- Medical Devices

- Podiatry Workstations Market

Podiatry Workstations Market Size, Share, and Growth Forecast, 2026 - 2033

Podiatry Workstations Market by Product (Podiatry Workstation on Casters, Podiatry Workstation with Monitor, Others), Application (Hospitals, Podiatry Clinics, Ambulatory Surgical Centers, Other Facilities), and Regional Analysis for 2026 - 2033

Podiatry Workstations Market Size and Trends Analysis

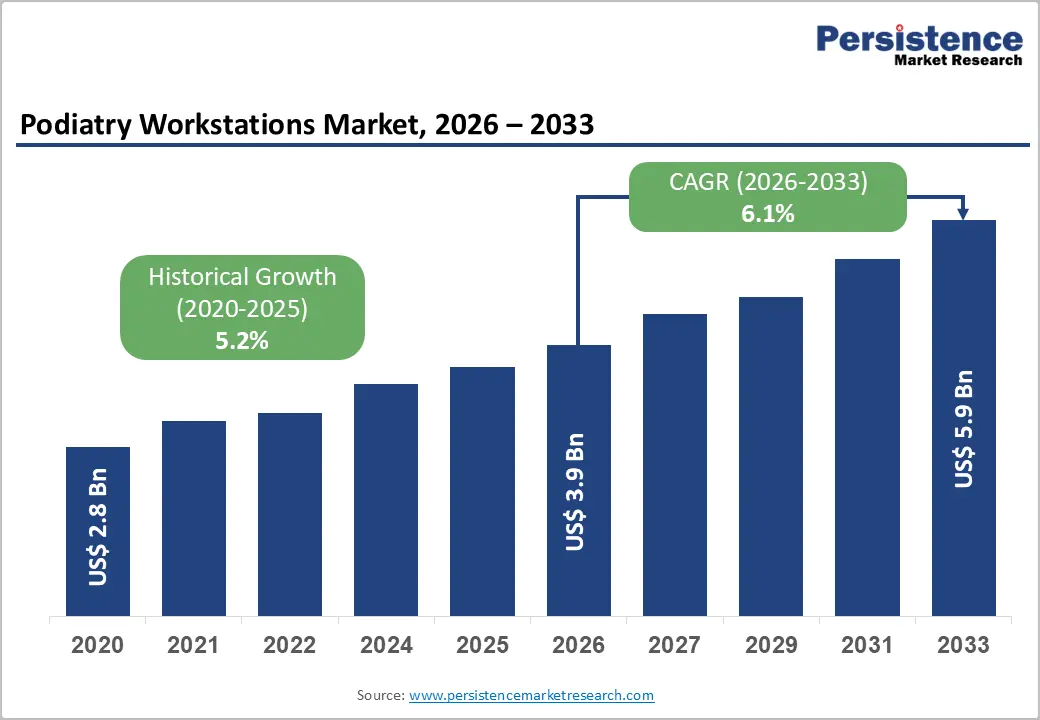

The global podiatry workstations market size is likely to be valued at US$3.9 billion in 2026, and is expected to reach US$5.9 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by the increasing need for specialized podiatric care and the rising prevalence of foot and ankle disorders.

Podiatry workstations are ergonomically designed medical units that equip podiatrists with integrated tools for examinations, treatments, and minor surgical procedures. These systems typically incorporate storage solutions, lighting, display monitors, and patient positioning features, helping to streamline clinical workflows, enhance patient comfort, and maintain high standards of infection control.

