- Pharmaceuticals

- Orally Disintegrating Tablet Market

Orally Disintegrating Tablet Market Size, Share, and Growth Forecast 2026 - 2033

Orally Disintegrating Tablet Market by Drug Class (Anti-Psychotics, Anti-Epileptics, Anti-Hypertensives, Proton Pump Inhibitors, Others), by Disease Indication (Neurological Diseases, Gastrointestinal Diseases, Cardiovascular Diseases, Allergic Diseases, Others), Technology (Direct Compression, Freeze Drying (Lyophilization), Molded Tablets, Cotton Candy Process, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, Online Pharmacies, Specialty Pharmacies, Others), and Regional Analysis, 2026 - 2033

Orally Disintegrating Tablet Market Size and Trend Analysis

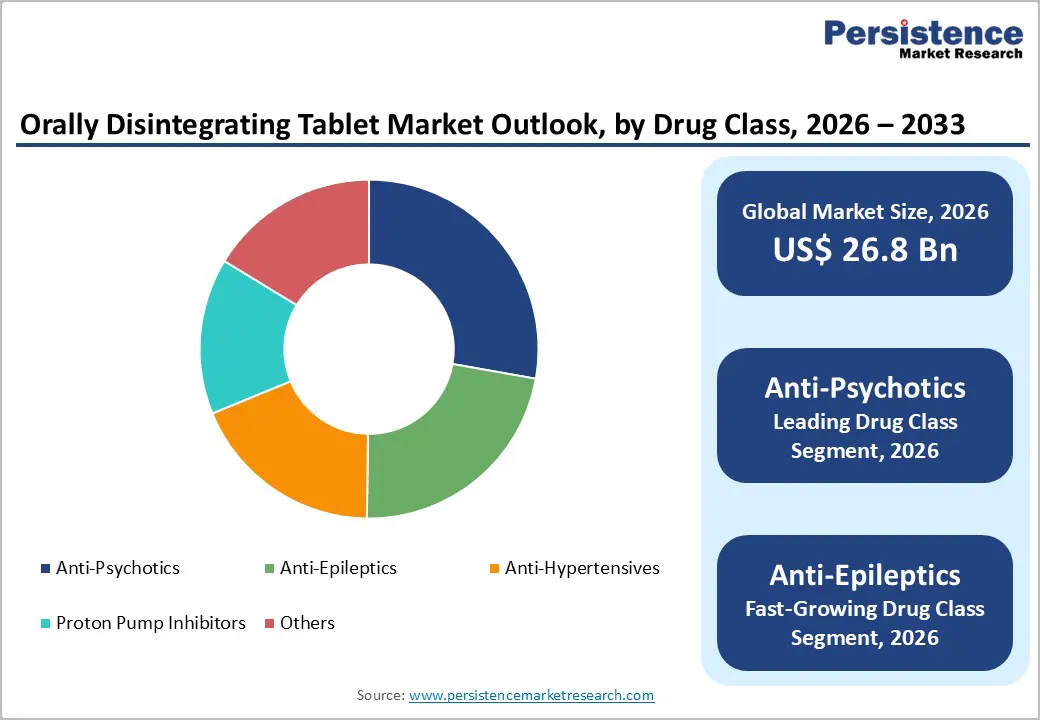

The global orally disintegrating tablet (ODT) market size is expected to be valued at US$ 26.8 billion in 2026 and projected to reach US$ 41.3 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

The market is driven by surging demand for patient-centric dosage forms, particularly among pediatric, geriatric, and dysphagia-affected populations who face significant difficulties swallowing conventional solid oral dosage forms. According to the World Health Organization (WHO), approximately 35% of adults globally experience dysphagia, creating a persistent clinical need for ODT formulations.

Regulatory encouragement from the U.S. FDA under its Pediatric Research Equity Act (PREA) and the European Medicines Agency (EMA)'s guidelines on age-appropriate pharmaceutical forms are incentivizing pharmaceutical companies to reformulate blockbuster drugs as ODTs, fueling sustained market momentum through the forecast period.

