- Medical Devices

- Orthokeratology Lens Market

Orthokeratology Lens Market Size, Share, and Growth Forecast, 2026 - 2033

Orthokeratology Lens Market by Product Type (Overnight Ortho-K lenses, Day-time Ortho-K lenses), Indication (Presbyopia, Others), Distribution Channels (Optometry Clinics, Ophthalmology Clinics, Hospitals, Others), and Regional Analysis for 2026 - 2033

Orthokeratology Lens Market Size and Trends Analysis

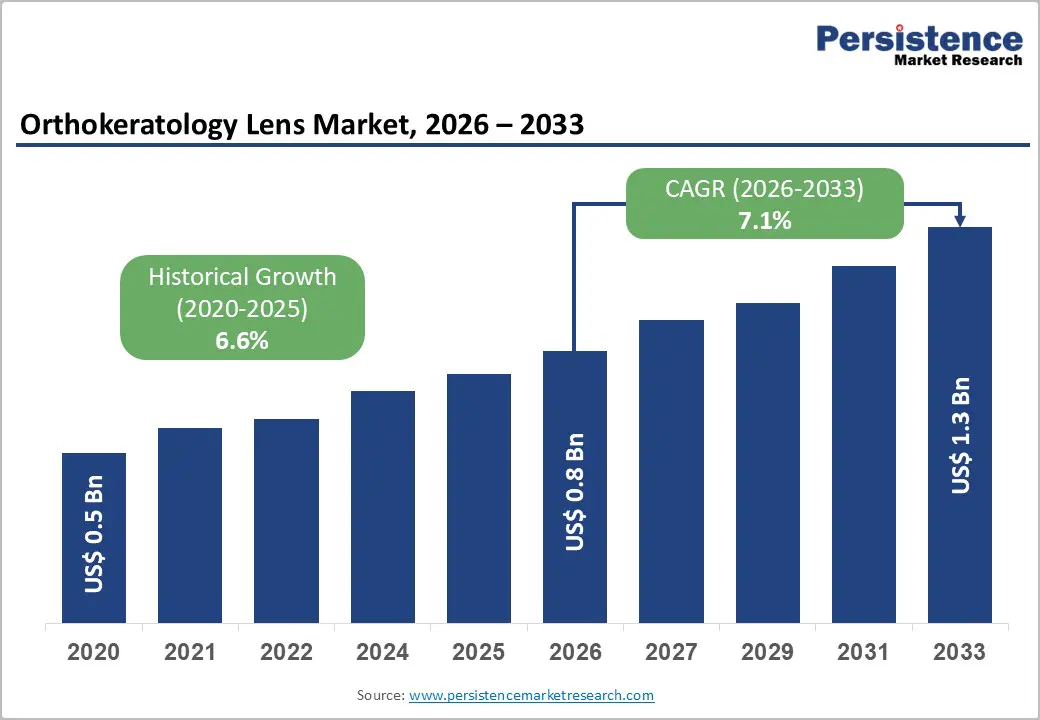

The global orthokeratology lens market size is likely to be valued at US$0.8 billion in 2026 and is expected to reach US$1.3 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033, driven by rising myopia prevalence and demand for non-surgical vision correction.

Growth is further supported by increasing clinical adoption, advances in lens materials and digital fitting technologies, expanding eye care infrastructure in emerging markets, and growing preference for preventive vision correction among children and young adults.

Key Industry Highlights:

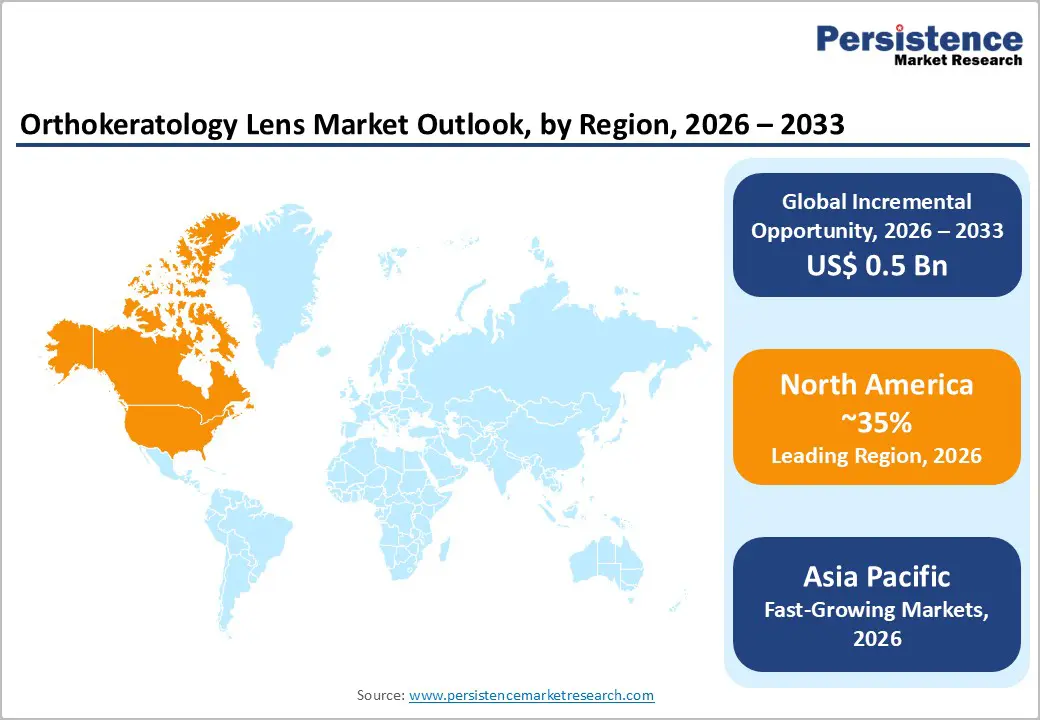

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by high myopia and advanced eye care.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by high myopia prevalence and early onset of refractive errors.

- Leading Product Type: Overnight Ortho-K lenses are projected to represent the leading product type in 2026, accounting for 60% of the revenue share, driven by superior clinical efficacy in myopia control and convenience for pediatric patients.

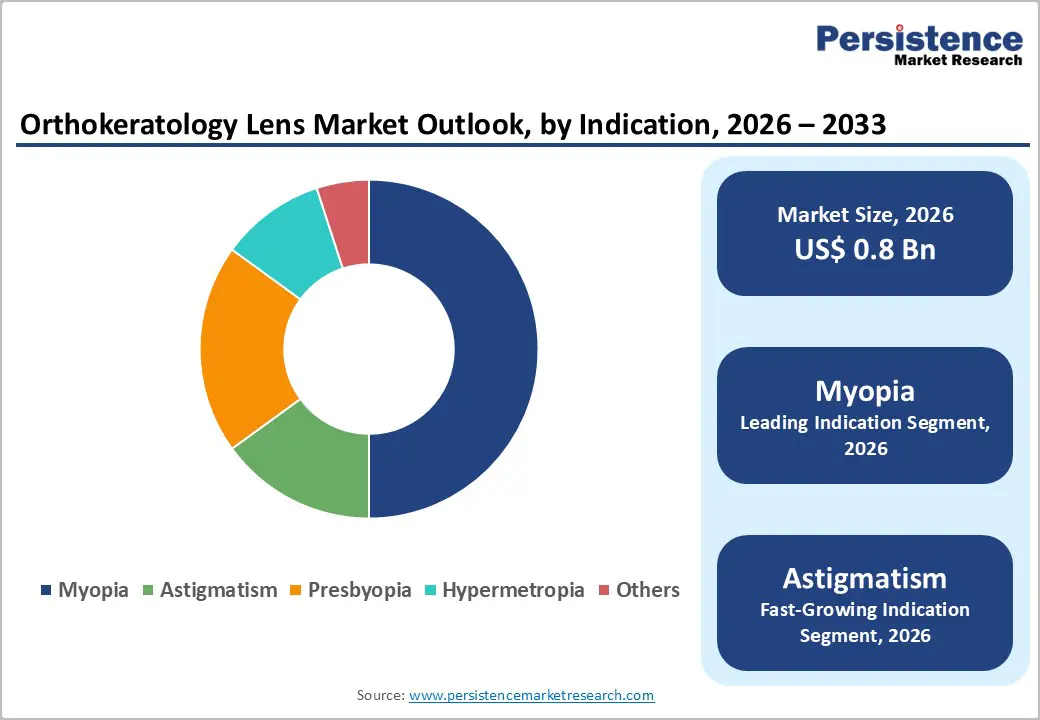

- Leading Indication Type: Myopia is anticipated to be the leading indication type, accounting for over 70% of the revenue share in 2026, supported by rising pediatric prevalence and early intervention programs.

| Key Insights | Details |

|---|---|

|

Orthokeratology Lens Market Size (2026E) |

US$0.8 Bn |

|

Market Value Forecast (2033F) |

US$1.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.6% |

DRO Analysis

Driver - Rising Prevalence of Myopia

The increase in myopia (nearsightedness) has directly elevated demand for corrective approaches that manage progression and reduce long-term complications. Public health data show that refractive errors such as myopia are a leading cause of distance vision impairment globally and contribute significantly to vision-related disability. According to the World Health Organization (2025), refractive errors remain one of the foremost causes of visual impairment worldwide, affecting 2.2 billion and imposing heavy social and economic burdens on health systems and productivity, with unmet needs particularly acute in lower-resource settings.

