- Executive Summary

- Global Pregelatinized Flour Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Product Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Pregelatinized Flour Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

- Global Pregelatinized Flour Market Outlook: Source

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Source, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Attractiveness Analysis: Source

- Global Pregelatinized Flour Market Outlook: Nature

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Nature, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Attractiveness Analysis: Nature

- Global Pregelatinized Flour Market Outlook: End Use-Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End Use-Application, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis: End Use-Application

- Key Highlights

- Global Pregelatinized Flour Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Pregelatinized Flour Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Source

- By Nature

- By End Use-Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis

- Europe Pregelatinized Flour Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Source

- By Nature

- By End Use-Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis

- East Asia Pregelatinized Flour Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Source

- By Nature

- By End Use-Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis

- South Asia & Oceania Pregelatinized Flour Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Source

- By Nature

- By End Use-Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis

- Latin America Pregelatinized Flour Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Source

- By Nature

- By End Use-Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis

- Middle East & Africa Pregelatinized Flour Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Source

- By Nature

- By End Use-Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Source, 2026-2033

- Wheat

- Corn

- Rice

- Rye

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Nature, 2026-2033

- Organic

- Conventional

- Market Size (US$ Bn) Analysis and Forecast, By End Use-Application, 2026-2033

- Food

- Bakery & Confectionery

- Dairy Alternatives

- Soups and Sauces

- Others

- Pet Food

- Industrial

- Food

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- ADM

- Overview

- Segments and Product Types

- Key Financials

- Market Developments

- Market Strategy

- Molendum Ingredients

- Mennel

- AGRANA Beteiligungs-AG

- Briess Malt & Ingredients

- Kröner-Stärke GmbH

- Sage V Foods, LLC

- LifeLine Foods

- Codrico Rotterdam BV

- Didion Inc.

- Caremoli Group

- Bunge

- Belourthe Group

- Crespel & Deiters GmbH & Co. KG

- Associated British Foods

- NorQuin

- Zippy Edible Products Pvt Ltd

- Others

- ADM

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Food Ingredients & Additives

- Pregelatinized Flour Market

Pregelatinized Flour Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Pregelatinized Flour Market by Source (Wheat, Corn, Rice, Rye, Others), Nature (Organic, Conventional), End Use-Application (Food, Pet Food, Industrial), and Regional Analysis from 2026 to 2033