Key Market Highlights

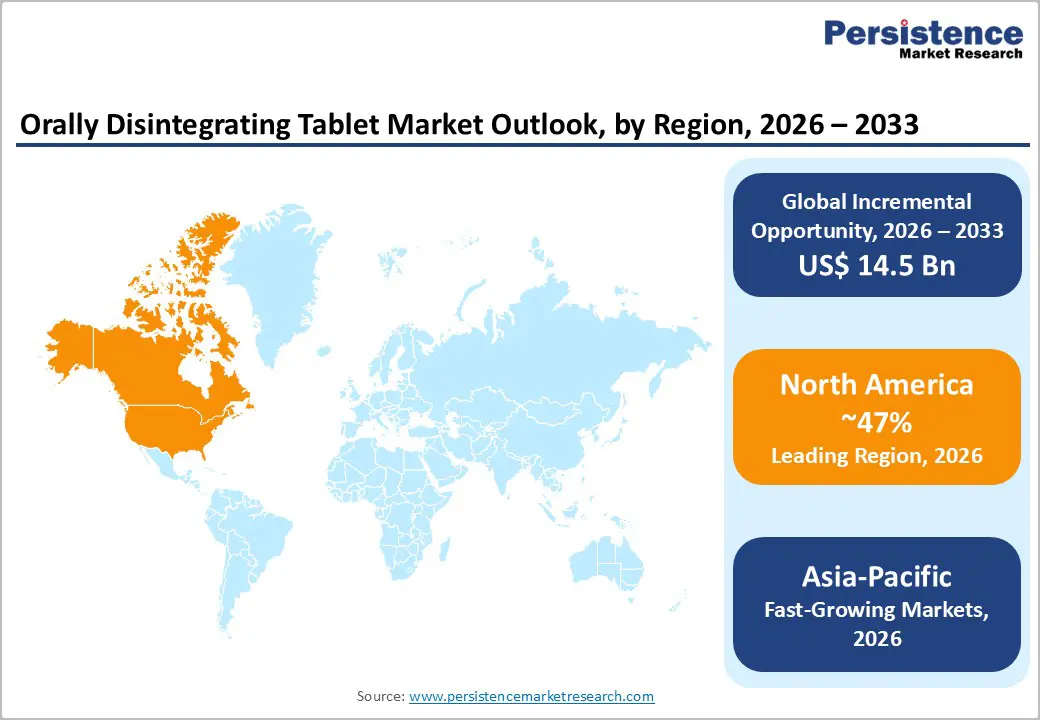

- Leading Region - North America: North America commands approximately 47% of the global ODT market share in 2025, supported by the U.S. FDA's robust ODT approval framework, a leading CDMO ecosystem, and high adoption of patient-centric formulations across CNS and GI indications.

- Fastest-Growing Region - Asia-Pacific: Asia-Pacific is the fastest-growing ODT market through 2033, driven by Japan's large elderly population, China's NMPA modernization, and India's cost-competitive ODT manufacturing capabilities serving global generic demand.

- Dominant Segment - Anti-Psychotics (Drug Class): Anti-Psychotics lead the ODT drug class segment with ~28% market share in 2025, anchored by olanzapine and risperidone ODT products and the clinical need for adherence-improving formulations in schizophrenia and bipolar disorder.

- Fastest-Growing Segment - Anti-Epileptics: Anti-Epileptics are the fastest-growing drug class segment, driven by rising epilepsy prevalence affecting over 50 million people globally, growing demand for rapid-dissolution formulations for acute seizure management, and an expanding ODT pipeline.

- Key Market Opportunity - Patent Expiry Reformulation & Online Pharmacies: ODT reformulation of off-patent blockbuster drugs via the FDA 505(b)(2) pathway, combined with the 50%+ growth in online pharmacy dispensing, represents a high-value commercial opportunity for ODT market participants.

