- Biotechnology

- Neurological Biomarkers Market

Neurological Biomarkers Market Size, Share, and Growth Forecast 2026 - 2033

Neurological Biomarkers Market by Biomarker Type (Proteomic Biomarkers, Genomic Biomarkers, Neuroimaging Biomarkers, Metabolomics Biomarkers), by Sample (Blood, Plasma, Cerebrospinal Fluid, Others), Indication (Alzheimer's Disease, Multiple Sclerosis, Parkinson's Disease, Autism Spectrum Disorder, Others), End-user (Hospital Labs, Diagnostic Centers, Academic & Research Institutes, Biopharma Companies, Others), and Regional Analysis, 2026 - 2033

Neurological Biomarkers Market Share and Trends Analysis

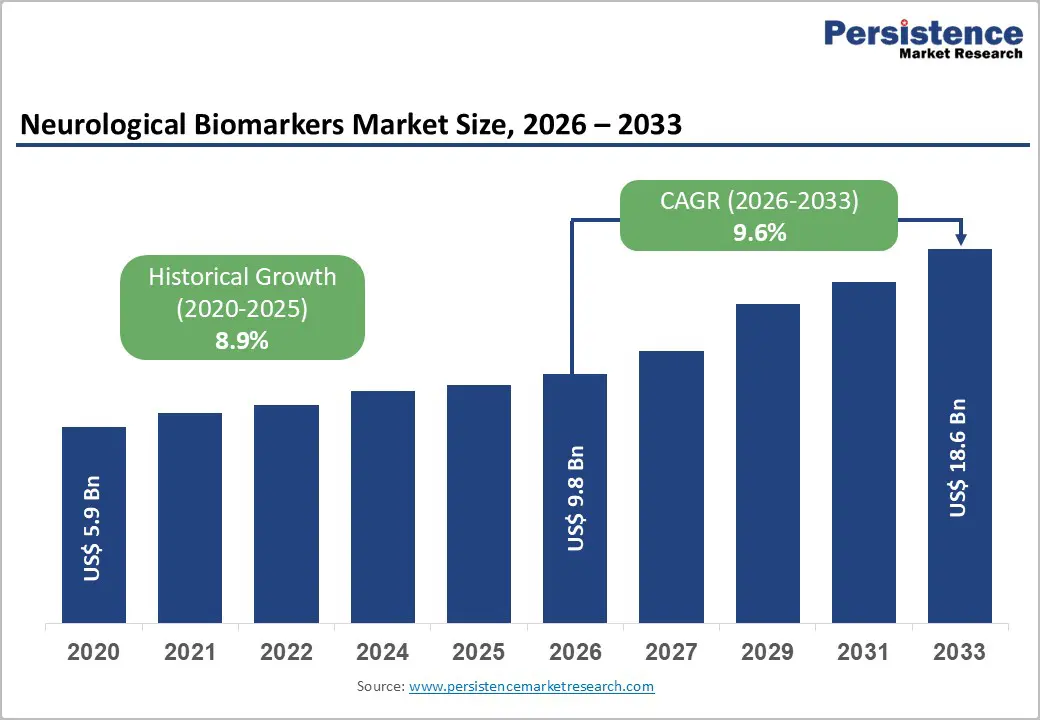

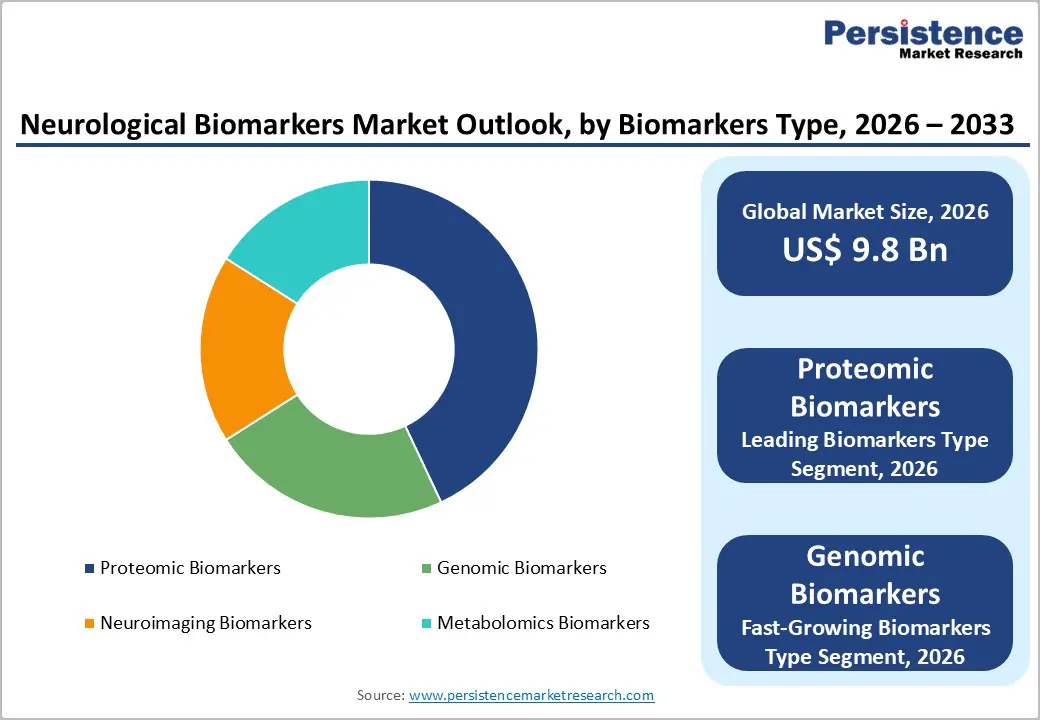

The global neurological biomarkers market size is expected to be valued at US$ 9.8 billion in 2026 and projected to reach US$ 18.6 billion by 2033, growing at a CAGR of 9.6% between 2026 and 2033. It is growing rapidly due to the increasing burden of neurodegenerative and neurological disorders such as Alzheimer’s disease, Parkinson’s disease, epilepsy, and multiple sclerosis.

Rising demand for early diagnosis, disease monitoring, and personalized treatment is driving adoption across healthcare systems. Advances in proteomics, genomics, neuroimaging, and metabolomics are improving biomarker accuracy and clinical utility. Blood-based and non-invasive biomarkers are gaining strong attention for faster and more accessible testing.

Key Industry Highlights:

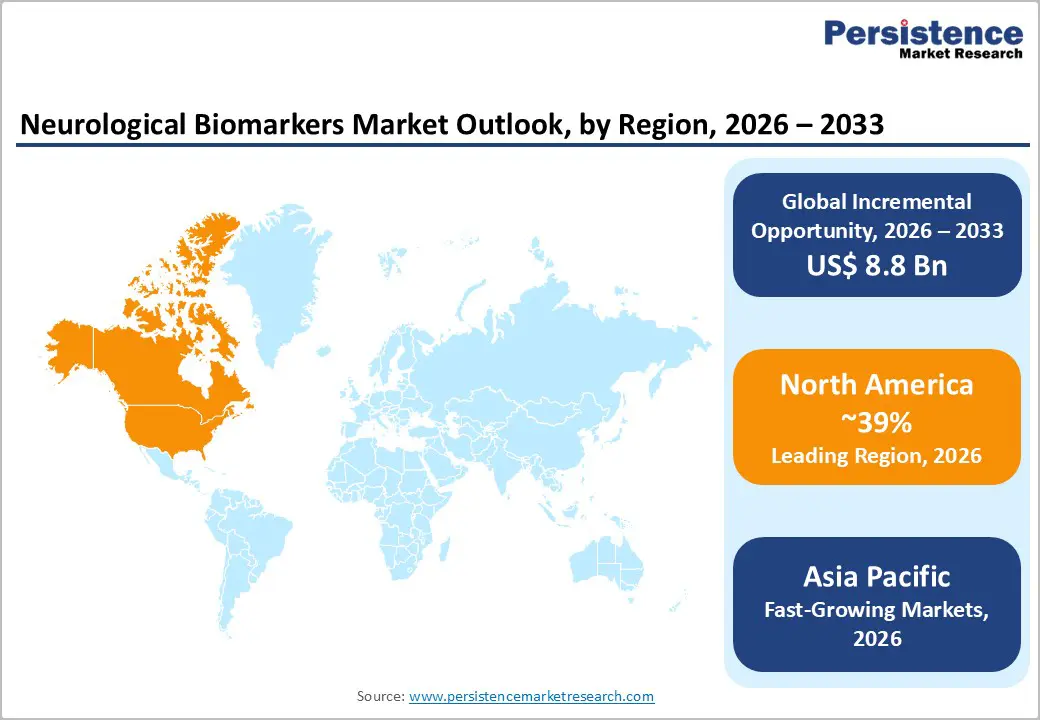

- Leading Region - North America holds approximately 39% of global market share in 2025, driven by FDA approvals of amyloid-targeting Alzheimer's therapies mandating biomarker patient selection, NIH research funding, and the world's most active CNS drug development ecosystem.

- Fast-Growing Market - Asia Pacific is the fast-growing market propelled by China's NSFC neuroscience investments, Japan's AMED-funded Alzheimer's programs, expanding biopharma CNS trial activity, and India's rapidly growing ARDSI-documented Alzheimer's disease burden.

- Dominant Biomarker Type Segment - Proteomic biomarkers are likely to lead with approximately 43% share in 2026, entrenched by the AT(N) biomarker framework, FDA-approved amyloid and tau assay requirements for lecanemab and donanemab patient selection.

- Fast-Growing Biomarker Type - Genomic biomarkers are the fast-growing type, driven by NIH All of Us program data (750,000+ participants), expanding pharmacogenomic applications in CNS drug development, and validated roles of APOE ε4, LRRK2, and GBA variants in neurological disease stratification.

Market Dynamics

Drivers - Surging Alzheimer's Drug Pipeline Demanding Biomarker-Validated Patient Selection and Monitoring

The breakthrough approvals of amyloid-targeting Alzheimer's therapies are fundamentally reshaping demand for neurological biomarkers by creating mandatory diagnostic gateway requirements for patient selection and treatment monitoring. The U.S. Food and Drug Administration (FDA) approved lecanemab (Leqembi) by Eisai/Biogen in July 2023 and donanemab (Kisunla) by Eli Lilly in July 2024 for early Alzheimer's disease, both requiring confirmed amyloid pathology via PET imaging or cerebrospinal fluid (CSF) biomarkers as a condition of treatment eligibility.

The commercial rollout of these therapies is creating direct, large-scale institutional demand for validated amyloid beta and tau biomarker assays. Eli Lilly's Lilly Diagnostics division and Fujirebio's plasma biomarker platforms are at the forefront of this rapidly expanding diagnostic infrastructure requirement, positioning neurological biomarkers as a critical commercial bottleneck in the Alzheimer's treatment pathway.

Blood-Based Neurological Biomarker Innovation Enabling Scalable, Minimally Invasive Diagnostics

The emergence of validated, ultrasensitive blood-based neurological biomarker assays is fundamentally transforming the clinical scalability and commercial addressability of the neurological biomarkers market. Historically, CSF biomarker collection via lumbar puncture limited adoption due to invasiveness, but advances in single-molecule array (Simoa) technology, pioneered by Quanterix and mass spectrometry-based plasma assays now enable detection of sub-picogram concentrations of neurofilament light chain (NfL), phosphorylated tau (p-tau217), and amyloid beta 42/40 ratios from standard blood draws.

The Alzheimer's Association and Alzheimer's Disease Neuroimaging Initiative (ADNI) have published extensively, validating the diagnostic concordance of plasma biomarkers with CSF and PET reference standards. The National Institute on Aging (NIA) has designated blood-based biomarkers as a research priority, with multiple NIH-funded programs accelerating clinical validation, opening a pathway to population-scale screening.

Restraints - Lack of Standardized Analytical Platforms and Inter-Laboratory Variability

A critical technical barrier constraining neurological biomarker adoption is the absence of universally standardized analytical platforms, reference materials, and harmonized cutoff values across laboratories globally. Published inter-laboratory comparison studies have demonstrated significant coefficient of variation (CV) differences of 15-40% for key biomarkers, including NfL and p-tau assays across different immunoassay and mass spectrometry platforms. The Global Biomarker Standardization Consortium (GBSC) and Alzheimer's Association are working toward harmonized reference standards, but clinical implementation of standardized cutoffs remains a work in progress, limiting confidence in cross-site result interpretation and slowing regulatory-grade clinical validation of emerging blood-based platforms.