Key Industry Highlights

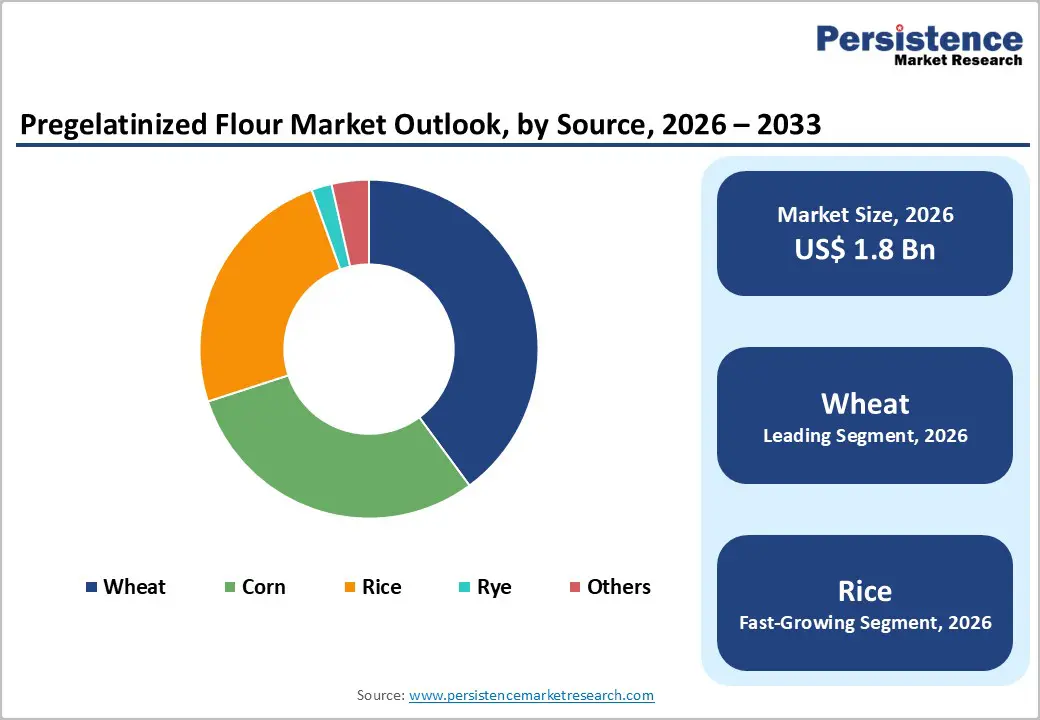

- Dominant Segment: Wheat-based pregelatinized flour held the largest share 39.9% in 2025, driven by its wide use in bakery, convenience, and processed foods.

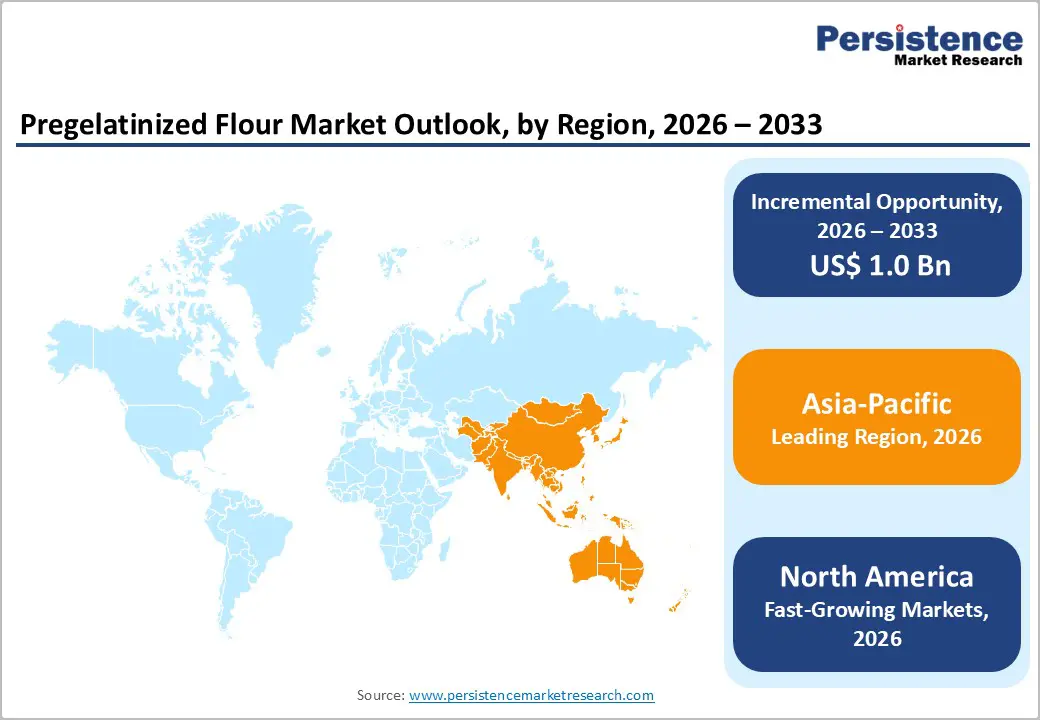

- Dominant Region: Asia-Pacific led the market in 2025 with 32.7% share, supported by expanding food processing industries, rising urbanization, increasing demand for convenience foods, and growing adoption of clean-label and gluten-free products.

- Growth Indicators: Growth is driven by rising demand for convenience and gluten-free foods, clean-label trends, expanding processed food industries, and increasing urbanization in emerging markets.