Market Dynamics

Drivers - Growing Geriatric and Pediatric Population Driving Demand for Patient-Friendly Formulations

The global geriatric population, individuals aged 65 and above, is expected to reach 1.6 billion by 2050, according to the United Nations (UN). Elderly patients commonly suffer from polypharmacy challenges and swallowing difficulties, making ODTs an essential therapeutic alternative. Similarly, the WHO estimates that children account for over 26% of the global population, and the lack of age-appropriate oral medications is a recognized public health challenge.

The EMA's Paediatric Regulation and the FDA's Best Pharmaceuticals for Children Act (BPCA) mandate pediatric-specific formulation studies, directly stimulating ODT development. These demographic and regulatory forces collectively strengthen the market's long-term growth foundation.

Expanding Neurological and Psychiatric Drug Pipeline in ODT Format

The prevalence of neurological and psychiatric conditions, including schizophrenia, bipolar disorder, and Alzheimer's disease, is rising globally. The World Health Organization estimates that over 1 billion people worldwide live with a mental health disorder. Antipsychotics and anti-epileptics in ODT formats offer critical compliance benefits for patients who may resist or be unable to take conventional tablets. Olanzapine ODT (Zyprexa® Zydis), developed by Eli Lilly and Company, and risperidone ODT products from Janssen Pharmaceuticals exemplify commercially successful neurological ODTs.

With over 150 new CNS drugs in active clinical development globally as of 2024, the ODT format is increasingly preferred for CNS agents to address adherence challenges.

Market Restraints

Formulation Complexity and High Manufacturing Costs

ODT manufacturing demands stringent control of disintegration time (typically under 30 seconds per USP <701> standards), mechanical strength, and moisture sensitivity. Technologies such as freeze-drying (lyophilization) require high capital investment; lyophilizer equipment can cost upward of US$ 500,000 to several million dollars per unit. The specialized excipients, controlled humidity manufacturing environments, and proprietary technology licensing fees (e.g., Zydis® technology by Catalent) significantly elevate per-unit production costs compared to conventional tablets, limiting ODT adoption among generic manufacturers and smaller pharmaceutical companies in cost-sensitive markets.

Stability and Packaging Challenges Limiting Product Shelf Life

ODTs, particularly lyophilized variants, are highly susceptible to moisture, humidity, and physical fragility, requiring specialized blister packaging and cold-chain logistics in certain cases. According to the International Council for Harmonisation (ICH) Q1A guidelines, stability testing requirements for ODTs are more stringent than for standard tablets, increasing time-to-market timelines. WHO data also indicates that improper packaging contributes to 30-40% of drug degradation in tropical climates, particularly impactful for Asia and Africa, constraining market penetration in these high-growth regions.

Opportunities - Biologic and Novel Drug Reformulation into ODT Platforms

A significant opportunity lies in the reformulation of existing blockbuster drugs reaching patent expiration as ODT versions, extending product life cycles and enabling premium pricing. Teva Pharmaceutical Industries and Dr. Reddy's Laboratories have both pursued ODT versions of off-patent CNS and gastrointestinal drugs. Additionally, advances in ODT technology platforms, including fast-dissolving films and nanotechnology-based ODTs, are opening avenues for novel API incorporation.

The FDA's 505(b)(2) regulatory pathway allows reformulated ODTs to leverage existing safety data, reducing development timelines by up to 30-40%. With over USD 250 billion worth of branded drug patents expected to expire by 2030, ODT reformulation represents a high-value commercial strategy for pharmaceutical companies.

Rapid Growth of Online Pharmacies Expanding ODT Accessibility

Online pharmacies are emerging as the fastest-growing distribution channel in the pharmaceutical sector. The U.S. Centers for Medicare & Medicaid Services (CMS) reported a 50%+ increase in online pharmacy dispensing post-COVID-19, driven by telehealth integration and home delivery preferences. ODTs, with their ease-of-use and caregiver-friendly administration, are well-suited for home healthcare and remote patient management particularly for neurological and psychiatric conditions requiring long-term adherence.

