Industry: Healthcare

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 180

Report ID: PMRREP35185

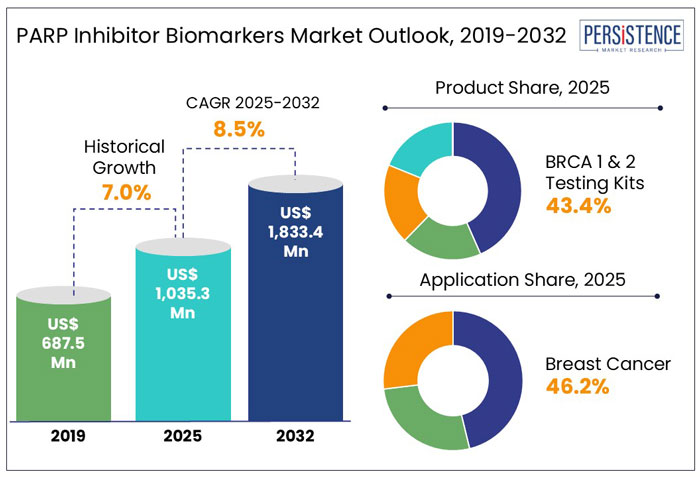

The global PARP inhibitor biomarkers market size is set to rise at a CAGR of 8.5% from 2025 to 2032. It is anticipated to be valued at US$ 1,833.4 Mn by 2032 from US$ 1,035.3 Mn in 2025.

PARP inhibitors, a type of targeted therapy, is commonly used to treat cancers like breast and ovarian cancer by targeting protein - PARP, or poly (ADP-ribose) polymerase. It helps repair damaged DNA. PARP inhibitors target cancer cells with DNA repair deficiencies, such as those caused by mutations in the BRCA1 or BRCA2 genes.

Biomarkers like BRCA mutations or other DNA repair defects help identify patients most likely to respond to PARP treatment. Rising prevalence of cancer, high demand for personalized medicine, and integration of companion diagnostics are projected to fuel market growth.

Key Highlights

|

Global Market Attributes |

Key Insights |

|

PARP Inhibitor Biomarkers Market Size (2025E) |

US$ 1,035.3 Mn |

|

Market Value Forecast (2032F) |

US$ 1,833.4 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

8.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.0% |

Historical Period Saw Discovery of New Biomarkers to Treat Different Cancer Types Apart from Ovarian Cancer

As per Persistence Market Research, the global market for PARP inhibitor biomarkers exhibited a CAGR of 7.0% from 2019 to 2024. PARP inhibitors were initially used to treat ovarian cancer, particularly in patients with BRCA mutations.

Discovery of biomarkers such as BRCA1/2 mutations and Homologous Recombination Deficiency (HRD), however, extended the use of PARP inhibitor therapy to other cancers like breast, prostate, and pancreatic cancer. Development of new biomarkers and broadening of indications significantly contributed to market growth during the historical period.

Research Work to Give Rise to Targeted Therapies and Personalized Medicine in Forecast Period

The global market is projected to witness a CAGR of 8.5% in the forecast period. Increasing awareness of personalized medicine and targeted therapies in cancer treatment will likely spur the global market to rise substantially.

Personalized medicine involves proteomic, genetic, and immunological profiling to provide therapeutic alternatives as well as prognostic insights into cancer. Targeted therapies, on the other hand, focus on selecting the most effective treatment based on the molecular characteristics of malignant cancer.

Several clinical trials are underway exploring PARP inhibitors to assess their efficacy in treating various cancers beyond ovarian cancer as well as their combinations with immunotherapies. Wider acceptance of PARP inhibitors is anticipated to offer more customized and effective treatments for cancer patients worldwide through 2032.

Innovations in Biomarker-based Companion Diagnostics for Precision Medicine to Propel Growth

Biomarker-based companion diagnostics allows for the identification of specific genetic or molecular markers. It also helps in guiding personalized treatment decisions to ensure right therapy is provided to patients based on their unique biomarker profile.

Growing focus on innovating enhanced biomarker testing for precision medicine is driving developments in personalized cancer therapies. This includes developing more sensitive, accurate, and comprehensive diagnostic tools to ensure administration of PARP inhibitors and other targeted treatments to the right patients.

In March 2024, for example, Labcorp revealed results from two studies demonstrating the critical role of biomarker testing in bridging gaps and guiding targeted therapies for patients with Epithelial Ovarian Cancer (EOC). Similarly, in August 2024, Foundation Medicine unveiled the development of the HRDsig1 biomarker, a HRD signature integrated into the FoundationOne®CDx comprehensive genomic profiling test.

In April 2024, Bio-Rad launched an ultrasensitive multiplexed PCR assay for breast cancer mutation detection. This assay increases the sensitivity and precision of biomarker testing, enabling more accurate mutation detection for PARP inhibitor therapies. Hence, increasing research activities by several academic institutions and leading players are set to propel development and efficacy of biomarker-driven treatments in oncology, thereby boosting the market globally.

