- Biotechnology

- Proteomics Market

Proteomics Market Size, Share and Growth Forecast, 2026 - 2033

Proteomics Market by Offering (Instruments, Reagents & Consumables, Software & Bioinformatics, Services), Technology (Mass Spectrometry, Others), Application (Drug Discovery, Clinical Diagnostics, Others), and Regional Analysis for 2026 - 2033

Proteomics Market Share and Trends Analysis

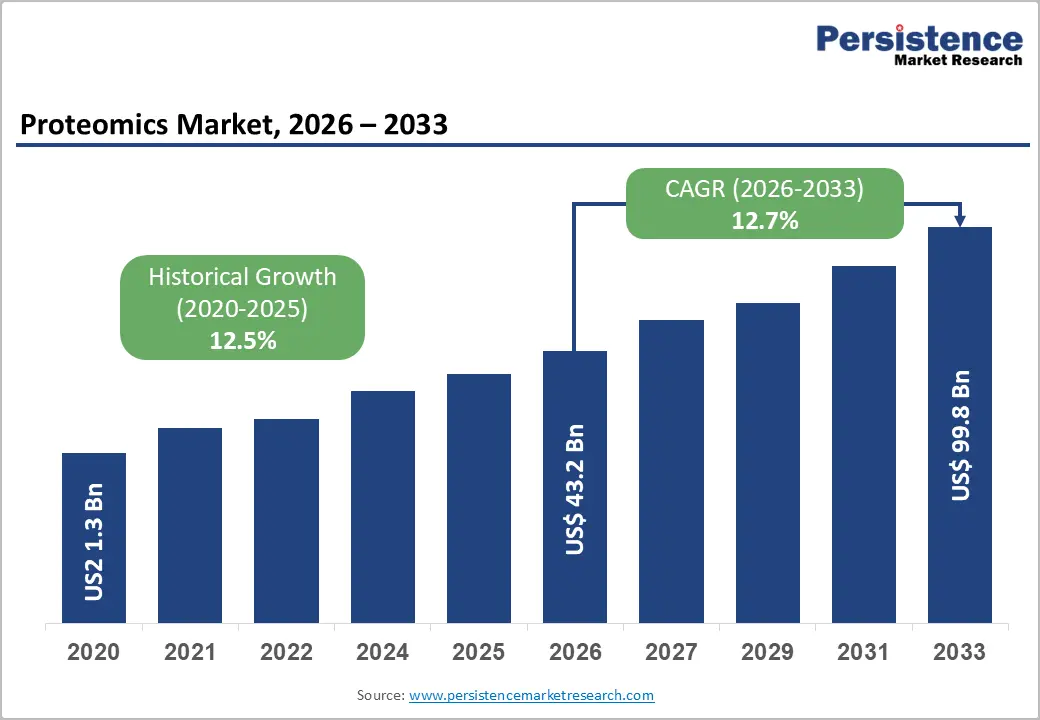

The global proteomics market size is likely to be valued at US$43.2 billion in 2026 and is projected to reach US$99.8 billion by 2033, growing at a CAGR of 12.7% during the forecast period from 2026 to 2033, driven by the rising adoption of proteomics market technologies in pharmaceutical research, biomarker discovery, and precision therapeutics.

Increasing investments in mass spectrometry, AI-enabled protein analytics, and multi-omics research are strengthening demand across biopharmaceutical and academic sectors. In addition, expanding clinical diagnostics applications and government-supported precision medicine initiatives are accelerating the adoption of precision medicine proteomics solutions across global healthcare markets.

Key Industry Highlights:

- Dominant Offering Segment: Instruments are set to command nearly 39% of the market share in 2026, while software & bioinformatics solutions are projected to grow the fastest at 13.1% CAGR through 2033, driven by rising adoption of AI-based proteomics analytics.

- Leading Technology Segment: Mass spectrometry is anticipated to lead with approximately 42% revenue share in 2026, while protein microarrays are likely to register the fastest growth at 12.9% CAGR during 2026 - 2033 due to expanding biomarker screening applications.

