- Communication Infrastructure & Services

- Network Forensics Market

Network Forensics Market Size, Share, and Growth Forecast 2026–2033

Network Forensics Market by Offering (Software, Services), by Deployment Mode (Cloud-based, On-premise, Hybrid), Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), End-user (BFSI, Government & Defense, Healthcare, Energy & Utilities, IT & Telecom, Manufacturing, Retail & E-commerce, Others), and Regional Analysis, 2026–2033

Global Network Forensics Market Size and Trend Analysis

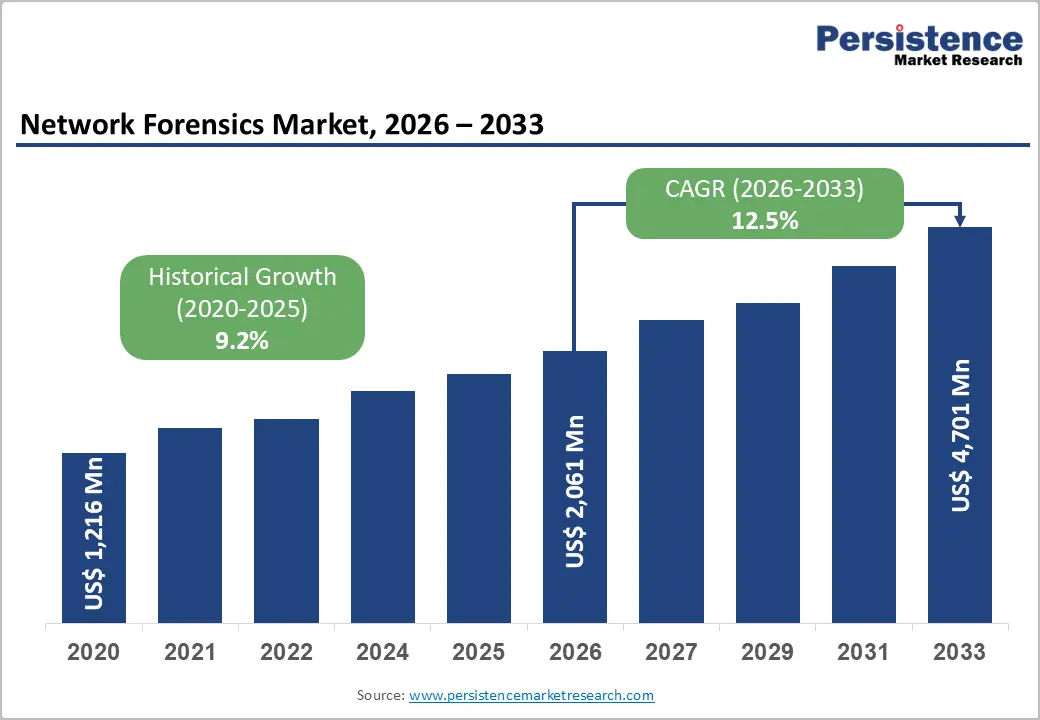

The global network forensics market size is expected to be valued at US$ 2,061.1 million in 2026 and is projected to reach US$ 4,700.8 million by 2033, growing at a CAGR of 12.5% between 2026 and 2033. This trajectory reflects surging enterprise demand for real-time packet capture, deep-packet inspection, and post-breach forensic reconstruction capabilities. The proliferation of sophisticated ransomware, advanced persistent threats (APTs), and state-sponsored intrusions has compelled organisations across every vertical to invest heavily in purpose-built network forensics tooling. Regulatory mandates, including the European Union's NIS2 Directive, the U.S. Cybersecurity and Infrastructure Security Agency (CISA) frameworks, and sector-specific compliance requirements, are further accelerating adoption by making forensic audit trails a legal necessity rather than a strategic choice.

Key Industry Highlights:

- Leading Offering: Software dominates with over 67.0% share in 2026, valued at more than US$ 1,380.94 Million, driven by enterprise demand for scalable, real-time packet capture, traffic analytics, and forensic reconstruction capabilities.

- Leading Deployment Mode: On-premise deployment holds over 35.0% market share in 2026, valued at more than US$ 721.38 Million, due to strong demand for data sovereignty, compliance, and forensic integrity in regulated industries.