This epidemiologic trend underpins market demand for solutions that can both correct vision and address progression risks, particularly among paediatric and adolescent cohorts where onset typically occurs. Increased prevalence elevates the total addressable population, drives routine optometric care utilization, and encourages adoption of interventions that offer measurable benefits beyond simple refractive correction.

Restraint - Limited Awareness and Training among Providers

Vision care providers must maintain a broad clinical skill set to diagnose, manage, and treat diverse eye conditions highlighted as public health objectives by the Centers for Disease Control and Prevention (CDC) Vision Health Initiative, which identifies vision impairment as a substantial contributor to disability and emphasizes the need for comprehensive services for all populations. The specialized clinical competence required for overnight corneal reshaping treatment extends beyond standard optometric practice and demands targeted training that many practitioners have not yet integrated into routine education, leading to uneven availability of qualified specialists.

This disparity in clinical exposure and professional development contributes to a limited recognition of available non-surgical therapeutic alternatives among providers and patients alike. The absence of uniform training pathways and standardized certification for advanced refractive care creates inconsistent practice patterns across regions, diminishing referral networks, and slowing clinical adoption rates.

Opportunity - Technological Convergence and Digital Health Integration

The convergence of advanced imaging, cloud-based analytics, and real-time remote monitoring platforms will catalyze transformative shifts in care pathways by supporting earlier detection, precision fitting, and ongoing performance tracking. High-resolution corneal topography combined with digital health records enables clinicians to tailor interventions based on individualized eye maps and longitudinal data trends rather than episodic in-office assessments, which enhances clinical efficiency and patient-centric care delivery.

Public health frameworks in the U.S. recognize the value of integrating vision care with broader health systems, with the Centers for Disease Control and Prevention (CDC) emphasizing digital and telehealth modalities as mechanisms to expand access and improve outcomes for eye health interventions under initiatives such as the Vision Health Initiative. According to CDC surveillance, innovative service delivery models that include remote screening and digital engagement contribute to improved access to vision services, with increased emphasis on technologies that support community-based screening and early intervention.

Category-wise Analysis

Product Type Insights

Overnight Ortho-K lenses are expected to lead, accounting for approximately 60% of revenue in 2026, driven by superior clinical efficacy in myopia control and convenience for pediatric patients. These lenses are worn during sleep, temporarily reshaping the cornea, providing clear vision during daytime without additional corrective devices. A prominent example is Paragon CRT Lens, which is widely prescribed for overnight wear and has demonstrated strong clinical outcomes in slowing myopia progression among children.

Day-time Ortho-K lenses are likely to represent the fastest-growing segment, as they offer continuous vision correction during waking hours without overnight wear. Advancements in material permeability, lens hydration, and patient-specific customization enhance safety and comfort. For instance, Euclid Emerald Toric Orthokeratology Lens demonstrates how advanced customization and high oxygen-permeable materials are expanding the scope of orthokeratology into more flexible and patient-specific applications, supporting future innovation toward alternative wear modalities.

Indication Type Insights

Myopia is projected to lead the market, capturing around 70% of the revenue share in 2026, supported by its increasing prevalence in pediatric and adolescent populations. Awareness among caregivers and early intervention programs in schools enhances adoption. A well-known example is MiSight 1 day, which, although a soft lens, reflects the growing clinical emphasis on structured myopia control strategies similar to Ortho-K approaches.

Astigmatism is likely to be the fastest-growing indication type, driven by rising recognition of its impact on vision quality and increasing demand for corrective solutions beyond standard myopia management. For example, the Paragon CRT Dual Axis Lens is specifically designed to address corneal astigmatism by incorporating dual-axis geometry, demonstrating how toric Ortho-K lens innovations are enabling more accurate and customized treatment for patients with complex refractive errors.

Regional Insights

North America Orthokeratology Lens Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by a combination of systemic clinical adoption, entrenched professional networks, and regulatory clarity that together elevate market penetration relative to other regions. The U.S. and Canada report high prevalence of myopia and refractive errors in adult and youth populations, driving demand for non-surgical corrective options. This demand is amplified by proactive professional education and integrated myopia management programs.