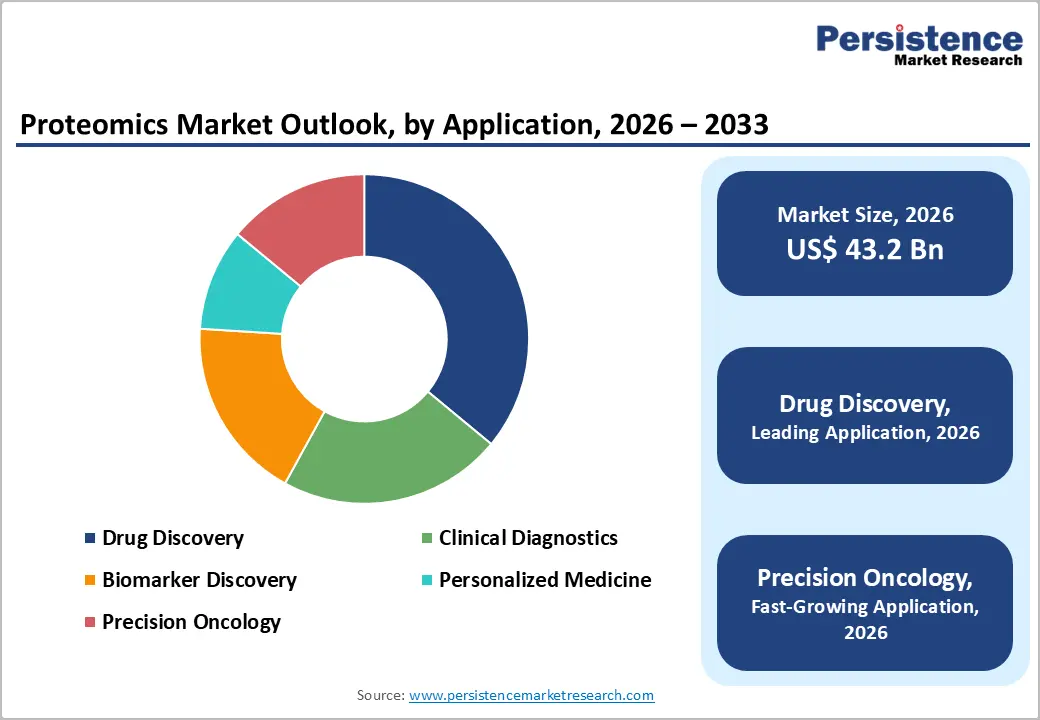

- Dominant Application Area: Drug discovery is projected to remain the leading application segment in 2026, while precision oncology is expected to grow the fastest at 13.5% CAGR through 2033, supported by increasing adoption of precision medicine proteomics solutions.

