- Medical Devices

- Operating Tables Market

Operating Tables Market Size, Share, and Growth Forecast 2026 - 2033

Operating Tables Market by Product (General Surgery Tables, Specialty Surgery Tables, Hydraulic Operating Tables, Others), Application (Orthopedic Surgery, Neurosurgery, Cardiovascular Surgery, Gynecology Surgery, Others), End-user (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Regional Analysis, 2026 - 2033

Operating Tables Market Share and Trends Analysis

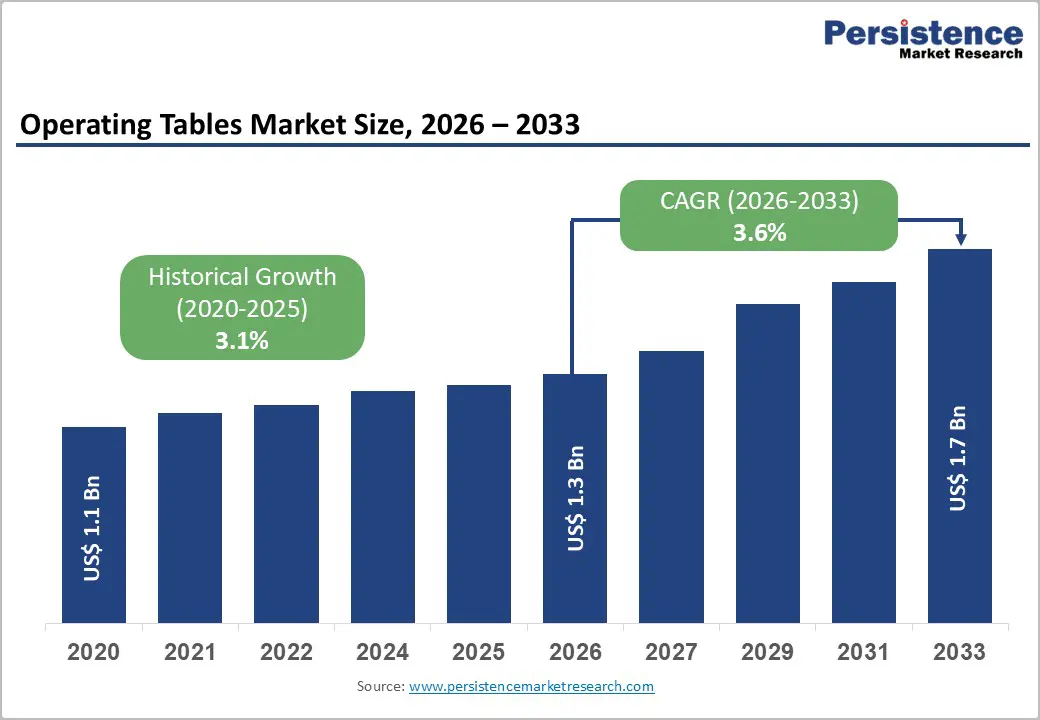

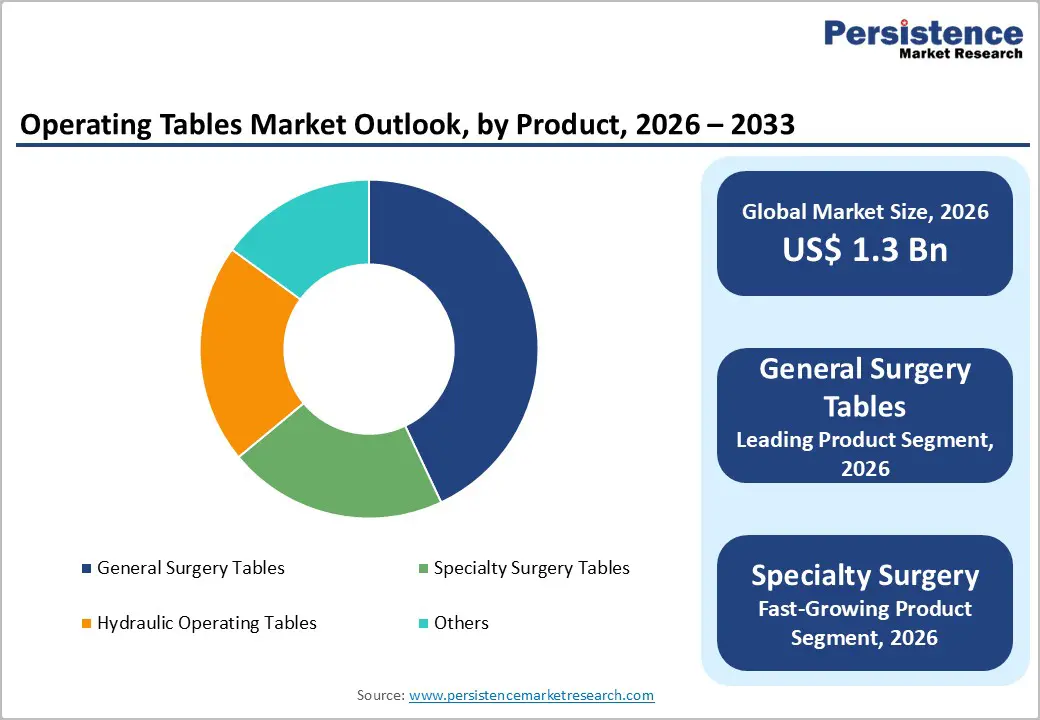

The global Operating Tables market size is expected to be valued at US$ 1.3 billion in 2026 and projected to reach US$ 1.7 billion by 2033, growing at a CAGR of 3.6% between 2026 and 2033. It is advancing on a steady trajectory, underpinned by rising global surgical procedure volumes, accelerating hospital infrastructure investment in emerging economies, and growing clinical demand for technologically advanced specialty surgery tables that optimize surgical access and patient safety outcomes.

The World Health Organization (WHO) estimates that approximately 313 million major surgical procedures are performed globally each year, with this figure expanding alongside aging populations and increasing chronic disease treatment rates. The parallel growth of ambulatory surgical centers (ASCs) and specialty clinics driven by cost containment pressures in developed healthcare systems is further expanding the institutional customer base for next-generation operating table solutions, including motorized and imaging-compatible table platforms tailored to minimally invasive and robotic-assisted surgical workflows.

