- Pharmaceuticals

- Radiodermatitis Market

Radiodermatitis Market Size, Share, and Growth Forecast, 2026 - 2033

Radiodermatitis Market by Product Type (Topical Agents, Dressings, Oral Medications), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), End-user (Hospitals, Oncology Centers, Home Care Settings, Others), and Regional Analysis for 2026 - 2033

Radiodermatitis Market Share and Trends Analysis

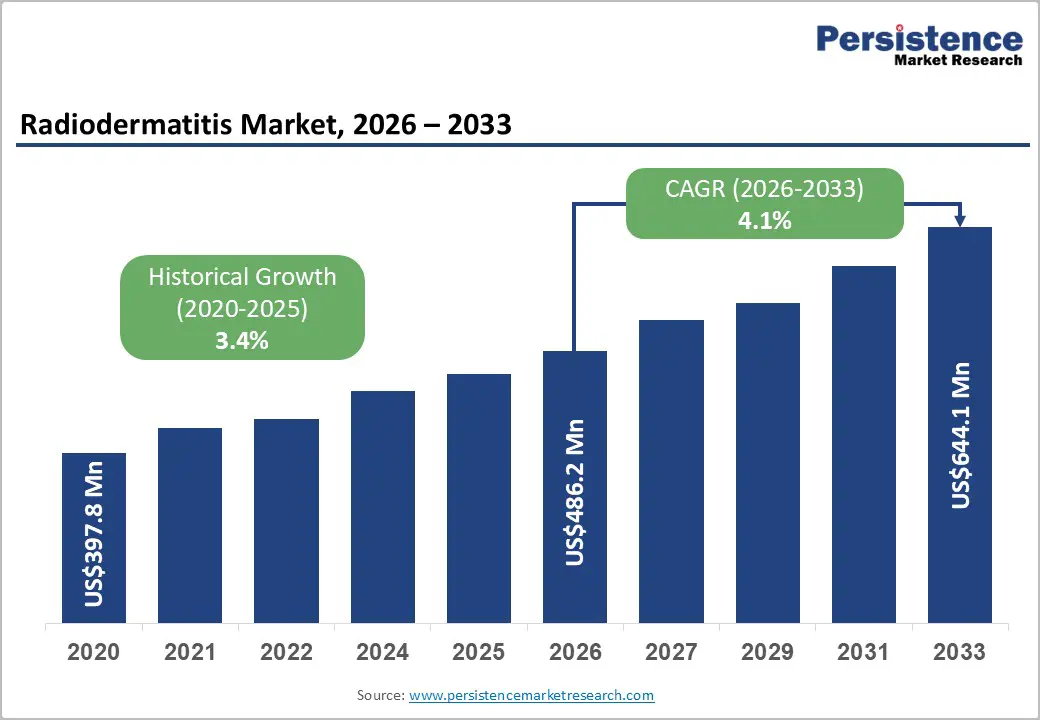

The global radiodermatitis market size is likely to be valued at US$486.2 million in 2026 and is estimated to reach US$644.1 million by 2033, growing at a CAGR of 4.1% during the forecast period from 2026 to 2033, driven by increasing utilization of radiation therapy in cancer management, rising cancer incidence, and expanding adoption of evidence-based skin care interventions.

Growth is supported by a steadily expanding oncology patient population requiring radiation treatment across acute and chronic care settings. Regulatory emphasis on quality-of-life outcomes in cancer care has encouraged wider implementation of supportive care protocols for radiation-induced skin toxicities. Technological advances in wound management products, protective dressings, and topical formulations have improved treatment outcomes and patient adherence.

Key Industry Highlights:

- Leading Product Type: Topical agents is set to hold around 38% revenue share in 2026, driven by established clinical confidence in localized, direct-to-skin therapeutic delivery mechanisms.

- Fastest-Growing Product Type: Dressings is projected as the fastest-growing segment, supported by escalating adoption of moisture-balancing, atraumatic wound management technologies within advanced oncology networks.