- Market Opportunity: Opportunities exist in organic and specialty flours, expansion in Asia-Pacific and Latin America, product innovation for functional foods, and increasing adoption in industrial applications.

| Key Insights | Details |

|---|---|

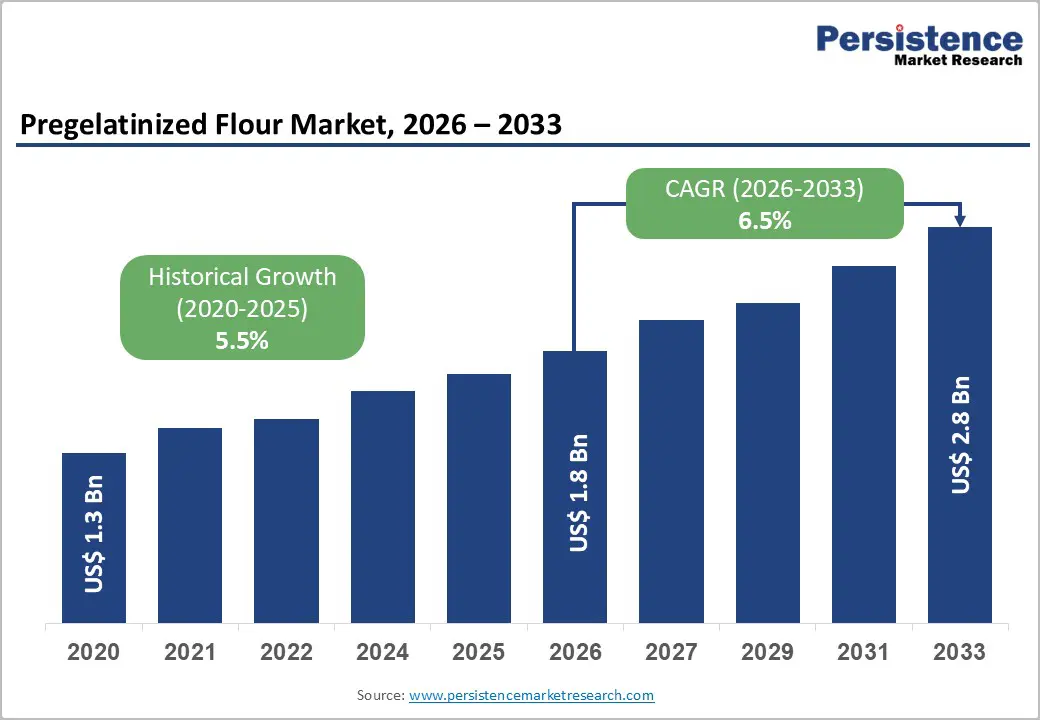

| Global Pregelatinized Flour Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Dynamics

Driver: Increasing popularity of gluten-free and clean-label products

The demand for gluten-free and clean-label products has risen sharply as consumers prioritize digestive health and transparency in ingredient lists. Data on the global gluten-free products market shows it was valued at approximately USD 8.5 billion in 2025 and is projected to nearly double by 2033 with a CAGR exceeding 10%, reflecting strong growth in gluten-free demand across food categories. In the U.S., the gluten-free sector alone is expected to grow at a ~9.7% CAGR through 2030, indicating that consumers are increasingly choosing foods perceived as healthier or containing fewer allergens. This trend is tightly linked to awareness of gluten-related disorders such as celiac disease and non-celiac gluten sensitivity, alongside broader lifestyle and wellness motives in developed markets.

For pregelatinized flour, this shift matters because pregelatinized wheat, corn, rice, and other grain flours are foundational ingredients in gluten-free baked goods, snacks, and convenience foods seeking clean-label positioning. Consumers seeking gluten-free alternatives often evaluate ingredients for simplicity and natural composition, thereby increasing demand for flours that can deliver texture and functionality without gluten. Manufacturers respond by reformulating products to incorporate rice-, corn, or alternative plant-based pregelatinized flours that support clean-label claims, boosting market penetration. Overall, the rising popularity of gluten-free and clean-label products is a structural demand driver for pregelatinized flour usage in mainstream food applications.