Key Industry Highlights

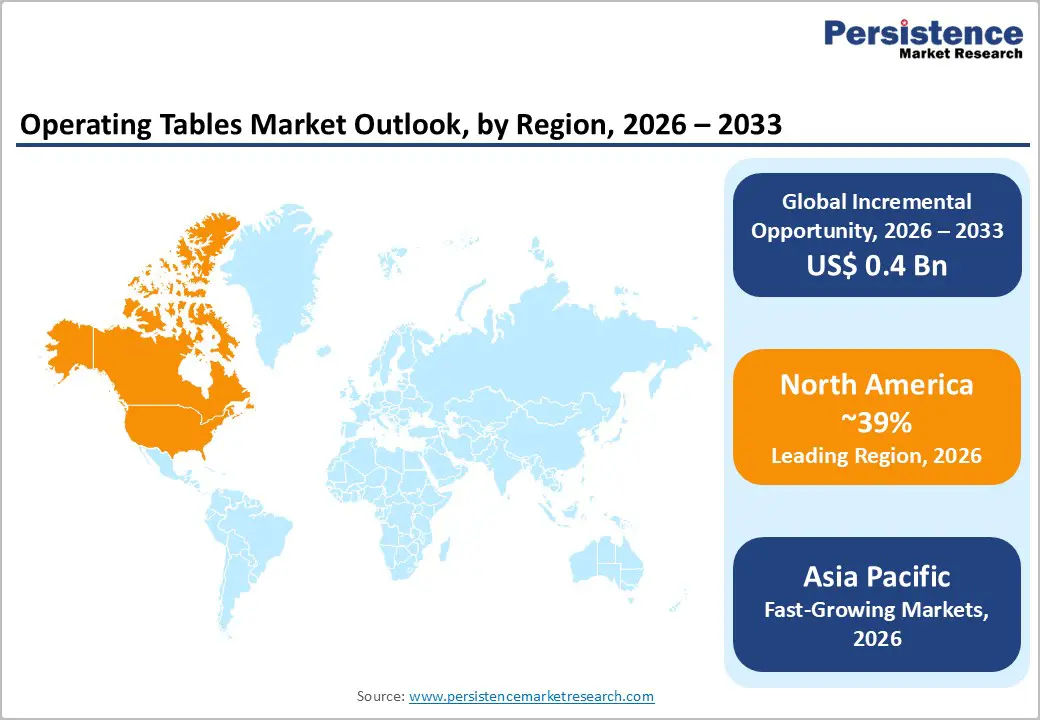

- Regional Leadership: North America leads the global Operating Tables market with approximately 39% market share in 2025, anchored by the United States performing over 50 million surgical procedures annually, an active hospital surgical suite modernization cycle driven by robotic surgery adoption, and the world's largest ASC network with over 9,900 certified centers.

- Fast-growing Market: Asia Pacific is the fast-growing regional market, propelled by China's Healthy China 2030 hospital modernization initiative, India's PM-JAY-driven surgical capacity expansion, and rising medical tourism investment in specialty surgical infrastructure across Singapore, Thailand, and Malaysia, driving premium operating table procurement.

- Dominant Product: General surgery tables dominate the product category with approximately 43% market share in 2025, reflecting their universal deployment across all hospital surgical specialties, broad procedural versatility, and consistent replacement demand driven by a standard 7–10 year operating table service lifecycle across global hospital procurement programs.

- Fast-growing Product: Specialty surgery tables are the fast-growing product segment, driven by accelerating robotic-assisted surgical procedure adoption with Intuitive Surgical reporting over 2 million da Vinci procedures in 2023, creating specific demand for imaging-compatible, robot-docking-optimized specialty table platforms from manufacturers including Getinge AB and Stryker Corporation.

Market Dynamics

Does The Rise in Global Surgical Procedure Volume Drive Demand for the Replacement of Equipment?

The sustained expansion of global surgical volumes is the primary demand driver for operating tables. The Lancet Commission on Global Surgery estimates that 313 million surgical procedures are performed annually worldwide, yet an additional 143 million procedures are needed in low- and middle-income countries to adequately address the burden of surgical disease.

In high-income markets, procedure volume growth in orthopedics, cardiovascular surgery, neurosurgery, and bariatric surgery is driving the replacement cycle for aging operating table inventories with modern motorized and modular platforms.

The American Hospital Association (AHA) reports that the United States performs over 50 million inpatient and outpatient surgical procedures annually, creating consistent capital equipment demand. Operating tables have an average service life of 7 to 10 years, creating a steady replacement-driven procurement cycle that sustains baseline market demand regardless of new facility construction activity.

Does Hospital Infrastructure Expansion and Modernization in Emerging Economies Fuel Growth?

Significant government-led hospital infrastructure investment across Asia Pacific, the Middle East, and Latin America is generating substantial new installation demand for operating tables as foundational surgical capital equipment. The World Bank and regional development banks have channeled billions in financing toward healthcare facility construction in low- and middle-income countries over the past decade. In India, the government's Ayushman Bharat–Pradhan Mantri Jan Arogya Yojana (PM-JAY) scheme is driving expansion of hospital surgical capacity across tier-2 and tier-3 cities.

In the Middle East, Saudi Vision 2030 and the UAE National Agenda include significant commitments to expanding and modernizing hospital surgical infrastructure, including replacement of legacy operating theater equipment. China's Healthy China 2030 initiative is similarly directing substantial public investment into hospital modernization, including surgical suite equipment upgrades, providing a multi-year demand runway for operating table manufacturers.

Why High Capital Cost and Extended Replacement Cycles Limit Volume Growth?