Companies such as Amazon Pharmacy and CVS Caremark are actively expanding digital dispensing capabilities, creating new distribution pathways for ODT manufacturers. Market participants that integrate with e-pharmacy platforms and direct-to-consumer models can capture this accelerating shift in pharmaceutical retail.

Category-wise Analysis

Drug Class Insights

Anti-Psychotics hold the leading position in the ODT market by drug class, commanding approximately 28% of the total market share in 2025. This dominance is underpinned by the clinical imperative for medication adherence in schizophrenia and bipolar disorder conditions, where patient non-compliance can lead to hospitalization and clinical relapse. Landmark ODT products such as olanzapine (Zyprexa® Zydis) by Eli Lilly and risperidone ODT by Janssen set early commercial precedents.

According to the National Institute of Mental Health (NIMH), over 3.5 million people in the U.S. are treated for schizophrenia annually, many of whom benefit from supervised ODT administration. The broad generic availability of antipsychotic ODTs further supports high prescription volumes across both developed and emerging markets.

Disease Indication Insights

Neurological diseases are likely to represent the leading disease indication segment in the ODT market, accounting for approximately 34% share in 2026. The high prevalence of conditions such as Parkinson's disease, epilepsy, migraines, and schizophrenia, where swallowing difficulties or acute episodic symptoms necessitate rapid drug dissolution, drives ODT adoption. The World Health Organization estimates that epilepsy alone affects over 50 million people globally, with a treatment gap exceeding 75% in low-income countries.

ODT anti-epileptics improve compliance by eliminating the need for water, making them especially suited for acute seizure management and institutional care. The strong neurological drug pipeline in ODT format reinforces this segment's market leadership.

Technology Insights

Direct compression is the leading technology segment in the ODT market, likely to represent approximately 40% of the technology segment in 2026. As the most cost-effective and scalable ODT manufacturing process, direct compression requires minimal processing steps, standard manufacturing equipment, and avoids the high capital outlays associated with lyophilization. The technology is favored by generic pharmaceutical manufacturers in cost-sensitive markets including India and China.

Advances in superdisintegrant excipients including crospovidone, croscarmellose sodium, and sodium starch glycolate have significantly improved the disintegration time achievable via direct compression, narrowing the performance gap with lyophilized ODTs. Companies such as JRS Pharma and DFE Pharma supply key excipient systems supporting this technology segment.

Distribution Channel Insights

Retail pharmacies and drug stores represent the dominant distribution channel for ODTs, accounting for 45% of the distribution channel segment in 2026. The broad accessibility of retail pharmacy networks with over 88,000 retail pharmacies operating in the U.S. alone, according to the National Community Pharmacists Association (NCPA) ensures wide patient access to ODT formulations across multiple therapeutic categories. ODTs dispensed for chronic neurological, psychiatric, and gastrointestinal conditions are predominantly managed through long-term retail pharmacy relationships.

Major retail pharmacy chains, including Walgreens, CVS Pharmacy, and Boots (U.K.), prominently stock ODT-format medications given their patient convenience value. The growth of pharmacy-based medication management programs further reinforces this channel's preeminence.

Regional Insights

North America Orally Disintegrating Tablet Market Trends and Insights

North America accounted for approximately 47% of the global orally disintegrating tablet (ODT) market in 2026, supported by extensive adoption of patient-friendly dosage forms, strong reimbursement systems, and widespread use in CNS and gastrointestinal therapies. The region benefits from a mature pharmaceutical innovation ecosystem and regulatory pathways that facilitate lifecycle management through reformulated products. The United States represents nearly 84.5% of the North American market. Rising dysphagia prevalence among elderly populations and growing pediatric applications continue to expand demand for ODT formulations across both branded and generic medicines.

