Industry: Chemicals and Materials

Published Date: December-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 191

Report ID: PMRREP33594

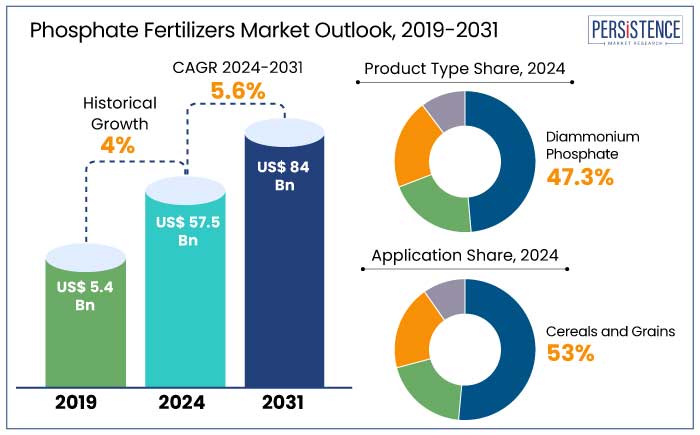

The phosphate fertilizers market is estimated to increase from US$ 57.5 Bn in 2024 to US$ 84 Bn by 2031. The market is projected to record a CAGR of 5.6% during the forecast period from 2024 to 2031.

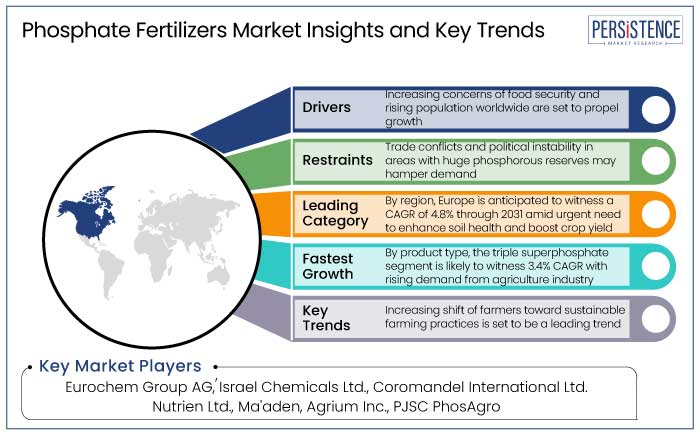

Phosphate fertilizers are becoming increasingly popular worldwide due to the need to increase agricultural output and satisfy the rising food demands of a growing population. Fertilizers account for around 60% of the world's food supply.

Phosphates are hence essential for maintaining crop health, increasing yields, and strengthening resilience to environmental challenges. By 2050, there will likely be 10 billion people on the planet, thereby surging the need for effective fertilizers like phosphates.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Phosphate Fertilizers Market Size (2024E) |

US$ 57.5 Bn |

|

Projected Market Value (2031F) |

US$ 84 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

5.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

4% |

In 2024, Asia Pacific is likely to account for around 60.6% of the global phosphate fertilizers market share. It is driven by robust agricultural practices and significant crop production in countries like China and India.

High demand for phosphate fertilizers in this region stems from its ever-increasing population, which relies heavily on staple food commodities. Agriculture plays a key role in sustaining livelihoods and ensuring food security. For example,

Asia Pacific’s strong market presence is further bolstered by a commitment to enhancing agricultural productivity. The region benefits from innovations in agricultural technology and a rising awareness of the importance of balanced nutrient management. This combination positions Asia Pacific as a key hub in the phosphate fertilizer industry.

Europe is likely to witness a considerable CAGR of 4.8% in the global market through 2031. Precision farming methods are being used by farmers in Europe to maximize fertilizer use. A vital component of phosphate fertilizers, phosphorus is essential for enhancing agricultural yields and soil health.

A move toward balanced fertilization techniques in line with the European Green Deal and Farm to Fork Strategy has led to rising use of phosphate fertilizers with improved efficiency. Products like coated or slow-release phosphates, for instance, are becoming immensely popular in countries like France and Germany.

Diammonium phosphate (DAP) is projected to hold the most prominent market share of about 47.3% in 2024. Its balanced nutrient profile, rich in both nitrogen and phosphorus, makes it a popular choice among farmers.

DAP is renowned for its effectiveness in promoting healthy plant growth and significantly enhancing crop yields, solidifying its presence in the market. It is mainly used in the production of fruits, barley, wheat, and vegetables.

It is highly soluble in nature and dissolves quickly in the soil. This allows it to release phosphate and ammonium to enhance root growth, color development, and flower bud growth. On the other hand, the triple superphosphate segment is anticipated to witness a CAGR of 3.4% through 2031. It is attributed to rising demand from the global agriculture industry as it has a high concentration of phosphorus fertilizer.

The cereals and grains segment is likely to hold a market share of 53% in 2024 by application. Demand for cereals and grains, which account for 45 to 50% of daily caloric consumption globally, is increasing in tandem with the world's population growth.

To increase the yield of these crops, especially in areas with soils that are deficient in nutrients, phosphate fertilizers are required. For example, high-intensity rice and wheat cultivation in China and India necessitates the continuous use of phosphates to sustain productivity levels.

Phosphate fertilizers are associated with the international market, which includes the production, distribution, and use of fertilizers. These are made of phosphorous compounds that promote plant growth. These fertilizers play a key role in agriculture by supplying phosphorus, which is a vital nutrient that supports root development, plant maturation, and energy conversion.