Advanced motorized and specialty operating tables carry significant capital costs premium systems from manufacturers such as Getinge AB and Stryker Corporation can range from US$ 20,000 to US$ 150,000 per unit creating substantial budget constraints for hospital capital procurement departments, particularly in cost-sensitive public healthcare systems. Extended service lifecycles of 7 to 10 years and rigorous preventive maintenance programs further reduce annual replacement volumes, constraining the market's organic growth rate and making it sensitive to public healthcare budget cycles and capital expenditure freezes during economic downturns.

Does Stringent Regulatory Approval Requirements and Product Certification Complexity Create Challenges?

Operating tables are classified as Class II or Class III medical devices in major regulatory jurisdictions, requiring FDA 510(k) clearance in the United States and CE marking under the EU Medical Device Regulation (EU MDR 2017/745) in Europe. Comprehensive biocompatibility, mechanical performance, electrical safety, and electromagnetic compatibility testing add significant time and cost to new product development cycles. For manufacturers seeking to commercialize imaging-compatible, robotic-integration-capable, or carbon fiber radiolucent tabletop innovations, regulatory pathways can extend development timelines substantially, creating barriers to rapid product iteration and market entry for new entrants.

How do Growing Adoption of Specialty Surgery Tables for Minimally Invasive and Robotic Surgery Create New Opportunities?

Specialty surgery tables are the fast-growing product segment and represent a high-value strategic opportunity for operating table manufacturers. The rapid global adoption of minimally invasive surgery (MIS) and robotic-assisted surgical systems including the da Vinci Surgical System by Intuitive Surgical is creating specific demand for operating tables engineered with precise Trendelenburg positioning, integrated imaging access, carbon fiber radiolucent tabletops, and compatibility with robotic arm docking systems.

The American College of Surgeons (ACS) reports consistent growth in laparoscopic and robotic-assisted procedure volumes across surgical specialties. Getinge AB, Stryker Corporation, and STERIS plc have each introduced specialty table platforms specifically designed for robotic-assisted surgery suites, reflecting strong commercial recognition of this opportunity. As robotic surgery adoption accelerates globally with Intuitive Surgical reporting over 2 million da Vinci procedures performed in 2023 specialty table demand is set for sustained above-market growth.

Expansion of Ambulatory Surgical Centers Creating New Institutional Customer Base

The rapid global proliferation of ambulatory surgical centers (ASCs) is creating an expanding institutional market for cost-optimized, versatile operating tables designed for high-throughput outpatient surgical environments. In the United States, the Ambulatory Surgery Center Association (ASCA) reports over 9,900 Medicare-certified ASCs, performing approximately 60% of all U.S. outpatient surgical procedures. ASC operating table procurement requirements differ from hospital settings emphasizing compact footprints, multi-specialty configurability, ease of positioning adjustment, and lower acquisition costs creating a distinct product opportunity for manufacturers developing ASC-specific table platforms

Internationally, Western European healthcare systems and select Asia Pacific are similarly expanding ASC-equivalent outpatient surgical facility networks as a cost-containment strategy, broadening the global institutional customer base for operating table manufacturers beyond traditional hospital procurement channels.

Category-wise Analysis

Product Insights

General surgery tables lead the operating tables market, commanding approximately 43% of global market share in 2026. General surgery tables designed for broad procedural versatility across abdominal, thoracic, vascular, and general surgical applications are the foundational capital equipment in virtually every hospital operating theater worldwide, securing their dominant procurement share. Their versatility, proven reliability across diverse surgical specialties, and broad compatibility with standard anesthetic and surgical accessories make them the default specification in hospital surgical suite procurement programs.

The American Hospital Association (AHA) data consistently reflects abdominal and general surgical procedures among the highest-volume categories in U.S. hospitals, generating persistent installation and replacement demand for general surgery tables. Market leaders including Getinge AB, Stryker Corporation, STERIS plc, and Mizuho Corporation maintain strong positions in the general surgery table segment through established institutional supply relationships and comprehensive service and maintenance networks.