Restraint: Price volatility due to climate and crop yield fluctuations

Agricultural price volatility significantly affects the cost and supply of raw materials used in flour production, including wheat, corn, and rice. Research into global grain markets shows that climate variability—such as extreme temperature shifts and irregular precipitation patterns—can lead to unpredictable crop yields year-to-year, influencing commodity prices and input costs for downstream markets. Although long-term trends in price volatility have mixed empirical support, some studies identify a slight upward trend in volatility for major grains like wheat over historical periods, suggesting continuing sensitivity to climatic factors. Climatic drivers such as droughts or heatwaves can reduce yields and trigger price spikes, complicating procurement planning for food producers.

For the pregelatinized flour market, such price volatility raises operational risks because production costs are tied directly to raw grain prices. Fluctuating prices for wheat, rice, or corn can compress margins or necessitate passing cost increases to customers, which may limit adoption in price-sensitive segments or slow market expansion in developing regions. Additionally, when commodity prices are unstable, both small and large millers may be reluctant to expand capacity, preferring to hedge risk rather than invest in new pregelatinization technologies. This restraint is compounded in markets where farmers lack robust risk-management tools or governmental support schemes that stabilize income, making price volatility a significant constraint on predictable market growth.

Opportunity: Development of organic and specialty pregelatinized flours

The food industry’s shift toward natural, minimally processed, and specialty ingredients presents a significant opportunity for organic and niche pregelatinized flours. Although concrete government data on pregelatinized flour itself is limited, trends in related gluten-free and specialty flour markets show consumers increasingly value products that offer both allergen-free attributes and clean-label certification. For example, the gluten-free flours segment was valued at billions and expanding as manufacturers innovate with alternative grain bases to meet diverse dietary needs. This trend highlights an appetite for differentiated flour products that can command higher price premiums and expand usage in premium bakery, snack, and convenience categories.

Organic and specialty pregelatinized flours, such as those derived from heirloom rice, quinoa, sorghum, or ancient grains can capitalize on this demand by providing both functional benefits (e.g., improved texture, instantization) and marketing appeal to health-conscious consumers. Advances in processing technologies also make it feasible to produce specialty variants that meet specific nutritional or functional requirements, such as low glycemic index or high fiber. As consumer interest grows for organic and ethically sourced food ingredients, producers who expand offerings in this segment can differentiate their value proposition, secure premium pricing, and capture share in emerging markets where specialty diets are gaining traction.

Category-wise Analysis

By Source Insights

Wheat’s dominance in the pregelatinized flour market is grounded in its global production scale and functional versatility. According to the UN Food and Agriculture Organization (FAOSTAT), global wheat production exceeded 780 million tonnes in 2024, making it one of the world’s most cultivated grains. Its wide availability helps ensure consistent supply and stable pricing, which supports large-scale processing into value-added flours. Wheat’s gluten properties also enhance texture, binding, and volume in bakery and convenience foods, making pregelatinized wheat flour attractive for formulators seeking functional performance. Additionally, wheat is a staple in regions with high processed food consumption, such as North America and Europe, further reinforcing its use. This extensive production and functional utility justify wheat’s leading share in the pregelatinized flour market.

By Nature Insights

Conventional pregelatinized flour dominates the market due to its mass availability, lower cost, and established supply chains. Government agricultural data shows that most cereal grains, wheat, maize, and rice are produced through conventional farming; for instance, the US Department of Agriculture (USDA) reported in 2025 that organic accounted for only ~1.7% of total U.S. cropland. This disparity means bulk conventional flour is far more accessible and cost-effective for food manufacturers. Conventional production also benefits from mechanized inputs and optimized yields, which reduce upstream costs. Since pregelatinized flour is a key functional ingredient in high-volume applications like bakery and snacks, price sensitivity favors conventional sourcing. These supply and cost dynamics explain why conventional varieties dominate the pregelatinized flour market.

