- Pharmaceuticals

- Psoriasis Drugs Market

Psoriasis Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

Psoriasis Drugs Market by Treatment Modality (Biologic Drugs, Others), Drug Class (TNF-α Inhibitors, IL-12/23 Inhibitors, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026 - 2033

Psoriasis Drugs Market Size and Trends Analysis

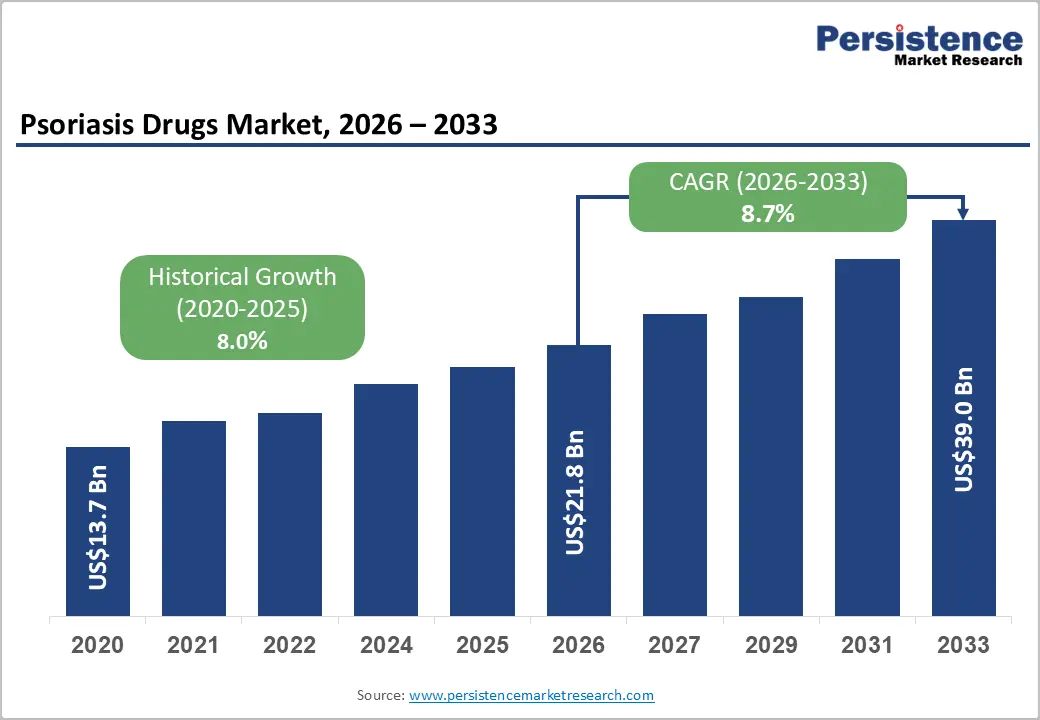

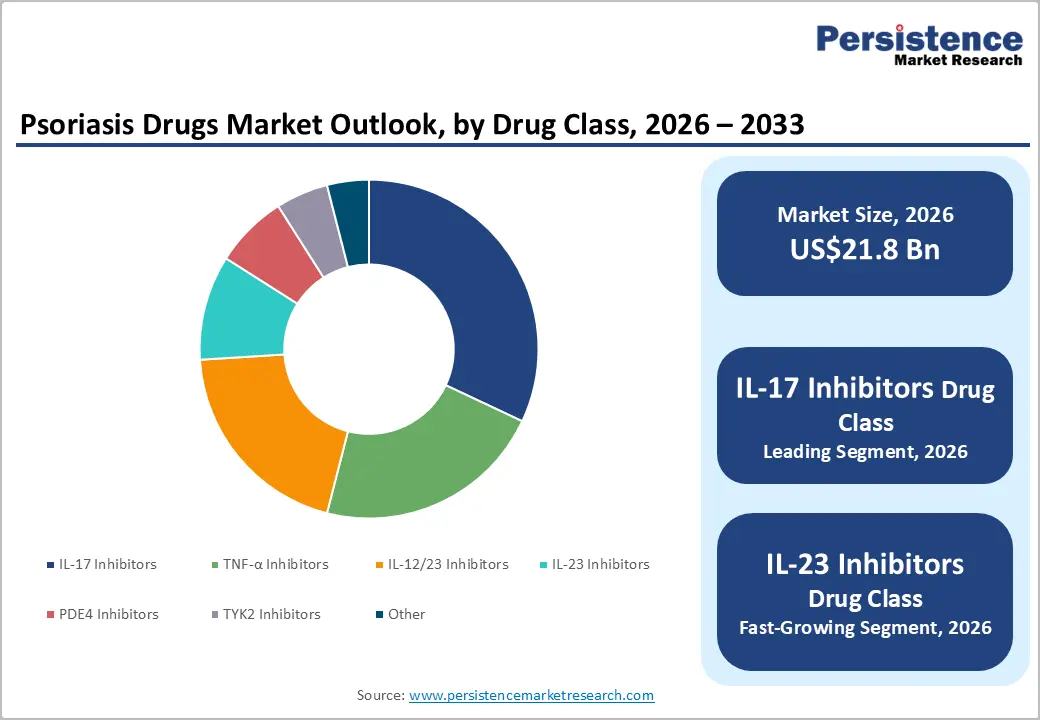

The global psoriasis drugs market size is likely to be valued at US$21.8 billion in 2026, and is expected to reach US$39.0 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2026 to 2033, driven by the increasing adoption of advanced targeted biologic therapies, including monoclonal antibodies and fusion proteins, designed to selectively block cytokine pathways responsible for psoriatic inflammation.

