- Transportation & Logistics

- Retail Logistics Market

Retail Logistics Market Size, Share, and Growth Forecast 2026 - 2033

Retail Logistics Market by Retail Type (Conventional Retail Logistics, E-commerce Retail Logistics), Solution Type (Transportation Management, Warehousing & Distribution, Commerce Enablement, Reverse Logistics & Liquidation), Mode of Transport (Roadways, Railways, Airways, Waterways), and Regional Analysis, 2026 - 2033

Retail Logistics Market Size and Trend Analysis

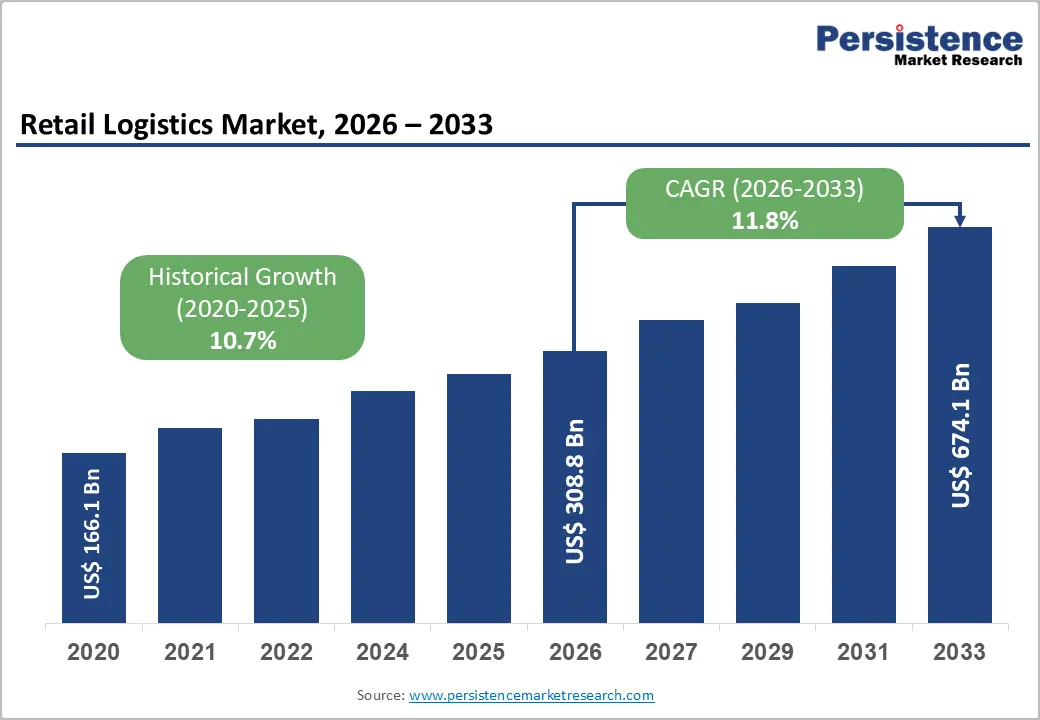

The global retail logistics market size is expected to be valued at US$ 308.8 billion in 2026 and projected to reach US$674.1 billion by 2033, growing at a CAGR of 11.8% between 2026 and 2033. The expansion is propelled by the shift in retail consumption toward digital channels and the resulting need for high-velocity, last-mile-ready supply chains. According to the UNCTAD Digital Economy Report 2024, global e-commerce sales crossed US$ 27 trillion, intensifying demand for integrated transportation, warehousing, and reverse logistics services.

Concurrent investments under the U.S. Bipartisan Infrastructure Law, the European Union's TEN-T network, and India's PM Gati Shakti programme are upgrading freight corridors, port capacity, and multimodal hubs, all of which directly compress order-to-delivery cycles and unlock further retail logistics throughput.

