- Food Ingredients & Additives

- Palm Oil Market

Palm Oil Market Size, Share, and Growth Forecast 2026 – 2033

Palm Oil Market by Product Type (Crude Palm Oil [CPO], Palm Kernel Oil [PKO], Fractionated Palm Oil, Red Palm Oil, Oleic Palm Oil), by Nature (Organic, Conventional, Fillers, Others), by End User (Food & Beverage Industry, Cosmetics & Personal Care, Biofuel & Energy, Pharmaceuticals, Others), by Regional Analysis, 2026–2033

Palm Oil Market Share and Trends Analysis

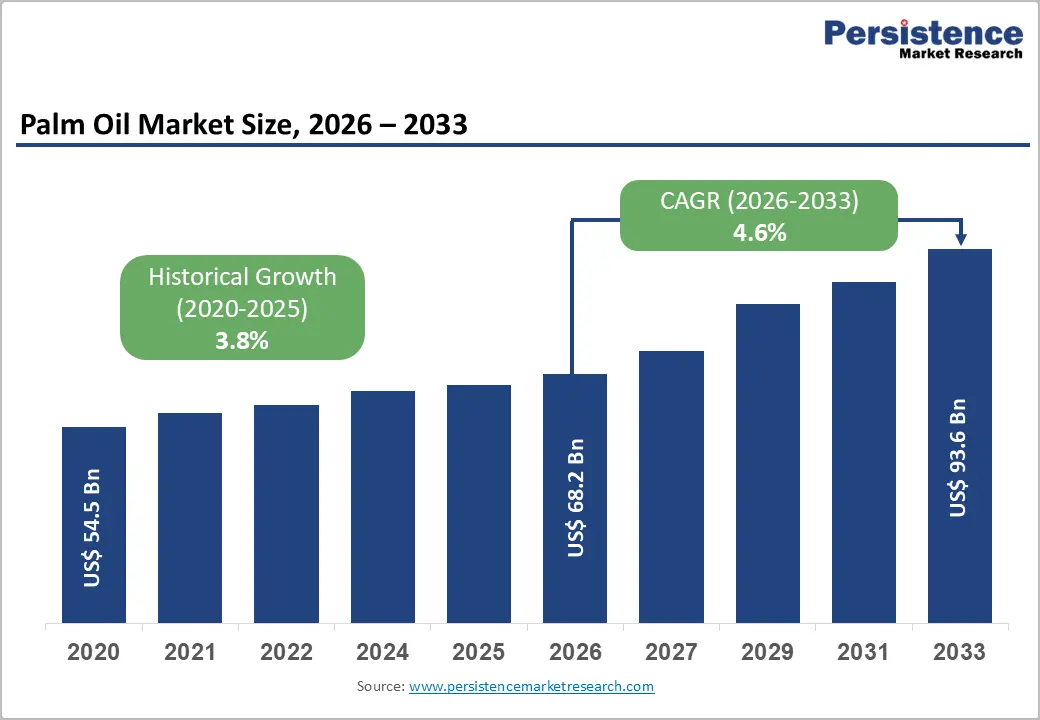

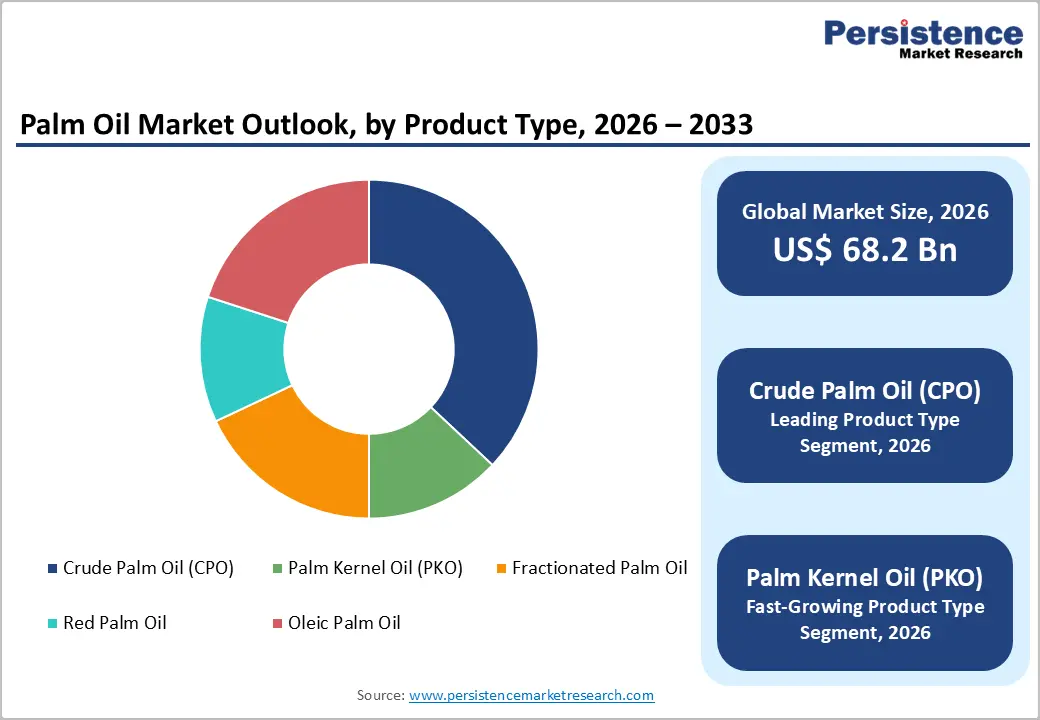

The global Palm Oil market size is expected to be valued at US$ 68.2 billion in 2026 and projected to reach US$ 93.6 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

The Palm Oil Market is growing steadily due to its wide application across food and beverage, cosmetics, personal care, biofuel, pharmaceuticals, and industrial sectors. Palm oil is valued for its high yield, cost-effectiveness, long shelf life, and versatile functional properties in cooking oils, bakery products, processed foods, soaps, and biodiesel production. Rising demand for renewable energy and increasing use in sustainable fuel applications are further supporting market growth. Emerging economies in Asia Pacific and Africa continue to drive production and consumption. Sustainability initiatives and certified sourcing practices are also becoming important factors shaping global market expansion.