High Cost of Neuroimaging Biomarkers and Restricted Access in Low-Resource Settings

Neuroimaging biomarkers, particularly amyloid and tau PET imaging with tracers such as florbetapir (Amyvid), florbetaben (Neuraceq), and flortaucipir (Tauvid) remain prohibitively expensive for broad clinical deployment, with a single amyloid PET scan costing approximately USD 3,000-5,000 in the U.S.. Despite CMS coverage decisions expanding Medicare reimbursement for amyloid PET in confirmed Alzheimer's treatment pathways, access remains limited in rural settings and developing economies. This cost barrier concentrates neuroimaging biomarker utilization within academic medical centers and specialty memory clinics, constraining broader population-level market penetration.

Opportunities - Genomic Biomarkers: The Fastest-Growing Segment Driven by Pharmacogenomics and Precision Neurology

Genomic neurological biomarkers represent the fastest-growing category, propelled by advances in whole-genome and whole-exome sequencing, expanding pharmacogenomic applications in neurological drug development, and growing clinical utility of genetic risk stratification for neurodegenerative disease. Variants in genes including APOE ε4 for Alzheimer's risk, LRRK2 and GBA for Parkinson's disease, and SMN1 for spinal muscular atrophy have established, validated roles in diagnosis, prognosis, and therapy selection.

The NIH's All of Us Research Program has enrolled over 750,000 participants with linked genomic and health data, generating unprecedented neurological genomic datasets. Companies including Bio-Rad Laboratories, Thermo Fisher Scientific, and Illumina are developing validated next-generation sequencing panels targeting neurological disease gene panels, creating a high-growth instrumentation and reagent demand vector for research and clinical laboratory end-users.

Biopharma Sector as Highest-Value End-User: Companion Diagnostics and Clinical Trial Biomarker Co-Development

Biopharma companies represent the highest-value and fastest-growing end-user segment within the neurological biomarkers market, driven by the critical role of biomarkers in de-risking clinical trial design, validating patient stratification, and supporting regulatory submissions for disease-modifying therapies. The IQVIA Institute for Human Data Science reports that the global neurological drug pipeline exceeds 1,200 active clinical programs as of 2024, with biomarker endpoints increasingly mandated as primary or secondary outcomes by FDA and EMA regulators.

Co-development agreements between biomarker platform companies and biopharma clinical programs such as Quanterix's Simoa partnerships with leading CNS drug developers generate recurring, high-margin assay service revenue. FDA's Biomarker Qualification Program and the Critical Path Institute's Coalition Against Major Diseases (CAMD) are providing regulatory clarity that accelerates biomarker qualification and commercial deployment in drug trials.

Category-wise Analysis

Biomarker Type Insights

Proteomic biomarkers lead the biomarker type category, commanding approximately 43% of total market share in 2026. Protein-based neurological biomarkers including amyloid beta 42/40, total tau, phosphorylated tau (p-tau181, p-tau217), neurofilament light chain (NfL), and glial fibrillary acidic protein (GFAP) represent the most clinically validated and commercially deployed category in both CSF and emerging blood-based formats. The Alzheimer's Association Research Roundtable has established these proteomic markers as core components of the AT(N) biomarker framework for Alzheimer's disease classification.

Fujirebio's Lumipulse platform and Quanterix's Simoa technology are the leading commercially deployed proteomic assay platforms with the deepest clinical validation evidence bases. The mandatory use of amyloid and tau protein biomarkers for lecanemab and donanemab patient selection further entrenches proteomic biomarker dominance in this market.

Sample Analysis

Blood (including plasma) samples represent the leading and fast-growing sample category, accounting for approximately 47% share in 2026 The shift from CSF-based to blood-based neurological biomarker testing is the defining structural transformation of this market, driven by superior patient accessibility, scalability, and potential for population-level screening programs. Plasma p-tau217 assays have demonstrated concordance rates of over 90% with amyloid PET in published studies in the Journal of the American Medical Association (JAMA), establishing clinical-grade confidence in blood-based Alzheimer's diagnostics.