Key Industry Highlights:

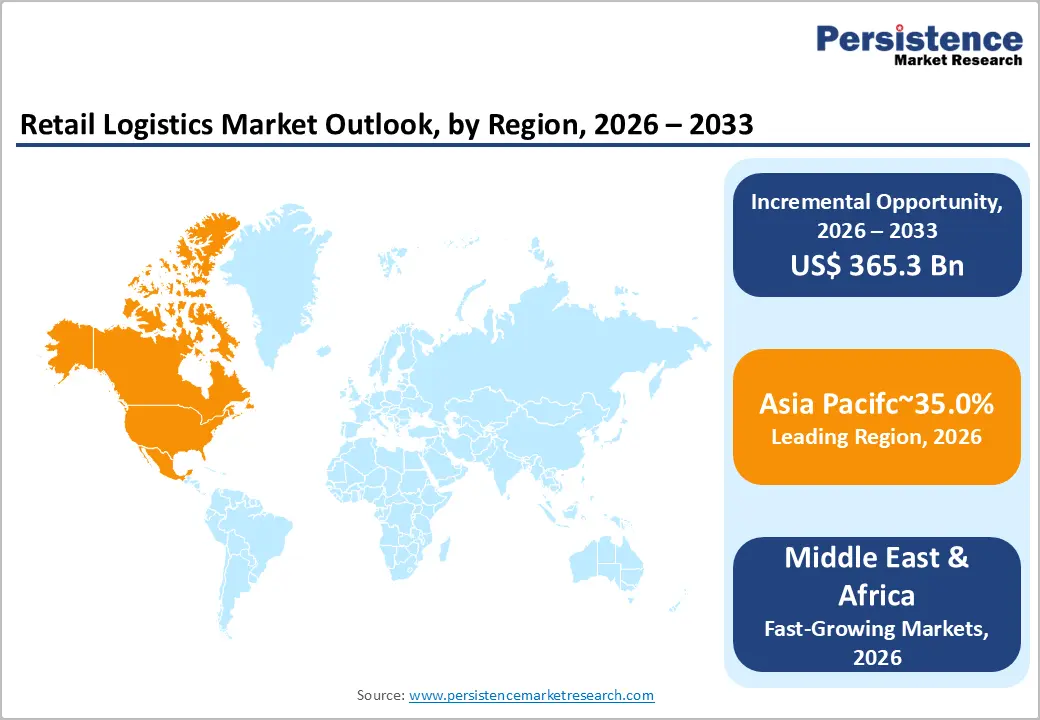

- Leading Region: North America leads the global retail logistics market with 30.5% share in 2025, anchored by mature e-commerce penetration, dense highway networks, and major investments by Amazon and Walmart in nearshoring-led regional fulfilment.

- Fastest Growing Market: Asia Pacific is the fastest-growing region at over 12.6% CAGR by 2033, fueled by China's scale, India's 63% YoY warehouse leasing surge, and rapid quick-commerce adoption across emerging Southeast Asian retail markets.

- Dominant Retail Type: Conventional retail logistics led with 54% share in 2025, supported by store-based retail's 84% share of U.S. retail sales and continued reliance on regional distribution centres serving hypermarket and grocery chains.

- Fastest Growing Retail Type: E-commerce retail logistics is the fast-growing segment at 11.9% CAGR through 2033, propelled by global online retail crossing US$27 trillion and rapid micro-fulfilment, dark store, and last-mile network buildouts.

- Key Opportunity: Quick commerce and AI-driven warehouse automation present the largest opportunity, with global quick commerce GMV projected to exceed US$195 billion by 2027 and AI-driven supply chains cutting logistics costs by up to 15%.

DRO Analysis

Drivers - Accelerated E-commerce Penetration and Omnichannel Retailing

The structural migration of retail consumption to online and hybrid channels has become the most decisive growth lever for retail logistics service providers. Per the U.S. Census Bureau, e-commerce accounted for 16.1% of total U.S. retail sales by Q4 2024, up from 11.0% in 2019, while Eurostat reports that 77% of EU internet users purchased goods online in 2024. In India, the e-commerce market is projected by IBEF to reach US$345 billion by 2030 from US$125 billion in 2024. This rapid digital adoption is forcing retailers to operate omnichannel fulfillment networks combining dark stores, micro-fulfilment centres, and same-day delivery, all of which structurally elevate logistics intensity per order and lift demand for specialised B2C retail logistics.