Key Industry Highlights

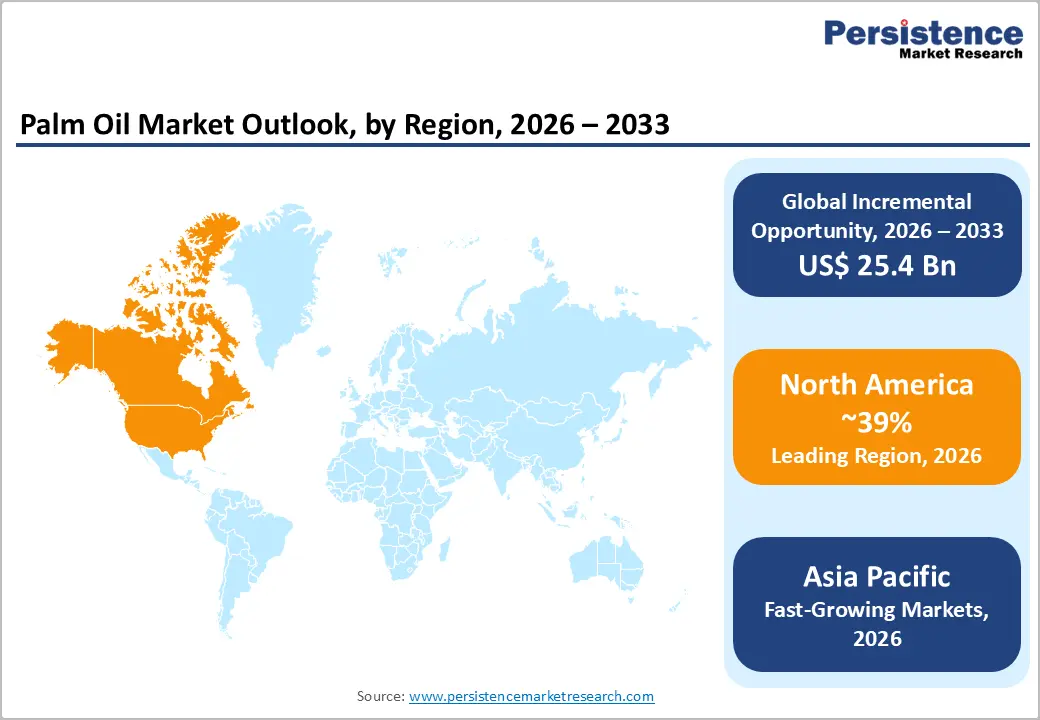

- Leading Region – North America: North America holds approximately 39% of the global Palm Oil market share in 2025, driven by the U.S.'s large food processing and oleochemical industries importing 1.1–1.3 million metric tonnes annually per USDA, combined with growing RSPO-certified procurement commitments from major U.S. FMCG corporations.

- Fast-Growing Market– Asia Pacific: Asia Pacific is the fastest-growing palm oil market through 2033, anchored by India's world-leading imports of 8–9 million metric tonnes annually, China's 5–6 million metric tonnes import demand, and rapidly expanding processed food manufacturing sectors across ASEAN markets driving consistent regional consumption growth.

- Dominant Product Segment – Crude Palm Oil (CPO): Crude Palm Oil leads the Product Type category with approximately 37% market share in 2025, reflecting its role as the primary traded palm oil commodity 77 million metric tonnes produced globally per FAO/USDA data serving as feedstock for all downstream refined and derivative products globally.

- Fast-Growing Product Segment – Palm Kernel Oil (PKO): Palm Kernel Oil is the fastest-growing product type, driven by its critical role as a lauric acid source for oleochemicals and personal care products aligned with the €80 billion+ European cosmetics market per Cosmetics Europe data and expanding Asia Pacific personal care consumption.

Market Dynamics

Market Growth Drivers

Global Food Security Demand and Palm Oil's Dominant Role in Edible Oils Supply

Palm oil's structural dominance in the global edible oils market remains the single most important commercial demand driver, rooted in its exceptional productivity, functional versatility, and cost competitiveness compared to alternative vegetable oils. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service, palm oil accounted for approximately 38–40% of global vegetable oil production in 2022/23, more than soybean oil (29%) and all other oils combined a structural supply advantage driven by oil palm's yield of approximately 3.8 tonnes of oil per hectare, roughly 5–10 times greater than soybean or rapeseed. The FAO projects that global food demand will increase by 70% by 2050, with edible oil demand growing proportionally as caloric intake rises across developing economies in Sub-Saharan Africa, South Asia, and Southeast Asia, where palm oil is a primary cooking and food processing staple.

