- Pharmaceuticals

- Postoperative Pain Management Market

Postoperative Pain Management Market Size, Share, and Growth Forecast, 2026 - 2033

Postoperative Pain Management Market by Drug Class (Opioids, NSAIDs, Others), Route of Administration (Injectable, Oral, Others), Surgery Type (Orthopedic, Cardiovascular & Thoracic, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

Postoperative Pain Management Market Size and Trends Analysis

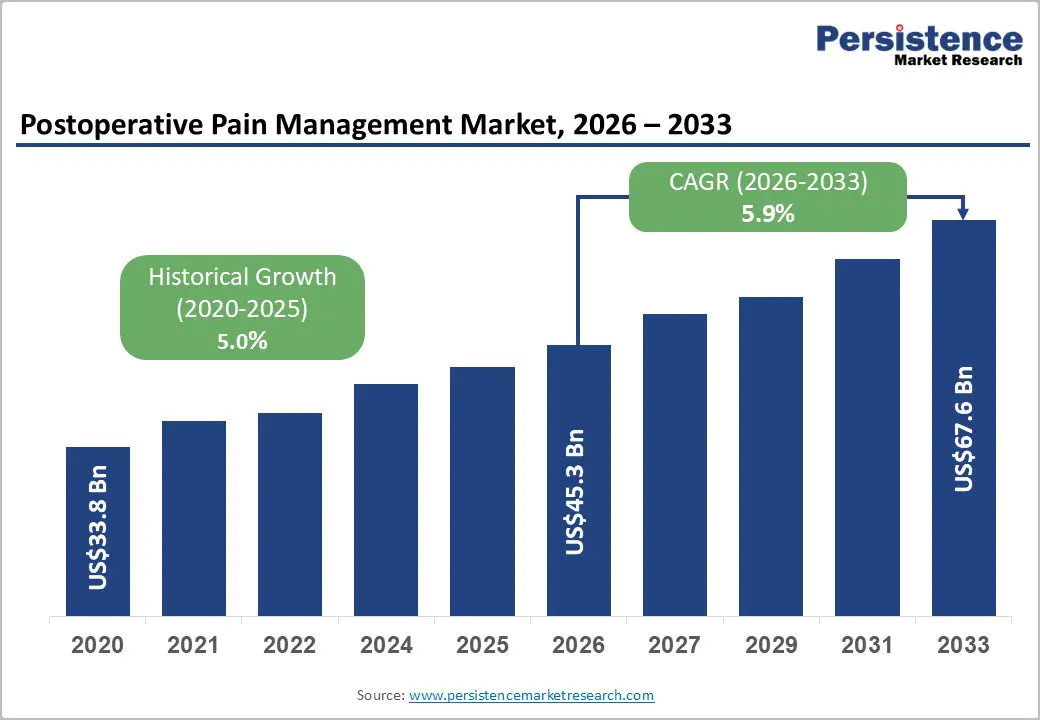

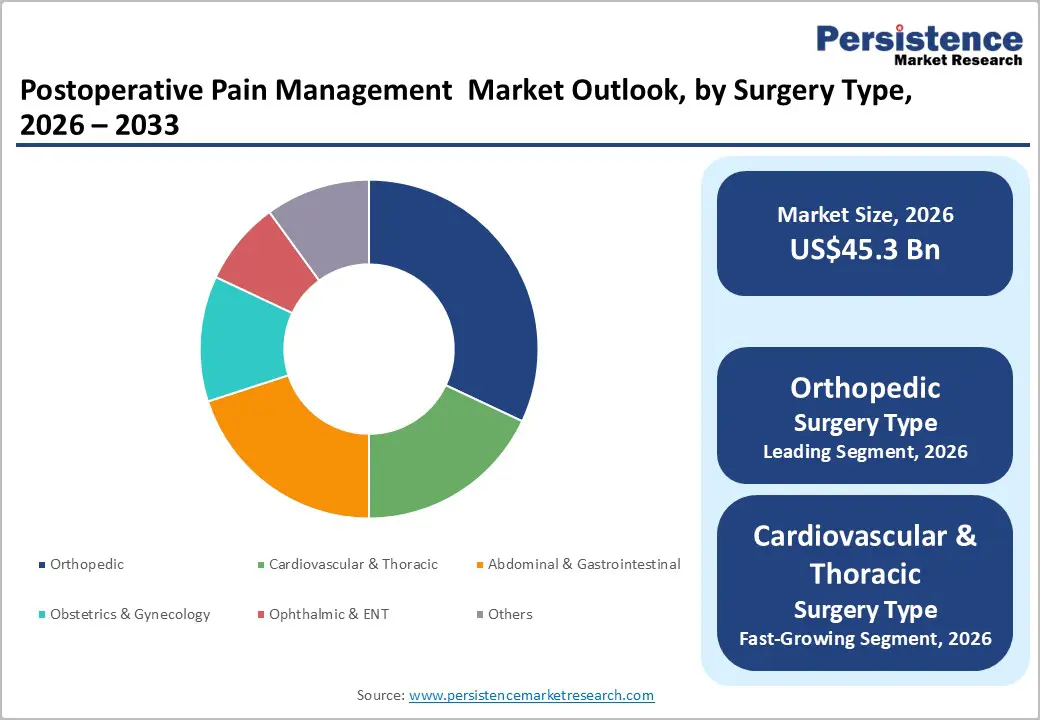

The global postoperative pain management market size is likely to be valued at US$45.3 billion in 2026, and is expected to reach US$67.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by the critical intersection of rising global surgical volumes, the urgent need to reduce opioid dependency through multimodal analgesia protocols, growing adoption of regional anesthesia and extended-release local anesthetic formulations, expanding