- Electrical Equipment & Services

- Servo Motors and Drives Market

Servo Motors and Drives Market Size, Share, and Growth Forecast 2026 - 2033

Servo Motors and Drives Market by Product Type (Servo Motors: AC Servo Motors, DC Servo Motors, Linear Servo Motors, Rotary Servo Motors; Servo Drives: AC Servo Drives, DC Servo Drives, Multi-Axis Servo Drives), Power Rating (Below 1 kW, 1 kW – 5 kW, 5 kW – 15 kW, Above 15 kW), Application (Robotics, CNC Machines / Machine Tools, Packaging Equipment, Semiconductor & Electronics Equipment, Others), and Regional Analysis, 2026 - 2033

Servo Motors and Drives Market Size and Trend Analysis

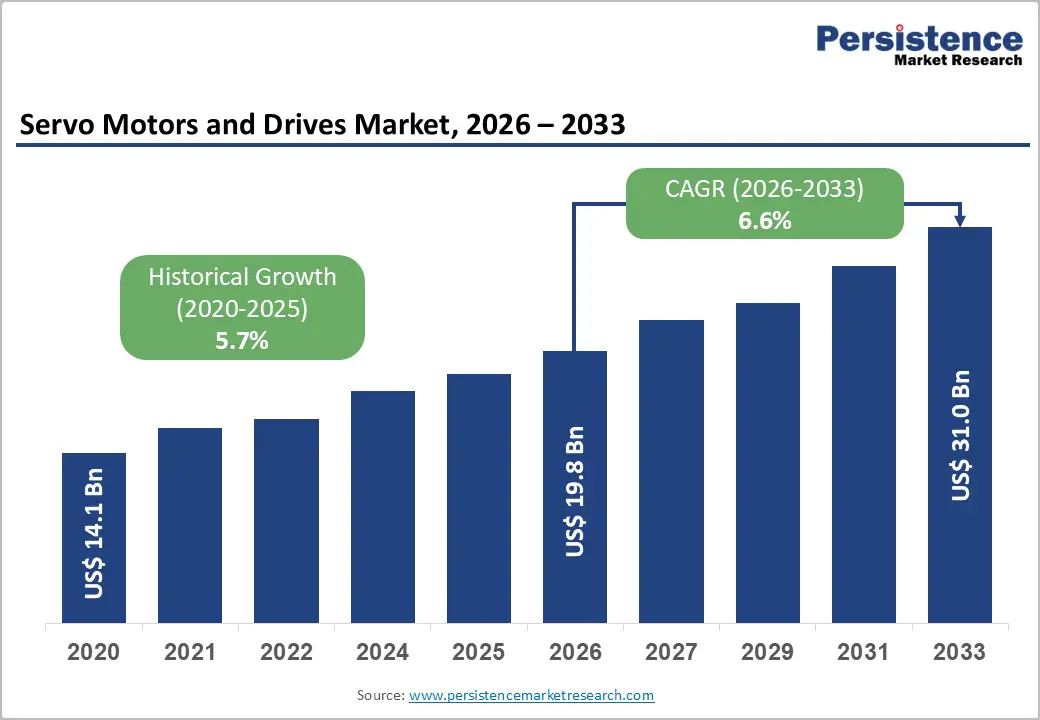

The global servo motors and drives market size is expected to be valued at US$ 19.8 Bn in 2026 and projected to reach US$ 31.0 Bn by 2033, growing at a CAGR of 6.6% between 2026 and 2033. Accelerating factory automation across automotive, electronics, food-processing industries; rapid surge in industrial robotics deployments globally; and intensifying adoption of CNC machine tools in precision manufacturing encourage the need for servo motors and drives.

According to the International Federation of Robotics (IFR), global robot installations exceeded 500,000 units in 2023, with each articulated robot requiring multiple servo axes, directly amplifying servo motor and drive demand. National industrial policies such as Germany's Industrie 4.0, China's Made in China 2025, and the U.S. CHIPS and Science Act are catalysing capital-intensive manufacturing upgrades, ensuring sustained procurement of high-precision motion-control components over the forecast period.