U.S. Orally Disintegrating Tablet Market Trends and Insights

The U.S. dominates the regional market with an estimated value of USD 9.9 billion in 2025 and is projected to expand at a CAGR of 7.6% in the forecast period. Growth is driven by strong adoption of orally disintegrating versions of psychiatric, antiemetic, and proton pump inhibitor drugs, supported by advanced formulation technologies and streamlined regulatory pathways. Pharmaceutical manufacturers are actively developing differentiated formulations to improve patient adherence, while growing investments in advanced oral drug delivery technologies and a well-established generic medicine sector continue to strengthen the country's leadership position.

Canada Orally Disintegrating Tablet Market Trends and Insights

Canada is poised to account for roughly USD 1.4 billion in 2026 and is expected to achieve a CAGR of 7.1% over the forecast period. Demand is supported by an aging population, rising prevalence of swallowing disorders, and increasing use of convenient dosage forms in hospital and outpatient settings. Rising adoption of patient-friendly medicines across hospitals and outpatient settings, coupled with expanding availability of generic ODT products, is driving demand. Continued investments in healthcare infrastructure, strong public reimbursement systems, and increasing awareness regarding medication adherence further support the country's market development.

Europe Orally Disintegrating Tablet Market Trends and Insights

Europe is likely to represent about 28.4% of the global orally disintegrating tablet market in 2026, with strong uptake across neurology, allergy, and pediatric applications. The region benefits from harmonized pharmaceutical regulations, broad generic penetration, and increasing demand for dosage forms that improve adherence in geriatric and pediatric populations. Germany accounts for nearly 24.6% of the European market, while the United Kingdom contributes around 18.3%. Continued expansion of pediatric-focused formulations and high acceptance of generic ODTs support steady market growth.

Germany Orally Disintegrating Tablet Market Trends and Insights

Germany generated an estimated USD 1.75 billion in 2026 and is projected to register a CAGR of 6.8% in the forecast period. Strong statutory insurance coverage and a large generic pharmaceutical market encourage widespread use of cost-effective ODT formulations for neurological and gastrointestinal disorders. High demand for neurological and gastrointestinal therapies, combined with broad insurance coverage and efficient pharmacy distribution networks, continues to drive adoption. The country's emphasis on pharmaceutical innovation, quality manufacturing standards, and patient-centric drug formulations further strengthens its position as Europe's leading ODT market.

UK Orally Disintegrating Tablet Market Trends and Insights

The UK market is valued at approximately USD 1.3 billion in 2025 and is expected to reach at a CAGR of 6.9%. Growing focus on medication adherence, expanding specialty pharmaceutical development, and continued investment in innovative drug delivery technologies are supporting market growth. Strong healthcare infrastructure and increasing use of differentiated formulations for chronic disease management further enhance demand.

Asia Pacific Orally Disintegrating Tablet Market Trends and Insights

Asia Pacific is likely to account for 20.3% share of the global market in 2026 and is projected to witness the fastest CAGR of 8.9% by 2033. Growth is fueled by expanding pharmaceutical manufacturing, improving healthcare access, and increasing incidences of chronic diseases. China represents approximately 33.8% of the regional market, while Japan contributes around 27.4%. Rising demand for pediatric and geriatric-friendly formulations and strong generic production capabilities continue to accelerate adoption across the region.

China Orally Disintegrating Tablet Market Trends and Insights

China is estimated at 34.2% of the Asia Pacific in 2026. Government support for advanced formulations and increasing domestic production of differentiated generics is strengthening the country’s role in regional market expansion. Rapidly expanding pharmaceutical manufacturing sector and growing domestic healthcare demand. Increasing prevalence of chronic diseases, rising investment in advanced formulation technologies, and government support for pharmaceutical innovation continue to drive market expansion.