Key Industry Highlights:

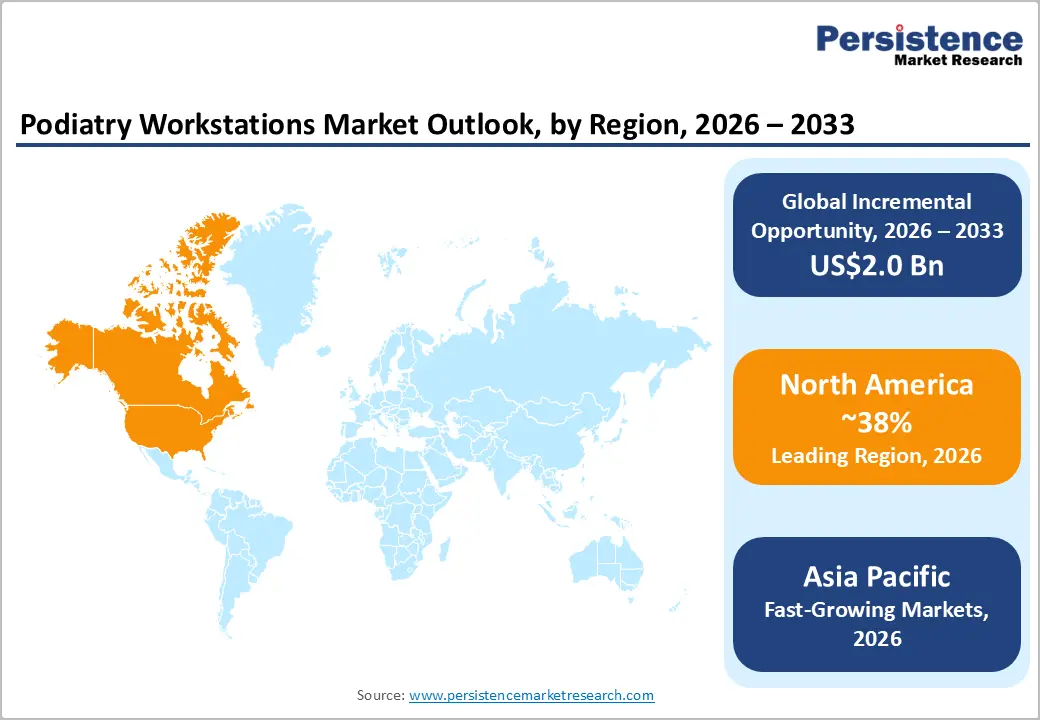

- Dominant Region: North America is projected to dominate with 38% revenue share in 2026, supported by advanced healthcare infrastructure and high prevalence of diabetes-related foot complications.

- Fastest growing Region: Asia Pacific is the fastest-growing region with a projected CAGR of 7.2% (2026 - 2033), driven by the rising diabetic population and expanding podiatry clinics in China and India.

