- Healthcare IT

- Patient Record Management Market

Patient Record Management Market Size, Share and Growth Forecast, 2026 - 2033

Patient Record Management Market by Products (Solutions, Services), Delivery Mode (On-Premise, Web-Based, Cloud-Based), Applications (Patient Medical Records Management, Others), and Regional Analysis 2026 - 2033

Patient Record Management Market Share and Trends Analysis

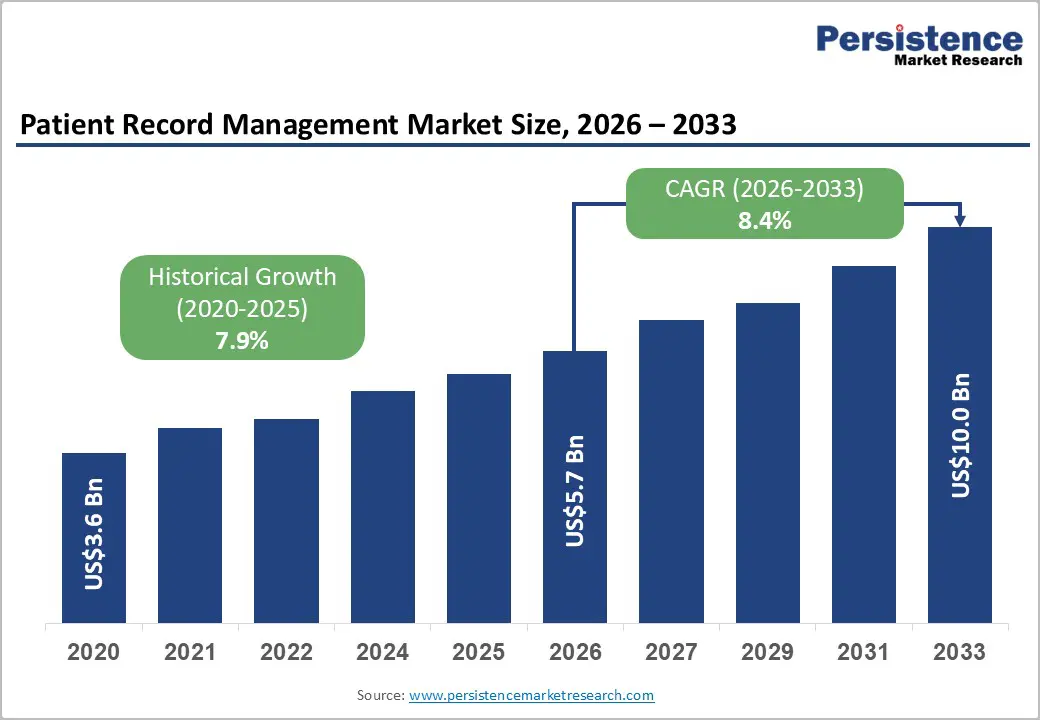

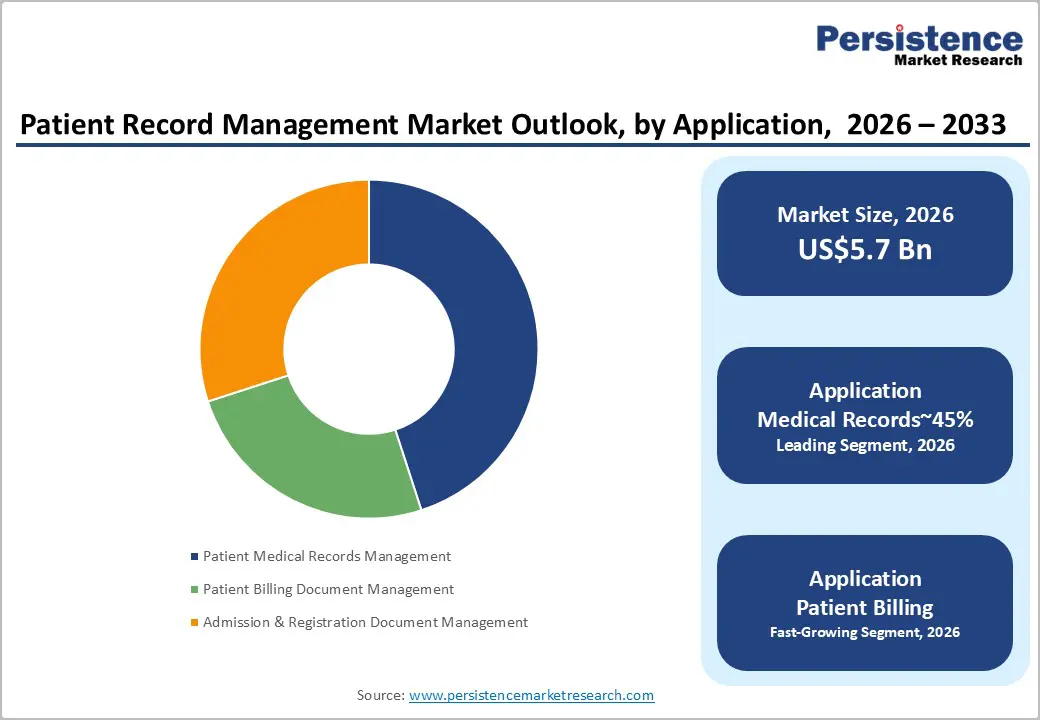

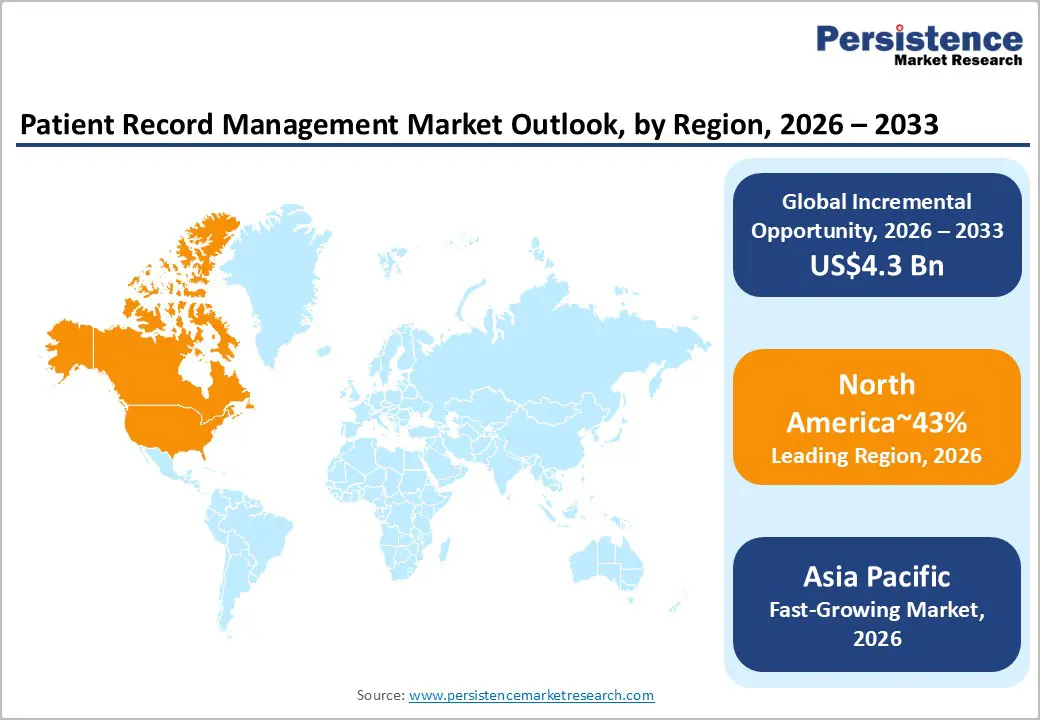

The global patient record management market is likely to be valued at US$5.7 billion in 2026 and is anticipated to reach US$10.0 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033, driven by providers adopting digital systems to streamline data access and compliance.

