- Media & Entertainment

- Penetration Testing As Service Market

Penetration Testing As Service Market Size, Share, and Growth Forecast 2026–2033

Penetration Testing As Service Market by Testing Type (Web / Application Penetration Testing, Network Penetration Testing, Cloud Penetration Testing, API Security Testing, Red Team/Advanced Simulation), by Deployment Model (Cloud-based PTaaS platform, Hybrid Deployment, On-premises), by End Use, by Regional Analysis, 2026–2033

Penetration Testing As Service Market Size and Trend Analysis

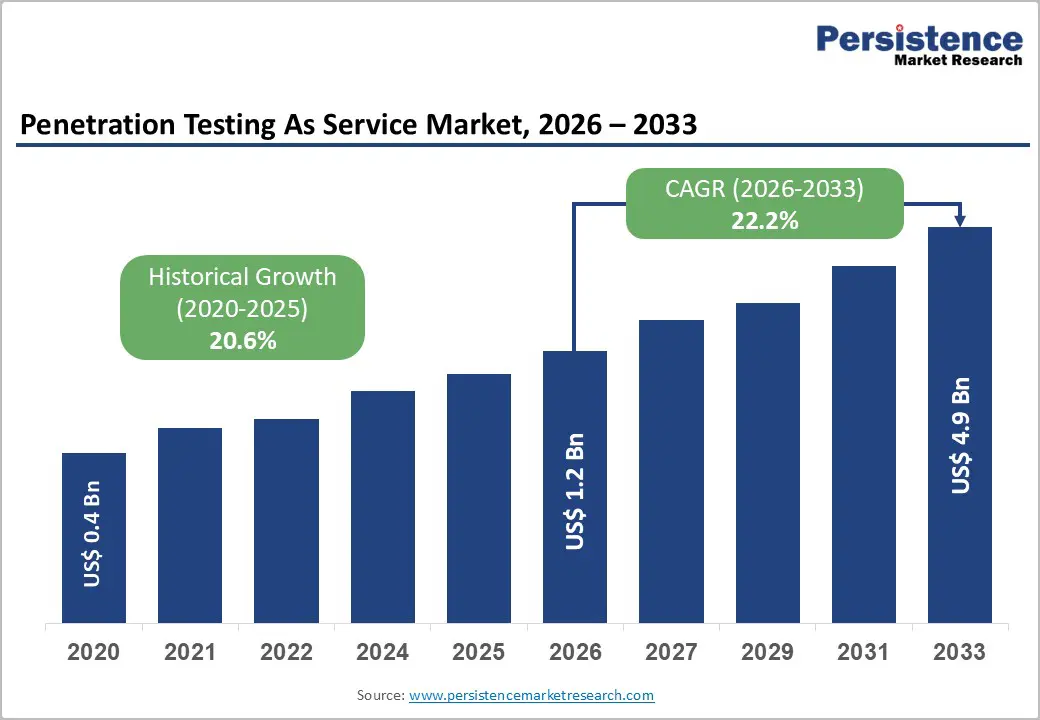

The global penetration testing as a service market is expected to be valued at US$ 1.20 Billion in 2026 and is projected to reach US$ 4.88 Billion by 2033, growing at a CAGR of 22.2% between 2026 and 2033.

The Global Penetration Testing as a Service (PTaaS) Market is experiencing rapid growth as organizations strengthen cybersecurity defenses against evolving threats and increasingly complex digital infrastructures. PTaaS combines expert-led security assessments with continuous testing platforms, enabling businesses to identify vulnerabilities, meet regulatory requirements, and improve security resilience across cloud, web, mobile, and enterprise environments.