Infrastructure Modernisation and Government-led Logistics Reforms

Public capital deployment toward logistics infrastructure is sharply expanding the addressable opportunity for retail logistics operators. The U.S. Department of Transportation committed nearly US$1.2 trillion under the Bipartisan Infrastructure Law for roads, ports, and freight rail upgrades. China's 14th Five-Year Plan earmarks heavy investment into multimodal logistics hubs, while India's National Logistics Policy targets the reduction of logistics cost from 13–14% of GDP to 8% by 2030, supported by PM Gati Shakti and dedicated freight corridors. The European Commission has allocated €25.8 Billion under the Connecting Europe Facility (2021–2027) for the TEN-T network. These reforms reduce transit lead times, formalise warehousing, and directly catalyze retail supply chain efficiency.

Restraints - Volatile Fuel Prices and Rising Operational Costs

Retail logistics margins remain highly sensitive to diesel, jet fuel, and shipping cost volatility. The U.S. Energy Information Administration (EIA) reported on-highway diesel prices fluctuating between US$ 3.4 and US$ 5.8 per gallon between 2021–2024, while the International Energy Agency (IEA) noted persistent bunker fuel volatility driven by geopolitical disruptions in the Red Sea and Strait of Hormuz.

The Drewry World Container Index spiked over 300% in 2024 versus pre-Suez crisis levels. These cost shocks compress retailer margins, force surcharge pass-throughs that dampen volumes, and raise the breakeven threshold for low-density e-commerce parcels, restraining smaller logistics service providers' scalability.

Fragmented Regulatory Landscape and Cross-border Compliance Burden

Retail logistics operations spanning multiple jurisdictions face mounting compliance friction. The World Customs Organisation highlights that diverging customs digitisation timelines and non-tariff barriers add 3–5% to landed cost. The EU's Carbon Border Adjustment Mechanism (CBAM) and varying e-invoicing mandates across ASEAN economies further strain documentation workflows. U.S. de minimis rule revisions in 2024–2025 have disrupted cross-border parcel flows from Asia, while data localisation rules in India and China complicate cloud-based TMS deployments. Such regulatory heterogeneity inflates compliance costs for global 3PLs and slows penetration into emerging markets, posing a measurable restraint on market expansion.

Opportunities - Rapid Growth of Quick Commerce and Hyperlocal Fulfilment

Quick commerce represents one of the most lucrative emerging frontiers for retail logistics participants. The India Brand Equity Foundation (IBEF) estimates Indian quick commerce GMV reached US$6 billion in 2024, expanding at over 70% annually. This is reshaping warehousing footprints toward sub-2,000 sq. ft. dark stores located within 2–3 km of consumers.

CBRE reported that 3PL and e-commerce firms drove 57% of 27.1 million sq. ft. Indian warehouse leasing in H1 2025. Players investing in micro-fulfilment automation, electric two-wheeler fleets, and route-optimisation AI stand to capture disproportionate value as retailers outsource last-mile execution to specialist logistics partners.

Adoption of Automation, Robotics, and AI-driven Supply Chain Solutions

Warehouse automation and AI-led logistics orchestration are unlocking step-change productivity gains for retail logistics providers. The International Federation of Robotics (IFR) reported a record 541,302 industrial robot installations in 2023, with logistics and warehousing among the fastest-adopting verticals. Amazon has deployed over 750,000 mobile robots across its global fulfilment network as of 2024.

The World Economic Forum estimates AI-driven supply chain optimisation could reduce logistics costs by 15% and inventory levels by 35%. Investments in autonomous mobile robots (AMRs), AS/RS systems, computer-vision sortation, and generative-AI demand forecasting are creating differentiated service tiers. The e-commerce retail logistics segment, growing at 11.9% CAGR, will be the principal beneficiary of these technologies.

Category-wise Analysis

Retail Type Insights

Conventional retail logistics continues to anchor the market with an estimated 54% share in 2025, underpinned by the persistent dominance of brick-and-mortar retail across most economies. According to the U.S. Census Bureau, store-based retail still accounts for nearly 84% of total U.S. retail sales in 2024, while Eurostat confirms physical retail commands a comparable majority across the EU. Established networks of Walmart, Costco, Carrefour, Tesco, and Aldi rely on full-truckload, less-than-truckload, and pallet-based distribution serving regional distribution centers.