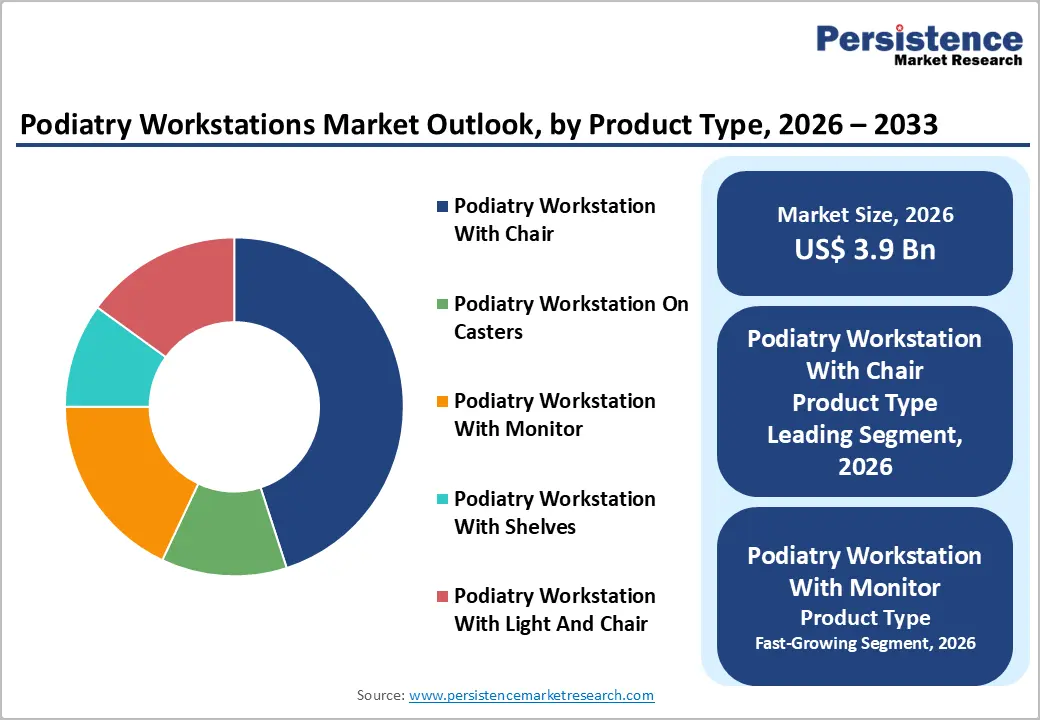

- Dominant Product Type: Podiatry workstation with chair expected to dominate with 45% share in 2026, due to integrated patient positioning.

- Leading Application: Podiatry clinics are projected to lead the application segment with the 55% share owing to dedicated foot care facilities.

DRO Analysis

Driver - Increasing Prevalence of Diabetes and Diabetic Foot-Related Disorders

The most powerful structural driver of the podiatry workstations market is the sustained global increase in diabetes mellitus, which directly elevates demand for specialized foot care infrastructure. According to the International Diabetes Federation, approximately 537 million adults worldwide were living with diabetes in 2021, with projections pointing to 643 million by 2030 and 783 million by 2045. Diabetic peripheral neuropathy affects nearly 50% of patients with long-duration diabetes, resulting in loss of protective sensation, chronic foot ulcerations, and elevated risk of lower-extremity amputation.

The clinical management of diabetic foot disease requires dedicated podiatry environments equipped with multi-functional workstations that support wound assessment, debridement, vascular monitoring, and offloading device fitting within a single patient encounter. Healthcare systems in the U.S., the U.K., Germany, and Australia have formalized diabetic foot care pathways that mandate podiatric consultation, creating institutional demand for examination-grade podiatry workstations across hospital outpatient departments and specialist clinics.

This direct correlation between diabetic foot disease burden and clinical podiatry capacity investment positions the podiatry workstations market as a structurally defensive, demand-driven segment, with procurement decisions in hospitals and specialist centers tied to disease prevalence trends rather than discretionary spending cycles.

Restraint - Limited Standardization and Fragmented Regulatory Frameworks

The podiatry workstations market is characterized by limited standardization in product design, safety certification requirements, and procurement specifications across geographies. Unlike high-regulated categories such as surgical tables or diagnostic imaging systems, podiatry workstations do not face a uniform international regulatory framework, leading to heterogeneous design standards and varying levels of clinical validation documentation required for procurement approvals. This fragmentation increases compliance complexity for manufacturers seeking multi-regional distribution and creates evaluation inefficiencies for hospital procurement committees comparing products across vendors.

The absence of formalized clinical guidelines specifying minimum workstation specifications for podiatric environments in several markets means procurement decisions are often made on aesthetic and ergonomic preference rather than standardized clinical performance criteria, reducing the ability of advanced manufacturers to differentiate premium products on measurable clinical outcomes.

Opportunity - Integration of Digital and Tele-Podiatry Technologies into Workstation Design

The convergence of digital health technologies with clinical podiatry workflows presents a compelling opportunity for workstation manufacturers to develop and differentiate products. The integration of digital plantar pressure analysis systems, 3D foot scanning compatibility, tele-consultation-ready camera and display mounting, and electronic health record (EHR)-connected workstation interfaces is creating a new generation of connected podiatry workstations capable of supporting hybrid in-person and remote care delivery models.

Following the acceleration of telemedicine adoption during the COVID-19 pandemic, healthcare providers are investing in clinical infrastructure that supports both in-person and virtual care continuity. Podiatry workstation manufacturers that embed connectivity, digital imaging compatibility, and data capture capabilities into their products can command premium pricing and establish differentiated positions in technology-forward healthcare systems, particularly in North America, Northern Europe, and Australia.