- Fast-Growing Deployment Mode: Cloud-based deployment is the fastest-growing segment, driven by rapid cloud migration, scalability benefits, and increasing adoption of cloud-native security analytics.

- Leading Enterprise Size: Large Enterprises dominate with over 65.0% market share in 2026, valued at more than US$ 1,339.71 Million, supported by complex hybrid infrastructures, high data volumes, and stringent regulatory requirements.

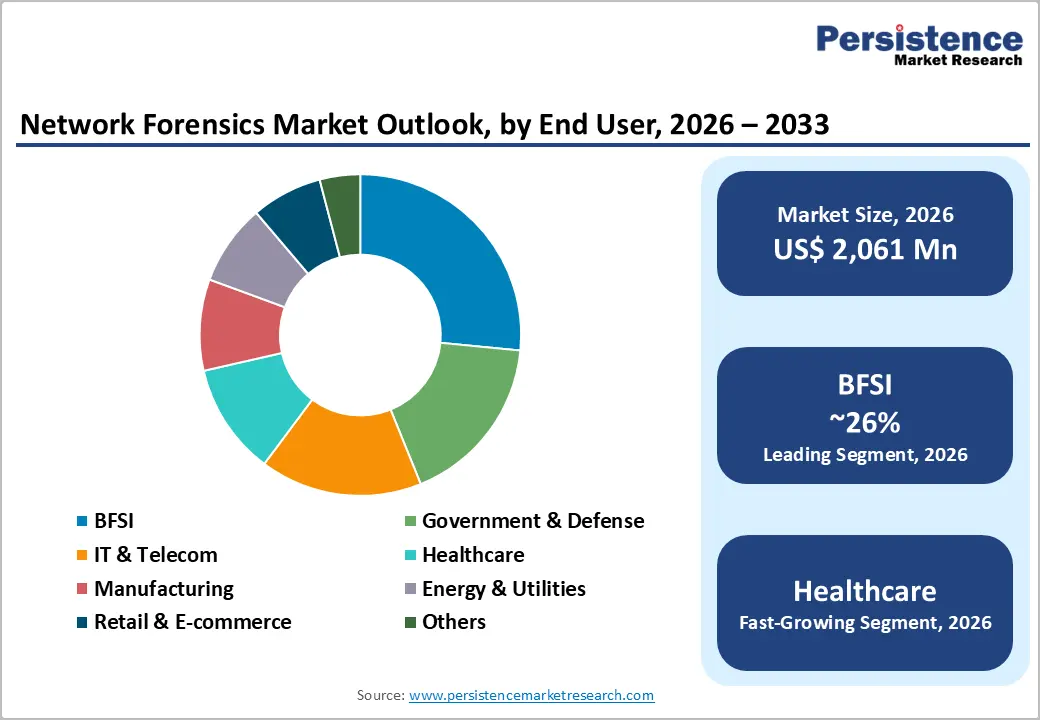

- Leading End-user: BFSI leads with over 26.0% market share in 2026, valued at more than US$ 535.89 Million, driven by high-value financial data exposure, strict regulatory oversight, and advanced cyber threat risks.