Biofuel Mandates in Indonesia and Malaysia Driving Sustained Industrial Palm Oil Demand

Government-mandated biofuel blending programs in the two largest palm oil-producing nations Indonesia and Malaysia are creating a significant structural industrial demand driver that supports palm oil price floors and production volumes. Indonesia's B35 biodiesel blending mandate requiring 35% palm oil-derived biodiesel in diesel fuel was implemented in February 2023 by the Indonesian Ministry of Energy and Mineral Resources, absorbing millions of metric tonnes of crude palm oil (CPO) annually into domestic biofuel production. Malaysia's B20 biodiesel mandate similarly supports domestic CPO absorption. The Roundtable on Sustainable Palm Oil (RSPO) estimates that biofuel applications account for approximately 15–20% of global palm oil consumption, and with both governments signaling potential mandate escalation to B40 and beyond, biofuel demand is expected to provide a durable upward pricing and volume support mechanism through the forecast period.

Market Restraints

EU Deforestation Regulation and Sustainability Compliance Costs Restricting Market Access

The European Union Deforestation Regulation (EUDR), which entered application in late 2024, represents the most significant regulatory barrier facing the palm oil market's access to European consumers and food manufacturers. Under EUDR, companies must demonstrate that palm oil and derived products have not contributed to deforestation or forest degradation after December 31, 2020. Non-compliant palm oil imports face EU market exclusion. This regulation imposes substantial supply chain traceability investment requirements on producers and traders, disproportionately affecting smallholder farmers who lack digital traceability infrastructure. The RSPO estimates that full EUDR compliance across the palm oil supply chain could take several years to implement at scale, creating near-term market access risk for European-destined palm oil volumes and increasing compliance costs.