Cloud solutions dominate uptake as regulations push interoperability. Expansion accelerates through AI integration and rising patient volumes. Healthcare facilities prioritize centralized documentation to enhance diagnostic accuracy and operational agility. The sector remains on track to witness sustained technology procurement throughout the forecast period.

Key Industry Highlights:

- Leading Region: North America is projected to lead due to established digital health infrastructure and stringent regulatory requirements, accounting for approximately 43% share in 2026.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest due to national digital health initiatives, rising medical infrastructure investments, rapid urbanization, and government subsidies for electronic medical record systems.

- Leading Product Type: Solutions are expected to lead accounting with approximately 53% share in 2026, through high demand for comprehensive EHR systems integrating clinical documentation, scheduling, and billing.

- Leading Delivery Mode: Cloud-based delivery is projected to dominate for remote accessibility, instant patient data access from various locations, holding approximately 76% share in 2026.

- Leading Application: Patient medical records management is projected to dominate due to focus on longitudinal patient health, capturing accurate diagnostic history, and maintaining regulatory compliance with approximately 45% share in 2026.

- Competitive Environment: Major participants emphasize artificial intelligence integration and cloud-native architecture to differentiate their portfolios. Strategic alliances and regional expansions define current industry movements as providers seek broader geographic reach.

DRO Analysis

Driver - Chronic Disease Management Needs

Rising non-communicable disease prevalence intensifies the requirement for longitudinal patient monitoring and structured clinical data. According to the World Health Organization (WHO), chronic conditions represent 74% of deaths worldwide, necessitating enhanced documentation protocols. Clinics adopt sophisticated systems to track patient health metrics over extended durations. Consistent reporting ensures that clinicians make informed decisions based on historical medical trends. This pressure compels healthcare organizations to invest in high-capacity information storage frameworks.

The industry is forecast to expand as providers deploy Oracle with the Oracle Health Patient Portal. This technology simplifies complex medical terminology for patients using advanced conversational intelligence tools. Engaged patients utilize these portals to manage personal health information more effectively. Secure data accessibility encourages better adherence to prescribed treatment plans and clinical schedules. Improved patient understanding reinforces the clinical necessity for integrated record management solutions.

Workflow Automation and AI Integration

Administrative bottlenecks and physician burnout catalyze the demand for intelligent workflow automation in medical facilities. Modern systems incorporate machine learning to automate repetitive tasks such as coding and documentation. These enhancements allow clinicians to spend more time on direct patient interactions and diagnoses. Staff efficiency improves as automated tools handle massive volumes of incoming clinical information. Technology uptake surges as hospitals seek to optimize their labor resources and operational costs.

Technological adoption continues to rise as clinics implement Athenahealth with athenaOne Fall 2025. This platform leverages AI-native technology to reduce the manual workload for busy medical practices. Providers utilize these features to generate clinical document summaries and verify insurance details automatically. Streamlined operations ensure that facilities remain financially viable while delivering high-quality medical services. Automation represents a fundamental structural shift in professional healthcare management strategies.

Restraint - Cybersecurity Threats and Breach Costs

Frequent cyberattacks on healthcare infrastructure create significant financial and reputational barriers to technology implementation. High-value patient data attracts malicious actors seeking to exploit vulnerabilities in hospital network security. According to IBM, healthcare data breach costs reached US$9.77 million per incident. These liabilities force organizations to allocate substantial budgets toward defensive measures rather than system expansion. Security concerns often delay the adoption of interconnected digital record platforms.