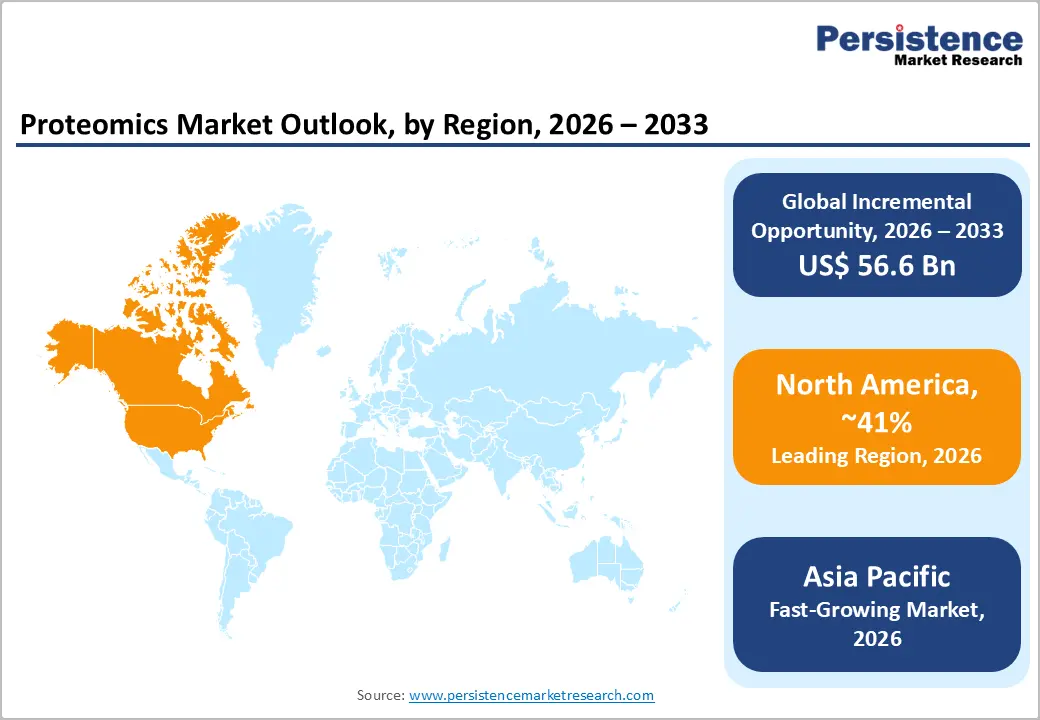

- Regional Leadership: North America is poised to account for nearly 41% of global revenue in 2026, while Asia Pacific is projected to witness the fastest expansion at 13.8% CAGR through 2033, driven by rising biotechnology and pharmaceutical investments.

- Competitive Environment: Competitive dynamics are centered on advanced mass spectrometry launches, AI-enabled proteomics collaborations, and expansion of spatial proteomics capabilities across the global proteomics industry.

DRO Analysis

Driver - Precision medicine and proteomics innovation driving market growth

The increasing use of proteomics technologies in personalized therapeutics and biomarker-driven clinical research remains a major growth driver for the market. Organizations such as the U.S. National Institutes of Health (NIH) and the European Medicines Agency (EMA) continue to support translational medicine and protein biomarker programs. Initiatives, including the NIH All of Us Research Program and Cancer Moonshot, are accelerating oncology-focused protein profiling applications. Pharmaceutical companies are also expanding proteomics in drug discovery workflows to improve target validation and therapeutic development efficiency.

The rising startup activity and strategic funding are advancing next-generation proteomics technologies. Companies are investing in ultra-sensitive protein analysis, AI-driven multi-omics platforms, and single-cell proteomics capabilities to improve research precision. Recent funding rounds by Alamar Biosciences, Syncell, Pluto Bio, and Age Labs highlight growing investor confidence in innovative proteomics solutions. These developments are strengthening the adoption of clinical proteomics market trends across the pharmaceutical, biotechnology, and academic research sectors.

Restraint - High infrastructure costs and workflow complexity are limiting the adoption

The market continues to face challenges linked to high capital investment and operational complexity. Advanced mass spectrometry systems, chromatography instruments, and proteomic sequencing platforms require specialized infrastructure, skilled professionals, and significant financial resources. Large-scale proteomics workflows also generate complex datasets, increasing reliance on bioinformatics and cloud computing capabilities. These factors continue to restrict adoption among smaller laboratories and emerging research institutions.

In addition, limited workflow standardization remains a major commercialization barrier. Variations in sample preparation, reproducibility, and protein data interpretation continue to create validation challenges across research settings. Regulatory approval processes for proteomics-based diagnostic assays also require extensive clinical evidence and longer timelines. These constraints are particularly significant in developing economies with limited healthcare and research infrastructure.

Opportunity - AI-driven proteomics and innovation, unlocking growth opportunities

The emergence of AI-driven protein analytics and single-cell analysis platforms presents a major market opportunity. Machine learning is improving protein identification accuracy, accelerating biomarker discovery, and enabling predictive disease modeling. Rising investments in AI-based proteomics analytics are strengthening data interpretation across clinical and pharma workflows. Expansion of the single-cell proteomics market is further driving demand across oncology, immunology, and neuroscience applications.

Research agencies such as NIH, Horizon Europe, and AMED are funding single-cell and spatial proteomics programs to advance precision healthcare. Pharma companies are leveraging these technologies for precision oncology and personalized therapies. Recent developments include Nomic Bio’s Omni 1000, Quantum-Si’s Proteus™ platform, and SCIEX’s ZenoTOF 7600+ with strategic collaborations. These innovations highlight strong commercialization potential across instruments, software, and proteomics services.

