- Pharmaceuticals

- Rheumatoid Arthritis Market

Rheumatoid Arthritis Market Size, Share, and Growth Forecast 2026 - 2033

Rheumatoid Arthritis Market by Drug Type (Disease-Modifying Anti-Rheumatic Drugs (DMARDs), Biologics, Janus Kinase (JAK) Inhibitors, Non-Steroidal Anti-Inflammatory Drugs (NSAIDs), Corticosteroids, Others), Route of Administration (Oral, Injectable, Intravenous), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis, 2026 - 2033

Rheumatoid Arthritis Market Share and Trends Analysis

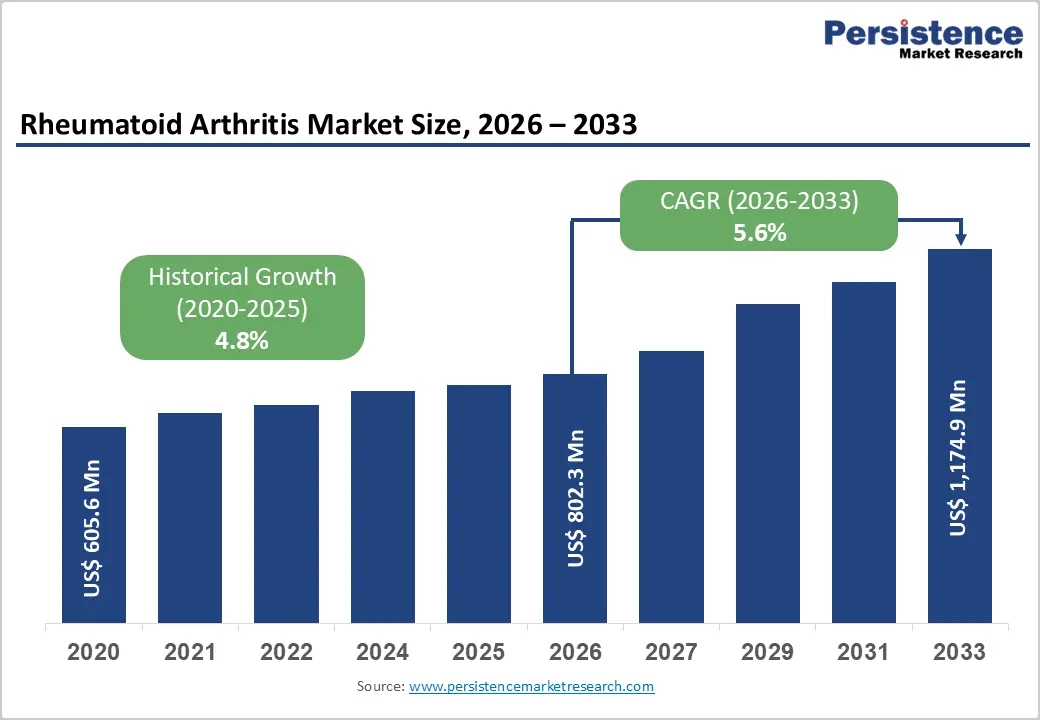

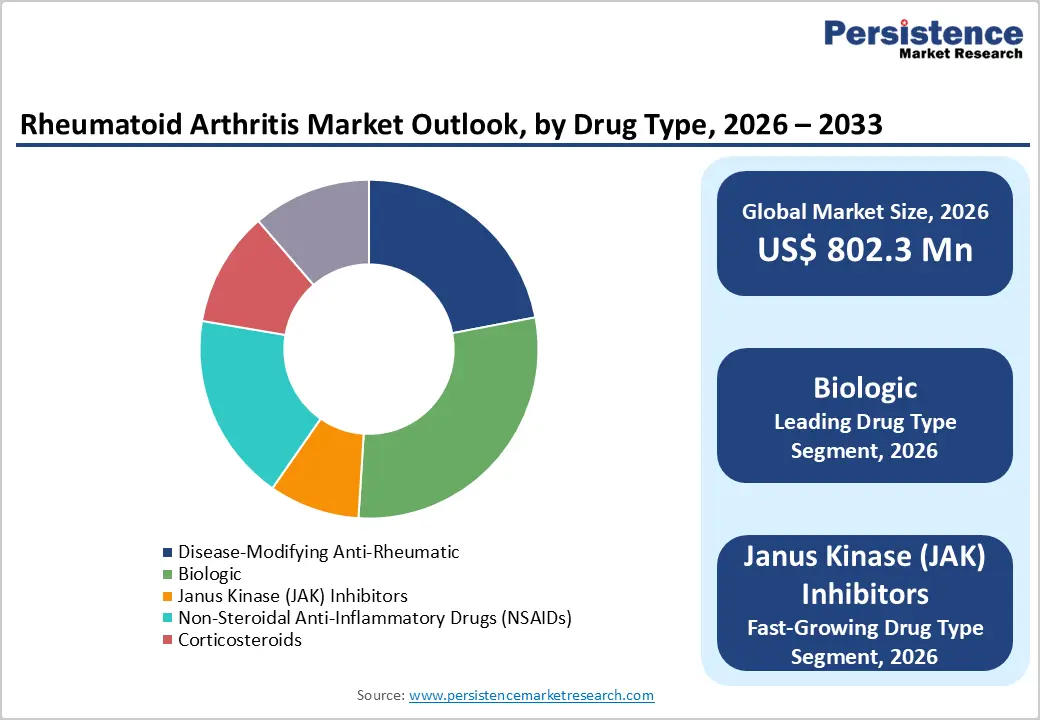

The global rheumatoid arthritis market size is expected to be valued at US$ 802.3 million in 2026 and projected to reach US$ 1,174.9 million by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

This growth is driven by the rising global prevalence of rheumatoid arthritis (RA), a chronic autoimmune condition affecting approximately 18 million people worldwide, according to the Global