Expansion is anticipated to slow where entities struggle with MEDITECH’s MEDITECH Expanse. Small facilities frequently face difficult trade-offs between advanced software capabilities and rising cybersecurity insurance premiums. Protecting unified patient records requires constant monitoring and expensive encryption updates across all clinical nodes. Legal consequences of data exposure discourage conservative providers from transitioning to fully digital environments. High risks associated with digital storage remain a primary deterrent for smaller clinical groups.

Implementation Complexity and Training Needs

Complex software installation processes and extensive staff training requirements hinder rapid technological deployment in medical centers. Transitioning from legacy paper-based systems or older digital tools involves significant operational downtime. Employees must learn new interfaces and data entry protocols to ensure clinical accuracy remains high. This learning curve often results in temporary productivity losses and physician resistance to change. Integration challenges complicate the alignment of various software modules within existing hospital networks.

Market uptake is expected to fluctuate as organizations deploy eClinicalWorks with Healow Genie AI. Integrating ambient computing features requires specialized hardware and robust network stability to function correctly. Clinicians must adapt to voice-activated tools and new ways of capturing patient encounter data. These logistical hurdles increase the total cost of ownership for modern management solutions. Technical complexity continues to limit the speed of implementation across underfunded public health systems.

High Capital Expenditure Requirements

High upfront costs for software licenses and infrastructure upgrades restrict the participation of budget-constrained hospitals. Large-scale digital transitions require significant investment in servers, high-speed networking, and mobile hardware. Annual maintenance fees and cloud subscription costs add to the long-term financial burden on clinics. Many facilities prioritize immediate clinical needs over expensive information technology projects during economic downturns. Financial limitations serve as a structural barrier to market expansion in developing regions.

Deployment is set to moderate as practitioners evaluate NextGen Healthcare’s NextGen Healthcare platform. Transitioning to a system of action necessitates significant financial commitments from ambulatory practices facing shrinking margins. Capital allocation remains tight as providers balance technology costs with rising labor and supply expenses. Investing in intelligent automation requires a clear return on investment that some facilities struggle to justify. Procurement cycles lengthen as organizations conduct thorough financial assessments before committing to new vendors.

Opportunity - Telehealth and Remote Monitoring

Increasing utilization of telehealth services expands the need for record management platforms that sync with remote tools. Patients require seamless access to their medical records during virtual consultations to ensure continuity of care. Integrating wearable device data into the primary record allows for real-time monitoring of vital signs. This connectivity bridges the gap between home-based care and professional medical facilities. Remote monitoring trends offer substantial opportunities for cloud-based vendors to broaden their service offerings.

Trajectory expansion is positioned to continue as providers implement InterSystems’ InterSystems TrakCare. This flexible electronic record system supports inpatient and outpatient workflows across diverse international healthcare markets. Clinicians utilize these tools to manage patient information during remote interactions and physical hospital stays. Enhanced interoperability ensures that medical data remains accessible regardless of the care delivery site. Evolving consumer preferences for convenient care drive the demand for portable digital health solutions.

Cloud-Enabled Imaging Integration

Merging diagnostic imaging data with standard medical records offers a more comprehensive view of patient health. Cloud-native storage allows for rapid sharing of high-resolution images across different clinical departments and hospitals. Centralized archives reduce the need for physical storage media and redundant imaging procedures. Clinicians benefit from having instant access to X-rays and MRI scans alongside laboratory results. This integration improves the speed and accuracy of medical diagnoses in urgent care environments.

The market is projected to expand as hospitals adopt GE Healthcare with Genesis cloud imaging. This portfolio utilizes software-as-a-service models to manage imaging dataflows through secure cloud pathways. Organizations redirect resources from managing physical hardware to focusing on higher-value clinical technology projects. Interoperable imaging archives facilitate better collaboration between radiologists and primary care physicians. Cloud-first strategies represent a vital technological evolution for modern diagnostic data management.