Successive advancements in treatment classes such as TNF-α inhibitors, IL-12/23 inhibitors, IL-17 inhibitors, IL-23 inhibitors, and, more recently, selective TYK2 inhibitors have significantly enhanced clinical outcomes, enabling higher levels of skin clearance, including PASI 90 and PASI 100 responses, that were previously difficult to achieve with traditional systemic therapies.

Key Industry Highlights:

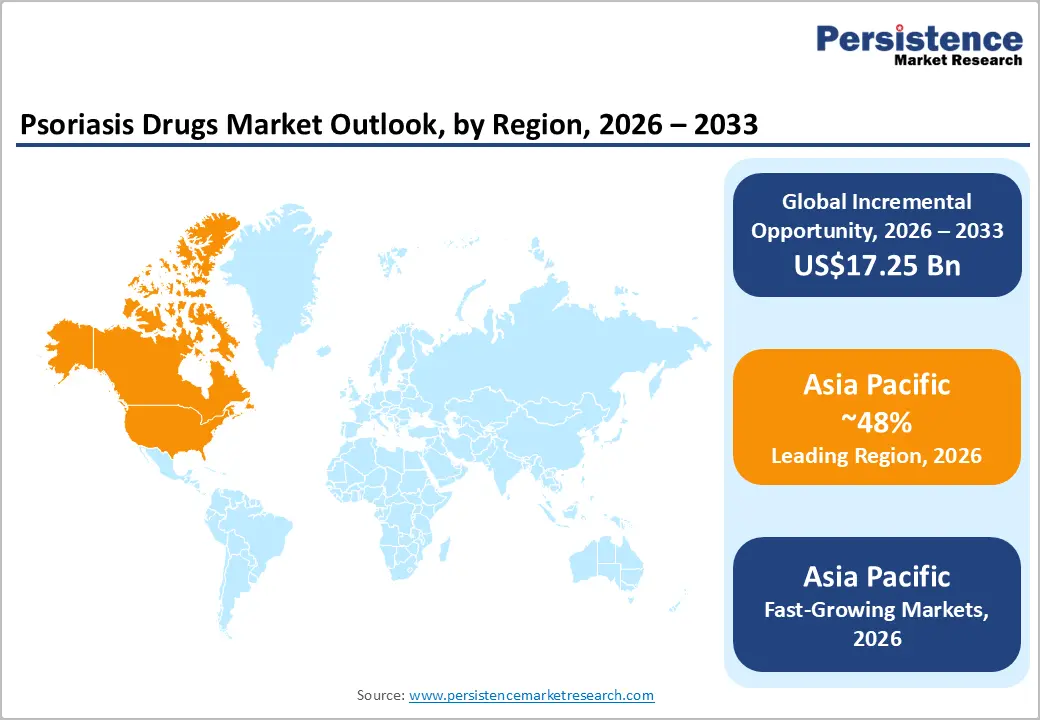

- Dominant Region: North America is expected to dominate with an estimated 48% revenue share in 2026, driven by high psoriasis diagnosis rates, comprehensive biologic therapy reimbursement through commercial and government payers, and the concentrated commercial presence of AbbVie, Johnson & Johnson, Eli Lilly, Amgen, and Bristol Myers Squibb.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing market, driven by rising psoriasis diagnosis awareness, expanding biologic therapy access, growing pharmaceutical market penetration in China, India, Japan, and South Korea, and government healthcare investment enabling specialist dermatology service access.