Application Insights

Orthopedic surgery is the leading application segment for operating tables, accounting for approximately 29% of global market share in 2026. Orthopedic procedures including total hip and knee arthroplasty, spinal surgery, and fracture fixation are among the highest-volume surgical specialties globally and require specialized table configurations including traction attachments, lateral positioning systems, fracture table extensions, and radiolucent tabletops for intraoperative fluoroscopic imaging. The American Academy of Orthopaedic Surgeons (AAOS) reports that over one million total knee replacement and 500,000 total hip replacement procedures are performed annually in the United States alone.

The aging global population is driving consistent growth in orthopedic procedure volumes, creating sustained and expanding demand for orthopedic-configured operating table systems. Manufacturers including Mizuho Corporation and Schaerer Medical AG have developed specialized orthopedic surgery table platforms specifically optimized for joint replacement and spinal surgical workflows.

End-user Insights

Hospitals represent the dominant end-user segment for operating tables, capturing approximately 62% of global market demand in 2025. Hospitals are the primary institutional procurement centers for the full range of operating table categories from general surgery and orthopedic tables to specialty neurosurgery and cardiovascular platforms owing to their role as the central venue for complex inpatient surgical care, emergency surgery, and high-acuity specialty procedures.

The World Health Organization (WHO) estimates approximately 136,000 hospitals globally, each maintaining multiple operating theatres with an average of 2 to 5 tables per theatre depending on facility size and surgical volume. Large academic medical centers and quaternary care hospitals are key procurement drivers for premium specialty table systems, while community hospitals represent the high-volume replacement procurement channel for general surgery platforms.

Regional Insights

North America Operating Tables Market Trends and Insights

North America leads the global operating tables market with approximately 39% market share in 2025, driven by the United States' dominant position as the world's largest surgical procedure volume market, high per-capita healthcare capital expenditure, strong adoption of robotic and minimally invasive surgical techniques, and a well-developed ASC ecosystem. The region benefits from active table replacement cycles in aging hospital surgical suites and strong demand for specialty table platforms compatible with robotic surgical systems.

U.S. Operating Tables Market Size

The United States accounts for approximately 89% of North America's operating table market, performing over 50 million surgical procedures annually per the AHA. Strong hospital capital budgets, an active surgical suite renovation cycle driven by robotic surgery suite buildouts, and the largest ASC network globally with over 9,900 centers per the ASCA collectively sustain robust demand for both general and specialty operating table platforms across institutional procurement channels.

Europe Operating Tables Market Trends and Insights

Europe is the second-largest regional market for operating tables, anchored by Germany, France, the U.K., and the Nordic countries, where well-funded universal healthcare systems maintain disciplined surgical infrastructure replacement programs. The EU MDR 2017/745 regulatory framework ensures high product quality standards across the region. Growing adoption of minimally invasive and robotic surgical techniques is accelerating specialty table procurement across European hospital surgical suites, with neurosurgery and orthopedic applications generating strong near-term demand.

Germany Operating Tables Market Size

Germany accounts for approximately 24% of Europe's operating tables market, reflecting its position as Europe's largest healthcare economy and most active hospital surgical market. Germany performs approximately 17 million inpatient hospital cases annually per Statistisches Bundesamt data, sustaining consistent demand for operating table capital equipment. Manufacturers including Schmitz u. Söhne GmbH & Co. KG and UFSK-International OSYS GmbH maintain strong domestic market presence in the German hospital procurement segment.

U.K. Operating Tables Market Size

The United Kingdom represents approximately 15% of Europe's operating table market, with the National Health Service (NHS) serving as the dominant institutional buyer through centralized procurement via NHS Supply Chain. The NHS Long Term Plan commitments to expand elective surgical capacity including investment in dedicated surgical hubs are generating incremental operating table procurement demand, with specialty orthopedic and cardiovascular table platforms among the higher-priority investment categories.

France Operating Tables Market Size

France accounts for approximately 13% of European operating table demand, supported by a comprehensive public hospital network administered by the Ministère de la Santé with over 3,000 public and private hospital facilities performing surgical procedures. France's Ségur de la Santé healthcare investment plan, which committed €19 billion to modernizing hospital infrastructure post-COVID-19, has accelerated surgical equipment procurement including operating table upgrades across the French public hospital system.