Category-wise Analysis

Product Type Insights

Solutions are forecast to lead the market, accounting for approximately 53% share in 2026, anchored by high demand for comprehensive EHR systems. These platforms integrate clinical documentation, scheduling, and billing into a unified digital interface. Facilities utilize IBM’s Patient Registry software to manage disease-specific data and track patient outcomes. Software procurement remains the primary driver of digital transformation within the modern healthcare sector.

Services are anticipated to be the fastest-growing segment, driven by complex system integration needs and ongoing maintenance requirements. Healthcare providers seek professional assistance to manage the migration of massive data volumes to new platforms. Organizations utilize IQVIA with Patient Registry software to leverage professional analytics and real-world evidence services. The expansion of professional consulting services reflects the rising technical complexity of health informatics.

Delivery Mode Insights

Cloud-based delivery is expected to dominate, accounting for approximately 76% share in 2026, underpinned by the shift toward remote accessibility. Medical professionals require instant access to patient data from various locations and devices. Hospitals utilize Health Catalyst’s Health Catalyst Patient Registry to store and analyze clinical information securely in the cloud. Reduced on-site hardware maintenance and lower capital expenditures favor the adoption of subscription-based delivery models.

The cloud segment is anticipated to be the fastest-growing segment, driven by rapid technology adoption in emerging medical markets. Developing regions bypass traditional on-premise installations in favor of scalable and cost-effective digital solutions. Facilities utilize UnitedHealth with Optum Patient Management to coordinate care through interconnected cloud networks. Real-time data synchronization allows for better management of patient flows and clinical resources across large territories.

Application Insights

The medical records application is forecast to lead, accounting for approximately 45% share in 2026, supported by the focus on longitudinal patient health. Capturing accurate diagnostic history and medication records remains the core function of clinical management systems. Providers utilize Epic Systems’ Epic EMR Software 2025 to ensure high-fidelity documentation across inpatient and outpatient care. Secure storage of sensitive medical data is critical for maintaining regulatory compliance and patient safety.

Patient billing is anticipated to be the fastest-growing segment, driven by the increasing complexity of reimbursement cycles. Medical practices require automated tools to manage insurance claims and minimize payment denials effectively. Organizations utilize Athenahealth with athenaOne Fall 2025 to streamline financial workflows and revenue cycle management. Integrated billing features reduce the administrative burden on office staff and improve cash flow.

Regional Analysis

North America Patient Record Management Market Trends

North America is expected to account for approximately 43% share in 2026, supported by established digital health infrastructure and stringent regulatory requirements. High healthcare spending facilitates the rapid adoption of advanced management software across large hospital networks. Regional policies mandate the use of interoperable systems to improve care quality.

U.S. Patient Record Management Market Trends

The U.S. is expected to dominate, driven by regulatory frameworks such as the HITECH Act and the 21st Century Cures Act. Epic Systems Corporation advances generative AI integration through ambient clinical documentation tools, improving workflow efficiency. Oracle Corporation strengthens market positioning through the expansion of unified healthcare data cloud platforms.

Canada Patient Record Management Market Trends

Canada is anticipated to lead growth, supported by provincial investments targeting the modernization of legacy healthcare IT systems. Federal and provincial data-sharing agreements accelerate the adoption of cloud-based interoperable health record platforms. TELUS Health expands virtual care solutions integrated with national patient data systems.

Europe Patient Record Management Market Trends

Europe is projected to remain a structurally stable market, with approximately 25% share, with demand anchored in compliance upgrades and cross-border interoperability initiatives. Strong data privacy laws necessitate the use of highly secure and localized record management solutions.

Germany Patient Record Management Market Trends

Germany is expected to dominate, driven by large-scale digitization initiatives under national healthcare funding frameworks. Siemens Healthineers strengthens diagnostic data integration through AI-enabled platforms such as Teamplay. Elekta AB supports oncology data management through advanced patient record systems in clinical workflows.