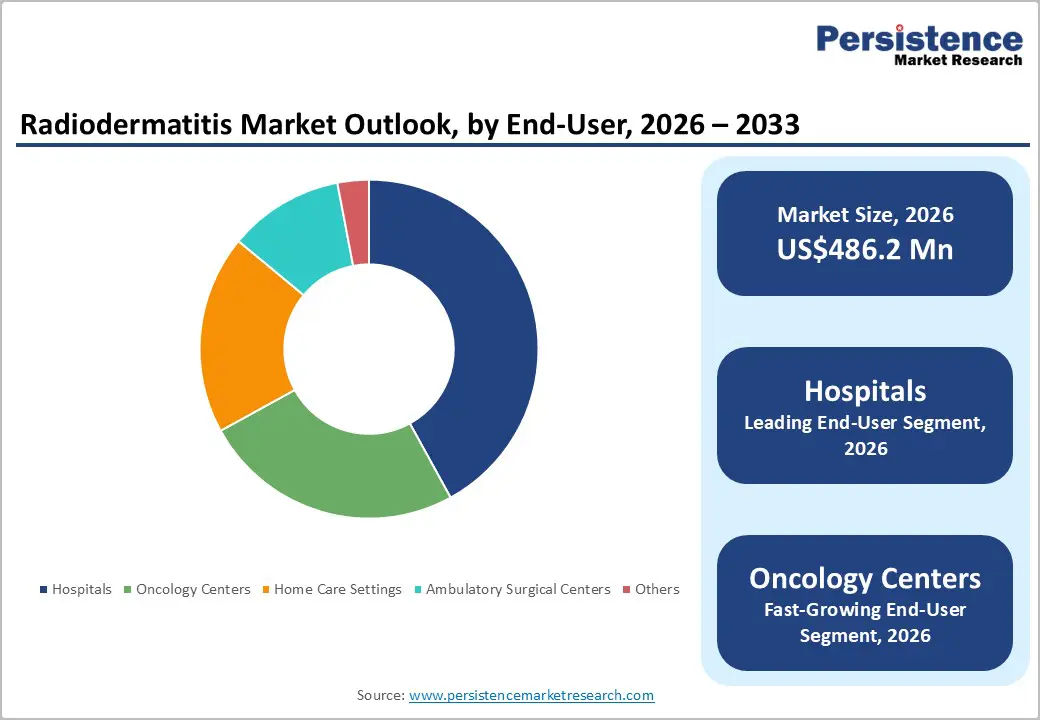

- Leading End-user: Hospitals is estimated to hold roughly 42% revenue share in 2026, due to the high concentration of advanced linear accelerators and multidisciplinary oncological teams within centralized medical institutions.

- Fastest-Growing End-user: Oncology centers is forecast to record the fastest growth, driven by the global proliferation of dedicated, standalone cancer treatment facilities optimizing specialized outpatient delivery models.