Burden of Disease Study published in The Lancet, combined with a robust pharmaceutical innovation pipeline advancing JAK inhibitors, next-generation biologics, and biosimilars.

The American College of Rheumatology (ACR) and European League Against Rheumatism (EULAR) guidelines continuously evolve to incorporate newer targeted therapies, broadening prescribing pathways. Expanding biosimilar access for key biologic agents is simultaneously improving affordability and increasing treatment initiation rates across both high-income and emerging markets, sustaining the upward revenue trajectory through the 2033 forecast period.

Key Industry Highlights

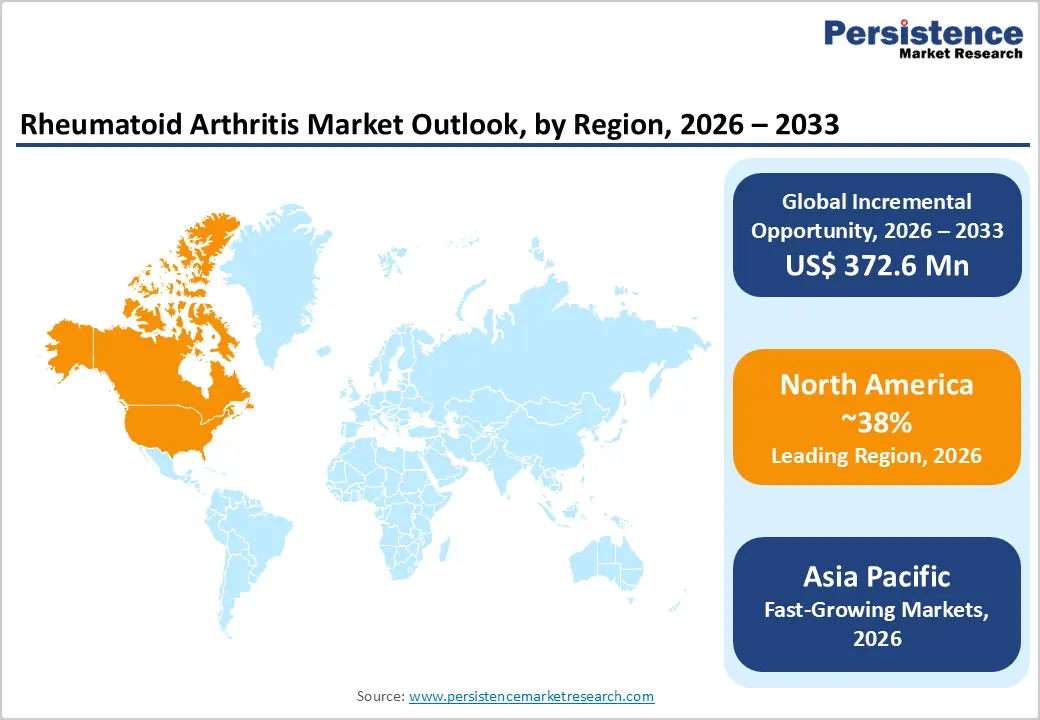

- Leading Region: North America leads the global Rheumatoid Arthritis market with approximately 38% revenue share in 2025, driven by over 1.5 million U.S. RA patients (Arthritis Foundation), highest global biologic prescribing rates, and comprehensive ACR treat-to-target guideline adoption.