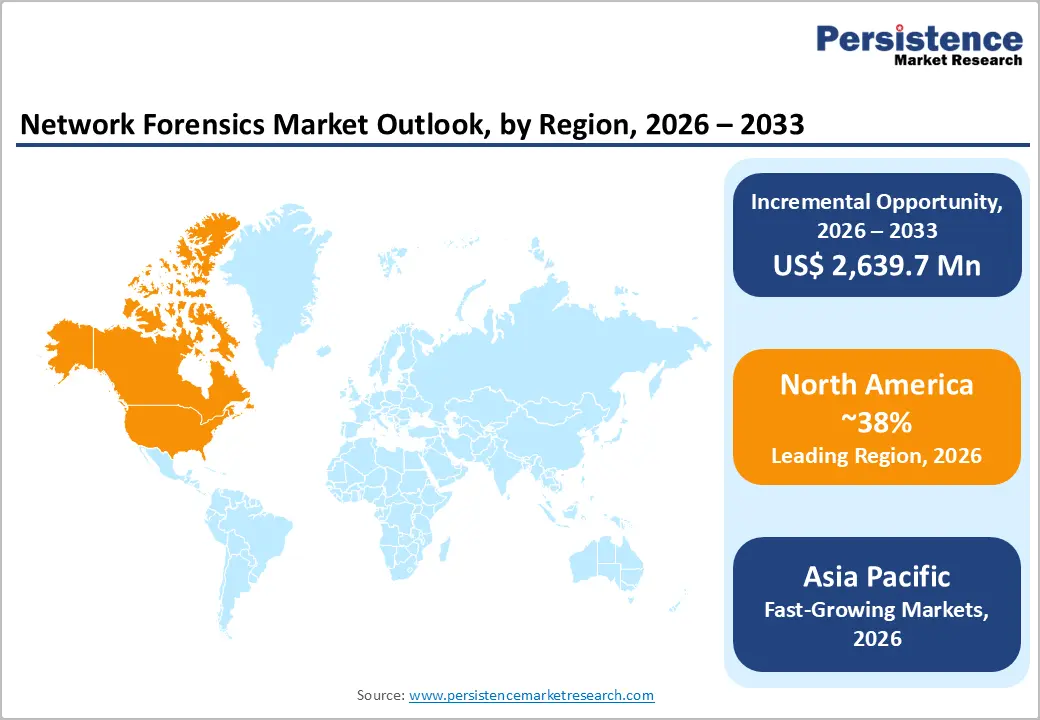

- Leading Region: North America dominates with over 38.0% market share in 2026, valued at US$ 783.22 Million, supported by advanced cybersecurity maturity, strong regulatory frameworks, and widespread SOC adoption.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a CAGR of 16.3%, driven by rapid digitalization, rising cyber threats, and increasing government investment in cybersecurity infrastructure.

Market Dynamics

Drivers - Surging Volume and Sophistication of Cyber Threats Compelling Investment in Deep Network Visibility

The irreversible escalation in both the frequency and technical complexity of cyberattacks targeting enterprise infrastructure is a defining feature of the current threat landscape. According to studies, ransomware incidents have increased by more than 50% year over year in recent reporting periods, with average dwell times, the duration during which attackers remain undetected inside a network, extending to several weeks in many enterprise environments.

Network forensics platforms address this challenge directly by enabling security teams to reconstruct attack timelines, identify lateral movement, and establish chain-of-custody evidence for legal proceedings. As threat actors increasingly exploit encrypted traffic and living-off-the-land techniques that evade endpoint detection, network-layer evidence capture is becoming the last reliable source of ground truth for incident responders.

Expanding Regulatory and Compliance Obligations Mandating Forensic Audit Capability

Regulatory pressure is one of the most structurally reliable demand drivers as compliance mandates create non-discretionary procurement cycles that persist through economic downturns. Frameworks such as the EU's General Data Protection Regulation (GDPR), the Health Insurance Portability and Accountability Act (HIPAA) in the United States, the Payment Card Industry Data Security Standard (PCI DSS), and the recently enacted NIS2 Directive all require organisations to demonstrate documented incident detection, investigation, and reporting capabilities.

Non-compliance penalties reaching up to €20 Million or 4% of global annual turnover under GDPR create a compelling financial case for investment in forensic infrastructure. Security and compliance teams that previously treated network forensics as a post-incident luxury increasingly treat it as a continuous, audit-ready function embedded within their security operations centres (SOCs).

Restraints - High Deployment Complexity and Skill Shortages Limiting Broad Adoption

Configuring and operating enterprise-grade network forensics platforms requires specialized skills in protocol analysis, traffic baseline, and forensic methodology that most mid-market organisations simply cannot source internally. The global cybersecurity workforce gap exceeded 4.8 million professionals in recent estimates, with forensic and incident response skills among the most acutely undersupplied competencies. This talent deficit slows procurement decisions, increases total cost of ownership, and in many cases causes licensed platforms to be underutilized, ultimately constraining the pace at which the network forensics space converts addressable demand into active deployment.

Data Volume Explosion Creating Storage, Processing, and Cost Scalability Challenges

Network traffic volumes scale exponentially, driven by cloud migration, Internet of Things (IoT) proliferation, and the adoption of 5G infrastructure. The cost and complexity of capturing, storing, and indexing full-packet data at enterprise scale create a significant adoption barrier.

