Comprehensive Analysis of Personalized Medicine Biomarkers Including Regional and Country Analysis in Brief.

Industry: Healthcare

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 180

Report ID: PMRREP35202

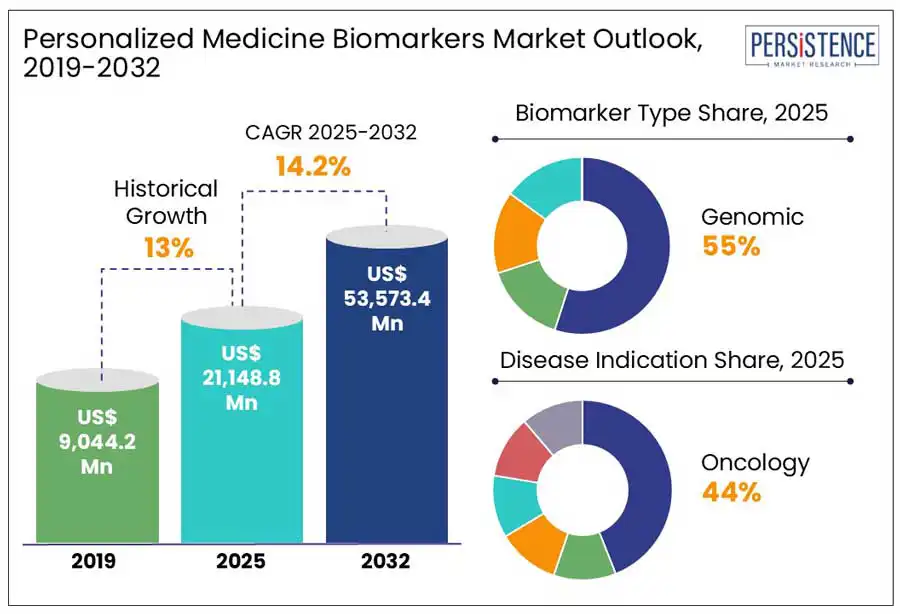

The global personalized medicine biomarkers market size is anticipated to reach a value of US$ 21,148.8 Mn in 2025 and will likely attain a value of US$ 53,573.4 Mn at a CAGR of 14.2% by 2032.

The personalized medicine biomarkers market is expanding steadily, driven by the advancements in precision medicine, increasing prevalence of chronic diseases, and the growing adoption of targeted therapies. The demand for biomarker-based diagnostics is rising as healthcare providers seek more accurate and individualized treatment approaches for conditions such as cancer, cardiovascular diseases, and neurological disorders. Technological innovations in genomics, proteomics, and bioinformatics are enhancing biomarker discovery and validation. North America and Europe lead the market due to robust healthcare infrastructure and high R&D investments, while Asia Pacific is emerging as a key growth region, supported by expanding clinical research and rising demand for personalized healthcare solutions.

Key Industry Highlights:

|

Global Market Attribute |

Key Insights |

|

Personalized Medicine Biomarkers Market Size (2025E) |

US$ 21,148.8 Mn |

|

Market Value Forecast (2032F) |

US$ 53,573.4 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

14.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

13.0% |

The rising prevalence of chronic and life-threatening diseases, such as cancer, cardiovascular disorders, and autoimmune conditions is a significant driver. As these diseases become more widespread, there is an increasing need for early detection, risk assessment, and targeted treatment strategies, which biomarkers enable. For instance, according to the Centers for Disease Control and Prevention (CDC) (February 2024), approximately 129 million U.S. individuals have at least one chronic illness, emphasizing the growing burden on healthcare systems. This necessitates predictive and prognostic biomarkers that helps tailor treatment plans, improving patient outcomes and reducing healthcare costs. As biopharmaceutical companies and healthcare providers increasingly focus on precision medicine, the investments are accelerating for biomarker research and development, further fueling market growth.