- Fast-Growing Region: Asia Pacific is the fastest growing RA market during 2026 - 2033, led by China's ~5 million RA patients expanding into biologic therapy through NMPA approvals and National Medical Insurance Drug List reimbursement expansion across the region.

- Dominant Drug Type: Biologics lead the drug type category with approximately 29% market share in 2025, anchored by guideline-endorsed TNF inhibitors, including Humira, Enbrel, and IL-6 inhibitors as the standard of care for moderate-to-severe RA after DMARD failure.

- Fast-Growing Drug Class: JAK Inhibitors are the fastest growing drug class during 2026 - 2033, driven by oral dosing convenience, FDA/EMA-approved products including Rinvoq (AbbVie) and Olumiant (Eli Lilly), and expanding indication portfolios across multiple autoimmune conditions.

- Key Opportunity: Biosimilar market expansion with 40+ FDA-approved biosimilars and adalimumab biosimilars priced 20-55% below Humira is dramatically expanding RA treatment access in Asia Pacific, Eastern Europe, and Latin America, creating high-volume commercial opportunities for biosimilar manufacturers.

Market Dynamics

Drivers - Rising Global RA Prevalence and Expanding Diagnosed Patient Pool

Rheumatoid arthritis is a systemic autoimmune disease with a global prevalence of approximately 0.5-1% of the adult population, with women affected at 2-3 times the rate of men, according to research published in Arthritis & Rheumatology. The Global Burden of Disease (GBD) Study estimates that the number of RA patients globally grew significantly over the past two decades, with aging populations in North America, Europe, and the Asia Pacific accounting for the majority of growth.

Significantly, improving diagnosis rates driven by wider availability of anti-CCP antibody testing, rheumatologist workforce expansion, and digital health screening tools are converting a historically underdiagnosed population into treated patients. Each newly diagnosed RA patient typically requires decades of pharmacological management, creating substantial long-duration prescription revenue across all drug categories.

Expansion of Targeted Therapies and ACR/EULAR Guideline-Driven Prescribing

The structural evolution of RA treatment guidelines toward earlier and more aggressive treatment with targeted therapies is a key commercial driver. The ACR 2021 RA Treatment Guidelines and EULAR 2022 Recommendations both endorse a treat-to-target (T2T) strategy recommending initiation of conventional DMARDs (methotrexate) at diagnosis and rapid escalation to biologic or JAK inhibitor therapy when targets are not met. This T2T paradigm systematically drives patients toward higher-value therapeutic categories.

AbbVie's Rinvoq (upadacitinib) and Eli Lilly's Olumiant (baricitinib) have both received FDA and EMA approvals for RA with broad label indications, reinforcing guideline-backed commercial expansion for the JAK inhibitor class across multiple markets.

Restraints - High Cost of Biologic and JAK Inhibitor Therapies Limiting Access

Biologic therapies for RA carry annual treatment costs of US$ 20,000-US$ 50,000 per patient in the U.S., and JAK inhibitors similarly range from US$ 25,000-US$ 30,000 annually, according to pricing disclosures by AbbVie and Pfizer. These costs create significant access barriers in uninsured or underinsured patient populations and constrain formulary adoption in cost-sensitive healthcare systems across the Asia Pacific, Latin America, and the Middle East & Africa. Despite biosimilar entry reducing biologic costs by 20-40%, affordability remains a structural constraint on total global RA treatment uptake.

FDA Safety Signals and Labeling Restrictions on JAK Inhibitors

The FDA's 2021 safety communication and subsequent 2022 updated Boxed Warning for all approved JAK inhibitors based on the ORAL Surveillance study findings from Pfizer's Xeljanz (tofacitinib) trial highlighted increased risks of major cardiovascular events, malignancy, thrombosis, and mortality compared to TNF inhibitors. This has restricted JAK inhibitor prescribing to patients who have failed or cannot tolerate TNF inhibitors in the U.S. and EU, limiting first-line commercial opportunity and creating prescribing friction that constrains the class's near-term growth trajectory.

Opportunities - Biosimilar Market Expansion Driving the Treatment Accessibility in Emerging Markets

The progressive loss of patent exclusivity for anchor biologic RA therapies, including adalimumab (Humira, AbbVie), etanercept (Enbrel, Pfizer/Amgen), and infliximab (Remicade, Johnson & Johnson) is creating a significant biosimilar commercial opportunity that expands RA treatment access globally.