Price Volatility Linked to Weather Events and Competing Vegetable Oil Dynamics

Palm oil is subject to significant commodity price volatility driven by weather-related production disruptions in Indonesia and Malaysia, which together account for approximately 85% of global supply. El Niño and La Niña climate cycles directly impact oil palm yields through drought and flooding effects, causing CPO price swings of 30–50% within single growing seasons. Per the USDA, palm oil prices reached record highs in 2022 before sharp corrections in 2023, creating financial planning uncertainty for buyers and processors. This volatility, combined with competitive price dynamics with soybean oil, particularly following Argentine export policy shifts, complicates long-term supply contract management for industrial buyers and restrains predictable market volume growth.

Market Opportunities

Palm Kernel Oil (PKO) Growth Driven by Cosmetics and Oleochemical Sector Demand

Palm Kernel Oil (PKO) represents the fastest-growing product segment within the Palm Oil market, driven by its critical and expanding role as a feedstock for the global oleochemical and cosmetics industries. PKO's high lauric acid content, similar to coconut oil makes it the preferred raw material for the production of surfactants, fatty acids, fatty alcohols, and glycerol used extensively in personal care products, detergents, and specialty chemicals. The European Oleochemicals and Allied Products Group (APAG) reports growing oleochemical production across European and Asian processing hubs, where PKO serves as a key lauric acid feedstock. Rising global demand for personal care products, the Cosmetics Europe industry association reports the European cosmetics market generates over €80 billion in sales annually, combined with expanding Asian personal care consumption, makes PKO's compound growth trajectory among the strongest within the broader palm oil complex in the coming years.

Sustainable and Certified Palm Oil Premiums Creating Commercial Differentiation Opportunity

The accelerating corporate sustainability procurement agenda among global FMCG companies, retailers, and food manufacturers is creating a significant commercial opportunity for producers and traders supplying RSPO-certified sustainable palm oil at price premiums. Major global brands, including Unilever, Nestlé, Procter & Gamble, and L'Oréal, have made binding sustainable palm oil sourcing commitments, generating demand for certified volumes.

The RSPO reports that certified sustainable palm oil (CSPO) production has grown to over 21 million metric tonnes annually, but uptake still lags certified supply creating both a market development challenge and an opportunity for producers investing in third-party certification and supply chain transparency. As the EUDR enforcement creates hard market access barriers, RSPO-certified and deforestation-free supply will command genuine price premiums in premium consumer goods supply chains through 2033.

Category-wise Analysis

Product Type Insights

Crude Palm Oil (CPO) is the dominant product type in the palm oil market, accounting for approximately 37% of total market share in 2025. CPO's leading position reflects its role as the primary traded commodity form of palm oil extracted from the mesocarp of the oil palm fruit through mechanical pressing that serves as the feedstock for virtually all downstream refined palm oil products, fractionated derivatives, and oleochemical inputs.

According to the USDA Foreign Agricultural Service, global CPO production exceeded 77 million metric tonnes in the 2022/23 marketing year, with Indonesia accounting for approximately 58% and Malaysia 23% of global supply. CPO's price-benchmark status on the Bursa Malaysia Derivatives Exchange makes it the reference product for all palm oil pricing globally, ensuring its central commercial and volume-dominant position within the market structure through the forecast period.

Nature Insights

Conventional palm oil represents the dominant nature segment in the palm oil market, accounting for approximately 88% of total volume in 2025. Conventional palm oil's overwhelming dominance reflects the practical reality of global supply chain scale. The vast majority of palm oil plantations in Indonesia and Malaysia operate under conventional (non-organic) frameworks, and the volume economics of global food manufacturing, biofuel production, and oleochemical processing prioritize price competitiveness and supply reliability over organic certification. The RSPO certification system the primary sustainability certification for conventional palm oil provides a more commercially practicable framework than organic certification for volume buyers. While organic palm oil commands meaningful price premiums in specialty food, cosmetics, and nutraceutical segments, its production scale remains a fraction of total supply, with conventional product dominating food manufacturing and industrial procurement globally.

