Industry: Industrial Automation

Published Date: September-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 177

Report ID: PMRREP34776

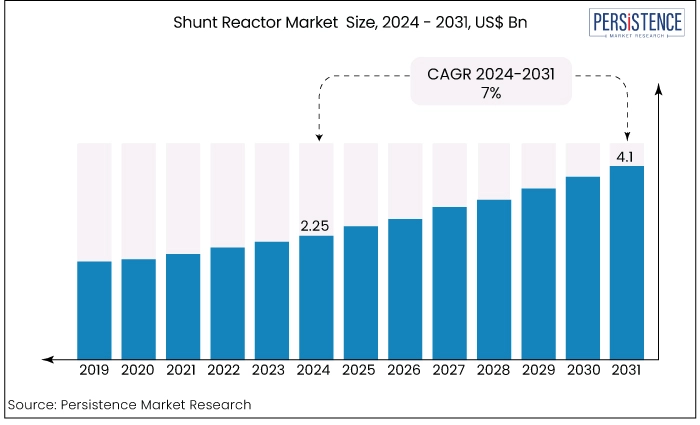

The shunt reactor market is estimated to increase from US$2.25 Bn in 2024 to US$4.1 Bn by 2031. The market is projected to record a CAGR of 7% during the forecast period from 2024 to 2031. The renewable energy systems integration into shunt reactors and the increased electricity demand in leading economies are the primary factors for market growth. Asia Pacific is estimated to dominate the market owing to the increased industrialization in the region.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Shunt Reactor Market Size (2024E) |

US$2.25 Bn |

|

Projected Market Value (2031F) |

US$4.1 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

7% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

6.4% |

|

Region |

Market Share in 2024 |

|

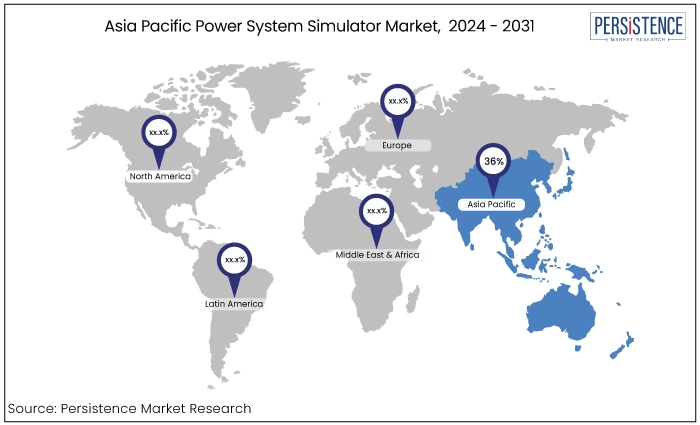

Asia Pacific |

36% |

Asia Pacific holds substantial share of the shunt reactor market primarily because of the fast-paced industrialization and urbanization in countries such as China and India. The market growth is primarily driven by the region's increasing power generation capacities and investments in smart grid technologies.

The implementation of government programs that support the development of sustainable energy infrastructure and the upgrading of power grids is hastening the acceptance of shunt reactors in the area. This region is the leading producer and consumer of energy, which boasts the highest capacity for generating electricity from renewable sources.

The region also encompasses a substantial manufacturing sector. Numerous global and regional manufacturers operate throughout Asia Pacific. The rising demand for reactors in the region can be attributed mostly to the increase in electricity generation and investment in renewable energy.

|

Category |

Market Share in 2024 |

|

Type - Oil-Immersed Insulator |

60% |

Based on type, the shunt reactor market is segmented into oil-immersed insulator and air-core insulator. Among these, the oil-immersed shunt reactors dominate the market. Oil-immersed shunt reactors are the most dominant product type. They employ mineral oil as a medium that will both cool and insulate the engine.

The oil-immersed shunt reactors have high heat dissipation and insulating capabilities, which are important for continuous and reliable operation under a variety of load circumstances. Its sturdy construction guarantees long-term performance and requires just a small amount of maintenance. Hence, they are recommended for use in applications that involve large-scale power grids.

|

Category |

Market Share in 2024 |

|

Application - Variable Shunt Reactor |

58% |

Based on application, the shunt reactor market is divided into variable shunt reactor and fixed shunt reactor. Among these, the variable shunt reactor segment dominates the market. Variable shunt reactors are the dominant segment in the market because they offer flexibility in altering reactive power compensation based on dynamic grid conditions and changing loads.

Variable shunt reactors are equipped with changeable tapping points or electronically controlled switching mechanisms that accurately manage voltage levels in response to changing demand or disruptions in the power grid. Their capacity to actively control reactive power offers the highest level of stability and efficiency in power grids especially in networks.

The shunt reactor market refers to the specific sector within the electrical equipment industry that focuses on producing, selling, and utilizing shunt reactors. Shunt reactors are not just components but the backbone of high-voltage power networks.

Primary function of these reactors is to counterbalance the capacitive reactive power generated by long transmission lines, cables, and other high-voltage equipment. Consequently, ensuring the stability of the entire network. These reactors aim to mitigate and assimilate excess reactive power, enhancing the stability and efficiency of the electrical grid.

One of the defining aspects of the shunt reactor market is its vital role in regulating voltage levels in power networks. Shunt reactors contribute to the maintenance of system stability, and the provision of a consistent electrical supply through the regulation of voltage fluctuations.

They are not just crucial but indispensable in optimizing the effectiveness of transmission and distribution networks particularly in regions with significant power infrastructure or a dense presence of renewable energy sources.

Various factors, including grid technology advancements, infrastructure development investments, and the expansion of renewable energy capacities influence the market for shunt reactors.