Key Market Highlights

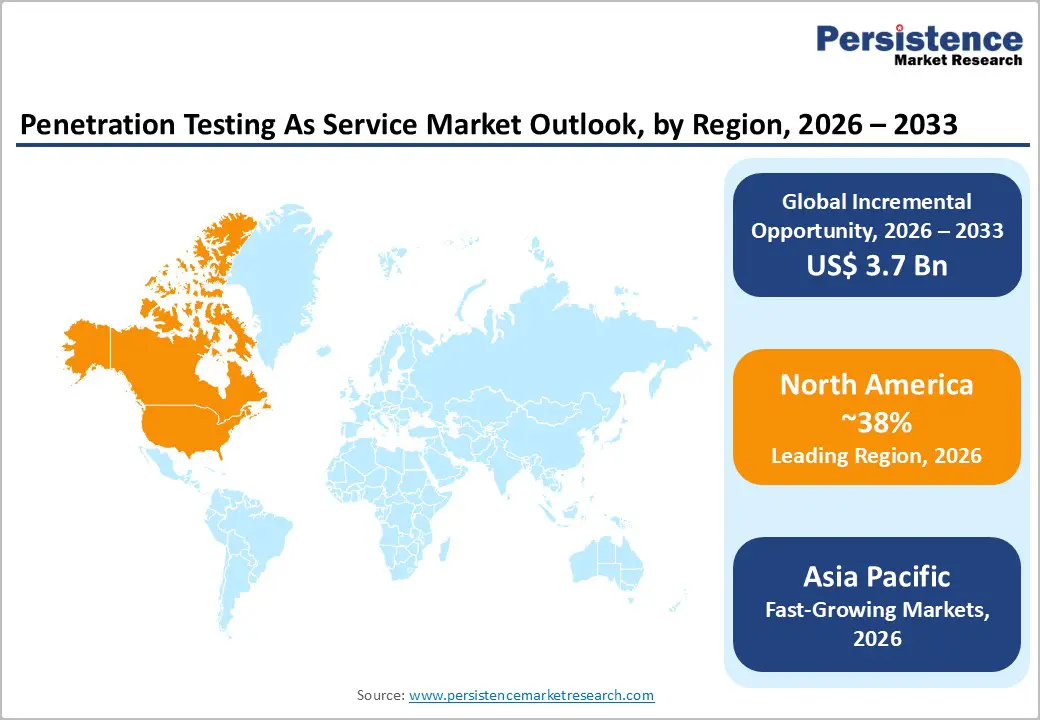

- Leading Region: North America holds 38.0% of the market, valued at US$ 0.46 Billion in 2026. Strong cybersecurity regulations, including SEC disclosure requirements, CISA mandates, and federal zero-trust initiatives, continue to drive PTaaS adoption and support the region’s market leadership through 2033.

- Fastest Growing Region: Asia Pacific is projected to grow at a CAGR of 27.8%, supported by expanding cybersecurity regulations in Singapore, India, and China. Increasing compliance requirements across major digital economies are expected to generate over US$ 0.80 Billion in annual PTaaS revenue by 2030.