Key Industry Highlights:

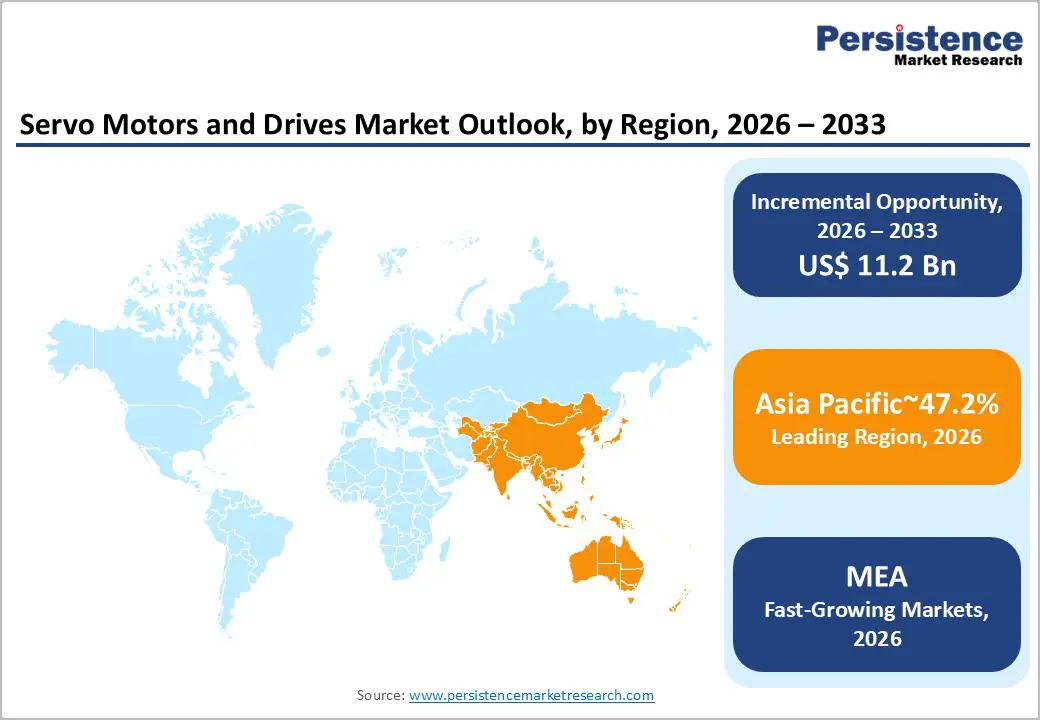

- Leading Region: Asia Pacific dominates with approximately 47% global market share in 2025, driven by China's world-leading industrial robot installations, Japan's precision manufacturing ecosystem, and accelerating electronics and EV manufacturing investments across South Korea and Southeast Asia.

- Dominant Product Type: AC servo motors command approximately 45% of global product-type share in 2025, underpinned by superior energy efficiency, maintenance-free permanent magnet synchronous motor (PMSM) designs, and broad compatibility with modern industrial automation architectures.

- Fastest Growing Product Type: Rotary servo motors are the fastest-growing product sub-segment at approximately 6% CAGR, driven by accelerating demand from industrial robotics, where rotary servo axes are the fundamental motion element and CNC machine tool expansion globally.

- Key Opportunity: Semiconductor Fab Expansion: The US$52.7 Bn U.S. CHIPS Act and €43 Bn EU Chips Act are catalysing unprecedented semiconductor manufacturing capital expenditure, creating a high-value, sustained demand pocket for ultra-precision servo motion-control systems in wafer handling, lithography, and inspection equipment.

DRO Analysis

Drivers - Industrial Automation and Smart Manufacturing as a Foundational Demand Driver for Servo Systems

The global shift toward Industry 4.0 and smart manufacturing is a primary catalyst for the demand for servo motors and drives. Industrial automation spending is accelerating as manufacturers seek precision, repeatability, and energy efficiency unattainable with conventional AC induction motors. The International Energy Agency (IEA) reports that electric motor systems, including servo systems, account for approximately 45% of global electricity consumption, incentivising companies to transition toward high-efficiency servo architectures.

Major economies, including the United States, Germany, Japan, and South Korea, are deploying government-backed programs to modernise manufacturing infrastructure. Siemens AG and Mitsubishi Electric have both reported double-digit growth in their motion-control divisions, citing factory automation as the principal demand driver. As production lines increasingly integrate vision systems, collaborative robots, and real-time quality inspection modules, servo-driven actuation becomes indispensable, forming a structural and durable demand driver over the 2026–2033 forecast horizon.