The market for shunt reactors is increasing because of the continuous investments made by utilities and grid operators to upgrade their infrastructure. This focus on enhancing grid efficiency and reliability is the main driving force behind the increased demand. Also, integrating renewable energy sources like wind and solar power necessitates the installation of shunt reactors to regulate voltage fluctuations caused by intermittent generation.

The shunt reactor market experienced steady growth up to 2023 driven by the increasing need for voltage regulation and reactive power compensation in electrical grids. The growth was primarily fueled by the expansion of transmission and distribution (T&D) networks, particularly in developing regions.

The integration of renewable energy sources like wind and solar power, which require enhanced grid stability further bolstered the demand for shunt reactors.

Post-2024, the shunt reactor market is expected to accelerate with a projected CAGR of around 7% through 2031. Several factors drive this uptick including the ongoing modernization of aging power infrastructure in developed economies and the increasing focus on grid reliability and efficiency.

The growing adoption of smart grids and the continued integration of renewable energy sources will further propel market demand. Additionally, government initiatives aimed at reducing carbon emissions and improving energy efficiency are expected to support the growth of the market the post-2024 period.

Modernization of Aging Power Infrastructure

The need to modernize and upgrade aging power infrastructure is another key driver of the shunt reactor market. Many developed countries including North America and Europe have aging transmission and distribution networks that are increasingly vulnerable to outages and inefficiencies.

Shunt reactors are essential for improving the reliability and efficiency of these older systems by providing voltage control and reducing losses in long transmission lines. As governments and utilities invest in upgrading and expanding their power infrastructure to meet the growing electricity demand, the adoption of shunt reactors is expected to rise. This trend is further supported by the push toward smart grid technologies, which require enhanced grid management and stability?.

Rising Electricity Demand in Developing Regions

In developing regions particularly in Asia-Pacific, Latin America, and Africa, rapid urbanization and industrialization are driving a significant increase in electricity demand. To support this growing demand, countries in these regions are expanding their transmission and distribution networks, which in turn is increasing the need for shunt reactors.

Reactors help maintain voltage levels and ensure stable power supply across long transmission distances, which is particularly important in vast and geographically diverse countries. As these regions continue to invest in renewable energy projects and grid infrastructure, the demand for shunt reactors is expected to grow further making this a critical driver for the market's expansion. ?

High Initial Investment Costs

One of the primary restraints on the Shunt Reactor market is the high initial investment cost associated with their deployment. Shunt reactors, especially high-voltage units used in large transmission networks, require significant capital outlay for installation. This includes not only the cost of the reactor itself but also expenses related to infrastructure modifications, transportation, and skilled labor.

High upfront costs can be a significant barrier to adoption for utilities and energy companies operating on tight budgets or in regions with limited financial resources. The financial strain of upgrading or expanding existing power grids can slow down the rate at which new shunt reactors are deployed particularly in developing countries where financial resources may be more constrained?.

Availability of Alternative Technologies

The availability of alternative technologies for voltage regulation and reactive power compensation presents another challenge for the shunt reactor market.

Technologies such as Static VAR Compensators (SVCs) and Static Synchronous Compensators (STATCOMs) offer dynamic and flexible solutions for managing reactive power and maintaining voltage stability. These alternatives can be more attractive in certain applications, particularly in regions where rapid response to grid fluctuations is required.

Although shunt reactors are cost-effective for long-term and steady-state reactive power compensation, the presence of these more advanced and versatile technologies can limit their market share. As utilities weigh the benefits and drawbacks of each technology, the competition from these alternatives could restrain the growth of the market.

Integration with Renewable Energy Systems

The demand for shunt reactors is estimated to grow significantly as the global push toward renewable energy sources accelerates. Shunt reactors play a critical role in stabilizing voltage levels and improving power systems' efficiency particularly in integrating renewable energy sources such as wind and solar power into the grid.

Renewable energy sources are inherently variable and can lead to voltage-level fluctuations. Shunt reactors help mitigate these fluctuations by absorbing excess reactive power, thereby stabilizing voltage levels and ensuring reliable power supply.

The integration of shunt reactors becomes increasingly crucial as countries invest significantly in renewable energy infrastructure to meet climate goals and reduce reliance on fossil fuels. The global shift to renewable energy presents a significant opportunity for the shunt reactor market. Energy providers and grid operators are actively seeking advanced solutions to manage the complexities of renewable energy integration.

The increasing adoption of smart grid Sensor technologies and the development of advanced control systems further underscore the relevance of shunt reactors in modern power grids. Manufacturers of shunt reactors can leverage this opportunity by offering solutions that enhance grid stability and efficiency, positioning themselves favourably in a rapidly expanding market.

Companies operating in the shunt reactor market have a unique opportunity to capitalize on these trends by innovating and providing solutions tailored to the evolving needs of the energy sector.

The major competitors in the shunt reactor market are primarily evaluated based on their product or service offerings, their financial statements, developments and the approaches implemented, the company's position in the global market scenario and its geographical reach.

The key competitors in the industry employ crucial strategies like partnership deals, mergers and acquisitions, and business expansion deals to strengthen their hold on a particular region or a particular service offering.

Recent Industry Developments in the Shunt Reactor Market

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Type

By Phase

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is estimated to be valued at US$4.1 Bn by 2031

The market is projected to exhibit a CAGR of 7% over the forecast period.

A few of the key players operating in the market are ABB, General Electric, and Siemens, Crompton Greaves.

Asia Pacific region dominates the market and to account for 36% market share.

The rising electricity demand drives the market forward.