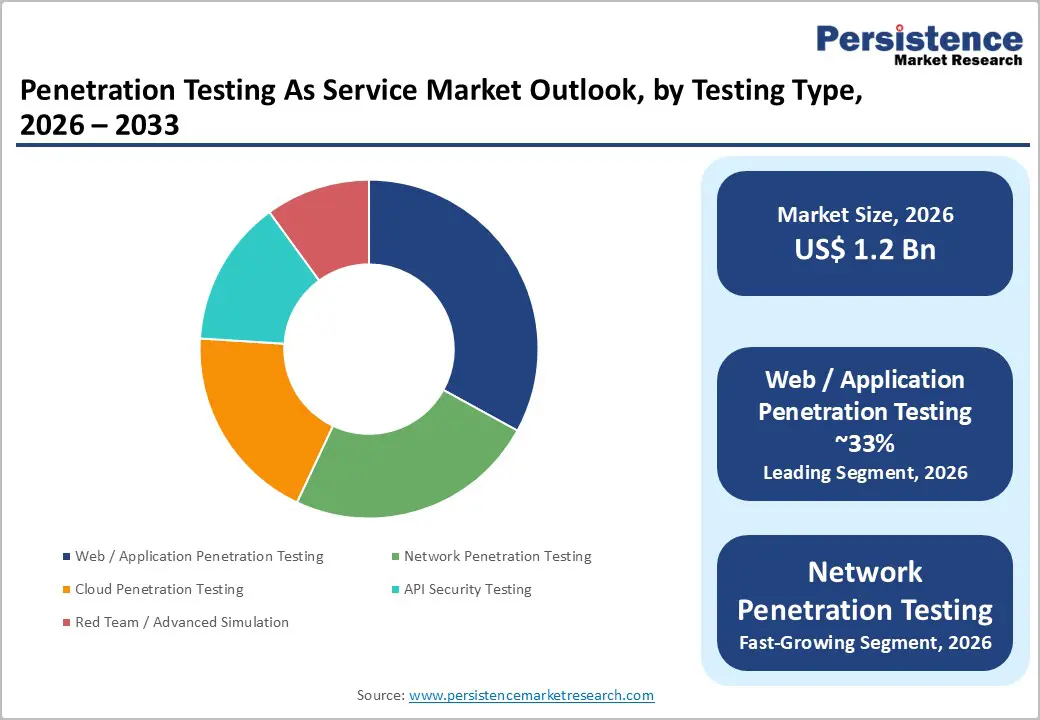

- Leading Segment: Web/Application Penetration Testing accounts for 33.0% of the market. Its leadership is driven by widespread adoption of OWASP standards, growing SaaS deployments, and increasing demand for SOC 2 and ISO 27001 compliance across industries.

- Fastest Growing Segment: Hybrid deployment is the fastest-growing segment, as organizations seek a balance between data sovereignty and cloud-based efficiency. Regulatory requirements such as CMMC 2.0 are accelerating adoption, particularly among defense-sector contractors.

- Key Opportunity: Small and medium-sized enterprises (50–500 employees) represent a major growth opportunity. Rising cyber insurance requirements and cybersecurity reporting obligations are driving demand for affordable PTaaS solutions with automated reporting and AI-assisted testing capabilities.

Market Dynamics

Market Growth Drivers

Regulatory Compliance Mandates Transforming Security Testing from Discretionary to Obligatory Spend

Compliance-driven purchasing now represents the single most durable demand floor for the penetration testing as a service market, because regulators are increasingly specifying testing frequency and methodology rather than leaving security posture to enterprise discretion. The Payment Card Industry Security Standards Council's PCI DSS v4.0, which became mandatory in March 2024, explicitly requires annual penetration testing of cardholder data environments and segmentation controls,

The European Union's NIS2 Directive, transposed into member-state law by October 2024, extends mandatory security testing obligations to over 160,000 entities across critical infrastructure sectors. Service providers that embed compliance reporting templates directly into their PTaaS platforms, as Coalfire did with its compliance-mapped testing workflows, will capture disproportionate wallet share from regulated industries over the next two to three years, as audit evidence generation becomes a core procurement criterion alongside raw technical capability.

Expanding Attack Surfaces Created by Cloud Migration and API-First Architectures

Every percentage point of workload shifted from on-premises data centres to public cloud environments creates a correspondingly larger, more dynamic attack surface that traditional scheduled penetration testing cannot adequately monitor, creating a structural tailwind for continuous PTaaS delivery models. Microsoft's 2023 Digital Defense Report documented over 156 trillion threat signals processed daily across its cloud infrastructure, underscoring the velocity at which new vulnerabilities emerge in multi-cloud environments.

Akamai Technologies reported in 2024 that API attacks accounted for 29% of all web application attacks it observed, validating PTaaS providers' rapid expansion into API security testing as a distinct service line. As enterprises accelerate hybrid cloud adoption through 2026 to 2028, PTaaS vendors offering automated, continuous cloud penetration testing integrated with cloud-native security posture management tools will command premium contract values and lower churn rates than point-solution competitors.

Market Restraints

Chronic Shortage of Qualified Ethical Hacking Talent Constraining Service Scalability

The penetration testing as a service market's growth trajectory faces a hard ceiling imposed by the global cybersecurity talent deficit, because PTaaS quality depends on skilled human testers who can simulate sophisticated adversary behaviour that automated scanners cannot replicate.

(ISC)² reported in its 2023 Cybersecurity Workforce Study that the global cybersecurity workforce gap reached 4 million professionals, with offensive security and red team specialists representing some of the scarcest sub-specialisms, a supply constraint that forces PTaaS providers to either cap client onboarding, accept longer engagement turnaround times, or dilute testing quality by substituting automation for human expertise. New entrants without established talent pipelines or crowdsourced researcher networks face a structural cost disadvantage of an estimated 30–40% premium on offensive security compensation relative to the broader IT sector, compressing operating margins at scale.

Data Sovereignty and Cross-Border Compliance Barriers Fragmenting Global Delivery Models

PTaaS platforms designed for centralised cloud delivery encounter significant friction when serving clients in jurisdictions with strict data residency requirements, because penetration test artefacts, including vulnerability evidence, system logs, and network topology data, frequently qualify as sensitive or regulated data under local law.