Robust replenishment cycles, large-format hypermarket throughput, and strong demand from grocery, apparel, and home improvement retailers sustain conventional logistics primacy. However, e-commerce retail logistics is the fastest-growing sub-segment at 11.9% CAGR through 2033, fueled by digital-first consumption.

Solution Type Insights

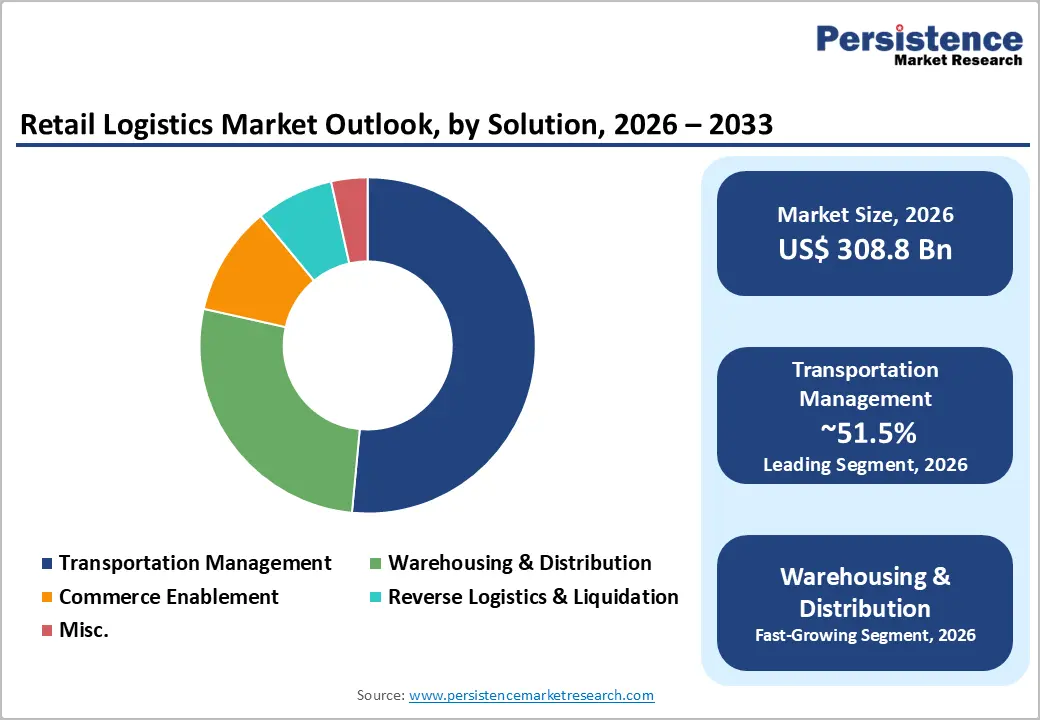

Transportation management leads the solution mix with around 52% share in 2025, reflecting the centrality of freight movement to every retail logistics workflow. The American Trucking Associations (ATA) reports trucks moved 72.6% of U.S. freight tonnage in 2023, generating US$987 billion in revenues, underscoring the strategic weight of transportation orchestration. Advanced TMS platforms from providers like SAP, Oracle, Manhattan Associates, and Blue Yonder enable dynamic route optimisation, multi-carrier rate shopping, and real-time visibility, all of which retailers prioritise to safeguard service-level agreements.

Warehousing & distribution is the fastest-growing solution at 11.6% CAGR through 2033, driven by surging e-commerce fulfillment, micro-fulfilment centre proliferation, and automation-led capacity additions across India, the U.S., and Europe.

Mode of Transport Insights

Roadways dominate the mode mix with approximately 68% share in 2025, a position reinforced by their unmatched flexibility in last-mile and middle-mile retail distribution. The International Road Transport Union (IRU) notes road freight handles over 75% of inland freight in the EU, while the Ministry of Road Transport and Highways, India, confirms roads carry roughly 64% of domestic freight. Dense highway networks in North America, accelerated National Highway expansion under India's Bharatmala project, and the rise of electric and CNG-powered delivery fleets keep roadways central.