Phosphate fertilizers offer several benefits to plants as they increase soil fertility and crop yields. They also ensure sustainability and global demand for food production. Growth of the market is fueled by increasing population, rising global food demand, and expansion of the agricultural sector. For instance,

The aforementioned drivers indicate the increasing demand for greater produce yields. Additionally, government initiatives, improved fertilizer formulations, and technological progress boost the industry.

The phosphate fertilizers market overview shows that demand in this industry has risen in the past few years. It witnessed a decent CAGR of 4% from 2019 to 2023.

Several factors are fueling the industry’s growth, such as increasing demand for food security and sustainable agricultural practices. The market was also driven by the popularity of products like Monoammonium Phosphate (MAP) and Diammonium Phosphate (DAP), which are essential for enhancing crop yields.

The market is projected to surge at a CAGR of 5.6% from 2024 to 2031. This anticipated growth is fueled by factors such as the rising global population, which necessitates high agricultural productivity, and a growing emphasis on sustainable farming practices. Additionally, innovations in fertilizer formulations and increased investments in agricultural technology are anticipated to further bolster market expansion.

Surging Focus on Sustainable Agricultural Practices to Fuel Sales

A leading factor accelerating the phosphate fertilizers market growth is the rising focus on sustainable farming. The U.S. has a population of 345,976,665. It is increasing by 0.7% and 0.9% per year. This shows the rising demand for food and the need for sustainable agricultural practices that can meet this requirement.

Phosphate fertilizers have the ability to boost soil fertility and improve yield productivity. It can also ease soil nutrient shortage, boosting demand worldwide.

Phosphate fertilizers help restore essential nutrients, such as phosphorous, in soil, promoting soil health and ensuring prolonged agricultural productivity. They are also crucial in adopting environmentally sustainable practices and ensuring crop yields while preserving environmental integrity.

Limited Availability of Cultivable Land to Propel Demand

Decreasing amount of arable land available per person in countries like India, China, and the U.S. is projected to boost the global market. With more people and less land to farm, it is essential to push agricultural yields to meet the surging need for food. Farmers are increasingly turning to crop protection strategies to tackle this challenge. They are hence using phosphorus fertilizers as these have proved to be an effective method to enhance crop production.

As industrialization and urbanization continue to take over, chances of extending agricultural land are slim. Demand for phosphorus fertilizers is likely to increase in the next ten years as people consume more meat and other food products, alongside population growth.

Geopolitical Tensions to Severely Affect Phosphorus Supply

Despite the rising demand for phosphate fertilizers, the availability of raw materials is facing significant challenges due to geopolitical uncertainties. Phosphorus, a key ingredient in these fertilizers, primarily comes from phosphate rock. A large portion of the world's reserves is located in areas that are politically sensitive.

Political instability, trade conflicts, or changes in regulations in these regions can disrupt the supply chain, leading to fluctuations in both the prices and availability of phosphate fertilizers. This uncertainty underscores the need for companies to navigate such complexities to ensure a stable supply for farmers. For instance,

Strict Regulations and Environmental Concerns May Hamper Demand

The global phosphate fertilizers market has been undergoing constant changes due to a lack of standardized market and free trade regulations governing the supply and demand for phosphate rock. Governments and state-owned companies play a significant role in managing and controlling this sector. Consequently, increased government intervention in response to shifts in the market can negatively impact both the market itself and the supply of phosphate rock.

Several challenges are currently facing the market, including concerns about the P2O5 grade of phosphorus and cadmium pollution, which poses risks to human health and the environment. Additionally, there is a growing awareness of inefficient phosphate usage and loss, especially as urbanization continues to rise. These issues highlight the need for a more balanced approach to managing this market.

Innovations in Agriculture Technology to Create Novel Opportunities

The rapid development of agricultural technology is driving growth in the phosphate fertilizers industry. Innovations like digital agriculture and precision farming are helping farmers use these fertilizers more efficiently.

By leveraging sensors, satellite imagery, and data analytics, farmers can tailor fertilizer applications to meet the specific needs of their crops. This targeted approach increases yields and minimizes fertilizer waste.

It further benefits the environment and enhances the effectiveness of these fertilizers. Moreover, smart agriculture techniques, supported by artificial intelligence and the Internet of Things (IoT), are opening up new possibilities for the industry.

Companies to Adopt Backward Integration Tactics to Gain Profit

Vertical integration is set to boost profit margins for companies in the phosphate fertilizer industry by reducing reliance on suppliers. Raw material costs are a significant expense for these manufacturers. Hence, several companies are adopting backward integration to produce essential materials like phosphoric acid in-house. For example,

The field of phosphorus fertilizers is characterized by intense competition among key players striving to enhance product efficiency and sustainability. Companies are increasingly focusing on innovation and vertical integration to secure supply chains and reduce costs.

Mosaic Company, for instance, has been launching several innovative products since 2022, including its MicroEssentials® S10 and Mosaic's Enhanced Efficiency Fertilizers. These are designed to optimize nutrient delivery and minimize environmental impact. These developments not only improve crop yields but also align with sustainable farming practices. It helps in positioning Mosaic as a leader in the evolving phosphate fertilizer landscape.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Product Type

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is predicted to rise from US$ 57.5 Bn in 2024 to US$ 84 Bn by 2031.

Eurochem Group AG, Israel Chemicals Ltd., Nutrien Ltd., Ma'aden, and Agrium Inc. are a few leading companies.

DAP is projected to lead by holding about 47.3% of the market share in 2024.

Asia Pacific is likely to account for about 60.6% of the market share in 2024.

Key opportunities in the industry include stringent environmental regulations and water scarcity awareness.