The EU General Data Protection Regulation (GDPR) and China's Personal Information Protection Law (PIPL), enacted in 2021, both impose restrictions on the cross-border transfer of data generated during security assessments, forcing PTaaS providers to build regionally isolated infrastructure that increases capital expenditure and operational complexity. Established providers with pre-existing regional cloud infrastructure absorb these compliance costs more readily than challengers, creating a structural moat that slows market entry and consolidates pricing power among a small number of globally capable incumbents.

Market Opportunities

Small and Mid-Market Enterprise Adoption Unlocking a Previously Underserved Demand Pool

Investors and PTaaS providers should prioritise building low-friction, self-service onboarding platforms targeting the SME segment, specifically companies with 50 to 500 employees, which historically lacked access to enterprise-grade penetration testing due to cost and complexity barriers that subscription-based PTaaS now eliminates.

The U.S. Small Business Administration identified cybersecurity as the top technology investment priority for SMEs in its 2024 technology adoption survey, and the Cyber Incident Reporting for Critical Infrastructure Act of 2022 is driving smaller critical infrastructure operators to adopt structured security validation for the first time to meet forthcoming mandatory incident reporting obligations. PTaaS platforms offering tiered subscription pricing below US$ 2,000 per month with automated scoping and AI-assisted reporting, as BreachLock has demonstrated with its AI-augmented delivery model, are best positioned to capture this segment, provided they can maintain test quality consistency at volume.

Embedded PTaaS With in Managed Security Service Provider Ecosystems

Managed Security Service Providers (MSSPs) represent an underutilised distribution channel through which PTaaS vendors can reach thousands of mid-market clients without building direct sales capacity, by white-labelling or co-branding continuous security testing as an add-on module to existing managed detection and response contracts.

Palo Alto Networks' acquisition of Talon Cyber Security in 2023 and its subsequent integration of offensive security capabilities into its Cortex XSIAM platform illustrate how security platform consolidation is creating bundled purchase decisions that reward PTaaS vendors with platform partnerships over standalone operators. For this opportunity to fully materialise, PTaaS providers must develop partner-ready APIs, MSSP-grade multi-tenancy architecture, and shared revenue models that align MSSP incentives with upselling continuous testing depth rather than minimising service time.

Category-wise Insights

Testing Type Analysis

Web / Application Penetration Testing accounts for 33.0% of the global penetration testing as a service market in 2026, equivalent to US$ 0.40 Billion, making it the leading testing type by a significant margin over network and cloud testing categories. Financial institutions conducting OWASP Top 10 assessments for customer-facing digital banking platforms, along with SaaS providers performing continuous application security testing before SOC 2 Type II certification audits, are the major demand drivers supporting this segment’s dominance.

Network Penetration Testing is emerging as the fastest growing testing type, supported by the increasing convergence of operational technology (OT) and IT networks across industrial environments where outdated infrastructure creates major security vulnerabilities. Manufacturing and energy companies are increasingly investing in specialised OT-focused testing to identify exploitable pathways that previously remained untested. Dragos Inc., which expanded its industrial cybersecurity offerings in 2024 to include OT-specific network penetration testing services, highlights how industrial cybersecurity is creating new demand beyond traditional IT security budgets.

Deployment Model Analysis

Cloud-based PTaaS platforms account for 60.0% of the global penetration testing as a service market in 2026, equivalent to US$ 0.72 Billion, reflecting strong enterprise preference for scalable delivery models that eliminate dependence on on-premises infrastructure while enabling continuous security testing. Mid-sized e-commerce companies operating on Amazon Web Services increasingly rely on cloud-native PTaaS dashboards to automate reconnaissance scans across production APIs and escalate detected vulnerabilities directly to human testers within integrated workflows.

Hybrid deployment is the fastest growing delivery model within the penetration testing as a service market, driven primarily by regulated industries that must maintain sensitive testing data within secure internal environments while still benefiting from cloud-based orchestration and reporting capabilities. Defence contractors complying with the U.S. Department of Defense’s Cybersecurity Maturity Model Certification (CMMC) 2.0 framework are increasingly adopting hybrid PTaaS models that allow testing agents to operate within protected networks while using approved cloud channels for coordination and reporting.