Regional Insights

Asia Pacific Pregelatinized Flour Market Trends

Asia Pacific’s dominance is rooted in its large population base and expanding food processing industry. According to the Food and Agriculture Organization (FAOSTAT), Asia accounts for over 60% of global rice production and a significant share of wheat and maize output, underlying vast raw material availability for pregelatinized flour. Rapid urbanization in countries like China and India, where the UN estimates urban populations will exceed 50% by 2030 has driven demand for convenience and processed foods that use pregelatinized flour for texture and shelf-life. Government policies in China and India also support food processing growth through incentives and infrastructure development. These demographic and industry fundamentals make Asia Pacific the largest regional market.

Europe Pregelatinized Flour Market Trends

Europe holds strategic importance due to high food safety standards and diversified food industrialization. The European Commission’s agricultural statistics show the EU produces over 140 million tonnes of cereals annually, providing robust raw material supply. European consumers also have strong demand for high-quality bakery, convenience, and specialty foods, which drives formulation innovation. The EU’s strict food regulations (e.g., Regulation (EC) No 178/2002 on food safety) require transparent ingredient usage, which supports the adoption of standardized pregelatinized flours. Additionally, Europe’s food processing sector is one of the largest globally, contributing over €700 billion in output, indicating significant application demand. These structural strengths make Europe a key regional market.

North America Pregelatinized Flour Market Trends

North America’s rapid growth is propelled by high consumption of convenience foods and strong industrial demand. The U.S. Department of Agriculture (USDA) reports that Americans spent over 60% of their food dollars on food away from home and convenience products, highlighting robust demand for ingredients like pregelatinized flour that enhance texture and processing performance. The region also has a large, modern food processing industry—the USDA notes food manufacturing is the second-largest industrial sector in the U.S., with an output exceeding $800 billion. Rising consumer interest in gluten-free and functional foods further fuels product reformulation. This combination of consumption patterns, industrial scale, and innovation underpin North America’s fast growth. Market

Competitive Landscape

The pregelatinized flour market is competitive, led by major players focusing on product innovation, quality, and functional applications. Companies prioritize expanding production capacity, developing specialty and organic flours, ensuring regulatory compliance, and strengthening distribution networks to meet rising demand in bakery, convenience, and processed food industries globally.

Key Industry Developments:

- In November 2025, KRÖNER-STÄRKE unveiled its next-generation clean-label solutions at Fi Europe 2025, showcasing advanced functional ingredients tailored for modern food processing needs. The company highlighted innovations designed to support cleaner ingredient lists, improved texture, and enhanced processing performance, reflecting rising industry demand for transparency and health-oriented food solutions at the event.

- In October 2025, ADM advanced its quality and testing capabilities by opening a new Central Milling Laboratory. The facility was established to enhance research, product development, and quality assurance for grains and flours. ADM’s new laboratory aims to support innovation in milling processes, improve product consistency, and meet growing industry demand for high-quality, functional ingredients.

Companies Covered in Pregelatinized Flour Market

- ADM

- Molendum Ingredients

- Mennel

- AGRANA Beteiligungs-AG

- Briess Malt & Ingredients

- Kröner-Stärke GmbH

- Sage V Foods, LLC

- LifeLine Foods

- Codrico Rotterdam BV

- Didion Inc.

- Caremoli Group

- Bunge

- Belourthe Group

- Crespel & Deiters GmbH & Co. KG

- Associated British Foods

- NorQuin

- Zippy Edible Products Pvt Ltd

- Others

Frequently Asked Questions

The global pregelatinized flour market is projected to be valued at US$ 1.8 Bn in 2026.

Rising demand for convenience foods, gluten-free products, clean-label trends, and expanding processed food industries.

The global pregelatinized flour market is poised to witness a CAGR of 6.5% between 2026 and 2033.

Growth in organic and specialty flours, emerging markets, functional food applications, and industrial product innovation.

ADM, Molendum Ingredients, Mennel, AGRANA Beteiligungs-AG, Briess Malt & Ingredients, Kröner-Stärke GmbH, Sage V Foods, LLC.