Asia Pacific Operating Tables Market Trends and Insights

Asia Pacific is the fastest-growing regional market for operating tables, propelled by massive hospital infrastructure expansion, rapidly rising surgical procedure volumes, and government healthcare modernization initiatives across China, India, Japan, and ASEAN nations. China is the region's single largest market, with the National Health Commission of China overseeing a network of over 36,000 hospitals and directing significant capital investment in surgical suite modernization under Healthy China 2030. Rising medical tourism in Thailand, Malaysia, and Singapore is also driving specialty surgical equipment investment.

India Operating Tables Market Size

India represents approximately 8% of Asia Pacific's operating tables market, with demand accelerating alongside healthcare infrastructure expansion under PM-JAY and private hospital group investment. India performs an estimated 30–50 million surgical procedures annually, with a large volume occurring in private tertiary hospitals that are actively investing in modern operating table platforms including motorized and specialty surgery configurations to compete for surgical tourism and premium patient segments.

Competitive Landscape

The Operating Tables Market is highly competitive, supported by rising surgical volumes, increasing hospital infrastructure investments, and demand for advanced operating room equipment. Manufacturers are focusing on developing technologically advanced tables with electro-hydraulic systems, imaging compatibility, and improved patient positioning features to support complex surgical procedures. Demand for specialty surgery tables is increasing due to growth in orthopedic, neurosurgical, and minimally invasive surgeries. Companies are also emphasizing ergonomic design, infection control, and integration with digital operating room systems.

Key Developments:

- In April 2026, NYC Health + Hospitals/Bellevue Hospital unveiled five new orthopedic surgical tables following a $500,000 internal investment to improve patient safety, surgical precision, and overall care quality.

- In February 2026, Schaeffler expanded its medical technology portfolio by launching the EWELLIX EMA-80M electromechanical linear actuator for patient tables and operating tables. The new actuator was designed for electric height adjustment in CT and MRI patient tables, offering a lifting capacity of up to 20,000 N and speeds of up to 25 mm/s.

Global Operating Tables Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.1 Billion |

|

Current Market Value (2026) |

US$ 1.3 Billion |

|

Projected Market Value (2033) |

US$ 1.7 Billion |

|

CAGR (2026–2033) |

3.6% |

|

Leading Region |

North America, 39% market share (2025) |

|

Dominant Product Category |

General Surgery Tables, ~43% market share (2025) |

|

Top-Ranking Application |

Orthopedic Surgery, ~29% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 0.4 Billion |

Companies Covered in Operating Tables Market

- Getinge AB

- Stryker Corporation

- STERIS plc

- Baxter International Inc.

- Skytron LLC

- Mizuho Corporation

- Merivaara Corp.

- Mindray Medical

- ALVO Medical

- Schaerer Medical AG

- UFSK-International OSYS GmbH

- Lojer Group

- Schmitz u. Söhne GmbH & Co. KG

Frequently Asked Questions

The global Operating Tables market size is estimated to be valued at US$ 1.3 billion in 2026.

The primary demand drivers are sustained global surgical volume growth with the Lancet Commission on Global Surgery identifying an additional 143 million procedures needed annually in low- and middle-income countries and significant hospital infrastructure modernization investment across Asia Pacific and the Middle East under programs including China's Healthy China 2030 and India's PM-JAY.

North America leads the global Operating Tables market with approximately 39% market share in 2025, anchored by the United States performing over 50 million surgical procedures annually per the AHA, a well-developed ASC network exceeding 9,900 certified centers per the ASCA, and active hospital surgical suite renovation programs driven by robotic surgery adoption. High per-capita healthcare capital expenditure and comprehensive reimbursement frameworks further sustain North America's market leadership position.

The fast and most strategic growth opportunity is the rising adoption of Specialty Surgery Tables engineered for robotic-assisted and minimally invasive surgical workflows.

Leading companies in the global Operating Tables market include Getinge AB, Stryker Corporation, STERIS plc, Mizuho Corporation, Schaerer Medical AG, Merivaara Corp., Mindray Medical, ALVO Medical, Lojer Group, Skytron LLC, UFSK-International OSYS GmbH, etc.