End Use Analysis

BFSI accounts for 25.0% of the global penetration testing as a service market in 2026, equivalent to US$ 0.30 Billion, making banking and financial services the largest end-use segment due to strict regulatory requirements and the severe financial and reputational impact of cybersecurity breaches. Leading commercial banks regularly conduct quarterly PTaaS engagements covering core banking APIs, mobile banking applications, and SWIFT payment network interfaces to strengthen operational resilience.

IT & Telecom is the fastest growing end-use segment in the penetration testing as a service market, driven by telecom operators’ increasing focus on securing 5G core network infrastructure and service-based architecture interfaces exposed to advanced signalling attacks. Major telecom equipment providers such as Ericsson and Nokia released multiple security advisories during 2023 and 2024 addressing vulnerabilities in legacy SS7 and Diameter protocol environments that continue to operate alongside new 5G deployments.

Regional Insights

North America Penetration Testing As Service Market Trends and Insights

North America accounts for 38.0% of the global penetration testing as a service market in 2026, representing US$ 0.46 Billion, anchored by the world's densest concentration of regulatory mandates, technology-forward enterprises, and mature cybersecurity procurement practices. The Biden Administration's National Cybersecurity Strategy, published in March 2023, designated offensive security validation as a core element of national cyber resilience, and Congress subsequently allocated US$ 3.1 Billion to CISA for cybersecurity capacity building, investment that cascades into private sector security testing demand through supply chain compliance requirements. North America's structural leadership will persist through 2033 as federal zero trust mandates propagate from government agencies into contractor and vendor ecosystems, continuously expanding the addressable buyer base for PTaaS engagements.

- United States Penetration Testing As Service Market Size

The United States constitutes an estimated 82% of the North American penetration testing as a service market, driven by the concentration of Fortune 500 financial institutions, federally regulated critical infrastructure operators, and cloud-native technology companies all operating under overlapping security testing mandates. The Federal Financial Institutions Examination Council (FFIEC) updated its IT Examination Handbook in 2023 to emphasise adversarial testing of authentication systems, pulling forward PTaaS adoption among community banks and credit unions previously reliant on annual vulnerability scans. Continued enforcement of the SEC cybersecurity disclosure rule will sustain U.S. demand growth through 2027 as public company audit committees formalise PTaaS as a standing board-reportable programme.

Europe Penetration Testing As Service Market Trends and Insights

Europe accounts for 25.0% of the global penetration testing as a service market in 2026, representing US$ 0.30 Billion, with demand concentrated in financial services, healthcare, and critical national infrastructure sectors responding to an exceptionally active regulatory legislative calendar between 2022 and 2025. The EU Digital Operational Resilience Act (DORA), which entered application in January 2025, requires financial entities operating in the EU to conduct Threat-Led Penetration Testing (TLPT) based on the TIBER-EU framework, a mandate that directly generates recurring PTaaS contract volumes across banks, insurers, and investment firms in all 27 member states. Europe's regulatory density creates a structurally higher baseline of mandatory PTaaS spending per regulated entity than any other global region, providing a durable demand floor through the forecast period.

- Germany Penetration Testing As Service Market Size

Germany represents an estimated 22% of the European penetration testing as a service market, reflecting its status as the EU's largest economy and home to a dense industrial manufacturing base increasingly targeted by state-sponsored threat actors. The German Federal Office for Information Security (BSI) mandated expanded cyber resilience testing for operators of critical infrastructure under the IT Security Act 2.0 (IT-SiG 2.0), enacted in 2021 with compliance timelines extending through 2024, creating a sustained wave of PTaaS procurement among energy, water, and automotive sector operators. Germany's Mittelstand manufacturing firms, estimated at over 3.5 million SMEs per Destatis data, represent a structurally underpenetrated PTaaS opportunity as supply chain cybersecurity requirements from OEM customers cascade downward.

- United Kingdom Penetration Testing As Service Market Size

The United Kingdom accounts for an estimated 19% of the European penetration testing as a service market, supported by London's position as Europe's leading financial centre and the National Cyber Security Centre (NCSC)'s influential CHECK scheme, which approves PTaaS providers for government and critical national infrastructure engagements. The UK Cyber Security and Resilience Bill, announced in the King's Speech of July 2024, proposes extending mandatory cyber incident reporting and security testing requirements to a broader range of digital service providers than covered under the existing NIS Regulations 2018. UK financial services firms face a parallel driver through the Bank of England's CBEST framework, which mandates intelligence-led penetration testing for systemically important financial institutions at least every three years.