Industrial Robotics and EV Manufacturing as a High-Volume Demand Engine for Servo Systems

The convergence of industrial robotics proliferation and electric vehicle (EV) manufacturing expansion represents a compounding demand engine for the servo motors and drives market. The International Federation of Robotics (IFR) recorded a global operational stock of approximately 3.9 million industrial robots by the end of 2023, and forecasts continued high single-digit annual growth. Each six-axis articulated robot requires six servo axes minimum, translating robot shipment volumes directly into servo component procurement.

EV manufacturing is reshaping automotive assembly: battery module assembly, motor winding, and chassis joining all rely on precision servo-driven equipment. Tesla, BYD, and Volkswagen Group have collectively invested over US$100 Bn in EV-dedicated gigafactory capacity through 2026, embedding high-density servo motion-control throughout new production lines. This dual robotics-EV tailwind is accelerating the servo market's trajectory beyond historical growth rates.

Restraints - High Initial Investment and Integration Complexity

Despite compelling efficiency advantages, the elevated capital cost of servo motor and drive systems relative to conventional induction-motor alternatives remains a significant adoption barrier, particularly for small and medium-sized enterprises (SMEs). A fully configured servo axis comprising motor, drive, encoder, cabling, and commissioning can cost three to five times more than an equivalent induction motor setup. Integration complexity is compounded by the need for specialised engineering expertise in motion-control programming, PLC interfacing, and tuning of control loops.

According to the European Commission's SME Observatory, over 99% of EU enterprises are classified as SMEs, yet fewer than 30% of manufacturing SMEs have deployed advanced automation, with cost cited as the primary obstacle. These economic friction points slow market penetration in cost-sensitive segments and developing economies.

Opportunities - Semiconductor & Electronics Manufacturing as a Core Precision-Driven Demand Cluster for Servo Systems

The global semiconductor manufacturing capacity expansion catalysed by the U.S. CHIPS and Science Act (US$52.7 Bn in federal funding), the EU Chips Act (€43 Bn mobilised investment target), and massive fabrication investments by TSMC, Samsung, and Intel is creating a high-value, sustained demand pocket for ultra-precision servo systems. Semiconductor wafer handling, photolithography stage positioning, wire bonding, and automated optical inspection all require nanometer-scale positional accuracy achievable only with advanced servo drives.

The Semiconductor Industry Association (SIA) projects that global chip sales will surpass US$1 trillion by 2030, necessitating substantial fab equipment investments where servo motion-control is integral. Manufacturers offering sub-micron accuracy linear servo systems and multi-axis drive controllers are positioned to capture disproportionate value in this high-margin application segment over the forecast period.

Medical Devices and Surgical Robotics as a Premium, High-Specification Servo Application Segment

Medical device manufacturing and surgical robotics represent a high-growth, high-margin opportunity for servo system suppliers. The global surgical robotics market is on a steep growth trajectory with systems such as Intuitive Surgical's da Vinci platform and competitive entrants from Medtronic, Johnson & Johnson MedTech, and CMR Surgical driving demand for miniaturised, ultra-low-noise servo motors.

The U.S. Food and Drug Administration (FDA) cleared over 100 novel robotic surgical or automation-assisted medical devices between 2021 and 2023, signalling regulatory openness to robotic-assisted interventions. Beyond surgical platforms, pharmaceutical fill-and-finish automation, laboratory liquid-handling robots, and diagnostic imaging equipment all increasingly incorporate servo-driven precision actuation. The World Health Organisation (WHO) projects global healthcare expenditure will reach US$10 trillion by 2030, a macro-environment that structurally supports continued investment in automated medical manufacturing and care-delivery robotics.

Category-wise Analysis

Product Type Insights

AC servo motors dominate the global servo motors and drives market, commanding approximately 45% of the total market share in 2025. This leadership is attributable to their superior torque density, energy efficiency, lower maintenance requirements compared to DC alternatives, and seamless compatibility with modern variable-frequency drive architectures. AC servo motors eliminate the commutator and brushes of DC designs, substantially reducing mechanical wear, a critical advantage in high-duty-cycle industrial environments.

The proliferation of permanent magnet synchronous motors (PMSM), the prevailing AC servo topology, has been further accelerated by advances in rare-earth magnet manufacturing and digital encoder technologies. Major producers, including Fanuc, Yaskawa Electric, and Beckhoff Automation, have substantially expanded their AC servo portfolios, offering integrated motor-drive solutions optimised for robotics, CNC machine tools, and semiconductor equipment applications, where precise velocity and position control are non-negotiable operational requirements.