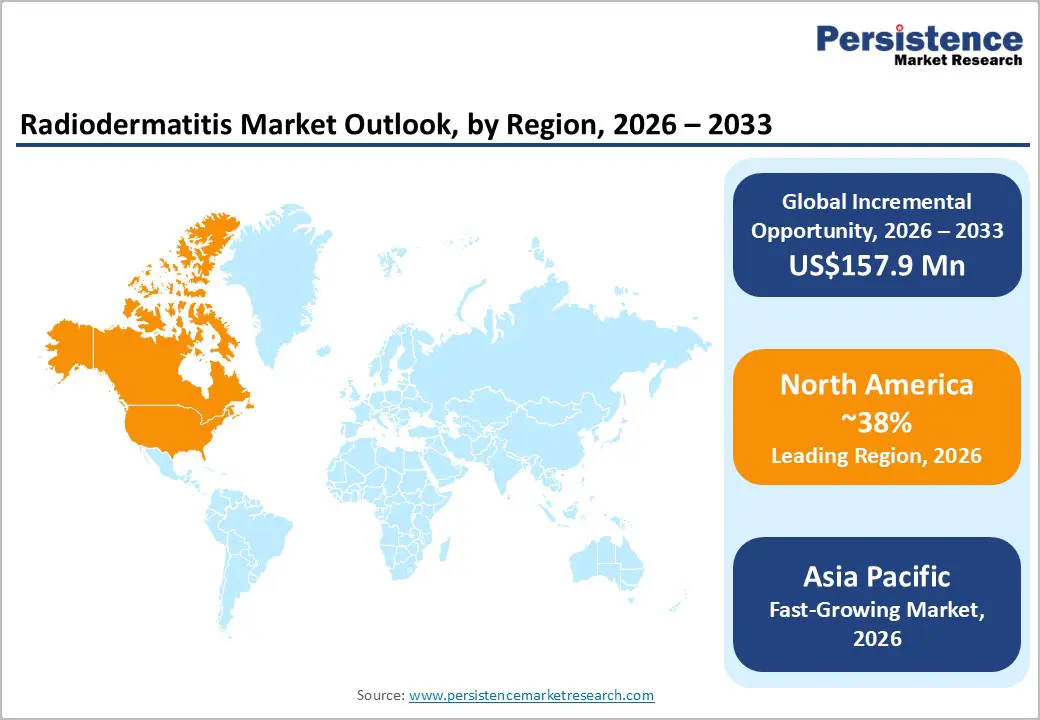

- Regional Leadership: North America is projected to capture roughly 38% market share in 2026, driven by advanced oncology infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as 3M Company and Smith & Nephew plc leveraging scale, supply chain integration, and processing efficiency to maintain competitive positioning.

- Innovation Trends: Technological advancements in bio-inductive formulations, expansion into specialized outpatient distribution networks, and the integration of novel antioxidant components are shaping long-term market evolution and investment direction.

DRO Analysis

Driver - Growing Global Utilization of Radiation Therapy in Cancer Treatment

Radiation therapy remains a fundamental component of modern oncology care, creating a direct increase in demand for interventions that prevent and manage radiation-induced skin damage. Expanding cancer diagnosis rates across aging populations have increased treatment volumes in hospitals and specialized oncology centers. Clinical guidelines increasingly recommend proactive skin management protocols, resulting in greater adoption of topical agents, dressings, and supportive care products throughout radiation treatment pathways.

According to the National Cancer Institute, approximately 50% of cancer patients receive radiation therapy during the course of treatment, highlighting the scale of exposure to radiation-related skin complications during 2025. Rising treatment intensity and longer treatment cycles contribute to higher incidences of skin reactions. Increased awareness among clinicians regarding treatment continuity and patient comfort is encouraging routine incorporation of supportive dermatological products into oncology care frameworks.

Restraint - Limited Standardization of Clinical Management Protocols

Variation in clinical practice patterns across healthcare institutions creates challenges in treatment selection and procurement planning. Differences in physician preferences, institutional guidelines, and reimbursement structures limit uniform adoption of specific products. Such variability reduces predictability in purchasing behavior and complicates commercialization strategies for manufacturers seeking broader market penetration.

Lack of universally accepted treatment pathways increases the need for clinician training and evidence generation. Product differentiation often requires extensive clinical validation, increasing development and marketing expenses. These factors place pressure on operating margins and limit scalability, particularly for smaller suppliers attempting to establish a competitive presence across multiple healthcare systems.

Opportunity - Development of Evidence-Based Advanced Skin Protection Solutions

Growing clinical focus on patient-reported outcomes creates opportunities for next-generation products capable of reducing radiation-induced skin complications. Manufacturers can invest in advanced dressings, bioactive formulations, and protective barrier technologies supported by robust clinical evidence. Stronger efficacy data can facilitate inclusion in institutional treatment protocols and improve adoption among oncology professionals.

Innovation pathways aligned with supportive care objectives enable differentiation in a competitive healthcare environment. Partnerships between healthcare providers, research institutions, and product developers can accelerate clinical validation and commercialization. Regulatory interest in improving quality-of-life outcomes within cancer treatment programs further supports adoption of innovative solutions that demonstrate measurable improvements in skin health and treatment adherence.