Clinical Challenges of PARPi Resistance and Identification of Patients Beyond BRCA1/2 PVs for Treatment May Limit Growth

PARP inhibitors (PARPi) have demonstrated remarkable efficacy in cancer treatment associated with BRCA mutations and other HR deficiencies. BRCA1/2 mutations significantly increase the risk of developing breast cancer (60 to 70%) and ovarian cancer (15 to 40%) in women, making PARPi a significant treatment option for such patients.

Despite their promising activity in patients with HR-tumors, resistance to these therapies may develop over time. This is attributed to various mechanism factors such as reactivation of DNA repair pathways, secondary mutations, and epigenetic regulation of BRCA genes. Changes in tumor biology that bypass or limit PARPi's effectiveness in long-term treatment may also limit efficacy.

Studies have revealed that ovarian cancer has one of the poorest prognoses among all gynecologic malignancies. The most prevalent subtype, i.e., high-grade serous carcinoma, is frequently diagnosed at advanced stages with a reported 5-year survival rate of just 30%.

It creates significant hurdles for healthcare providers, as patients initially respond to PARPi therapies, only to experience relapses over time. Hence, it often complicates treatment regimens and leads to disease progression.

Identifying patients beyond BRCA1/2 pathogenic variants (PVs) who could benefit from PARPi treatment remains a challenge. Historically, PARPi has been the most effective in patients with BRCA1/2 mutations. However, recent evidence shows its effectiveness in other gene mutations such as ATM, PALB2, and RAD51C.

Identifying these patients requires precise and comprehensive biomarker testing to broaden the population eligible for PARPi therapies. Ongoing research into combination therapies to counteract resistance mechanisms and the development of new biomarkers will likely be crucial to boost PARP inhibitor therapies and enhance their effectiveness in cancer treatment.

PARP Inhibitors Propel Developments in Cancer Treatment with Expanding Clinical Applications

Globally, more than 18 Mn cases of cancer are diagnosed every year, with an estimated 9.7 Mn cancer-related deaths recorded as of 2022, placing a huge burden on healthcare systems. In recent years, developments in targeted therapies like PARPi have gained significant momentum.

Several PARP inhibitors have been approved for BRCA-mutated ovarian, breast and pancreatic cancer treatment. More than 300 clinical trials are currently underway to examine the use of PARP inhibitors as an anti-cancer therapy in chemo-resistant germline or somatic BRCA1/2 mutated breast, lung, ovarian, and pancreatic cancers.

PARPi veliparib (ABT-888) is currently undergoing various clinical trials to understand its efficacy in treating patients with High-Grade Glioma (HGG), advanced solid tumors, and HER2-negative metastatic breast cancer. Exploration of new PARP inhibitor’s efficacy and applicability is set to propel demand for novel biomarker assays, opening new avenues for companies to innovate next generation diagnostic platforms.

BRCA 1 and 2 Testing Kits Gain Momentum due to Ability to Detect Patients with Hereditary Cancer Risk

BRCA 1 and 2 testing kits segment is set to account for a PARP inhibitor biomarkers market share of 43.4% in 2025. BRCA mutations are well-known biomarkers for PARP inhibitor therapies. This makes BRCA testing an important diagnostic tool to identify patients with hereditary cancer risk, particularly ovarian and breast cancers. It also offers more personalized treatment.

Compared to other testing kits such as Homologous Recombination Deficiency (HRD) or Homologous Recombination Repair (HRR), BRCA 1 and 2 testing is more widely recognized to be used for patient selection in PARP inhibitor therapies, contributing to its high share. A key challenge of HRD testing kits is their high cost due to the involvement of complex genetic analysis. HRR testing kits, on the other hand, require next-generation sequencing to assess various genes, making these more expensive than single-gene tests.

Strong Clinical Evidence to Accelerate PARP Inhibitor Adoption in Breast Cancer Treatment

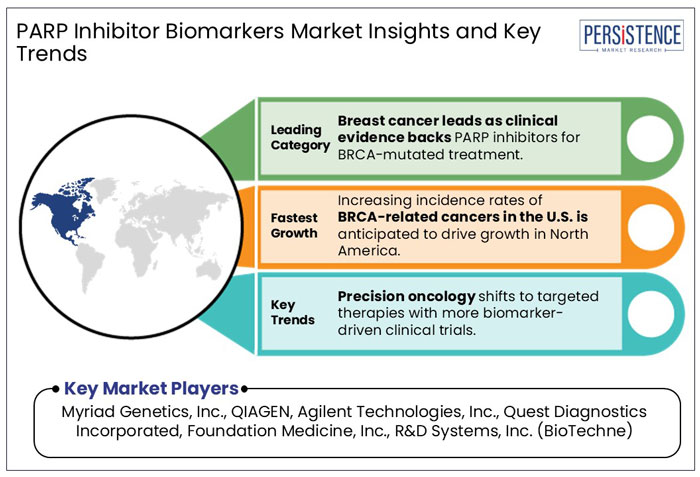

The breast cancer segment is anticipated to lead with a share of 46.2% in 2025. This is due to its high prevalence and the strong clinical evidence supporting the use of PARP inhibitors in treating BRCA-mutated breast cancer. As per the International Agency for Research on Cancer (IARC) 2025 report, nearly 2.3 Mn new breast cancer cases were reported in 2022, while 670,000 breast cancer-related deaths occurred globally.