- Leading Treatment Modality: Biologic drugs are expected to dominate with approximately 72% share in 2026, reflecting their established clinical superiority with PASI 90 and PASI 100 response rates significantly exceeding conventional therapies and comprehensive third-party payer reimbursement coverage across major markets for approved biologic psoriasis indications.

- Dominant Drug Class: IL-17 inhibitors are expected to dominate the psoriasis drugs market with a 38% share in 2026, driven by rapid efficacy, high skin-clearance rates, strong safety profiles, and widespread adoption across major global markets.

DRO Analysis

Driver - Biologic Therapy Innovation and the TYK2/IL-23 Inhibitor Pipeline Driving Premium Revenue Growth

Advancements in biologic therapies, particularly those targeting the IL-23/Th17 pathway and the emerging TYK2 inhibition mechanism, are transforming the psoriasis drugs market by offering superior efficacy, prolonged remission periods, and improved safety profiles compared to conventional systemic treatments. IL-23 inhibitors, including guselkumab, risankizumab, and tildrakizumab, provide sustained skin clearance with less frequent dosing schedules, which enhances patient adherence and supports higher-value treatment adoption.

At the same time, TYK2 inhibitors such as deucravacitinib are introducing a targeted oral treatment option that fills the gap between traditional small-molecule therapies and injectable biologics, thereby improving accessibility for patients with moderate-to-severe plaque psoriasis. The expanding pipeline of next-generation biologics is increasing market competition while broadening the treatable patient population through earlier therapeutic intervention. Collectively, these innovations are shifting treatment strategies toward long-term disease management and sustained disease control rather than temporary symptom relief.

Restraint - Biosimilar Erosion of Mature Biologic Revenue and Market Exclusivity Loss

The gradual loss of patent exclusivity for first- and second-generation biologic therapies used in psoriasis treatment is leading to sustained revenue declines for originator pharmaceutical companies as biosimilar competition intensifies, fundamentally reshaping the economics of the psoriasis drugs market. With several major biologics moving beyond patent protection, biosimilars are gaining market share by delivering comparable clinical outcomes at lower treatment costs, thereby increasing pricing pressure across the therapeutic category.

This trend is especially visible in tumor necrosis factor (TNF-α) inhibitor therapies, where established blockbuster drugs have witnessed considerable patient and prescription shifts toward biosimilar alternatives in both developed and emerging markets. Although originator companies are mitigating some of the impact through the introduction of newer biologics and advanced therapies with differentiated mechanisms of action, the market is steadily transitioning toward more cost-effective treatment options. As a result, healthcare providers and payers are increasingly incorporating biosimilars into treatment guidelines and reimbursement frameworks, further accelerating competitive substitution across the market.

Opportunity- Combination Regimens and Personalized Medicine Expanding Treatment Optimization

The increasing clinical adoption of combination therapy strategies involving biologic agents alongside topical treatments, phototherapy, or oral small-molecule therapies, as well as the growing integration of precision medicine approaches in psoriasis care, is creating significant opportunities for market expansion by increasing treatment duration and per-patient drug utilization. Treatment guidelines from organizations such as the National Psoriasis Foundation Medical Board and the American Academy of Dermatology (AAD) are progressively supporting combination therapy approaches for patients who show inadequate response to biologic monotherapy or who present with comorbid psoriatic arthritis requiring broader immune pathway modulation.

In parallel, pharmacogenomic and biomarker-driven patient stratification is emerging as an important precision medicine opportunity in psoriasis treatment. Genetic, transcriptomic, and immunological profiling techniques are being explored to identify patients most likely to achieve high-level clinical responses, including PASI 90 and PASI 100 outcomes, with specific biologic mechanisms of action. This approach has the potential to optimize therapy selection, reduce the frequency of biologic switching, and enhance both clinical effectiveness and pharmacoeconomic value for healthcare providers and payers.

Category-wise Analysis

Treatment Modality Insights

Biologic drugs are expected to represent the dominant treatment modality, commanding approximately 72% of global revenue in 2026. Pivotal trials demonstrated PASI 90 response rates for IL-17 and IL-23 inhibitors significantly exceeding those achieved with methotrexate in North America and Western Europe.

Small-molecule systemic drugs represent the fastest-growing treatment modality, advancing at an estimated CAGR of 12.0%-14.0% through 2033. The commercial success of Bristol Myers Squibb's Sotyktu (deucravacitinib), the first selective TYK2 inhibitor for moderate-to-severe plaque psoriasis, achieved FDA approval in 2022.