Category-wise Analysis

Product Type Insights

Topical agents are anticipated to secure around 38% of the radiodermatitis market share in 2026, reflecting established clinical confidence in localized, direct-to-skin therapeutic delivery mechanisms. These formulations provide immediate hydration and anti-inflammatory relief to irradiated tissues. Clinicians frequently prescribe low-potency corticosteroid creams to mitigate early-stage erythema in breast cancer patients. The high volume of routine prescriptions for moisturizing lotions ensures steady baseline sales across all healthcare tiers.

Dressings are expected to be the fastest-growing segment, propelled by escalating adoption of moisture-balancing, atraumatic wound management technologies within advanced oncology networks. These advanced matrix structures absorb excessive exudate while preventing secondary bacterial contamination. Utilizing soft silicone-coated foam sheets on fragile head and neck cancer wounds minimizes pain during dressing changes. The accelerating clinical transition toward non-adherent dressings reduces the incidence of mechanical skin tearing.

Distribution Channel Insights

Hospital pharmacies are poised to dominate with a forecast market share of over 45% in 2026, powered by close integration with centralized clinical oncology departments and immediate inpatient treatment access. These internal pharmacies stock specialized, high-potency therapeutics and specialized dressings mandated by immediate institutional care pathways. A patient finishing a radiation fraction for pelvic malignancy receives immediate access to prescribed hydrogels prior to hospital discharge. Direct alignment with institutional formularies guarantees dominant volume share for hospital-contained distribution networks.

Online pharmacies are estimated to be the fastest-growing segment, fueled by rising home-care management trends and the convenience of automated prescription renewal services for long-term convalescing patients. Digital platforms allow homebound individuals to acquire specialized skin care products without traveling to physical brick-and-mortar storefronts. A caregiver managing a family member with chronic radiation-induced skin damage orders specialized barrier films via a smartphone interface. The ongoing expansion of specialized e-commerce infrastructure drives rapid home-delivery adoption.

End-user Insights

Hospitals are likely to be the leading segment with a projected 42% of the radiodermatitis market share in 2026 due to the high concentration of advanced linear accelerators and multidisciplinary oncological teams within centralized medical institutions. These acute care hubs process substantial patient volumes requiring complex, high-dose fractional radiation regimens. A tertiary referral hospital treats numerous complex head, neck, and pelvic malignancies daily, generating substantial clinical demand for advanced skincare management systems.

Oncology centers are anticipated to be the fastest-growing segment, fueled by the global proliferation of dedicated, standalone cancer treatment facilities optimizing specialized outpatient delivery models. These specialized clinics streamline therapeutic pathways, offering rapid access to targeted external beam radiation without the administrative overhead of general hospital environments. A localized community oncology clinic integrates standardized skin protection protocols directly into daily breast cancer treatment procedures.

Regional Insights

North America Radiodermatitis Market Trends

North America is expected to lead with an estimated 38% of the global market share in 2026, supported by extensive radiation oncology infrastructure, high cancer treatment volumes, and widespread adoption of supportive care protocols. Expansion of outpatient cancer services is increasing demand for preventive skin management solutions. Product innovation from companies including 3M Company and Smith+Nephew is strengthening clinical adoption.

U.S. Radiodermatitis Market Insights

The U.S. is projected to account for approximately 82% of North America revenue share in 2026, driven by a large radiation therapy patient population and extensive availability of specialized cancer centers. Ongoing investment in oncology infrastructure is expanding treatment capacity. Commercial activity from Mölnlycke Health Care and Convatec Group plc continues to support product availability.

Canada Radiodermatitis Market Insights

Canada is expected to contribute nearly 18% of North American revenue in 2026, supported by expansion of publicly funded oncology services and increasing emphasis on supportive cancer care. Healthcare providers are incorporating structured skin management programs into radiation treatment pathways. Growth in regional cancer treatment capacity is creating opportunities for advanced dressings and topical products. Clinical focus on reducing treatment interruptions is supporting wider product adoption.

Europe Radiodermatitis Market Trends

Europe is forecast to hold approximately 29% of the market share in 2026, supported by established healthcare systems, strong oncology treatment networks, and growing implementation of supportive care guidelines. Rising cancer prevalence is increasing utilization of radiation therapy services. Research collaboration between healthcare institutions and product manufacturers is accelerating adoption of innovative skin management solutions.