The high costs associated with biomarker development and personalized therapies are challenging. The research and development (R&D) of biomarkers and companion diagnostics require substantial financial investment with clinical validation being a particularly lengthy and expensive process due to the need for large-scale clinical trials. Additionally, the manufacturing of precision therapies demands significant capital expenditure to meet stringent regulatory requirements. The technical complexity of biomarker testing and analysis followed by the need for advanced laboratory infrastructure, adds to the overall expense, making personalized treatments less accessible in certain regions.

Companion diagnostics (CDx) present a significant opportunity in the field of oncology. As of 2023, the FDA has approved more than 50 CDx tests, supporting tailored therapy for particular biomarkers, such as osimertinib and pembrolizumab. Over 70% of cancer medications now under research include a biomarker approach, underscoring the growing dependence on CDx to direct therapy. Precision prescribing is made possible by these tests, which also increase efficacy and decrease side effects. CDx integration is spreading beyond cancer into chronic diseases as the need for individualized care increases, establishing it as a major force behind innovation and advancement in customized medicine.

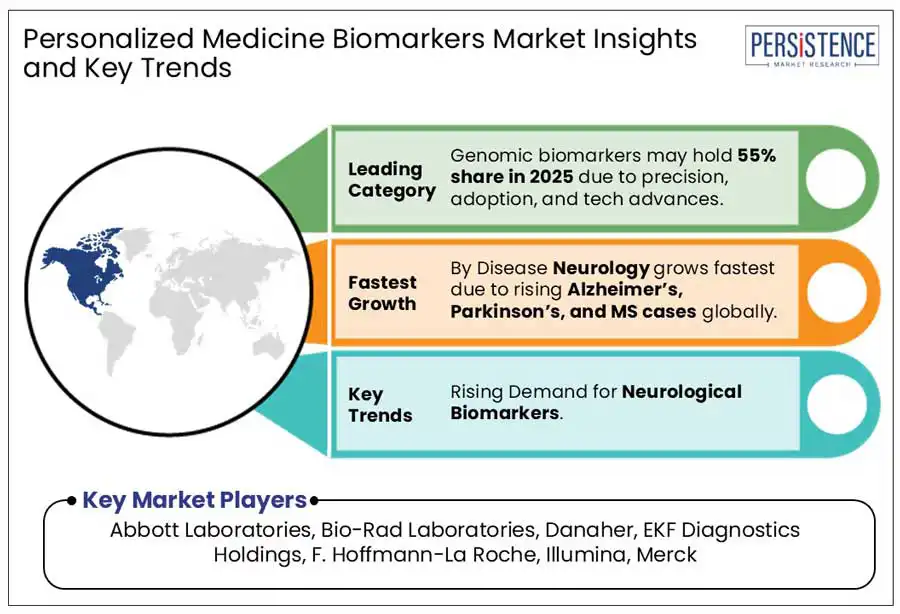

Genomics are the leading biomarker types projected to hold approximately 55% share in 2025. Genomic biomarkers lead due to their high clinical relevance, precision in disease prediction, and strong technological advancements. These biomarkers play a crucial role in identifying disease risk, monitoring progression, and tailoring treatments, particularly in oncology, rare diseases, and hereditary conditions. The rapid development of next-generation sequencing (NGS), whole-genome sequencing, and CRISPR-based diagnostics has significantly improved accessibility and cost-effectiveness, further driving adoption.

Oncology is the leading disease indication with a projected share of 44% in 2025. It dominates for its high prevalence, strong demand for precision therapies, and significant advancements in biomarker-driven cancer diagnostics and treatments. Cancer remains one of the leading causes of death globally, necessitating early detection, targeted therapies, and companion diagnostics, all rely heavily on biomarkers. The rapid adoption of liquid biopsy, circulating tumor DNA (ctDNA) analysis, and next-generation sequencing (NGS) has further strengthened oncology by enabling non-invasive cancer detection and personalized treatment planning.