Major operators, including DHL Supply Chain, XPO, J.B. Hunt, and Maersk Logistics, continue to invest in road-based regional fulfilment networks. Waterways, although smaller, is the fastest-growing mode at 11.4% CAGR, reflecting cost-efficient cross-border retail movements.

Regional Insights

North America Retail Logistics Market Trends and Insights

North America holds a 30.5% share of the global retail logistics market in 2025, anchored by mature e-commerce penetration, dense highway networks, and the largest concentration of organised retail capacity. The presence of Walmart, Amazon, Target, and Kroger, alongside leading 3PLs such as C.H. Robinson, XPO, and J.B. Hunt, sustains continuous investment in automation, nearshoring-driven inventory positioning, and same-day delivery infrastructure across the region.

U.S. Retail Logistics Market Size

The U.S. retail logistics market was valued at approximately US$ 69.5 billion in 2025, supported by record US$1.2 trillion in e-commerce sales reported by the U.S. Census Bureau for 2024. Nearshoring from Mexico under the USMCA, the expansion of regional fulfilment centers by Amazon and Walmart, and the adoption of AI-driven inventory positioning underpin this scale. Investments under the Bipartisan Infrastructure Law further strengthen the country's port-to-shelf logistics velocity.

Europe Retail Logistics Market Trends and Insights

Europe accounts for a 24.5% share of the global retail logistics market in 2025, supported by harmonised customs procedures under the Union Customs Code, the TEN-T corridor network, and dense intra-EU road and rail freight flows. Cross-border e-commerce growth, sustainability-driven fleet electrification under the EU Green Deal, and rising adoption of automated warehousing across Germany, the Netherlands, France, and Poland continue to anchor regional momentum. Türkiye, holding around 4.5% share in 2025, is among the fastest-growing markets, driven by its position as a Europe-MENA logistics gateway.

Germany Retail Logistics Market Size

The German retail logistics market is valued at approximately US$17.9 billion in 2025, retaining its position as Europe's largest retail logistics economy. Anchored by retailers such as Schwarz Group (Lidl, Kaufland), Aldi, Rewe, and Otto Group, and supported by Deutsche Post DHL as the dominant logistics integrator, the country benefits from a strategic location at the heart of EU freight corridors. Destatis reports German e-commerce turnover of approximately €80.6 Billion in 2024, underpinning warehousing demand.

U.K. Retail Logistics Market Size

The U.K. retail logistics market is estimated at around US$ 13.2 billion in 2025, accounting for nearly 16% of European retail logistics value. Per the Office for National Statistics (ONS), online sales accounted for 26.1% of total U.K. retail in 2024, the highest in Europe. Operators such as Wincanton, DHL Supply Chain, and GXO support major retailers including Tesco, Sainsbury's, and Marks & Spencer through automated regional distribution centers.

France Retail Logistics Market Size

France retail logistics market is valued at approximately US$ 10.1 billion in 2025, representing close to 12% of Europe market value. According to FEVAD, French e-commerce reached €175.3 Billion in 2024, expanding 9.6% YoY. Major players such as Carrefour, Auchan, Leclerc, and Decathlon rely on integrated 3PL networks managed by Geodis, STEF, and FM Logistic, supported by France's strategic Atlantic and Mediterranean port access.

Asia Pacific Retail Logistics Market Trends and Insights

The Asia Pacific region is the fastest-growing market, projected to expand at over 12.6% CAGR through 2033, propelled by rapid e-commerce adoption, large-scale infrastructure spending, and rising middle-class consumption. China remains the regional anchor, leveraging integrated rail-port-road corridors, while India, Indonesia, and Vietnam exhibit accelerating retail digitization. The proliferation of quick commerce, omnichannel retail, and tier-2/3 city expansion is structurally reshaping logistics demand across the region.

India Retail Logistics Market Size

India is the fastest-growing retail logistics market, valued at approximately US$15.5 billion in 2025. CBRE reported industrial and warehousing leasing surged 63% YoY to 27.1 million sq. ft. in H1 2025, with 3PL and e-commerce players accounting for 57% of demand. PM Gati Shakti, the National Logistics Policy, and dedicated freight corridors are reducing logistics cost from 13–14% of GDP toward global benchmarks, reinforcing the country's high-growth trajectory.