ambulatory surgery center procedure volumes requiring effective outpatient pain control strategies, and accelerating pharmaceutical innovation in non-opioid and opioid-sparing analgesic drug development.

Key Industry Highlights:

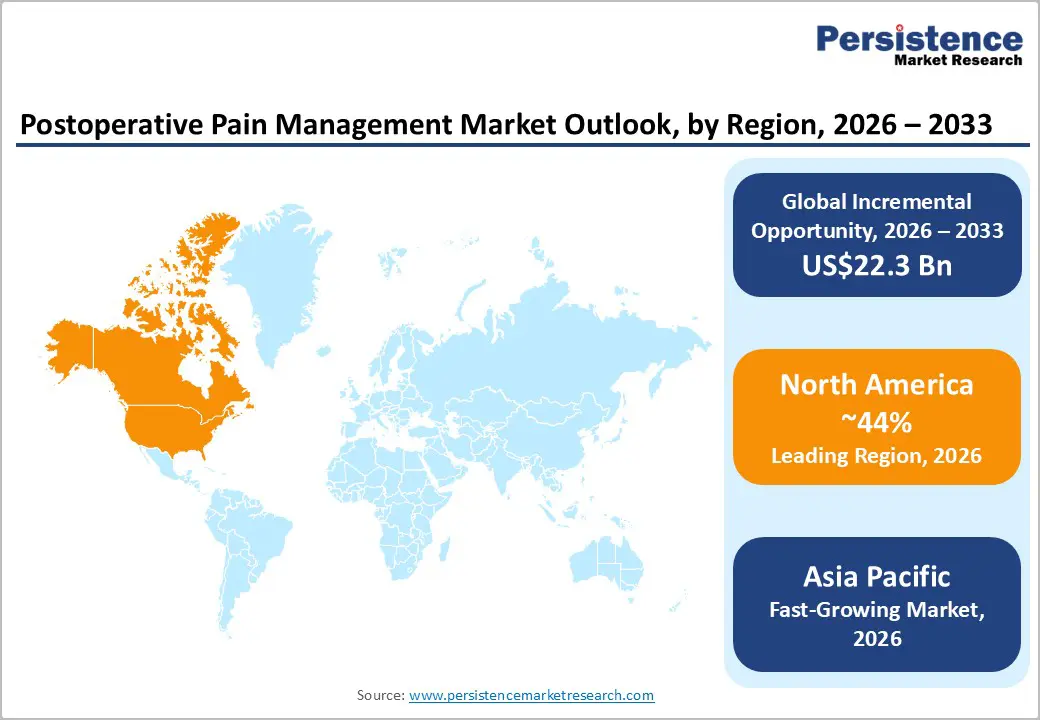

- Dominant Region: North America is expected to dominate, holding approximately 44% revenue share in 2026, driven by the world's highest surgical procedure volumes, established multimodal analgesia clinical guidelines, comprehensive insurance reimbursement frameworks, and the concentrated commercial presence of AbbVie, Johnson & Johnson, Pfizer, Pacira BioSciences, and Heron Therapeutics.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing postoperative pain management market, driven by rapidly expanding surgical procedure volumes, growing pharmaceutical market penetration, and rising healthcare infrastructure investment across China, India, Japan, and Southeast Asia.