- France Penetration Testing As Service Market Size

France contributes an estimated 14% of the European penetration testing as a service market, with the Agence Nationale de la Sécurité des Systèmes d'Information (ANSSI) serving as the primary driver of PTaaS adoption through its mandatory security qualification requirements for providers serving French critical infrastructure operators. ANSSI's PASSI (Prestataires d'Audit de la Sécurité des Systèmes d'Information) qualification scheme, requiring rigorous methodological certification before providers can conduct penetration tests on regulated systems, creates a credentialing barrier that concentrates market share among approximately 40 approved service providers. France's 2024 Olympic and Paralympic Games legacy investments in public digital infrastructure have extended the government's appetite for continuous security testing into public sector digital transformation programmes, providing incremental PTaaS demand through 2026.

Asia Pacific Penetration Testing As Service Market Trends and Insights

Asia Pacific accounts for 20.0% of the global penetration testing as a service market in 2026, representing US$ 0.24 Billion, and registers the fastest regional growth at a CAGR of 27.8%, driven by the combined force of rapid digital economy expansion, escalating nation-state cyber threat activity, and a wave of new cybersecurity legislation across major economies. Singapore's Cyber Security Agency (CSA) launched the Operational Technology Cybersecurity Masterplan 2.0 in 2024, mandating regular penetration testing of industrial control systems across critical information infrastructure sectors, establishing a regional policy template that Malaysia, Thailand, and Indonesia are actively replicating. Asia Pacific's PTaaS CAGR will exceed the global average through 2030 as regulatory frameworks in China, India, and ASEAN economies mature from awareness to enforcement, converting latent enterprise security spending into contracted PTaaS engagements.

- China Penetration Testing As Service Market Size

China accounts for an estimated 30% of the Asia Pacific penetration testing as a service market, with demand shaped primarily by the Multi-Level Protection Scheme (MLPS) 2.0, China's mandatory cybersecurity compliance framework, which requires graded security assessments including penetration testing for information systems classified at Level 3 and above. Domestic PTaaS providers including Qi An Xin Technology Group and DBAPPSecurity dominate the market due to data sovereignty requirements under the Cybersecurity Law of the People's Republic of China (2017) and the subsequent Data Security Law (2021), which effectively restrict foreign-operated testing platforms from accessing Chinese enterprise network environments. Continued MLPS 2.0 enforcement across state-owned enterprises and financial institutions will sustain double-digit PTaaS demand growth within China through 2028.

- India Penetration Testing As Service Market Size

India represents an estimated 25% of the Asia Pacific penetration testing as a service market, propelled by the Reserve Bank of India's 2023 circular mandating annual comprehensive cyber risk assessments, including penetration testing, for all regulated payment system operators and urban cooperative banks. India's Digital Personal Data Protection Act 2023 (DPDPA), which establishes data fiduciary obligations requiring demonstrable security safeguard validation, is expanding PTaaS demand beyond financial services into e-commerce, healthtech, and edtech platforms handling personal data at scale. India's IT services export sector, valued at over US$ 245 Billion per NASSCOM's FY2024 annual report, creates additional PTaaS demand as global enterprise clients require their Indian development and BPO partners to evidence application security through third-party testing certifications.

- Japan Penetration Testing As Service Market Size

Japan accounts for an estimated 20% of the Asia Pacific penetration testing as a service market, with PTaaS adoption accelerating following a series of high-profile breaches targeting Japanese critical infrastructure, including the 2023 JAXA (Japan Aerospace Exploration Agency) network intrusion and the Nagoya Port ransomware attack that disrupted Toyota Motor Corporation's parts logistics for three days. The Japanese government's 2022 National Security Strategy explicitly elevated offensive cyber capability development and mandated active cyber defence, spurring corresponding growth in private sector penetration testing demand as enterprises benchmark their defences against government-modelled threat scenarios. Japan's Financial Services Agency (FSA) expanded its cybersecurity assessment guidelines for financial institutions in 2024 to include scenario-based adversarial simulations, opening a new PTaaS procurement cycle across Japan's approximately 130 regionally chartered banks.

Competitive Landscape

The penetration testing as a service market operates as a moderately concentrated but rapidly fragmenting competitive landscape, with Synack, NetSPI, and Cobalt holding leading positions among pure-play PTaaS providers while IBM Security and Palo Alto Networks compete as integrated platform players commanding larger wallet share within existing enterprise security contracts.