China Retail Logistics Market Size

China is the largest retail logistics market in the Asia Pacific, valued at approximately US$34.8 billion in 2025. Per the National Bureau of Statistics of China, online retail sales reached CNY 15.5 Trillion in 2024, with JD.com, Alibaba (Cainiao), and Pinduoduo operating world-leading automated fulfilment networks. The country's high-speed rail freight, coastal mega-ports, and Belt and Road Initiative corridors give it unmatched scale advantages in retail logistics throughput.

Competitive Landscape

The global retail logistics market is moderately fragmented, with the top ten players holding under 35% of the total market value. Competitive intensity is shaped by integrated end-to-end providers like DHL Supply Chain, Kuehne+Nagel, DB Schenker, and Maersk Logistics competing alongside asset-light digital freight platforms and regional specialists.

Strategic priorities include automation-led warehousing, last-mile electrification, near-shoring corridor capacity, and AI-enabled visibility. M&A activity remains high, exemplified by DSV's acquisition of Schenker in 2024. Emerging business models such as logistics-as-a-service, micro-fulfillment partnerships, and embedded shipping APIs are redefining differentiation, while ESG and Scope-3 emissions tracking emerge as critical procurement criteria for retailer-shippers.

Key Developments

- In September 2024, Kuehne+Nagel inaugurated its largest-ever highly automated omnichannel retail logistics hub in Mantova, Italy, featuring advanced robotics, real-time data integration, and sustainable infrastructure, enabling processing of up to 500,000 daily shipments across 19 countries while setting a new benchmark for efficient, digitalised, and environmentally responsible retail distribution.

- In November 2025, C.H. Robinson expanded its cross-border retail and supply chain logistics operations by adding 450,000 sq. ft. of warehousing and cross-docking capacity in El Paso, Texas, bringing its total U.S.–Mexico border footprint to over 2 million sq. ft., strengthening its ability to support growing nearshoring-driven retail and high-tech trade flows with more agile, scalable distribution infrastructure.

Global Retail Logistics Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 167.8 Billion |

|

Current Market Value (2026) |

US$ 308.8 Billion |

|

Projected Market Value (2033) |

US$ 674.1 Billion |

|

CAGR (2026-2033) |

11.8% |

|

Leading Region |

North America, 30.5% |

|

Dominant Category-1 |

Conventional Retail Logistics, US$ 166.8 Billion (2026E) |

|

Top-ranking Category-2 |

Transportation Management, US$ 159.0 Billion (2026E) |

|

Incremental Opportunity |

US$ 365.3 Billion (2026-2033) |

Companies Covered in Retail Logistics Market

- DSV

- XPO Logistics, Inc.

- Kuehne+Nagel International AG

- FedEx Corporation

- C.H. Robinson Worldwide, Inc.

- APL Logistics Ltd

- Nippon Express Co., Ltd.

- United Parcel Service, Inc.

- DHL International GmbH

- A.P. Moller – Maersk

- DB Schenker

Frequently Asked Questions

The global retail logistics market is expected to be valued at US$308.8 billion in 2026 and is projected to reach US$674.1 billion by 2033, expanding at a CAGR of 11.8% during the forecast period.

Accelerated e-commerce penetration is the principal demand driver, with global online retail crossing US$27 trillion per UNCTAD, U.S. e-commerce reaching 16.1% of retail sales, and India's e-commerce projected to hit US$345 billion by 2030.

North America leads the global retail logistics market with a 30.5% share in 2025, supported by mature e-commerce ecosystems, US$1.2 trillion infrastructure investments under the Bipartisan Infrastructure Law, and a strong network of fulfilment hubs.

Quick commerce and AI-led warehouse automation present the most significant opportunity, with global quick commerce GMV projected to surpass US$ 195 Billion by 2027 and AI-enabled supply chains capable of reducing logistics costs by up to 15%.

Leading players include DHL Supply Chain, Kuehne+Nagel, DB Schenker (DSV), A.P. Moller Maersk, C.H. Robinson, XPO, GXO Logistics, J.B. Hunt, FedEx, UPS, CEVA Logistics, and Nippon Express Holdings.