The FDA's Breakthrough Device Designation for multiple plasma biomarker platforms including Lilly's p-tau217 plasma test and C2N Diagnostics' PrecivityAD2 validates the regulatory trajectory. CSF biomarkers remain clinically important as confirmatory tests in specialized memory clinic settings, but blood-based platforms are rapidly expanding the addressable end-user base.

Indication Insights

Alzheimer's disease (AD) is the dominant indication segment, estimated at approximately 40% of global share in 2026. Alzheimer's disease affecting over 55 million people worldwide per the Alzheimer's Disease International (ADI) represents the single largest neurological disease burden and the most commercially developed neurological biomarker indication. The FDA approvals of lecanemab and donanemab have created mandatory biomarker-gated treatment pathways, directly driving large-scale clinical deployment of amyloid and tau biomarker assays. The Alzheimer's Association's revised diagnostic criteria emphasizing biological confirmation now positions biomarker testing as central to the clinical workup rather than supplementary. Multiple Sclerosis (MS) is the second-largest indication, with NfL serving as a validated treatment response and disease activity biomarker endorsed by the European Committee for Treatment and Research in Multiple Sclerosis (ECTRIMS).

End-user Insights

Biopharma companies are the leading end-user segment, accounting for approximately 34% of global market share in 2026. The pharmaceutical and biotechnology industry's intensive investment in CNS drug development with over 1,200 active neurological clinical programs globally per IQVIA creates the highest per-unit value demand for validated neurological biomarker assay services. Biomarker endpoints in Phase II/III clinical trials for Alzheimer's, Parkinson's, and MS therapies command premium pricing for assay validation, sample analysis, and data interpretation services.

Academic & Research Institutes represent the second-largest segment, driven by NIH- and EU Horizon Europe-funded neuroscience research programs deploying large biomarker sample cohorts. Hospital Labs are the fastest-growing clinical end-user, driven by expanding blood-based biomarker clinical implementation following FDA approvals and CMS reimbursement decisions for Alzheimer's diagnostic pathways.

Regional Insights

North America Neurological Biomarkers Market Trends and Insights

North America leads the global neurological biomarkers market with approximately 39% share in 2026, anchored by the world's most active CNS drug development ecosystem, robust NIH neuroscience research funding exceeding USD 47 billion annually, and the transformative FDA approvals of amyloid-targeting Alzheimer's therapies creating immediate large-scale biomarker infrastructure demand.

U.S. Neurological Biomarkers Market Size

The United States dominates North America, accounting for approximately 89% of regional revenue in 2026, estimated at around US$ 3.4 billion. FDA approvals of lecanemab and donanemab, combined with CMS coverage expansion for amyloid PET imaging, are driving unprecedented clinical deployment of Alzheimer's biomarker assays across specialized memory centers and academic medical institutions.

Europe Neurological Biomarkers Market Trends and Insights

Europe is the second-largest market, with strong academic neuroscience research programs, EU Horizon Europe neurodegenerative disease funding, and progressive clinical adoption of blood-based NfL and p-tau biomarkers across Germany, U.K., France, and the Netherlands. EMA regulatory frameworks are supporting biomarker qualification pathways aligned with the U.S. FDA Biomarker Qualification Program.

Germany Neurological Biomarkers Market Size

Germany is Europe's largest neurological biomarkers market, estimated at approximately US$ 650 million in 2026 representing around 27% of European revenue. Germany's leading neuroscience institutions—including the Deutsches Zentrum für Neurodegenerative Erkrankungen (DZNE)—and its large biopharma sector with active CNS clinical programs sustain robust biomarker platform demand.

U.K. Neurological Biomarkers Market Size

The United Kingdom holds approximately 18% of the regional share in 2026. The UK Dementia Research Institute (UK DRI), funded with £290 million, and NHS memory services integrating biomarker-based diagnostic pathways are key demand drivers for both CSF and emerging blood-based neurological biomarker platforms.