- Leading Drug Class: NSAIDs and COX-2 inhibitors are estimated to dominate the drug class segment, commanding approximately 35% of revenue in 2026, reflecting their essential role in multimodal analgesia protocols as opioid-sparing analgesic components across all surgical specialties.

- Dominant Surgery Type: Orthopedic surgery is expected to dominate the surgery type, accounting for approximately 32% of market value in 2026, driven by the enormous and growing volume of joint replacement, spinal fusion, and sports medicine procedures generating significant post-surgical analgesic demand.

DRO Analysis

Driver - Opioid Crisis Response and the Multimodal Analgesia Transition

The public health imperative to reduce postoperative opioid prescribing, driven by the devastating consequences of the opioid epidemic, is one of the most powerful structural forces reshaping the postoperative pain management market globally. The Centers for Disease Control and Prevention (CDC) reports approximately 80,000 opioid overdose deaths annually in the U.S., with postoperative opioid prescriptions identified as a significant pathway to opioid dependency and diversion.

The Enhanced Recovery After Surgery (ERAS) Society's evidence-based perioperative care protocols now adopted as the clinical standard of care across major U.S. and European hospital systems for colorectal, orthopedic, gynecologic, and cardiac surgery explicitly mandate opioid-sparing multimodal analgesia as a core protocol element. ERAS protocols incorporating preoperative analgesic optimization, intraoperative regional anesthesia, postoperative NSAID and COX-2 inhibitor use, and adjuvant analgesic agents have demonstrated 30%-50% reductions in postoperative opioid consumption alongside improved recovery metrics and shorter hospital stays.

Restraint - Generic Drug Competition and Pricing Pressure on Branded Analgesic Products

The postoperative pain management market's most commercially significant drug categories, including NSAIDs, opioid analgesics, and conventional local anesthetics, are heavily genericized, creating intense pricing pressure on branded pharmaceutical companies seeking to maintain revenue premium for differentiated pain management products.

Hospital formulary committee decisions driven by pharmacy and therapeutics committees applying pharmacoeconomic evaluation frameworks systematically favor generic analgesic substitution for non-differentiated pain management products, constraining branded manufacturer market access in institutional procurement channels.

Opportunity - Extended-Release and Non-Opioid Analgesic Innovation for Opioid-Sparing Protocols

The growing emphasis on opioid-sparing pain management protocols is creating a significant opportunity for innovation in extended-release and non-opioid analgesics within the market. Healthcare providers are increasingly adopting multimodal pain management strategies that reduce reliance on opioids due to rising concerns regarding opioid addiction, adverse side effects, respiratory depression, and prolonged hospitalization.

This shift is accelerating demand for advanced analgesic formulations such as extended-release local anesthetics, long-acting injectables, NSAIDs, nerve block therapies, and non-opioid combination drugs that provide sustained pain relief with fewer complications. Pharmaceutical companies are investing heavily in novel delivery technologies, including liposomal formulations, transdermal systems, and biodegradable implants, designed to improve patient recovery and reduce repeat dosing requirements. Regulatory agencies and hospital systems are also supporting opioid-minimization initiatives through enhanced recovery after surgery (ERAS) protocols, further strengthening adoption of alternative pain therapies.

Category-wise Analysis

Drug Class Insights

NSAIDs and COX-2 inhibitors are expected to dominate the drug class segment, commanding approximately 35% of global revenue in 2026. Their market leadership reflects their universal clinical deployment as opioid-sparing analgesic components within multimodal analgesia protocols across virtually all surgical specialties, from orthopedic and cardiovascular surgery through to abdominal and gynecologic procedures.

Local anesthetics are likely to represent the fastest-growing drug class, driven by the growing adoption of ERAS protocols, increasing use of peripheral nerve block techniques, and rising demand for extended-release local anesthetics in outpatient and orthopedic surgeries, which are accelerating growth in the postoperative pain management market.

Route of Administration Insights

Injectable formulations are expected to dominate the route of administration segment, capturing approximately 45% of market revenue in 2026. The injectable route's leadership reflects the clinical primacy of intravenous, intramuscular, subcutaneous, and regional nerve block drug delivery in immediate postoperative pain control, where rapid, titratable, and reliable analgesic onset is required in hospital and surgical center settings, where intravenous access is routinely established.