The FDA has approved over 40 biosimilar products across all therapeutic categories as of 2024, with multiple adalimumab biosimilars from Amgen (Amjevita), Boehringer Ingelheim (Cyltezo), and Sandoz (Hyrimoz) entering the U.S. market in 2023. Biosimilars priced 20-50% below reference products are enabling RA treatment initiation in cost-sensitive healthcare systems across Asia Pacific, Eastern Europe, and Latin America, expanding the addressable treated patient population and creating large-volume, competitively priced biosimilar revenue streams for participating manufacturers.

Category-wise Analysis

Drug Type Insights

The Biologic drug segment leads the Rheumatoid Arthritis market, accounting for approximately 29% of total drug type revenue in 2025. Biologics including TNF inhibitors (adalimumab, etanercept, infliximab), IL-6 inhibitors (tocilizumab, sarilumab), and co-stimulation modulators (abatacept) are the guideline-endorsed standard of care for moderate-to-severe RA following inadequate DMARD response, as established by ACR 2021 and EULAR 2022 recommendations. AbbVie's Humira (adalimumab) was for many years the world's best-selling pharmaceutical product, reflecting the category's commercial scale.

Although biosimilar entry is compressing biologic revenue per patient, volume growth through expanded access in emerging markets and broadening indication approvals sustains biologics' leading revenue position within the RA drug type hierarchy through the forecast period.

Route of Administration Analysis

The Injectable route of administration leads the RA therapeutics market, accounting for approximately 52% of route-based revenue in 2025. Injectable delivery encompassing both subcutaneous self-injection and intramuscular administration is the dominant route for biologic RA therapies, as most approved TNF inhibitors, IL-6 inhibitors, and co-stimulation modulators require subcutaneous injection. Products including Humira, Enbrel, and Actemra (tocilizumab, Roche) are administered via subcutaneous autoinjector or prefilled syringe, with established patient training programs supporting long-term self-administration adherence.

The introduction of autoinjector device improvements by AbbVie, Amgen, and UCB has increased patient comfort and adherence rates. The oral route's share is growing, however, as JAK inhibitor adoption expands among patients preferring pill-based administration over self-injection.

Distribution Channel Analysis

The Hospital Pharmacies segment leads the RA market by distribution channel, representing approximately 46% of channel revenue in 2025. Hospital pharmacies are the primary dispensing point for intravenous biologic therapies, including infliximab (Remicade, Inflectra) and Orencia (abatacept, Bristol-Myers Squibb) IV formulations, which require supervised clinical administration and cold-chain management. ACR and EULAR guidelines recommend initiating biologic therapy under rheumatologist supervision, further anchoring new prescription generation to hospital and specialty clinic settings.

The growing Specialty Pharmacy sub-channel within retail pharmacies is expanding its role for subcutaneous biologic dispensing under U.S. specialty pharmacy benefit manager (PBM) frameworks, creating a dual-channel procurement dynamic for RA biologics.

Regional Insights

North America Rheumatoid Arthritis Market Trends and Insights

North America leads the global RA market with approximately 38% of total revenue in 2025, driven by the highest global biologic and JAK inhibitor prescribing rates, comprehensive insurance reimbursement under Medicare Part D and commercial plans, and active FDA approval pipelines for RA therapeutics. The Arthritis Foundation estimates over 1.5 million Americans live with RA, representing one of the world's largest nationally treated RA populations.

U.S. Rheumatoid Arthritis Market Size

The U.S. accounts for approximately 88% of North America's RA market revenue. The introduction of multiple adalimumab biosimilars in 2023 has structurally shifted the biologic procurement landscape. AbbVie's Rinvoq, Eli Lilly's Olumiant, and Pfizer's Xeljanz hold strong formulary positions, supported by ACR guideline-backed treat-to-target prescribing that drives biologic and JAK inhibitor adoption for inadequate DMARD responders.

Europe Rheumatoid Arthritis Market Trends and Insights

Europe is the second-largest RA market, characterized by EMA-regulated drug approval pathways and national HTA reimbursement bodies-including NICE (U.K.), HAS (France), and IQWiG (Germany) that govern biologic access. EULAR 2022 Recommendations provide the clinical framework for RA management across member states, supporting consistent biologic prescribing practices. Biosimilar penetration is highest in Scandinavia and Germany, reducing per-patient biologic costs and expanding reimbursed treatment access.

Germany Rheumatoid Arthritis Market Size

Germany accounts for approximately 22% of the European RA market revenue. GKV reimbursement covers biologic and JAK inhibitor RA therapies following DMARD failure, and Germany's IQWiG benefit assessment framework drives biosimilar adoption. AbbVie, Pfizer, and UCB maintain leading branded positions, while Boehringer Ingelheim's Cyltezo and Sandoz biosimilars gain growing formulary share.