Power Rating Insights

The 1 kW – 5 kW power rating segment leads the global servo motors and drives market with approximately 38% of total revenue share in 2025. This mid-range segment occupies the performance sweet spot for the broadest array of industrial applications, encompassing robotic joint actuation, CNC axis drives, packaging machinery servo axes, and automated assembly equipment. Motors in this range deliver sufficient torque for meaningful payload handling while remaining compact enough for integration into space-constrained machine designs.

Standard industrial robot joints are the fastest-growing application, predominantly utilising servo motors in the 1 kW – 3 kW range per axis. The IFR notes that the average collaborative robot (cobot) integrates six servo axes, typically all within this power band. Additionally, the 1 kW–5 kW bracket benefits from mature manufacturing volumes, enabling competitive pricing that accelerates adoption among mid-tier manufacturing enterprises globally.

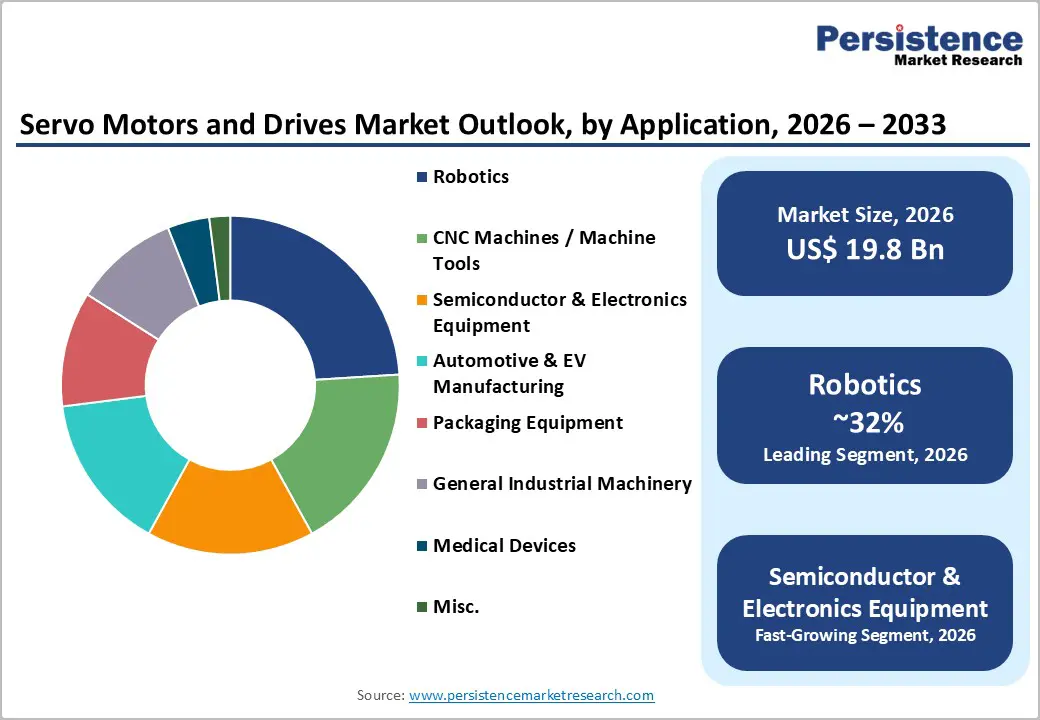

Application Insights

Robotics stands as the leading application segment for servo motors and drives, accounting for approximately 32% of the global application-based market share in 2025. Industrial robots spanning articulated, SCARA, delta, and collaborative configurations are the single largest per-unit consumer of servo motor-drive pairings, with each robot requiring a minimum of four to six precision servo axes.

The IFR's World Robotics 2023 report documented a record 553,052 industrial robot installations globally in 2022, with automotive and electronics sectors absorbing the largest volumes. China alone installed over 290,000 robots in 2022, demonstrating the scale of servo demand generated by robotics adoption. The trend toward human-robot collaboration in flexible manufacturing cells and the rapid deployment of mobile manipulators in logistics and warehousing are further expanding robotics' already dominant share of servo system demand through the forecast period.

