Other reasons for the use of cystoscopes in hospitals by expertise are to detect bladder cancer, cystitis, and benign prostatic hyperplasia as well as to look into the causes of bladder signs and symptoms, like hematuria, frequent UTIs, incontinence, and dysuria. In order to identify bladder cancer, this method can be used to acquire a biopsy or tissue sample from the bladder lining. Catheter insertion can also be done by cystoscopy (thin drainage tube of urine).

Another reason for expanding hospital end users is the healthcare reimbursement facilities in various countries.

For instance, Medicare has approved the reimbursement policies in the U.S., which allows the payment of US$ 170.28 at the national level for separate procedure of flexible cystoscope with CPT code 52000

The key players are concentrating on launching new devices, developing devices that improve efficiency. The key players are primarily focused on new product line innovation and product expansion with partnership of domestic companies for commercialising high quality, cost-effective, disposable endoscopic products.

A few examples of strategies acquired by the key players:

Similarly, the team at Persistence Market Research has tracked recent developments related to companies in the single-use cystoscope market, which are available in the full report.

|

Attribute |

Details |

|

Forecast Period |

2025 – 2032 |

|

Historical Data Available for |

2019 – 2024 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Key Countries Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Covered |

|

| Report Highlights |

|

|

Customization & Pricing |

Available upon Request |

Product

End User

Region

To know more about delivery timeline for this report Contact Sales

The global market is expected to reach US$ 104.5 million in 2025.

The global market is set to reach valuation of around US$ 175.3 Million by the end of 2032

Coloplast Group, NeoScope Inc., Asieris Pharmaceuticals, Stryker, Ambu, Olympus Medical Corporation, PENTAX Medical, Richard Wolf GmBH, Cogentix Medical, Karl Storz, Henke-Sass Wolf, Advanced Health Care Resources, and UroViu Corporation are the key players of the global market.

The U.S., Germany, China, U.K., and Japan are the top countries driving the global market with revenue share of around 58.1% in 2022.

The U.S. accounts for around 33.7% share of the global market in 2024.

The Indian market held a share of about 4.4% in the global market in 2024.