Network forensics solutions must ingest and index terabytes to petabytes of traffic daily to maintain forensic fidelity, and the infrastructure required to do so at scale introduces substantial capital and operational expenditure. Organisations operating under tight security budgets, particularly Small and Medium-sized Enterprises (SMEs) and public-sector entities in emerging markets, frequently defer full-fidelity forensics deployments in favour of less comprehensive log-based alternatives.

Opportunities - Cloud-Native Forensics-as-a-Service Models Opening a High-Growth Untapped Segment

The accelerating enterprise migration to multi-cloud and hybrid cloud architecture creates a compelling opportunity for vendors to deliver network forensics capabilities through scalable, consumption-based cloud models. Vendors investing in agentless cloud traffic mirroring, API-native integrations with hyperscaler environments including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), and elastic storage architectures capture share from enterprises re-evaluating their forensic stack during cloud transformation programmes.

Vendors should prioritise tight integrations with cloud-native security information and event management (SIEM) and extended detection and response (XDR) platforms to embed forensics capabilities within existing security workflows rather than positioning them as standalone products.

SME Market Expansion Through Managed Security Service Provider (MSSP) Channel Partnerships

SMEs historically lacked the budget, staff, and infrastructure to deploy and operate dedicated network forensics platforms, but MSSP-delivered forensics services allow them to access enterprise-grade capabilities through a predictable, opex-structured monthly subscription. Regulatory pressure on SMEs is intensifying, particularly in Europe, following NIS2 scope expansion to cover mid-size organisations in critical sectors, creating a compliance-driven pull that MSSPs are well-positioned to fulfil. Vendors that build MSSP-optimised licensing models featuring multi-tenancy, centralised management consoles, and tiered forensic depth stand to unlock a structurally large and previously inaccessible revenue pool.

Category-wise Analysis

Offering Insights

Software segment accounts for 67.0% of the global Network Forensics market in 2026, equivalent to US$ 1,380.94 million, due to enterprise and government demand for scalable, continuously upgradable investigative platforms that enable real-time packet capture, traffic analytics, and forensic reconstruction. Organizations increasingly prioritize in-house software deployments to ensure full control over sensitive network evidence, meet regulatory and compliance requirements, and strengthen incident response and legal defensibility through reliable chain-of-custody data management.

The services segment is expected to grow at a significant rate due to increasing demand for specialized expertise in threat investigation, incident response, and forensic analysis. Many organizations lack in-house capabilities to manage complex, multi-vector cyberattacks, driving reliance on managed security and forensic services. The rising frequency of advanced persistent threats (APTs) and ransomware attacks further accelerates the need for rapid, expert-led investigation support. Services provide continuous monitoring, deployment support, and platform optimization, which are critical for organizations with evolving and resource-constrained security teams.

Deployment Mode Insights

On-premise deployment mode accounts for over 35.0% of the share in 2026, reaching over US$721.38 million value, as organisations in highly regulated and security-sensitive sectors prioritize data sovereignty, compliance, and forensic integrity. Regulatory frameworks across the United States, European Union, and several Asia-Pacific jurisdictions enforce strict data residency and auditability requirements, often necessitating that full-packet network traffic and forensic logs remain within organisation-controlled infrastructure. Enterprises continue to prefer on-premise and hybrid deployments to ensure secure retention, chain-of-custody preservation, and compliance with evolving cybersecurity and data protection mandates.

Cloud-based deployment mode is the fast-growing segment, driven by accelerating enterprise cloud adoption and the increasing availability of cloud-native forensic and security analytics capabilities offered by hyperscalers and SaaS providers. Organizations are prioritizing these deployments to reduce infrastructure overhead, improve scalability, and enable faster investigation across distributed environments. While on-premise deployments continue to serve high-security and legacy environments, the market is gradually shifting toward cloud and hybrid models as their operational and compliance maturity improves.

Organization Size Insights

Large Enterprises segment is expected to account for more than 65.0% of the share in 2026, reaching over to US$ 1,339.71 million, driven by their need for advanced network visibility and forensic capabilities. These organisations operate highly complex and distributed infrastructures spanning data centres, branch networks, cloud environments, and industrial systems, which require continuous, high-fidelity traffic capture for effective threat detection and incident reconstruction. Rising regulatory compliance requirements and exposure to sophisticated multi-vector cyberattacks further necessitate robust network forensics solutions capable of delivering end-to-end visibility across hybrid environments.