France Neurological Biomarkers Market Size

France accounts for approximately 13% of European market revenue in 2026. The French Plan Maladies Neurodégénératives (PMND) and network of CMRR (Memory Resource and Research Centers) across France actively deploy CSF and blood-based biomarker protocols for Alzheimer's and neurodegeneration diagnostics, supporting consistent laboratory platform procurement.

Asia Pacific Neurological Biomarkers Market Trends and Insights

Asia Pacific is the fast-growing regional market, driven by rapidly expanding neuroscience research investment, aging population demographics, and growing biopharma CNS clinical trial activity. China is the region's dominant market, with the National Natural Science Foundation of China (NSFC) substantially increasing neurodegeneration research funding and domestic biopharma companies, including Zai Lab and BeiGene, expanding CNS drug pipelines requiring biomarker infrastructure.

India Neurological Biomarkers Market Size

India represents a high-growth emerging market for neurological biomarkers, estimated at approximately US$ 195 million in 2025, accounting for around 10% of Asia Pacific revenue. Growing neuroscience academic research, expanding CRO clinical trial infrastructure, and rising awareness of Alzheimer's disease affecting approximately 4 million people in India, per the Alzheimer's and Related Disorders Society of India (ARDSI) are key demand drivers.

Competitive Landscape

The global neurological biomarkers market is highly competitive, driven by continuous innovation in early disease detection and precision diagnostics for disorders such as Alzheimer’s, Parkinson’s, and multiple sclerosis. Companies compete through advanced biomarker discovery platforms, strong clinical validation, and expansion of diagnostic portfolios across proteomics, genomics, and neuroimaging. Strategic collaborations with research institutes, hospitals, and pharmaceutical firms accelerate biomarker development and commercialization.

Investments in AI-powered analytics, liquid biopsy technologies, and personalized medicine approaches are strengthening market presence. Regulatory approvals and growing demand for non-invasive diagnostic solutions further intensify competition across global healthcare and life sciences markets.

Key Developments

- In March 2025, A recent study by CSL, Australia-based, validated Brainomix's imaging biomarkers as reliable predictors of clinical outcomes in stroke patients. The findings demonstrated improved diagnostic accuracy and treatment decisions, supporting the technology’s clinical value in stroke care.

- In December 2024, ESYA Labs partnered with Alamar Biosciences to enhance biomarker detection and diagnostics for neurological diseases, combining their expertise in lysosomal biology with Alamar's NULISA platform and ARGO HT System.

- In July 2024, Biogen Inc., Beckman Coulter, and Fujirebio collaborated to identify and develop blood-based tau biomarkers, aiming to advance and commercialize tests for Alzheimer’s disease and support future therapies targeting tau pathology.

Companies Covered in Neurological Biomarkers Market

- Quanterix

- Amoneta Diagnostics

- Bio-Rad Laboratories, Inc

- Eli Lilly and Company

- IXICO plc

- Biognosys

- Revvity

- Beckman Coulter, Inc.

- PreOmics GmbH

- ADx NeuroSciences NV (A Fujirebio Company)

- Fujirebio

- Brainomix

- Merck KGaA

- Bio-Techne

Frequently Asked Questions

The global neurological biomarkers market is estimated at US$ 9.8 billion in 2026.

The primary demand drivers in the Neurological Biomarkers market include the rising prevalence of neurological disorders such as Alzheimer’s disease, Parkinson’s disease, multiple sclerosis, and epilepsy, which increase the need for early and accurate diagnosis.

North America leads with approximately 39% of global market share in 2025. The U.S. dominates, driven by NIH neuroscience funding exceeding USD 47 billion annually, transformative FDA Alzheimer's drug approvals mandating biomarker infrastructure, and the world's highest concentration of biopharma CNS drug development activity.

Expanding applications of AI-integrated biomarker analysis, liquid biopsy technologies, and companion diagnostics for targeted therapies further create high-growth opportunities. Additionally, increasing demand for precision medicine and biomarker-guided clinical trials in neurology offers strong long-term commercial potential across diagnostics, therapeutics, and pharmaceutical research.

Leading players include Quanterix Corporation, Fujirebio Holdings, Bio-Techne Corporation, Bio-Rad Laboratories, Eli Lilly and Company, Revvity, Beckman Coulter, Merck KGaA, and ADx NeuroSciences NV.