Category-wise Analysis

Offering Insights

Instruments are anticipated to lead, holding nearly 39% share in 2026, driven by heavy reliance on mass spectrometers, chromatography platforms, and automated protein analyzers in both pharma R&D and academic labs. Their dominance is reinforced by the constant push for higher sensitivity, faster throughput, and deeper proteome coverage in oncology and translational research programs. As precision medicine pipelines scale, demand for robust, high-resolution instrumentation is becoming increasingly non-negotiable.

A notable 2025 move came from Bruker, which upgraded its timsTOF Ultra 2 ecosystem, sharpening ultra-deep proteome mapping for clinical and translational workflows. On the other side, software & bioinformatics, growing at a strong 13.1% CAGR through 2033, is rapidly becoming the “brain layer” of proteomics. In 2026, Waters expanded its cloud-native analytical environment to streamline AI-assisted protein interpretation across biopharma R&D. This shift is accelerating AI-based proteomics analytics, turning raw protein data into faster, decision-ready insights.

Technology Insights

Mass spectrometry is anticipated to dominate, capturing about 42% revenue share in 2026. Its dominance comes from unmatched accuracy in protein identification, quantification, and disease pathway mapping, especially across oncology and immunology research. Continuous upgrades in Orbitrap and time-of-flight systems are pushing analytical boundaries, making it indispensable for next-gen proteomics workflows. In 2025, Shimadzu expanded deployment of its LCMS-8065XE systems across Asia-Pacific research hubs, strengthening high-precision disease profiling capabilities.

Meanwhile, protein microarrays are gaining momentum as the fastest-growing segment at a 12.9% CAGR through 2033, fueled by demand for scalable biomarker screening. In 2026, RayBiotech broadened its multiplex protein array portfolio for autoimmune and oncology applications, accelerating adoption in clinical diagnostics and translational research ecosystems.

Application Insights

Drug discovery is anticipated to lead, contributing nearly 36% of total revenue in 2026, as pharma companies increasingly embed proteomics into every stage of target validation and drug response modeling. This shift is helping reduce late-stage failures while sharpening biologics development pipelines. Proteomics has quietly become a core engine behind smarter, faster therapeutic innovation. In 2025, AstraZeneca deepened its multi-omics discovery initiatives in Cambridge, integrating proteomics-driven target identification into oncology and immunology programs.

Precision oncology, however, is moving fastest at a 13.5% CAGR through 2033, powered by real-world adoption of protein biomarkers in cancer stratification. In 2026, Roche expanded proteomics-based companion diagnostics across Europe, strengthening clinical uptake of precision medicine proteomics solutions and enabling more tailored, data-driven cancer treatment decisions.

Regional Analysis

North America Proteomics Market Trends

North America is estimated to account for nearly 41% of global market revenue in 2026, driven by strong biotech innovation, early precision medicine adoption, and deep integration of Proteomics in drug discovery. The market is reshaping the region into a highly translational ecosystem where biomarker research is rapidly moving from lab to clinic. Expanding use of AI-enabled workflows and advanced mass spectrometry is further strengthening clinical and pharmaceutical applications.

U.S. Proteomics Market Trends

The U.S. is projected to hold around 38% of the North America market in 2026, reflecting its dominance in biotech R&D and clinical proteomics adoption. In 2025-2026, the growing integration of proteomics into oncology diagnostics and drug discovery pipelines is improving treatment precision and accelerating research translation. Increased adoption of AI-based proteomics analytics is also reshaping pharma decision-making and target identification.

Canada Proteomics Market Trends

Canada is estimated to contribute nearly 22% of the regional market in 2026, supported by academic-led innovation and translational healthcare programs. The market is influencing stronger adoption of proteomics in oncology trials and neurodegenerative research. Expanding collaboration between hospitals and biotech firms in 2026 is improving access to advanced protein analysis tools and strengthening precision medicine capabilities.

Europe Proteomics Market Trends

Europe is estimated to account for nearly 29% of global market revenue in 2026, supported by regulatory harmonization and strong clinical research infrastructure. The market is accelerating the adoption of proteomics biomarker discovery, especially in oncology and rare disease research. It is also driving stronger standardization of clinical workflows and increasing cross-border research collaboration across major economies.