Regional Insights

North America Servo Motors and Drives Market Trends and Insights

North America holds approximately 26% of the global servo motors and drives market share in 2025, supported by robust automotive manufacturing, a rapidly expanding semiconductor fabrication sector, and significant investments in defence and aerospace automation. The U.S. CHIPS and Science Act and the reshoring of critical manufacturing are generating multi-year capital expenditure cycles in precision automation equipment. Adoption of collaborative robots in SME manufacturing and EV battery gigafactory construction further sustains regional demand.

U.S. Servo Motors and Drives Market Size

The United States is expected to generate approximately US$ 4,092.4 million in servo motors and drives revenue in 2026, making it the largest contributor within North America. Demand is structurally anchored in EV-focused production ecosystems, where gigafactories operated by Tesla, Rivian, and General Motors deploy high-density servo motion across battery assembly, e-drive manufacturing, and automated body shops.

Parallel capacity additions in advanced semiconductor fabrication, particularly facilities established by Intel and TSMC in Arizona are driving demand for ultra-precision servo systems used in wafer handling and lithography support equipment. Incremental contributions also arise from defence-grade precision machining and pharma fill-finish automation, reinforcing the country’s dominant and technology-intensive demand profile.

Europe Servo Motors and Drives Market Trends and Insights

Europe represents approximately 21% of the global servo motors and drives market share in 2025, underpinned by the region's advanced mechanical engineering tradition, dense concentration of machine tool manufacturers, and the EU's Strategic Autonomy agenda driving industrial technology investments. Germany, Italy, and Switzerland lead regional demand. The EU Chips Act and Net-Zero Industry Act are catalysing precision manufacturing investments. Fastest growth is observed in Eastern European automotive supply-chain expansion.

Germany Servo Motors and Drives Market Size

Germany commands generates US$ 1,395.9 million in servo motors and drive revenue in 2026, reflecting the country's role as the continent's premier machine tool and industrial automation hub. Siemens, Beckhoff, and Bosch Rexroth are headquartered here, reinforcing domestic supply and application expertise. Automotive electrification investments by Volkswagen Group and BMW are driving sustained servo system procurement for EV battery and powertrain assembly lines.

France Servo Motors and Drives Market Size

France accounts for approximately US$ 654.3 Mn of the European servo motors and drives market. The country's strong nuclear energy infrastructure maintenance programs, automotive manufacturing base led by Stellantis and Renault Group and aerospace sector centered on Airbus and Safran are the primary demand generators. France's Plan France Relance industrial reinvestment program has also accelerated automation upgrades across food processing and packaging industries.

Asia Pacific Servo Motors and Drives Market Trends and Insights

Asia Pacific is the dominant global region, commanding approximately 47% of total servo motors and drives market share in 2025 and representing the fastest-growing region at an estimated 7.1% CAGR through 2033. China alone drives over half of regional volume, supported by the world's largest industrial robotics installation base, exceeding 290,000 units annually and a massive electronics manufacturing ecosystem. South Korea, Japan, and Southeast Asia further add depth to regional demand through semiconductor, automotive, and consumer electronics manufacturing expansions.

India Servo Motors and Drives Market Size

India is positioned as one of the fastest-scaling markets within Asia Pacific, with an estimated market value of US$ 931.9 million in 2026 and a projected CAGR of 7.7% through 2033. Demand is being structurally shaped by the Production Linked Incentive (PLI) scheme, which is channelling capital into electronics, automotive, and pharmaceutical manufacturing segments that inherently require servo-driven precision automation in assembly, inspection, and material handling.

India’s automotive electrification roadmap is translating into tangible servo demand at the production level, particularly in battery module assembly and e-powertrain manufacturing, led by OEMs such as Tata Motors and Mahindra Electric. This combination of policy-backed industrialisation and EV-focused manufacturing is creating a technology-intensive demand base for servo motors and drives across new and upgraded production lines.

China Servo Motors and Drives Market Size

China commands the largest share of the global servo motors and drives market, with a market value of US$ 4,193.5 million in 2026. Demand is anchored in electronics and semiconductor manufacturing clusters such as Shenzhen, Suzhou, and Shanghai, where high-speed SMT lines, wafer handling systems, and precision assembly equipment rely on dense servo integration. At the same time, EV manufacturing ecosystems led by BYD and NIO are embedding servo-driven automation across battery pack assembly, motor production, and final assembly lines.

Competitive Landscape

The global servo motors and drives market exhibits a moderately consolidated competitive structure, with the top five players, Siemens AG, Fanuc Corporation, Yaskawa Electric Corporation, Rockwell Automation, and Mitsubishi Electric, collectively commanding approximately 45–50% of global revenue. The remainder is distributed across a diverse ecosystem of regional specialists and application-focused niche players.