North America is expected to account for 38% share in 2025, due to the advanced healthcare infrastructure, significant R&D investments, and strong government support for precision medicine initiatives. The U.S. is a significant market and benefits from programs such as the ‘All of Us’ Research Program and the FDA’s Biomarker Qualification Program, that accelerates biomarker adoption in clinical practice.

A study presented at the ESMO Asia Congress 2024 reported that in North America, c-Met protein overexpression was observed in 40% of patients with non-small cell lung cancer (NSCLC) with 23% exhibiting high overexpression. This highlights the region’s advanced capabilities in biomarker-driven oncology treatments, fostering greater adoption of targeted therapies. The presence of key biotech firms, rising adoption of next-generation sequencing (NGS), and increasing demand for companion diagnostics further strengthens North America’s position.

Europe is the second most leading region expected to account for 27% share in 2025. Germany, France, and the U.K. lead based on their advanced healthcare systems, research funding, and favorable regulatory frameworks supporting biomarker adoption. Germany, with its robust biotechnology and pharmaceutical industry, drives innovation in genomic and proteomic biomarkers. France benefits from increasing government investments in precision medicine, while the U.K. witness rising demand due to expanding clinical trials and personalized oncology programs. Additionally, the growth of biomarker-based diagnostics, increasing adoption of next-generation sequencing (NGS), and the advancements in AI-driven biomarker discovery further propel market expansion across the region.

Asia Pacific is poised to witness the fast-growth driven by the rapid advancements in healthcare infrastructure, expanding patient population, and increased participation from emerging biotech firms. The region accounts for a significant portion of the global cancer burden. According to Global Cancer Statistics 2020, Asia recorded approximately 50% of all cancer cases and 58.3% of cancer-related deaths that year. This has led to a surge in cancer screening initiatives, including government-backed programs offering free breast cancer screening and strategic partnerships for test development and distribution.

The clinical industry for biomarkers in Latin America is gaining momentum due to the rising prevalence of infectious diseases, increasing participation in global clinical trials, and a growing focus on improving patient outcomes through targeted therapies. Additionally, regulatory agencies are streamlining approval processes for precision medicine innovations, facilitating market entry for international biotech firms. Increasing investments in bio-banks and genomic research centers across the region are further enhancing biomarker discovery and adoption, supporting the market’s steady growth.

?The market in the Middle East and Africa (MEA) is experiencing significant growth driven by the increasing prevalence of chronic diseases such as diabetes, cardiovascular conditions, and cancer, which have heightened the demand for personalized diagnostic and therapeutic solutions. Among the countries in the region, the GCC Countries are expected to register the high CAGR during this period.

Notably, Abu Dhabi's extensive investment in genetic sequencing, including the sequencing of over 800,000 genomes as part of the Emirati Genome Programme, exemplifies the region's commitment to advancing personalized medicine. Additionally, initiatives such as Ghana's Yemaachi Biotech's development of Africa's largest cancer database underscore the continent's dedication to leveraging genomic data for improved healthcare outcomes.

The global personalized medicine biomarkers market is moderately competitive due to the presence of small and large market players who offer a range of personalized medicine biomarkers. The market players are actively involved in enhancing their offerings to augment their market share.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Biomarker Type

By Application

By Disease Indication

By End-user

By Region

To know more about delivery timeline for this report Contact Sales

The global market is estimated to increase from US$ 21,148.8 Mn in 2025 to US$ 53,573.4 Mn in 2032.

Chronic disease prevalence, genomic sequencing advances, biomarker diagnostics, targeted therapy demand, and precision medicine investments indicate the need for personalized medicine biomarkers.

The market is projected to record a CAGR of 14.2% during the forecast period from 2025 to 2032.

Major players include Abbott Laboratories, Bio-Rad Laboratories, Danaher, EKF Diagnostics Holdings, F. Hoffmann-La Roche, Illumina, Merck and Others.

Opportunities include biomarker-driven drug development, AI-powered diagnostics, expanding companion diagnostics, liquid biopsy advancements, and rising precision medicine adoption.