Germany Proteomics Market Trends

Germany is expected to hold around 32% of the regional market in 2026, driven by strong pharmaceutical manufacturing and advanced biomedical research ecosystems. In 2025-2026, increasing use of automated proteomics platforms in drug development is improving efficiency in biologics and disease pathway research. The market is reinforcing strong academia-industry integration in high-resolution protein analysis.

U.K. Proteomics Market Trends

The U.K. is projected to account for nearly 24% of the Europe market, supported by NHS-led precision medicine initiatives and strong biotech innovation. The market is driving wider adoption of proteomics in early cancer detection and rare disease diagnostics. In 2026, AI-enabled proteomic platforms are improving diagnostic accuracy and strengthening integration with genomics-based healthcare systems.

Asia Pacific Proteomics Market Trends

Asia Pacific is estimated to represent nearly 23% of global market revenue in 2026, and is the fastest-growing region, driven by rapid pharmaceutical expansion and increasing adoption of Precision medicine proteomics solutions. The market is transforming healthcare systems through improved biomarker-driven diagnostics and rising investment in biotechnology infrastructure. Government support is further accelerating clinical and research adoption.

China Proteomics Market Trends

China is anticipated to hold around 38% of the Asia Pacific market, supported by large-scale biotechnology initiatives and strong government funding. The market is accelerating the integration of proteomics into drug development and cancer research pipelines. In 2026, the rising adoption of AI-based protein analytics is improving research productivity and strengthening translational outcomes.

India Proteomics Market Trends

India is projected to account for nearly 18% of the regional market, driven by expanding clinical research outsourcing and biotech investments. The market is influencing stronger adoption of proteomics in infectious disease surveillance and oncology research. In 2026, CRO-led expansion of proteomics services is improving global clinical trial capabilities and strengthening India’s role in translational research support.

Competitive Landscape

The global proteomics industry is moderately consolidated, with leading players such as Thermo Fisher Scientific, Bruker, Agilent Technologies, Danaher, and Waters Corporation holding a strong revenue share. Their dominance is driven by integrated mass spectrometry platforms, chromatography systems, and end-to-end proteomics workflows. Strong pharma partnerships and lab networks further reinforce their market control. Continuous investment in AI-based proteomics analytics and automation is strengthening their technological leadership.

Alongside these leaders, niche innovators such as Olink, Seer, Standard BioTools, and Biognosys are gaining traction in biomarker discovery and advanced proteomics analytics. These firms are focusing on high-growth areas such as single-cell proteomics and precision oncology applications. In 2025-2026, rising collaborations between biotech firms and pharma companies are expanding their market reach. However, high entry barriers and regulatory complexity continue to limit new entrants while encouraging strategic partnerships and gradual consolidation.

Key Industry Highlights:

- In October 2024, The Human Protein Atlas (HPA) launched version 24 at the HUPO 2024 meeting, introducing a Disease Blood Atlas with data from 59 diseases, including cancers and autoimmune disorders. It also features multiplex tissue profiling, spatial transcriptomics of the brain, and 3D structures of over 80,000 protein isoforms. These updates enhance the HPA's role in advancing precision medicine and biomarker discovery.

- In February 2024, M42 and SomaLogic launched the first-ever proteomics grant competition in the GCC, inviting regional researchers to submit innovative proposals utilizing SomaLogic's SomaScan® Assay for advanced protein analysis.

Companies Covered in Proteomics Market

- Thermo Fisher Scientific

- Bruker Corporation

- Agilent Technologies

- Danaher Corporation

- Waters Corporation

- Bio-Rad Laboratories

- PerkinElmer

- Shimadzu Corporation

- Sartorius AG

- QIAGEN

- Illumina

- Seer

- Olink Holding AB

- Standard BioTools

Frequently Asked Questions

The global proteomics market is projected to reach US$43.2 billion in 2026.

Rising adoption of precision medicine, biomarker-based research, and proteomics in drug discovery drives market growth.

The proteomics market is expected to grow at a CAGR of 12.7% from 2026 to 2033.

Growth opportunities emerge from AI-based proteomics analytics, single-cell technologies, and the expansion of clinical applications.

Key players include Thermo Fisher Scientific, Bruker Corporation, Agilent Technologies, Danaher Corporation, and Waters Corporation.