Sustained dominance is also shaped by concentrated leadership among manufacturers and service providers whose research, development, and distribution hubs are rooted in the U.S. and Canada. Local regulatory oversight by the U.S. Food and Drug Administration (FDA) ensures a clear pathway for premarket approvals and product refinements that align with rigorous safety and performance expectations, encouraging investment in next-generation designs and niche clinical applications.

Europe Orthokeratology Lens Market Trends

Europe is likely to be a significant market for orthokeratology lenses, due to well-established healthcare infrastructure and high standards of clinical practice. Countries such as Germany and the U.K. report growing prevalence of myopia among adolescents, creating sustained demand for non-surgical refractive interventions. Public health initiatives emphasize early vision screening and corrective strategies, which enhance the adoption of overnight corneal reshaping lenses.

France and Italy exhibit expanding clinical networks supported by structured professional training programs that promote adoption among pediatric and specialty populations. Regulatory oversight ensures adherence to stringent safety and performance standards, fostering trust in innovative lens designs and encouraging investment from manufacturers. Consumers demonstrate elevated willingness to pay for advanced corrective solutions, supported by reimbursement frameworks for vision care and preventive interventions.

Asia Pacific Orthokeratology Lens Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by an unprecedented demand for myopia-management solutions, driven by high prevalence rates among youth and adults. In Singapore, official health data show that approximately 65% of children aged 12 years are myopic, a level among the highest in the world. This intense clinical need fuels substantial uptake of non-surgical corrective strategies, including overnight reshaping lenses, as parents and healthcare practitioners seek interventions that mitigate long-term vision deterioration.

Rapid urbanization, intensive near-work academic environments, and increased digital screen exposure create an early onset of refractive errors, prompting government-linked public health screening programs that detect and manage vision issues at earlier ages. India shows rising urban myopia prevalence and expanding middle-class access to advanced eye care, which broadens the base for advanced corrective devices.

Competitive Landscape

The global orthokeratology lens market demonstrates moderate fragmentation, with several regional players shaping competitive dynamics. Key participants such as CooperVision, Bausch & Lomb Inc., MiracLens L.L.C., Alpha Corporation (Menicon Group), and Johnson & Johnson Vision Care, Inc. collectively capture a significant portion of market share, establishing strong brand recognition and clinical credibility. These companies leverage advanced manufacturing capabilities and proprietary lens designs to differentiate offerings, targeting both pediatric and adult segments with specialized solutions.

Market positioning emphasizes quality of service, material performance, and strategic collaborations with eye care providers and research institutions. Leading players focus on strengthening distribution networks, expanding optometry partnerships, and integrating digital diagnostics to optimize clinical outcomes. Investment in research and development enables iterative improvements in lens efficacy, comfort, and safety, reinforcing market reputation and customer loyalty. Companies differentiate through training programs for practitioners, advanced fitting technologies, and tailored solutions for myopia management, which collectively enhance adoption rates.

Key Industry Developments:

- In March 2026, CooperVision expanded the availability of its MyDay MiSight 1-day myopia-control soft contact lenses into the Asia-Pacific region with immediate shipments in Australia and New-Zealand as part of its global rollout aimed at making evidence-based pediatric vision solutions more accessible worldwide.

- In March 2025, Bausch & Lomb launched the Arise orthokeratology lens system in the U.S., introducing a cloud-based fitting platform that integrates with corneal topographers to generate precise overnight myopia-treating lens designs in seconds.

Companies Covered in Orthokeratology Lens Market

- CooperVision

- Bausch & Lomb Inc.

- MiracLens L.L.C.

- Alpha Corporation (Menicon Group)

- Johnson & Johnson Vision Care, Inc.

- TruForm Optics, Inc.

- Euclid Systems Corp.

- Brighten Optix, Co.

- Art Optical Contact Lens, Inc.

- GP Specialists

Frequently Asked Questions

The global orthokeratology lens market is projected to reach US$0.8 billion in 2026.

Rising prevalence of myopia, growing preference for non-surgical vision correction, and advancements in lens technology drive the orthokeratology lens market.

The orthokeratology lens market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Expansion into emerging markets, AI-based customization, pediatric-focused innovations, and growing public health myopia programs present key market opportunities.

CooperVision, Bausch & Lomb Inc., MiracLens L.L.C., Alpha Corporation (Menicon Group), and Johnson & Johnson Vision Care, Inc. are the leading players.