Drug Class Insights

IL-17 inhibitors are anticipated to dominate the drug class market, holding 38% of the total share in 2026, supported by a large and well-established patient base. The category, which includes IL-17A and IL-17A/F inhibitors, continues to hold a leading position in global biologic psoriasis therapy revenues. Their strong market presence is attributed to the rapid onset of action, high levels of skin clearance, and well-established long-term safety profiles, which have driven consistent adoption across North America, Europe, and Asia Pacific.

IL-23 inhibitors represent the fastest-growing drug class. The IL-23 p19 subunit-selective inhibitor class, comprising risankizumab, guselkumab, and mirikizumab, offers the compelling combination of sustained high PASI 100 response rates (complete skin clearance) with infrequent dosing intervals (every 8-12 weeks after induction) that drive superior treatment persistence and patient satisfaction versus agents requiring monthly or more frequent administration.

Distribution Channel Insights

Hospital pharmacies are estimated to dominate the distribution channel, capturing approximately 58% of global revenue in 2026. The channel's dominance reflects the prescribing concentration of biologic psoriasis therapies, which require specialist dermatologist or rheumatologist initiation within hospital outpatient dermatology and rheumatology departments, where integrated patient support programs, laboratory monitoring coordination, and infusion administration services (for intravenous biologics) are centrally managed.

Online pharmacies are likely to be the fastest-growing distribution channel. The expansion of specialty pharmacy home delivery services, including manufacturer-integrated patient support programs (PSPs) that coordinate biologic medication delivery, auto-injection training, adherence monitoring, and insurance authorization support directly to patient homes, is progressively shifting a growing share of biologic psoriasis drug fulfillment from hospital and retail pharmacy settings to direct-to-patient digital distribution channels.

Regional Insights

North America Psoriasis Drugs Market Trends

North America is projected to dominate, holding approximately 48% of total revenue in 2026. The U.S. market is driven by the NPF-estimated 8 million U.S. psoriasis patients, one of the world's highest biologic therapy prescribing rates, comprehensive commercial and Medicare/Medicaid specialty drug coverage for approved biologic psoriasis indications, and the operational headquarters or major commercial presence of AbbVie, J&J, Eli Lilly, Amgen, Bristol Myers Squibb, and Pfizer all of whom maintain flagship biologic psoriasis portfolios with sustained U.S. commercial investment.

U.S. Psoriasis Drugs Market Insights

The U.S. market represents the largest share of the global market, driven by a high diagnosed patient population and widespread access to advanced biologic therapies. Strong reimbursement support from public and private insurers has accelerated the adoption of premium treatments, including IL-17, IL-23, and TYK2-targeted therapies. Continuous product innovation, robust clinical research activity, and the presence of major pharmaceutical manufacturers further strengthen market growth.

Canada Psoriasis Drugs Market Insights

The Canada psoriasis drugs market is characterized by strong access to innovative biologic therapies through a publicly funded healthcare system and provincial drug reimbursement programs. Growing awareness of psoriasis as a chronic immune-mediated disease is supporting earlier diagnosis and treatment initiation. Demand for IL-17 and IL-23 inhibitors continues to rise due to their effectiveness in achieving long-term disease control.

Europe Psoriasis Drugs Market Trends

The Europe psoriasis drugs market is witnessing a shift toward advanced biologic therapies, particularly IL-17 and IL-23 inhibitors, due to their strong efficacy and long-term disease management benefits. Biosimilar adoption continues to expand across the region, increasing treatment accessibility and intensifying pricing competition. Favorable reimbursement policies and established treatment guidelines support the widespread use of innovative therapies.

Germany Psoriasis Drugs Market Trends

Germany represents one of the largest markets in Europe, supported by a well-developed healthcare system and broad access to innovative therapies. The market is experiencing increased adoption of IL-17 and IL-23 inhibitors as physicians prioritize highly effective biologic treatments for moderate-to-severe psoriasis. Biosimilar uptake is also expanding, helping improve treatment accessibility while creating pricing pressure on originator products.

U.K. Psoriasis Drugs Market Trends

The U.K. psoriasis drugs market is increasingly focused on the adoption of advanced biologic therapies, particularly IL-17 and IL-23 inhibitors, for the management of moderate-to-severe psoriasis. National treatment guidelines and reimbursement support are facilitating access to innovative therapies across the healthcare system. Biosimilar penetration continues to grow, helping optimize healthcare spending while expanding patient access to treatment.