Germany Radiodermatitis Market Insights

Germany is likely to represent around 24% of Europe revenue share in 2026, supported by advanced radiotherapy infrastructure and substantial healthcare expenditure. Comprehensive cancer treatment programs increasingly incorporate preventive skin care measures throughout radiation therapy. Demand for clinically validated products is encouraging supplier investment and product innovation.

U.K. Radiodermatitis Market Insights

The U.K. is forecast to account for nearly 18% of Europe revenue share in 2026, driven by modernization of radiotherapy services and continued focus on cancer treatment quality. Healthcare providers are prioritizing interventions that improve patient comfort and treatment adherence. Growth in outpatient oncology services is supporting broader use of topical agents and protective dressings. Clinical guideline implementation remains a key adoption catalyst.

Asia Pacific Radiodermatitis Market Trends

Asia Pacific is forecast to be the fastest-growing market for radiodermatitis, stimulated by an estimated 24% market share in 2026, expanding cancer treatment infrastructure, rising healthcare expenditure, and increasing access to radiation therapy. Government-supported oncology development programs are increasing treatment capacity across major economies. Investments in specialized cancer hospitals and radiotherapy equipment are strengthening demand for supportive skin care products.

China Radiodermatitis Market Insights

China is expected to contribute approximately 36% of Asia Pacific revenue share in 2026, supported by rapid expansion of oncology infrastructure and increasing cancer treatment volumes. Healthcare reforms focused on improving cancer care accessibility are encouraging greater use of supportive therapies. Growth in domestic manufacturing capabilities is improving product availability.

India Radiodermatitis Market Insights

India is projected to account for nearly 19% of Asia Pacific revenue share in 2026, driven by increasing cancer incidence and ongoing expansion of radiation oncology centers. Government initiatives aimed at strengthening cancer treatment access are supporting utilization of supportive care products. Growing awareness regarding radiation-induced skin complications is encouraging preventive treatment adoption.

Competitive Landscape

The global radiodermatitis market is moderately fragmented, characterized by the presence of established wound care manufacturers, dermatology product suppliers, and specialized oncology supportive care companies. Competition is centered on product efficacy, clinical validation, healthcare provider relationships, and distribution network strength. Key participants include 3M Company, Smith+Nephew, Mölnlycke Health Care, Convatec Group plc, and B. Braun SE.

Manufacturers are focusing on advanced dressings, skin barrier technologies, and evidence-based topical formulations to strengthen competitive positioning. Strategic investments in research, regulatory compliance, and healthcare partnerships are supporting product differentiation. Expansion of oncology treatment infrastructure is encouraging suppliers to broaden commercial reach and strengthen engagement with hospitals, oncology centers, and outpatient treatment facilities.

Key Industry Developments:

- In February 2026, La Roche-Posay partnered with the Oncology Nursing Society (ONS) to fund the first skin toxicity photo repository focused on diverse skin tones, strengthening early identification and management of radiation dermatitis and other cancer treatment-related skin toxicities.

Companies Covered in Radiodermatitis Market

- 3M Company

- Smith+Nephew

- Mölnlycke Health Care

- Convatec Group plc

- B. Braun SE

- Coloplast A/S

- Integra LifeSciences

- Cardinal Health

- Medline Industries

- Paul Hartmann AG

- Derma Sciences

- Hollister Incorporated

- Urgo Medical

- Advancis Medical

- Alliqua BioMedical

Frequently Asked Questions

The global radiodermatitis market is projected to reach US$486.2 million in 2026.

Rising utilization of radiation therapy in cancer treatment drives the radiodermatitis market by increasing demand for effective skin toxicity management solutions.

The radiodermatitis market is poised to witness a CAGR of 4.1% from 2026 to 2033.

Expansion of home-based cancer care and development of advanced evidence-based skin protection products create significant market opportunities.

Some of the key market players include 3M Company, Smith+Nephew, Mölnlycke Health Care, Convatec Group plc, and B. Braun SE.