End-user Insights

The food & beverage Industry is the leading end-user segment of the palm oil market, accounting for approximately 60–65% of total consumption in 2025. Palm oil's food industry dominance is structurally embedded in its functional properties high oxidative stability, semi-solid consistency at room temperature, neutral flavor profile, and cost competitiveness making it ideal for frying oils, margarine, shortening, confectionery fats, bakery products, and processed food applications.

The FAO and USDA data consistently confirm that edible uses account for the majority of global palm oil consumption, with India, China, the European Union, and Pakistan among the world's largest importing nations for food applications. Indonesia's and Malaysia's domestic food manufacturing sectors also generate substantial internal consumption, further cementing the Food & Beverage industry's dominant and structurally stable end-user share globally.

Regional Insights

North America Palm Oil Market Trends and Insights

North America leads the Palm Oil market with approximately 39% of global market share in 2025 driven primarily by the United States' large-scale food processing, oleochemical, and personal care industries that consume significant palm oil volumes, combined with active biofuel blending demand and growing sustainable sourcing commitments from major U.S. food and FMCG corporations aligning with RSPO certification procurement policies.

U.S. Palm Oil Market Size

The United States accounts for approximately 87% of the North American Palm Oil market revenue. The U.S. imports approximately 1.1–1.3 million metric tonnes of palm oil and palm kernel oil annually per USDA data, primarily for food manufacturing (snacks, baked goods, spreads), oleochemicals for personal care, and biofuel feedstock. U.S. EPA Renewable Fuel Standard (RFS) compliance drives industrial demand.

Europe Palm Oil Market Trends and Insights

Europe is a major palm oil-consuming region, though market access is increasingly shaped by the EU Deforestation Regulation (EUDR) implementation, which is compelling importers and food manufacturers to prioritize RSPO-certified and traceable supply chains. The region's strong sustainability mandates from the European Commission and active consumer advocacy for deforestation-free sourcing are driving premiumization toward certified palm oil across European food, personal care, and oleochemical industries.

Germany Palm Oil Market Size

Germany accounts for approximately 20–22% of the European Palm Oil market share, driven by its large food manufacturing and oleochemical processing sectors. Germany is one of Europe's largest palm oil importers per European Palm Oil Alliance (EPOA) data, with food processors, detergent manufacturers, and personal care companies relying on palm oil derivatives. Germany's active EUDR compliance programs are accelerating certified supply chain adoption.

U.K. Palm Oil Market Size

The United Kingdom holds approximately 14–16% of the European Palm Oil market share. The U.K. food industry, including major retailers including Tesco, Sainsbury's, and Marks & Spencer, has some of Europe's most advanced certified sustainable palm oil procurement policies, with UK Roundtable on Sustainable Palm Oil (RSPO UK) members accounting for significant proportions of U.K. palm oil imports under certified supply chains.

France Palm Oil Market Size

France accounts for approximately 14% of the European market share. France has maintained a notably complex relationship with palm oil. The Nutri-score and labeling debates led to public discourse on palm oil in food products, but the ingredient remains essential for French food manufacturing, confectionery, and personal care industries. French EUDR compliance is being actively managed by major food companies, including Danone and L'Oréal.

Asia Pacific Palm Oil Market Trends and Insights

Asia Pacific is the fastest-growing regional Palm Oil market and also home to the world's largest producers, Indonesia and Malaysia, making the region simultaneously the dominant supply hub and an enormous consumption market. China, the world's second-largest palm oil importer, imports approximately 5–6 million metric tonnes annually per USDA data for food processing, oleochemicals, and industrial applications, and its import volumes closely track domestic economic and consumer demand cycles. Intraregional palm oil trade across ASEAN is expanding in parallel with regional food manufacturing growth.