PARP inhibitors like Olaparib have been successfully approved and used for the treatment of breast cancer with BRCA mutation, driving the segment’s growth, while outpacing other cancers like ovarian cancer or other less common indications. The identification of BRCA biomarkers has become a key factor in personalized cancer treatment, enabling more precise targeting and improved outcomes with PARP inhibitors.

Ovarian cancer, on the other hand, is anticipated to see moderate growth through 2032. It is because not all ovarian cancer patients are eligible for this treatment. HRD status and BRCA mutations are the main biomarkers used to assess patient responses.

Only about 20 to 25% of ovarian cancer patients, however, have BRCA1/2 mutations, while another 30 to 40% have tumors that are HRD-positive. This implies that a sizable fraction of patients (30 to 50%) is ineligible for PARP inhibitor therapy, which restricts its application.

Increasing Prevalence of BRCA-related Cancers to Create High Demand in the U.S.

North America is projected to hold 42.7% of the global market share in 2025, driven by rising clinical demand for BRCA1/2 testing and precision oncology solutions. In the U.S., breast and ovarian cancers are among the most prevalent cancers.

Currently, there are more than 4 Mn U.S. women with a history of breast cancer. Nearly 316,950 women are set to be newly diagnosed in 2025 with invasive breast cancer and 59,080 new cases of non-invasive ductal carcinoma in situ (DCIS). Additionally, ovarian cancer is anticipated to account for more than 20,000 new cases in 2025.

High incidence rates of BRCA-related cancers are set to significantly fuel demand for biomarker testing in treatment selection. BRCA mutations are a key biomarker in determining the effectiveness of PARP inhibitors. Growing need for precision oncology solutions targeting specific genetic mutations is projected to spur the U.S. PARP inhibitor biomarkers market.

Collaboration efforts of key players for biomarker testing combined with a focus on innovative biomarker-based therapies, is also likely to support growth. In January 2024, Myriad announced its endorsement of the new American Society of Clinical Oncology (ASCO) and Society of Surgical Oncology (SSO) guideline for germline testing in breast cancer patients. The updated guideline provides comprehensive, evidence-based recommendations for clinical practice, reflecting industry's focus on accelerating biomarker-based clinical practices.

Rising Adoption of Genetic Testing to Strengthen Demand for Biomarker Assays in Europe

Europe is anticipated to generate a significant share of 28.4% in 2025. It is a key market for assay manufacturers owing to widespread acceptance of genetic testing, strong regulatory framework, and the ongoing expansion of personalized cancer therapies.

The Cancer Care 2025 study revealed that the number of new oncology medicines approved in Europe has accelerated in the past 5 years, backed by scientific advances and innovations delivering targeted therapies and immunotherapies. This is set to continue as PARP inhibitors show promising results, particularly in cancers related to gene mutations and malignancies.

Countries like Germany and the U.K. have seen increasing integration of biomarker-driven therapies, with collaborations between pharmaceutical companies and research institutions. Several companies are extending their biomarker test offerings in Europe, particularly for BRCA mutations. These collaborations and strategic market efforts are important for the ongoing success and growth of Europe’s market.

Government Support for Precision Medicine to Boost Use of PARP Inhibitors in Japan

Asia Pacific is estimated to rise at 9.6% CAGR from 2025 to 2032. Increasing adoption of personalized cancer therapies and rising focus on precision oncology in countries like Japan, China, and India are significantly driving the regional market.

Notably, Japan plays a key role in boosting demand for PARP inhibitor biomarker testing. Studies like those from Oda et al. revealed that 21.5% of ovarian cancer patients in Japan tested positive for gBRCA mutations, while 60% had HRD mutations, indicating a substantial patient population eligible for PARP inhibitor therapies. Yoshihara et al. reported that 45.2% of ovarian cancer patients in Japan exhibited HRR mutations, further extending the need for accelerating biomarker testing, boosting Japan’s market growth.

The country’s government supports precision medicine through initiatives like the Japan Agency for Medical Research and Development (AMED), It funds cancer research and trials, encouraging the use of PARP inhibitors in clinical practice. These efforts are critical to extending access to cutting-edge cancer treatments in the country.

The global market for PARP inhibitor biomarkers is highly competitive with key players focusing on collaborations with diagnostic companies. They aim to offer innovative biomarkers and diagnostic tools to enhance patient selection and improve treatment outcomes.

|

Attributes |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Product:

By Application:

By End User:

By Region:

To know more about delivery timeline for this report Contact Sales

The global market is set to reach US$ 1,035.3 Mn in 2025.

By product, BRCA 1 and 2 testing kits are projected to dominate the global market in 2025.

Myriad Genetics, Inc., Illumina, Inc., QIAGEN, and Agilent Technologies, Inc. are a few key players.

The industry is estimated to rise at a CAGR of 8.5% through 2032.

North America is projected to hold the largest share of the industry in 2025.