Intrathecal and epidural administration is expected to be the fastest-growing route of administration. The increasing use of neuraxial analgesic techniques such as epidural infusions, intrathecal opioids, and patient-controlled epidural analgesia (PCEA) is driving demand for specialized intrathecal and epidural formulations with preservative-free, sterile, and optimized concentration specifications in postoperative pain management.

Surgery Type Insights

Orthopedic surgery is estimated to dominate the surgery type segment, accounting for approximately 32% of global revenue in 2026. The segment's dominance reflects both the enormous and growing volume of orthopedic procedures globally, with the AAOS projecting 401% growth in the U.S. total knee arthroplasty demand through 2040 and the particularly complex, high-intensity pain management requirements of major joint replacement and spinal fusion procedures.

Cardiovascular and thoracic surgery represents the fastest-growing segment of surgery. The increasing procedural complexity of cardiac and thoracic surgery, combined with the critical clinical imperative for optimal postoperative analgesia to enable early extubation, respiratory physiotherapy, and rapid rehabilitation, is driving demand for multimodal pain management protocols in cardiac ICU and thoracic surgery ward settings.

Distribution Channel Insights

Hospital pharmacies are expected to dominate the distribution channel, commanding 58% of total revenue in 2026, as most analgesics are administered during inpatient surgical care under direct clinical supervision. They ensure the immediate availability of injectable drugs, regional anesthesia agents, and controlled pain medications used in perioperative and recovery settings.

Online pharmacies are likely to be the fastest-growing segment in the market, due to the increasing digital healthcare adoption and e-prescription integration. They offer convenient access to prescribed non-opioid oral analgesics and discharge medications, supporting post-surgery home recovery.

Regional Insights

North America Postoperative Pain Management Market Trends

North America market growth is projected to dominate, capturing around the 44% of total revenues in 2026. The market is shifting toward opioid-sparing and multimodal analgesia strategies, driven by the opioid crisis and strict prescribing regulations. There is strong adoption of ERAS protocols, regional anesthesia, and non-opioid alternatives such as NSAIDs, local anesthetics, and nerve blocks.

U.S. Postoperative Pain Management Market Insights

The U.S. market is one of the world's most commercially advanced, characterized by rapid adoption of ERAS protocol-driven multimodal analgesia, extensive deployment of extended-release local anesthetic formulations, and a highly competitive branded versus generic pharmaceutical landscape. Strict regulatory frameworks in the U.S., including CDC opioid prescribing guidelines, DEA Schedule II controls, and state PDMP mandates, are driving strong adoption of non-opioid analgesics in postoperative care. This shift is accelerating formulary changes in hospitals toward opioid-sparing options.

Canada Postoperative Pain Management Market Insights

Market growth in Canada is shaped by Health Canada's pharmaceutical approval processes, provincial formulary listing decisions, and the Canadian Agency for Drugs and Technologies in Health (CADTH) pharmacoeconomic evaluation frameworks. Canada's national opioid strategy, which includes prescriber education, surveillance, and harm reduction programs, parallels U.S. opioid reduction objectives and is generating equivalent clinical practice pressure toward multimodal non-opioid analgesic adoption.

Europe Postoperative Pain Management Market Trends

Europe’s market is increasingly shaped by strong regulatory caution around opioid use and a structured shift toward multimodal analgesia in clinical practice. Healthcare systems across the region emphasize evidence-based pain control, leading to higher use of regional anesthesia techniques such as nerve blocks and neuraxial methods, especially in major orthopedic and abdominal surgeries.

Germany Postoperative Pain Management Market Trends

Germany is the leading European postoperative pain management market, driven by the comprehensive GKV statutory health insurance coverage for in-hospital analgesic therapy, the strong institutional adoption of ERAS protocols across German university hospital surgical programs, and Bayer AG's commercial analgesic portfolio, including injectable parecoxib (Dynastat) and branded NSAID formulations. Germany's healthcare system favors evidence-based pain management protocols, and the German Pain Society (DGSS) guidelines drive consistent prescribing practices across hospital pain management teams.

U.K. Postoperative Pain Management Market Trends

The U.K. postoperative pain management market is shaped by NHS England's formulary frameworks, NICE clinical guidelines for postoperative pain management, and the widespread NHS adoption of enhanced recovery programs developed by the NHS Enhanced Recovery Partnership Programme. NHS formulary restrictions systematically favor generic analgesic prescribing over branded alternatives for non-differentiated products, compressing branded revenue while sustaining generic pharmaceutical demand volumes.