Japan Orally Disintegrating Tablet Market Trends and Insights

Japan is likely to reach approximately USD 1.4 billion in 2026 and is expected to expand at a CAGR of 7.8%. It has one of the highest adoption rates of ODTs globally due to its aging population and long-standing physician preference for easy-to-administer dosage forms. High demand for patient-friendly medicines in neurological and gastrointestinal therapies, combined with continuous pharmaceutical innovation and advanced formulation technologies, sustains market growth. Strong physician preference for convenient dosage forms and an established healthcare system further reinforce Japan's significant position in the regional market.

Competitive Landscape

The global ODT market exhibits a moderately fragmented competitive structure, with large multinationals including Teva Pharmaceutical, Pfizer, Catalent, and GlaxoSmithKline competing alongside a large number of regional generic manufacturers. Key differentiators include proprietary ODT platform technologies (e.g., Catalent's Zydis® and Takeda's WOWTAB®), CDMO capabilities, and strength in regulated market filings. Strategic trends include licensing deals for ODT technology access, acquisition of specialty formulation CDMOs, and investment in continuous manufacturing.

Emerging players are leveraging 3D printing and nanotechnology-based ODT platforms to differentiate in niche therapeutic areas, intensifying innovation-driven competition.

Key Developments:

- In July 2024, Mind Medicine (MindMed) Inc., a clinical stage biopharmaceutical company developing novel product candidates to treat mental health disorders, announced the issuance of a new patent by the United States Patent and Trademark Office (USPTO) covering MM120 (lysergide). MM120 is an Orally Disintegrating Tablet (ODT).

- In March 2024, Dr. Reddy’s Laboratories Ltd. announced that it had received approval from the Central Drugs Standard Control Organization (CDSCO) for the manufacturing and marketing of Omeprazole delayed-release orally disintegrating tablets in the Indian market.

Companies Covered in Orally Disintegrating Tablet Market

- Teva Pharmaceutical Industries Ltd.

- Pfizer Inc.

- Catalent, Inc.

- Dr. Reddy’s Laboratories Ltd.

- Eli Lilly and Company

- Sun Pharmaceutical Industries Ltd.

- Zydus Lifesciences Ltd.

- Aurobindo Pharma Ltd.

- Takeda Pharmaceutical Company Limited

- Merck & Co., Inc.

- GlaxoSmithKline plc.

- Eisai Co., Ltd.

- Viatris Inc.

- Torrent Pharmaceuticals Ltd.

- Bausch Health Companies Inc.

- Others

Frequently Asked Questions

The global Orally Disintegrating Tablet Market is estimated to be valued at US$ 26.8 billion in 2026, growing from US$ 19.8 billion in 2020. It is projected to reach US$ 41.3 billion by 2033, expanding at a forecast CAGR of 6.4%.

The primary drivers include the growing geriatric and pediatric population globally with the UN projecting 1.6 billion people aged 65+ by 2050 combined with regulatory mandates for age-appropriate formulations under the FDA's BPCA and EMA's Paediatric Regulation, and the rise of neurological and psychiatric drug reformulations in ODT format.

North America leads with approximately 47% of global ODT market share in 2025, driven by the U.S. FDA's established ODT regulatory guidance, advanced CDMO infrastructure through companies like Catalent, Inc., and high per-capita pharmaceutical spending supporting premium patient-centric formulations.

Key opportunities include the reformulation of off-patent blockbuster drugs into ODTs via the FDA 505(b)(2) pathway with over US$ 250 billion in patent expirations expected by 2030 and the rapid expansion of online pharmacy channels that have grown over 50% post-COVID-19, enhancing ODT distribution and patient access.

Key players include Catalent, Inc. (proprietor of the Zydis® technology), Teva Pharmaceutical Industries Ltd., Pfizer Inc., Eli Lilly and Company, Sun Pharmaceutical Industries Ltd., Zydus Lifesciences Ltd., and Takeda Pharmaceutical Company Limited, each competing through proprietary ODT platforms, CDM capabilities, and broad regulated market generic portfolios.