Small and Medium-sized Enterprises (SMEs) represent the fastest-growing, propelled by rising regulatory obligations under frameworks such as NIS2 and PCI DSS v4.0, as well as increasing cyber incident exposure. Their adoption is enabled by MSSP-delivered and SaaS-based forensic solutions that reduce infrastructure, cost, and skills constraints. While large enterprises continue to dominate in absolute revenue due to complex, high-volume deployments, SMEs are accounting for a growing share of incremental demand as cloud-native and subscription-based models democratize access to forensic capabilities. This bifurcation underscores a dual market need for advanced, scalable feature sets for large enterprises and simplified, cost-efficient, compliance-oriented solutions for SMEs.

End-user Insights

BFSI accounts for over 26.0% of the global network forensics market in 2026, equivalent to US$ 535.89 Million, driven by its exceptionally high threat exposure arising from high-value financial data, real-time transaction systems, and increasingly sophisticated cyberattacks. Financial institutions operate under stringent regulatory frameworks from bodies such as FINRA and the European Banking Authority (EBA), which mandate strong capabilities for monitoring, logging, and incident response. These requirements indirectly create sustained demand for network forensics solutions, as organizations must be able to reconstruct attack paths, ensure audit readiness, and support regulatory investigations

Healthcare is the fast-growing end-user segment, accelerated by a sharp rise in ransomware attacks targeting hospital systems, increasing deployment of connected medical and IoMT devices, and stringent regulatory frameworks such as HIPAA that mandate breach detection, investigation, and audit readiness. This combination of elevated threat exposure and compliance pressure is accelerating demand for deep network visibility and forensic reconstruction capabilities across clinical and hospital IT environments. For vendors, this represents a high-value vertical expansion opportunity, particularly in solutions tailored for healthcare networks and medical device traffic monitoring.

Regional Insights

North America Network Forensics Market Trends and Insights

North America accounts for over 38.0% of the global network forensics market in 2026, representing US$ 783.22 Million, driven by advanced enterprise security maturity, stringent regulatory enforcement, and widespread adoption of zero-trust architectures. The region’s leadership is reinforced by deep SOC integration, high cybersecurity spending density, and strong federal initiatives mandating advanced threat detection and forensic capabilities.

The United States Network Forensics market is expected to surpass US$ 657.90 Million value by 2026, supported by extensive enterprise compliance requirements such as the NIST Cybersecurity Framework, financial sector regulations, and federal zero-trust mandates. The high concentration of Fortune 500 enterprises further accelerates demand for network forensic solutions that enable real-time investigation, attack reconstruction, and regulatory-grade evidence generation.

Europe Network Forensics Market Trends and Insights

Europe accounts for 27.0% of the global Network Forensics market in 2026, representing US$ 556.50 Million value. The EU's NIS2 Directive, which came into force in October 2024, significantly expanded the scope of mandatory cybersecurity obligations to include mid-size organisations in essential and important sectors, creating a substantial wave of new forensic investment demand. Combined with GDPR breach investigation requirements and the EU Cyber Resilience Act (CRA), regulatory compliance is the primary structural driver of network forensics market growth in the European region.

Germany Network Forensics market accounts for more than 21.0% of the European regional market in 2026, equivalent to US$ 116.86 Million, driven by the country's industrial scale, advanced manufacturing sector exposure to OT network threats, and the Federal Office for Information Security (BSI)'s role in setting rigorous national cybersecurity standards. The United Kingdom Network Forensics market is expected to surpass US$ 105.73 Million value in 2026, sustained by a mature financial services sector, an active government cybersecurity programme led by the National Cyber Security Centre (NCSC), and post-Brexit regulatory alignment efforts that maintain high cybersecurity standards.

Asia Pacific Network Forensics Market Trends and Insights

Asia Pacific accounts for over 24.0% of the share in 2026, representing US$ 494.66 Million, and it is the fast-growing market in the network forensics space, expanding at a projected CAGR of 16.3% driven by rapid digitisation of economies with previously low cybersecurity maturity baselines, surging government investment in national cyber defence capabilities and the proliferation of cyber incidents targeting financial institutions, healthcare systems, and critical infrastructure.