U.K. Rheumatoid Arthritis Market Size

The U.K. represents approximately 17% of European RA revenue. NICE Technology Appraisals govern biologic and JAK inhibitor reimbursement within the NHS, with specific NICE TA pathways for TNF inhibitors, JAK inhibitors, and IL-6 inhibitors. The NHS Biosimilar Medicines Programme has systematically driven adalimumab and etanercept biosimilar uptake, generating substantial cost savings that have expanded funded patient access.

France Rheumatoid Arthritis Market Size

France contributes approximately 15% of the European RA market revenue. The Haute Autorité de Santé (HAS) evaluates biologic RA therapies for reimbursement, and Assurance Maladie provides comprehensive coverage for guideline-recommended biologics. France has an active rheumatology specialist network supporting T2T treatment protocols, with AbbVie, Roche, and Sanofi holding significant revenue shares in the French RA therapeutic market.

Asia Pacific Rheumatoid Arthritis Market Trends and Insights

Asia Pacific is the fastest-growing RA market, expected to register the highest CAGR during 2026 - 2033. China dominates regional demand. The Chinese Rheumatology Association estimates approximately 5 million RA patients nationally with NMPA-approved biologic therapies, including domestic biosimilars gaining adoption as reimbursement frameworks expand under China's National Basic Medical Insurance Drug List. Japan, South Korea, India, and Australia are active markets with established biologic reimbursement pathways.

India Rheumatoid Arthritis Market Size

India accounts for approximately 13% of the Asia Pacific's RA market. The Indian Rheumatology Association (IRA) estimates RA affects approximately 10 million Indians, though the treated population remains underpenetrated. Domestically manufactured methotrexate and hydroxychloroquine DMARDs dominate, but growing bioequivalent biologic manufacturing by Cipla, Intas Pharmaceuticals, and Dr. Reddy's Laboratories is expanding biologic access.

Competitive Landscape

The rheumatoid arthritis market is highly competitive, supported by continuous innovation in biologics, targeted therapies, and advanced oral treatment options. Market participants focus on improving long-term disease control, reducing side effects, and enhancing patient convenience through easier administration methods. Strong investment in biosimilars is increasing pricing competition and expanding treatment accessibility across emerging regions. Strategic collaborations, clinical trials, and regulatory approvals remain key growth strategies to strengthen product pipelines.

Key Developments

- In May 2026, Artiva Biotherapeutics advanced its AlloNK therapy toward Phase 3 development for refractory rheumatoid arthritis after reporting positive Phase 2a results and securing FDA alignment for a single registrational trial.

- In May 2026, Bristol Myers Squibb received European Commission approval for Sotyktu (deucravacitinib) for the treatment of adults with active psoriatic arthritis who had an inadequate response or intolerance to prior DMARD therapy.

Companies Covered in Rheumatoid Arthritis Market

- AbbVie Inc.

- Pfizer Inc.

- Johnson & Johnson

- Amgen Inc.

- Bristol-Myers Squibb

- F. Hoffmann-La Roche Ltd.

- Novartis AG

- Eli Lilly and Company

- UCB S.A.

- Boehringer Ingelheim

- Regeneron Pharmaceuticals

- Sanofi S.A.

- Merck & Co.

Frequently Asked Questions

The global Rheumatoid Arthritis market is estimated to be valued at US$ 802.3 million in 2026.

Primary demand drivers include the global RA prevalence affecting approximately 18 million people (Global Burden of Disease Study, The Lancet), the ACR 2021 and EULAR 2022 treat-to-target guidelines systematically escalating patients to high-value biologic and JAK inhibitor therapy, and expanding biosimilar availability, reducing biologic costs by 20-55% and improving treatment access in Asia Pacific, Latin America, and Eastern Europe.

North America leads with approximately 38% of the global RA market revenue in 2025.

JAK Inhibitors the fastest growing drug class with AbbVie's Rinvoq and Eli Lilly's Olumiant expanding into multiple autoimmune indications beyond RA; and biosimilar biologics priced 20-55% below reference products (Boehringer Ingelheim's Cyltezo, Amgen's Amjevita) expanding RA treatment access across cost-sensitive markets in Asia Pacific, Eastern Europe, and Latin America.

The market is led by AbbVie Inc. (Humira/Rinvoq), Pfizer Inc. (Xeljanz/Enbrel/biosimilars), Eli Lilly (Olumiant), Johnson & Johnson (Remicade/Stelara), and F. Hoffmann-La Roche (Actemra).