Category-wise Analysis

Product Type Insights

The podiatry workstation with chair segment is anticipated to lead the product type category, accounting for 45% of revenue in 2026. Integrated chair-based workstations represent the standard-of-care configuration for podiatric examinations and minor procedures, offering clinicians a single, ergonomically optimized unit that combines adjustable patient seating, a stable base platform, instrument storage, and lighting in a single, deployable system. Midmark Corporation offers the Midmark 647 podiatry chair, which integrates powered positioning, ergonomic foot access, and control systems to streamline examinations and procedures in a single unit.

The podiatry workstation with monitor is the fastest-growing product type, reflecting escalating clinician demand for integrated illumination in the examination environment. As clinical standards for wound assessment, nail pathology diagnosis, and surgical site inspection tighten, the ability to deliver high-intensity, color-accurate, and directionally adjustable lighting at the point of care becomes a critical procurement criterion. The NAMROL Duna podiatry workstation integrates a monitor, chair, and lighting system in a single unit, controlled via a touchscreen interface, enabling clinicians to adjust parameters and maintain optimal visibility during procedures.

Application Insights

Podiatry clinics are projected to dominate, capturing 55% of the market in 2026, driven by the global expansion of specialist foot care practices and the routine capital investment cycle of clinic establishment and refurbishment. Dedicated podiatry clinics are the primary point-of-care environment for the full spectrum of foot and ankle conditions, including routine nail care, orthotic fitting, wound management, and surgical consultation. The Foot Practice offers services such as orthotics, skin and nail care, diabetic foot management, and gait analysis, demonstrating how modern clinics handle comprehensive podiatric care within a single facility.

Ambulatory surgical centers are the fastest-growing segment, driven by the global shift toward outpatient surgical care as health systems prioritize cost efficiency and patient convenience. In the U.S., where ASC volume growth for podiatric procedures has been particularly pronounced, CMS reimbursement policy changes have incentivized the migration of common podiatric surgeries, including bunionectomy, hammertoe repair, and plantar fascia release, to ASC settings. The UChicago Medicine Ingalls Memorial Ambulatory Surgery Center offers outpatient podiatric procedures, including bunionectomy, hammertoe repair, and ankle arthroscopy, all performed as same-day surgeries.

Regional Insights

North America Podiatry Workstations Market Trends

North America is projected to lead the global podiatry workstations market, expanding at a CAGR of approximately 5.8% through 2033. The U.S. is the dominant national market, driven by a well-established podiatric medicine profession, the only country in the world that offers a distinct four-year Doctor of Podiatric Medicine (DPM) degree, which sustains a large, growing community of licensed podiatrists operating approximately 14,000 podiatric practices nationwide.

The U.S. market trends are shaped by rising diabetic foot case volumes, with over 37 million Americans diagnosed with diabetes and associated podiatric complications driving steady outpatient clinic caseloads. The expansion of value-based care models and Medicare reimbursement frameworks for podiatric services in ASC settings is accelerating clinical infrastructure investment, with new clinic openings and ASC buildouts generating direct workstation procurement demand. Aging demographics with the 65+ population in the U.S. exceeding 57 million and projected to reach 80 million by 2040 are reinforcing structural demand for specialist outpatient foot care services.

Canada represents a secondary but consistently growing market. Growing provincial investments in community health clinic infrastructure and expanding chiropody/podiatry service coverage under extended health benefits are supporting workstation adoption across British Columbia, Ontario, and Quebec.

Europe Podiatry Workstations Market Trends

Europe represents the second-largest regional market for podiatry workstations, supported by well-established universal healthcare systems, structured diabetic foot care programs, an aging population, and a strong base of medical furniture and clinical equipment manufacturers.

Within the region, Germany is expected to lead the market, driven by its growing elderly population, high prevalence of diabetes, and robust statutory health insurance system (GKV), which includes podiatric care under the Disease Management Programme (DMP). Favorable reimbursement policies have encouraged continuous investment in advanced podiatry workstations across healthcare facilities.