Asia Pacific Psoriasis Drugs Market Trends

Asia Pacific is likely to be the fastest-growing regional market, driven by rising psoriasis diagnosis rates as dermatology specialist capacity expands, improving biologic therapy access through government insurance scheme expansion and biosimilar availability, and pharmaceutical company investment in Asia Pacific commercial infrastructure to capitalize on the region's large and growing diagnosed psoriasis patient population.

China Psoriasis Drugs Market Trends

China is the dominant Asia Pacific psoriasis drugs market. The Chinese National Reimbursement Drug List (NRDL) has progressively incorporated biologic psoriasis therapies, including secukinumab and ixekizumab, following National Healthcare Security Administration price negotiation rounds that secured meaningful price reductions from manufacturers in exchange for broad public insurance coverage.

India Psoriasis Drugs Market Trends

India is one of the fastest-growing psoriasis drug markets in Asia Pacific, driven by the country's large psoriasis patient population, predominantly undertreated due to conventional therapy limitations and awareness gaps, combined with the rapidly expanding private dermatology specialist network and growing private health insurance penetration, enabling biologic therapy access among higher-income patient segments.

Competitive Landscape

The global psoriasis drugs market is one of the most commercially competitive specialty pharmaceutical markets, driven by the extraordinary commercial success of biologic therapies and the strategic imperative of every major immunology-focused pharmaceutical company to maintain or build competitive positions in the large and growing psoriasis indication. AbbVie Inc. maintains the strongest overall psoriasis commercial franchise with Skyrizi (risankizumab) achieving US$5.3 billion in 2023 global net revenue and growing rapidly even as Humira biosimilar competition erodes the company's legacy TNF-α inhibitor revenue.

Amgen Inc. participates in the psoriasis drugs market both through its Enbrel (etanercept) franchise, now facing biosimilar headwinds, and through its strategic positioning in the biosimilar dermatology space. Bristol Myers Squibb Company's Sotyktu (deucravacitinib) has emerged as the competitive benchmark for the oral small-molecule psoriasis category, offering an oral tablet once-daily regimen with efficacy challenging established subcutaneous biologics in head-to-head clinical programs.

Key Industry Developments

- In June 2026, Johnson & Johnson announced that the U.S. Food and Drug Administration (FDA) approved ICOTYDE™ (icotrokinra) for the treatment of moderate-to-severe plaque psoriasis in adults and pediatric patients aged 12 years and older weighing at least 40 kg who are eligible for systemic therapy or phototherapy. The company introduced ICOTYDE as the first targeted oral peptide designed to selectively block the IL-23 receptor, expanding treatment options for patients seeking effective non-injectable therapies.

- In December 2025, Sun Pharmaceutical Industries launched Ilumya in India for the treatment of moderate-to-severe plaque psoriasis. The company reported that clinical studies conducted in India demonstrated significant skin clearance among patients. With this launch, Sun Pharma expanded treatment options for individuals living with psoriasis and strengthened access to an innovative biologic therapy already available in multiple international markets.

Companies Covered in Psoriasis Drugs Market

- AbbVie Inc.

- Johnson & Johnson Services Inc.

- Novartis AG

- Eli Lilly and Company

- Amgen Inc.

- Bristol Myers Squibb Company

- Pfizer Inc.

- Sun Pharmaceutical Industries Ltd.

- Boehringer Ingelheim Intl. GmbH

- Leo Pharma A/S

- Dr. Reddy’s Laboratories Ltd.

- Takeda Pharmaceutical Co. Ltd.

Frequently Asked Questions

The global psoriasis drugs market is projected to reach US$21.8 billion in 2026.

Advancements in IL-23 biologics and TYK2 inhibitors are driving premium revenue growth in the psoriasis drugs market by delivering superior efficacy, longer remission, improved patient adherence, and expanded treatment options.

The psoriasis drugs market is poised to witness a CAGR of 8.7% from 2026 to 2033.

The expanding use of combination therapies and precision medicine approaches is creating significant growth opportunities in the psoriasis drugs market by improving treatment outcomes, optimizing patient selection, and increasing long-term therapy utilization.

Key players include AbbVie Inc., Johnson & Johnson Services Inc., Novartis AG, Eli Lilly and Company, Amgen Inc., Bristol Myers Squibb Company, Pfizer Inc., Sun Pharmaceutical Industries Ltd., and Boehringer Ingelheim Intl. GmbH, Leo Pharma A/S, Dr. Reddy's Laboratories Ltd., and Takeda Pharmaceutical Co. Ltd.