Market leaders are differentiating through integrated motion-control ecosystems, bundling servo motors, drives, PLCs, and industrial software, reducing customer switching costs. Key strategic themes include acquisitions of industrial software and IIoT analytics firms, co-development partnerships with robotics OEMs, and substantial R&D investment in SiC-based servo drive inverters for higher efficiency and power density. Emerging players are competing on application specialisation, notably in medical robotics and semiconductor equipment niches.

Key Developments:

- In May, 2025, Yaskawa Electric Corporation: The company announced the global rollout of its Σ-X Series 400V AC servo drive models, expanding its flagship servo lineup to support large-scale industrial equipment across Europe and Asia; the new models deliver industry-leading motion performance (up to 3.5 kHz response frequency and 7000 rpm speed), enhanced 26-bit encoder precision, and integrated digital data solutions (including predictive maintenance and sensor connectivity), strengthening Yaskawa’s position in high-performance, Industry 4.0–enabled servo systems.

- June, 2025, Mitsubishi Electric Corporation: The company launched its MELSERVO-JET servo system, a new cost-effective servo drive lineup designed to enable affordable industrial automation; offering compact design, flexible deployment, and power ranges from 0.1 kW to 7 kW, the system delivers high positioning accuracy (24-bit encoders) and fast response speeds (up to 3.2 kHz), addressing manufacturers’ growing demand for high-performance yet budget-efficient servo solutions amid increasing focus on ROI-driven automation investments.

Global Servo Motors and Drives Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 14.2 Bn |

|

Current Market Value (2026) |

US$ 19.8 Bn |

|

Projected Market Value (2033) |

US$ 31.0 Bn |

|

CAGR (2026–2033) |

6.6% |

|

Leading Region |

Asia Pacific, 47% share (2025) |

|

Dominant Product Type |

AC Servo Motors, 45% share (2025) |

|

Top-ranking Power Rating |

1 kW – 5 kW, 38% share (2025) |

|

Incremental Opportunity (2026–2033) |

~US$ 11.2 Bn |

Companies Covered in Servo Motors and Drives Market

- Siemens AG

- Fanuc Corporation

- Yaskawa Electric Corporation

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- ABB Ltd.

- Bosch Rexroth AG

- Beckhoff Automation GmbH & Co. KG

- Schneider Electric SE

- Parker Hannifin Corporation

- Panasonic Industry Co., Ltd.

- Nidec Corporation

- Delta Electronics, Inc.

- Kollmorgen Corporation (Roper Technologies)

- Lenze SE

- OMRON Corporation

- Oriental Motor Co., Ltd.

- Moog Inc.

- Regal Rexnord Corporation

Frequently Asked Questions

The global Servo Motors and Drives market is estimated to be valued at US$ 19.8 Bn in 2026, driven by accelerating industrial automation and robotics adoption worldwide.

The primary demand drivers include accelerating industrial automation under Industry 4.0 initiatives, explosive growth in industrial robotics with the IFR reporting over 553,000 robot installations in 2022 and the rapid expansion of EV gigafactory construction requiring precision servo-intensive assembly systems. Government-backed semiconductor manufacturing programs, including the U.S. CHIPS and Science Act, are also generating significant incremental servo system demand.

Asia Pacific is the leading region, accounting for approximately 47% of global market share in 2025. The region's dominance is driven by China's world-leading industrial robot installation volumes, Japan's deep precision manufacturing ecosystem anchored by Fanuc and Yaskawa Electric, and accelerating EV and electronics manufacturing investments across South Korea, India, and Southeast Asia.

The most significant forward-looking opportunity lies in semiconductor manufacturing expansion, where the U.S. CHIPS and Science Act (US$ 52.7 Bn) and EU Chips Act (€43 Bn) are catalyzing unprecedented fab construction requiring ultra-precision servo motion-control in wafer handling, lithography staging, and automated inspection a high-value, durable demand pocket through 2033.

The leading companies in the global Servo Motors and Drives market include Siemens AG, Fanuc Corporation, Yaskawa Electric Corporation, Rockwell Automation, Mitsubishi Electric, ABB Ltd., Bosch Rexroth, Beckhoff Automation, Schneider Electric, and Parker Hannifin.