India Palm Oil Market Size

India is the world's largest palm oil importer, accounting for approximately 25–28% of the Asia Pacific market share and importing approximately 8–9 million metric tonnes annually, according to the Solvent Extractors' Association of India (SEA) data. India's dependence on edible oil imports, with palm oil constituting over 60% of its vegetable oil imports, combined with government incentives under the National Mission on Edible Oils – Oil Palm (NMEO-OP) program, drives consistent high-volume demand.

Competitive Landscape

The global Palm Oil market is moderately consolidated at the production and trading level, with Wilmar International Ltd., Golden Agri-Resources Ltd., IOI Corp Bhd, Sime Darby Oils, Musim Mas Group, and Apical Group collectively accounting for a significant proportion of global refining and trading volumes. Cargill and Archer Daniels Midland lead the multinational trader segment. Key competitive differentiators include RSPO certification breadth, traceability platform investment, geographic refining network coverage, and EUDR compliance capabilities. Emerging business model trends include sustainability-linked supply chain financing, blockchain-based traceability platforms, and smallholder support programs that enable certified sustainable palm oil volume scaling at the plantation level.

Key Developments:

- In November 2024, the first shipment of RSPO-Identity Preserved (IP) Certified Sustainable Palm Oil reached the Shanghai Port, marking a key turning point for China’s market. Under the RSPO group membership of Wilmar, Inner Mongolia Yili Industrial Group (Yili Group), Asia's top dairy brand, led this innovative endeavor in collaboration with Yihai Kerry Arawana Holdings Co., Ltd (Yihai Kerry), China's largest palm oil trader.

- In July 2024, members of the Indonesian Peasants Union (SPI) inaugurated a new Oil Palm Plantation Cooperative in Sei Kopas Village, Asahan Regency, North Sumatra, aiming to boost the province’s palm oil sector significantly.

Global Palm Oil Market – Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 54.5 billion |

|

Current Market Value (2026) |

US$ 68.2 billion |

|

Projected Market Value (2033) |

US$ 93.6 billion |

|

CAGR (2026–2033) |

4.6% |

|

Leading Region |

North America, ~39% market share in 2025 |

|

Dominant Category (Product Type) |

Crude Palm Oil (CPO), ~37% market share in 2025 |

|

Top-ranking Category (End User) |

Food & Beverage Industry, ~60–65% consumption share in 2025 |

|

Incremental Opportunity |

US$ 25.4 billion (Absolute Dollar Opportunity, 2026–2033) |

Companies Covered in Palm Oil Market

- Olam International

- Archer Daniels Midland Company

- Presco PLC

- Agarwal Industries Pvt. Ltd.

- DAO

- Asian Agri

- Apical Group Ltd.

- IOI Corp Bhd

- Oleo-Fats, Incorporated

- Agropalma Group

- Golden Agri-Resources Ltd.

- Sime Darby Oils Liverpool Refinery Ltd.

- Cargill, Incorporated

Frequently Asked Questions

The global Palm Oil market is expected to be valued at US$ 68.2 billion in 2026.

Primary demand drivers include palm oil's structural position as the world's most produced vegetable oil exceeding 77 million metric tonnes per FAO/USDA data combined with Indonesia's B35 biodiesel mandate absorbing millions of additional CPO tonnes annually, rising food demand from developing economies per FAO's projection of 70% food demand growth by 2050, and growing PKO demand from the oleochemicals and cosmetics sectors.

North America leads the global Palm Oil market with approximately 39% of market share in 2025.

The most significant opportunities are in RSPO-certified and EUDR-compliant sustainable palm oil supply where major FMCG brands' sustainability commitments and EU market access requirements are creating premium pricing corridors and in Palm Kernel Oil's (PKO) growing oleochemical and cosmetics applications, aligned with the €80 billion European cosmetics sector and Asia Pacific personal care market expansion through 2033.

The Palm Oil market is led by global players including Wilmar International Ltd., Golden Agri-Resources Ltd., IOI Corp Bhd, Sime Darby Oils, Musim Mas Group, Apical Group Ltd., Cargill Incorporated, Archer Daniels Midland Company, Olam International, Agropalma Group, Asian Agri, Presco PLC, and Oleo-Fats Incorporated.