The U.K. also holds a prominent position, supported by the National Health Service (NHS) Diabetic Foot Care Service, which ensures structured podiatric assessment across all levels of care. The market in the U.K. is projected to grow at a CAGR of approximately 5.2% through 2033. Meanwhile, France ranks as the third-largest market in Europe, benefiting from a well-established podology profession and comprehensive health insurance coverage for podiatric services.

Asia Pacific Podiatry Workstations Market Trends

Asia Pacific is expected to be the fastest-growing regional market for podiatry workstations, and is projected to expand at a CAGR of approximately 7.3% through 2033. The region's growth trajectory is underpinned by a rapidly expanding diabetic population, rising healthcare infrastructure investment, and growing consumer awareness of specialist foot care services.

China represents the largest national market in the region and one of the fastest-growing globally. With the International Diabetes Federation estimating approximately 140 million diabetic individuals in China, the world's largest diabetic population, the systemic demand for diabetic foot care infrastructure is substantial. China's CAGR in podiatry workstations is estimated at approximately 7.8% through 2033.

India emerged as a high-growth market, driven by a diabetic population exceeding 77 million, expanding private hospital networks, and broader access under Ayushman Bharat. Japan maintained steady demand due to its aging population (29% over 65) and advanced healthcare system, growing at a 5.5% CAGR through 2033. Southeast Asian markets, including Indonesia, Thailand, and Vietnam, remained at earlier development stages but showed accelerating growth, with private hospitals adding podiatric services and a collective CAGR above 8.5% through 2033.

Competitive Landscape

The global podiatry workstations market is moderately consolidated, with a mix of specialized medical furniture manufacturers and broader clinical equipment companies competing on design innovation, clinical integration capability, and global distribution reach. Euro Clinic Medi-Care Solutions and Gharieni are among the most recognized specialist manufacturers, offering comprehensive podiatry workstation portfolios that span entry-level examination configurations to fully motorized, light-integrated, and digital-ready systems.

Competitive differentiation in the podiatry workstations market centers on four key dimensions: ergonomic design and patient comfort, infection-control surface materials compliance with EN 13485 and equivalent standards, modularity and configurability to meet diverse clinical environment requirements, and digital integration capability for tele-podiatry and EHR-connected workflows. Manufacturers with demonstrated capability in motorized height adjustment, integrated LED examination lighting, and compatibility with digital plantar pressure analysis or 3D scanning systems command premium positioning in clinically sophisticated procurement environments.

Key Industry Developments:

- In January 2025, Zimmer Biomet Holdings, Inc. announced that it had entered into a definitive agreement to acquire Paragon 28, Inc. The deal included an upfront cash payment of US$13.00 per share, valuing Paragon 28 at approximately US$1.1 billion in equity and about US$1.2 billion in enterprise value.

- In 2024, VERITAS Medical Solutions expanded its distribution agreements in the Asia Pacific region, targeting growing private hospital and clinic chain procurement channels in China, Australia, and Southeast Asia, where rising podiatric service adoption is driving first-time workstation procurement at scale.

Companies Covered in Podiatry Workstations Market

- Euro clinic Medi-Care Solutions

- Capron

- Eduard Gerlach

- Gharieni

- Namrol

- Planmeca

- VERITAS Medical Solutions

Frequently Asked Questions

The global podiatry workstations market is projected to reach US$3.9 billion in 2026.

The podiatry workstations market is primarily driven by the rising prevalence of diabetes-related foot complications, the growing number of podiatry clinics, and demand for ergonomic, efficient treatment setups.

The podiatry workstations market is poised to witness a CAGR of 6.1% from 2026 to 2033.

Key opportunities in the podiatry workstations market include expansion in ambulatory surgical centers, growth of dedicated podiatry clinics, and rising healthcare investments in emerging economies.

Key players in the podiatry workstations market include Euro clinic Medi-Care Solutions, Capron, Eduard Gerlach, Gharieni, Namrol, Sartorius, VERITAS Medical Solutions, and EKF Diagnostics.