Competition centres on three dimensions: tester quality and researcher network depth, platform automation sophistication, and compliance reporting breadth, with winners demonstrating all three simultaneously rather than excelling in isolation. HackerOne's pivot from bug bounty-only programmes toward structured PTaaS engagements in 2023 represents the most significant disruptive move, importing crowdsourced vulnerability discovery economics into the traditionally labour-intensive pen testing workflow and pressuring incumbent pricing on web application engagements specifically.

Key Market Developments

- January 2025: Synack announced integration of its AI-assisted vulnerability triage engine with ServiceNow's Security Incident Response module, enabling real-time PTaaS findings to populate enterprise GRC workflows automatically, eliminating manual reporting lag that previously extended remediation cycles by an average of 14 days.

- September 2024: NetSPI completed its acquisition of nVisium, a specialist application security testing firm, expanding NetSPI's web and mobile application penetration testing capacity by an estimated 40% and deepening its presence in the financial services and healthcare verticals.

- March 2024: Bugcrowd launched its AI Bias Bounty programme and expanded its PTaaS platform to include LLM (large language model) security testing as a distinct engagement type, becoming one of the first PTaaS providers to offer structured adversarial testing for generative AI applications in production environments.

Companies Covered in Penetration Testing As Service Market

- NetSPI

- Synack

- Cobalt

- HackerOne

- Bugcrowd

- Veracode

- Rapid7

- IBM Security

- Qualys

- Tenable

- BreachLock

- Synopsys

- Palo Alto Networks

- Secureworks

- Coalfire

- Trustwave

- NCC Group

- Bishop Fox

- Pentest People

- Offensive Security

Frequently Asked Questions

The global penetration testing as a service market is valued at US$ 1.20 Billion in 2026 and is forecast to reach US$ 4.88 Billion by 2033, expanding at a CAGR of 22.2%. The primary growth catalyst is the convergence of mandatory regulatory testing requirements, including PCI DSS v4.0 and the EU's NIS2 Directive, with enterprise adoption of continuous DevSecOps security validation frameworks.

Two structural forces are driving PTaaS market growth: mandatory adversarial testing requirements embedded in financial resilience frameworks such as the EU Digital Operational Resilience Act (DORA), effective January 2025, and the expansion of exploitable API attack surfaces, with Akamai documenting that API-targeted attacks constituted 29% of observed web application attacks in 2024. Together, these forces are converting security testing from a discretionary budget line into a mandated, recurring operational expenditure across regulated industries globally.

Web / Application Penetration Testing holds the largest share at 33.0% of the market in 2026, driven by universal enterprise reliance on customer-facing web platforms and the standardisation of testing scope through the OWASP Application Security Verification Standard, which reduces procurement complexity and sustains high repeat engagement rates. This segment's dominance is structurally stable because web application proliferation across every industry vertical continuously expands the addressable testing scope without requiring buyers to adopt new procurement frameworks.

North America dominates the penetration testing as a service market with 38.0% of global revenue in 2026, driven by the density of overlapping federal mandates, including OMB Memorandum M-22-09 on zero trust architecture and the FFIEC IT Examination Handbook updates of 2023, and the concentration of globally significant financial institutions requiring continuous adversarial validation. The United States alone accounts for approximately 82% of the North American total, and sustained federal cybersecurity investment through CISA will extend North America's regional leadership position well into the 2030s.

The highest-magnitude opportunity lies in productising PTaaS for the SME segment, specifically enterprises with 50 to 500 employees, where cyber insurance underwriters are beginning to require documented penetration test results as a policy condition, creating a commercially mandated buyer cohort that did not previously participate in structured PTaaS purchasing. MSSPs distributing PTaaS as a bundled module within managed detection and response contracts are best positioned to capture this opportunity at scale, provided they develop API-connected, multi-tenant PTaaS platforms that enable sub-US$ 2,000-per-month subscription economics.

Synack, NetSPI, Cobalt, HackerOne, and IBM Security are the leading companies in the penetration testing as a service market, competing across tester network depth, platform automation, and compliance reporting capability. The competitive landscape is moderately intense with low buyer switching costs at the platform level but high switching friction at the tester relationship level, meaning providers that combine researcher community quality with integrated GRC reporting, as Coalfire and Secureworks demonstrate within their enterprise client bases, retain accounts more durably than automation-only competitors.