U.K. Market Patient Record Management Market Trends

The U.K. is anticipated to lead, supported by centralized healthcare data transformation initiatives across national systems. Palantir Technologies enables large-scale data integration through national healthcare data platforms. Oracle Corporation and Epic Systems Corporation remain embedded within core hospital record infrastructures. Adoption of modular software procurement strategies strengthens analytical capabilities and real-time resource planning across healthcare networks.

Asia Pacific Patient Record Management Market Trends

Asia Pacific is anticipated to register the fastest expansion, as national digital health initiatives and rising medical infrastructure investments accelerate uptake. Rapid urbanization and growing middle-class populations drive the demand for high-quality healthcare services.

China Patient Record Management Market Trends

China is expected to dominate, supported by strong policy mandates under national healthcare modernization frameworks. Dassault Systèmes advances clinical data management through Medidata platforms, enabling streamlined trials and patient record integration. Growth of internet-based healthcare ecosystems by Tencent and Alibaba Group strengthens mobile-first patient data management.

Japan Patient Record Management Market Trends

Japan is anticipated to lead, supported by aging demographics requiring highly interoperable healthcare record systems. Fujitsu and NEC Corporation enable secure data exchange through advanced digital infrastructure solutions. National platforms for lifetime medical record access strengthen patient-centric care coordination.

Competitive Landscape

The global patient record management market reflects a consolidated structure dominated by enterprise technology vendors with extensive clinical deployments. Oracle with Oracle Health Patient Portal strengthens patient engagement through cloud-based interoperability and data accessibility. Epic Systems with Epic EMR Software reinforces dominance via large hospital network integrations and predictive analytics capabilities. These players leverage cybersecurity investments and scalable architectures to maintain procurement leadership across institutional healthcare environments.

Competitive dynamics increasingly emphasize artificial intelligence integration and specialized clinical modules across diverse care settings. NextGen Healthcare targets ambulatory segments with value-focused cloud platforms, while Health Catalyst advances registry-driven outcomes tracking. Innovation centers on ambient AI, predictive diagnostics, and real-time data orchestration, shifting competition toward execution efficiency and integrated patient journey management.

Key Industry Developments:

- In February 2026, Epic Systems launched its built-in "AI Charting" solution to automate ambient clinical documentation. This move directly challenges third-party AI scribe vendors by embedding native ambient listening into the EHR, significantly reducing clinician burnout and administrative time.

- In January 2026, ‘Oracle Health’ announced the expansion of its acute care functionality for its next-generation AI-driven EHR. By moving beyond ambulatory care into full acute care settings, Oracle is positioning its voice-first, AI-native platform to compete for large-scale hospital system contracts.

Companies Covered in Patient Record Management Market

- Epic Systems Corporation

- Oracle Corporation

- athenahealth, Inc.

- MEDITECH

- eClinicalWorks LLC

- NextGen Healthcare, Inc.

- InterSystems Corporation

- GE HealthCare Technologies Inc.

- IBM Corporation

- IQVIA Holdings Inc.

- UnitedHealth Group Incorporated

- Health Catalyst, Inc.

- Dassault Systèmes SE

- Conduent Incorporated

- Veradigm Inc.

- Elekta AB

Frequently Asked Questions

The global patient record management market is projected at US$5.7 billion in 2026, reaching US$10.0 billion by 2033.

Frequent cyberattacks impose high financial liabilities, with breach costs around, diverting budgets from system expansion.

The global patient record management market is expected to grow at a CAGR of 8.4% from 2026 to 2033.

Asia Pacific is the fastest-growing region, driven by digital health initiatives and expanding medical infrastructure investments.

Key players include Epic Systems Corporation, Oracle Corporation, athenahealth, MEDITECH, eClinicalWorks, NextGen Healthcare, InterSystems Corporation, GE HealthCare, IBM, IQVIA, UnitedHealth Group, and Health Catalyst.