Asia Pacific Postoperative Pain Management Market Trends

Asia Pacific is likely to be the fastest-growing regional market, driven by rising surgical volumes, expanding healthcare infrastructure, and increasing access to advanced medical care. There is a gradual shift toward multimodal analgesia, driven by improving clinical awareness of opioid-related risks and adoption of global ERAS protocols in major hospitals. Demand for cost-effective non-opioid analgesics, regional anesthesia techniques, and generic pain management drugs is particularly strong in emerging economies.

China Postoperative Pain Management Market Trends

China’s market is expanding steadily, driven by rising surgical procedures, hospital modernization, and increasing focus on patient recovery outcomes. The adoption of Enhanced Recovery After Surgery (ERAS) protocols is growing in tier-1 and major tertiary hospitals, supporting multimodal and opioid-sparing analgesia approaches. Regional anesthesia techniques, including nerve blocks and epidural analgesia, are being increasingly integrated into orthopedic, abdominal, and cancer surgeries.

India Postoperative Pain Management Market Trends

India’s market is witnessing rapid evolution, driven by expanding surgical volumes, growth in multispecialty hospitals, and increasing penetration of insurance-backed healthcare. There is a rising preference for protocol-driven pain management, particularly in corporate hospital chains adopting ERAS frameworks to improve bed turnover and surgical efficiency. Demand is increasing for affordable multimodal regimens combining non-opioid injectable, local anesthetics, and adjuvant therapies, aligned with cost-sensitive treatment settings.

Competitive Landscape

The global postoperative pain management market is highly competitive and diverse, comprising large pharmaceutical companies, specialty pain-focused firms, generic manufacturers, and emerging biotech players addressing a broad range of analgesic needs. Key leaders such as Johnson & Johnson, AbbVie, Pfizer, Novartis, and Bayer dominate branded NSAIDs, COX-2 inhibitors, opioid therapies, and adjuvant analgesics across hospital and retail channels.

Specialty and innovation-focused companies are reshaping the competitive landscape through differentiated extended-release and non-opioid analgesic formulations that address the clinical imperative for opioid-sparing postoperative pain control. Pacira BioSciences Inc., with EXPAREL generating approximately US$ 500 million in annual U.S. net revenue, has established the commercial proof-of-concept for premium-priced extended-release local anesthetic innovation in the U.S. postoperative pain market.

Key Industry Developments:

- In April 2026, the FDA expanded the approval of Caldolor to include postoperative pain management in adults and pediatric patients aged three months and older. Manufactured by Cumberland Pharmaceuticals, the IV ibuprofen injection can now be used alone or alongside opioids for surgical pain control. The decision supported broader use of non-opioid, multimodal pain management approaches in hospital and ambulatory settings, reinforcing Caldolor’s role in improving postoperative recovery outcomes.

Companies Covered in Postoperative Pain Management Market

- AbbVie (Allergan)

- AFT Pharmaceuticals

- Alembic Pharmaceuticals

- Baxter International

- Bayer AG

- Boston Scientific

- Cipla Inc.

- Eli Lilly & Co.

- Endo International

- GSK plc

- Heron Therapeutics

- Hikma Pharmaceuticals

- Hyloris Pharmaceuticals

- Johnson & Johnson

- Mallinckrodt plc

- Medtronic plc

- Neumentum Inc.

- Novartis AG

- Pacira BioSciences Inc.

- Pfizer Inc.

- Teva Pharmaceutical Industries

Frequently Asked Questions

The global postoperative pain management market is projected to reach US$45.3 billion in 2026.

The key driver is the global push to reduce postoperative opioid use due to the opioid epidemic, with regulatory and public health agencies promoting safer prescribing practices.

The postoperative pain management market is poised to witness a CAGR of 5.9% from 2026 to 2033.

The key opportunity lies in the rapid expansion of opioid-sparing protocols driving demand for extended-release and non-opioid analgesics, including long-acting injectables, NSAIDs, nerve blocks, and combination therapies.

The leading companies include AbbVie (Allergan), AFT Pharmaceuticals, Alembic Pharmaceuticals, Baxter International, Bayer AG, Boston Scientific, Cipla Inc., Eli Lilly & Co., Endo International, and GSK plc.