The China Network Forensics market is expected to exceed the value of US$202.81 Million by 2026, due to rising cybersecurity demand in response to increasing attack surfaces, as enterprises rapidly adopt cloud computing, 5G networks, IoT ecosystems, and hybrid IT infrastructures, which significantly increase network complexity and investigative requirements.

The Japan Network Forensics market is expected to surpass the value of US$84.09 Million, driven by rising cybersecurity threats targeting critical infrastructure and the government’s strengthened national cybersecurity framework following high-profile cyber incidents. Increasing regulatory emphasis on incident preparedness, real-time network monitoring, and forensic investigation capabilities is accelerating adoption across key sectors such as financial services, semiconductors, and critical infrastructure operators.

India Network Forensics market represents over 14.0% of the Asia Pacific regional market in 2026, equivalent to US$ 69.25 Million, fueled by regulatory compliance in financial services, increasing frequency and sophistication of cyberattacks on critical infrastructure sectors such as government and healthcare, and the growing requirement for SOC-enabled monitoring and forensic capabilities within India’s expanding IT services ecosystem serving both domestic and global clients.

Competitive Landscape

The network forensics market reflects a moderately concentrated competitive structure at the upper tier, where a small number of established cybersecurity platforms compete based on integration depth, platform breadth, and enterprise relationships. Below this tier, the network forensics competitive landscape becomes meaningfully fragmented, with a significant number of specialist vendors competing on technical differentiation, particularly in AI-driven anomaly detection and cloud-native forensic architectures. Vendor differentiation increasingly centres on the ability to deliver cross-environment forensic coverage spanning on-premise, cloud, and OT network layers within a single management interface.

Key Developments:

- In April 2026, the U.S. Cybersecurity and Infrastructure Security Agency (CISA) is investigating a suspected backdoor, dubbed Firestarter, found on Cisco firewall devices within a federal network. The intrusion raised concerns about potential unauthorized access and persistence mechanisms in critical infrastructure systems. Cisco is working with CISA to assess the scope of the compromise and mitigate any security risks.

- In September 2025, Darktrace introduced new automated forensics capabilities within its ActiveAI Security Platform, enabling organizations to rapidly investigate and reconstruct cyberattack activity across network, cloud, and host environments. The enhancement leverages AI to accelerate evidence collection and incident analysis for faster threat response. This strengthens its positioning in AI-driven cybersecurity and network forensics capabilities.

Companies Covered in Network Forensics Market

- Cisco Systems

- IBM

- Broadcom

- NETSCOUT Systems

- Palo Alto Networks

- Fortinet

- Trellix

- RSA Security

- Viavi Solutions

- NIKSUN

- LogRhythm

- Darktrace

- Vectra AI

- Check Point Software Technologies

- Others

Frequently Asked Questions

The global Network Forensics market is valued at US$ 2,061.10 Million in 2026 and is projected to reach US$ 4,700.75 Million by 2033, expanding at a CAGR of 12.5% over the forecast period, driven by the rising need for advanced cyberattack investigation capabilities and regulatory compliance across industries like BFSI, healthcare, and government.

The increasing frequency and sophistication of ransomware and APTs require deeper forensic visibility. Strict compliance mandates such as GDPR, NIS2, and HIPAA are pushing organisations to adopt forensic-ready security infrastructures.

Software dominates with an over 67.0% share in 2026, as organisations prefer scalable, AI-enabled forensic platforms for internal investigation and compliance. Its dominance is reinforced by demand for cloud-native, automated, and analytics-driven security solutions.

North America leads the market with a more than 38.0% share in 2026 due to high cybersecurity investment and strong regulatory enforcement. The need for advanced threat detection and nationwide zero-trust initiatives continues to drive strong enterprise adoption.

The key opportunity lies in cloud-native forensics-as-a-service to support multi-cloud and hybrid environments. Organizations increasingly need scalable solutions to close visibility gaps created by cloud migration and distributed infrastructures.

The leading companies in the Network Forensics Market include Cisco Systems, IBM, Broadcom, NETSCOUT Systems, Palo Alto Networks, Fortinet, among others.