- Beauty & Personal Care

- Nail Care Products Market

Nail Care Products Market Size, Share, and Growth Forecast 2026 - 2033

Nail Care Products Market by Product Type (Nail Polishes, Nail Hardeners & Strengtheners, Nail Removers, Cuticle Care Products, Nail Extensions & Enhancements, Nail Primers & Coats, Nail Tools & Accessories, Others), Pricing Level (Mass, Premium), Distribution Channel (Offline, Online), End-user (Individual Consumers, Professional Salons & Spas, Others), and Regional Analysis, 2026 - 2033

Nail Care Products Market Size and Trend Analysis

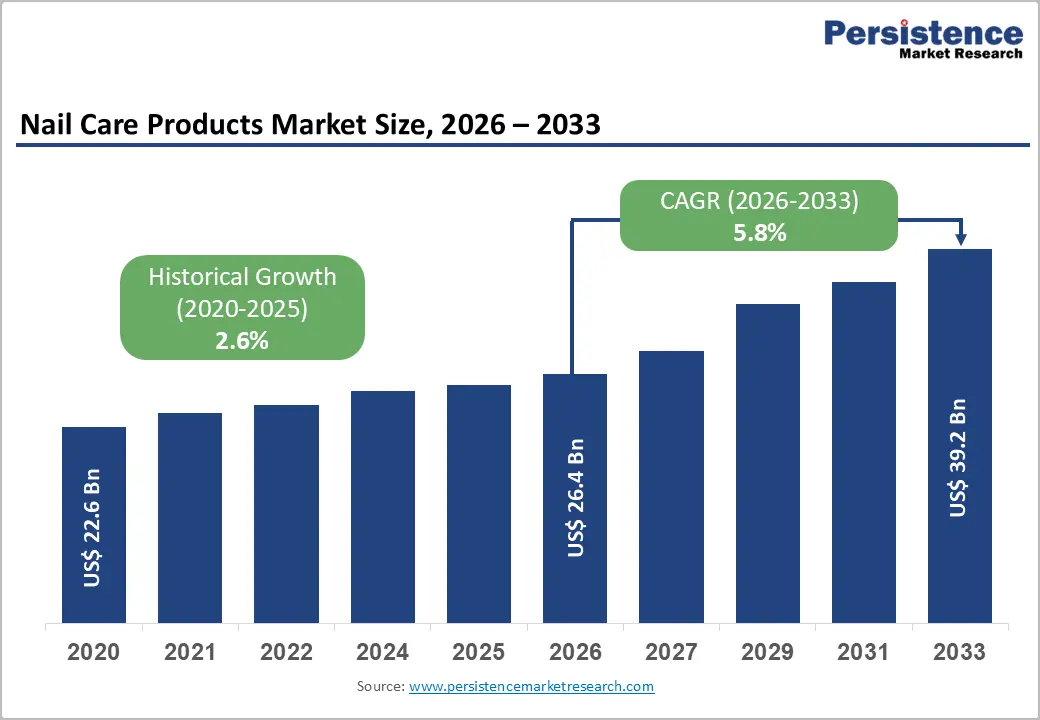

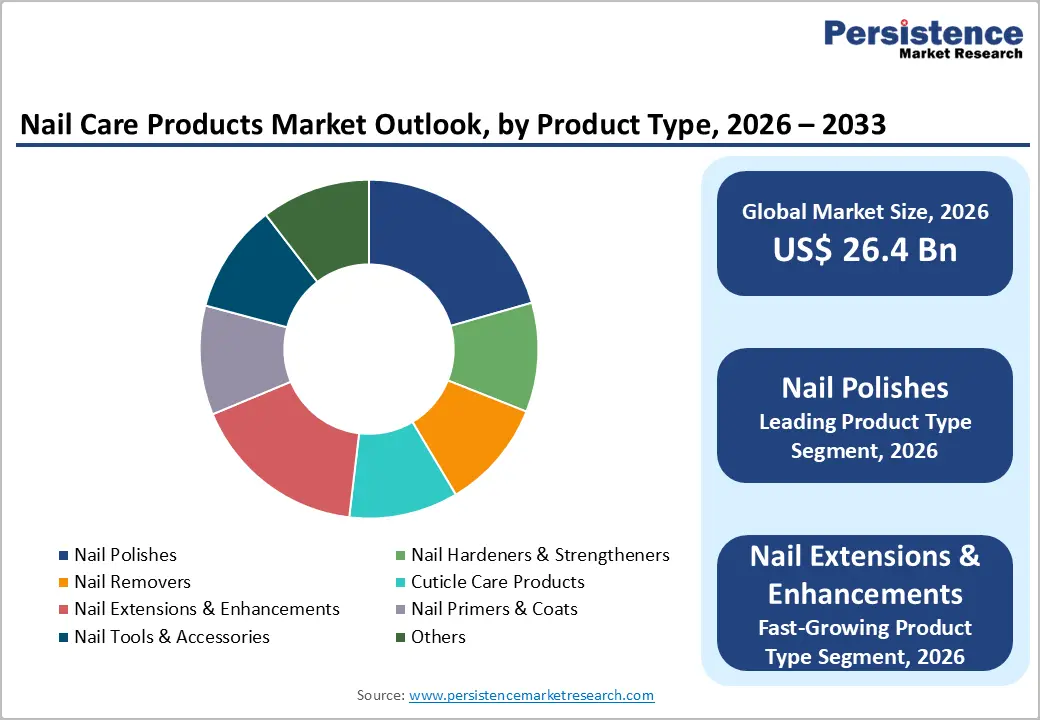

The global nail care products market size is expected to be valued at US$ 26.4 billion in 2026 and projected to reach US$ 39.2 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The market is benefiting from the expanding self-care economy, rising influence of social media beauty content, and growing acceptance of at-home nail grooming routines. According to the U.S. Bureau of Labor Statistics, employment in personal care services, including nail technicians, has shown consistent recovery post-pandemic, supporting professional channel sales. Simultaneously, brand innovation in long-wear formulas, vegan lacquers, and nail strengtheners is broadening the consumer base across age groups, while e-commerce penetration accelerates accessibility in emerging markets.

Key Industry Highlights:

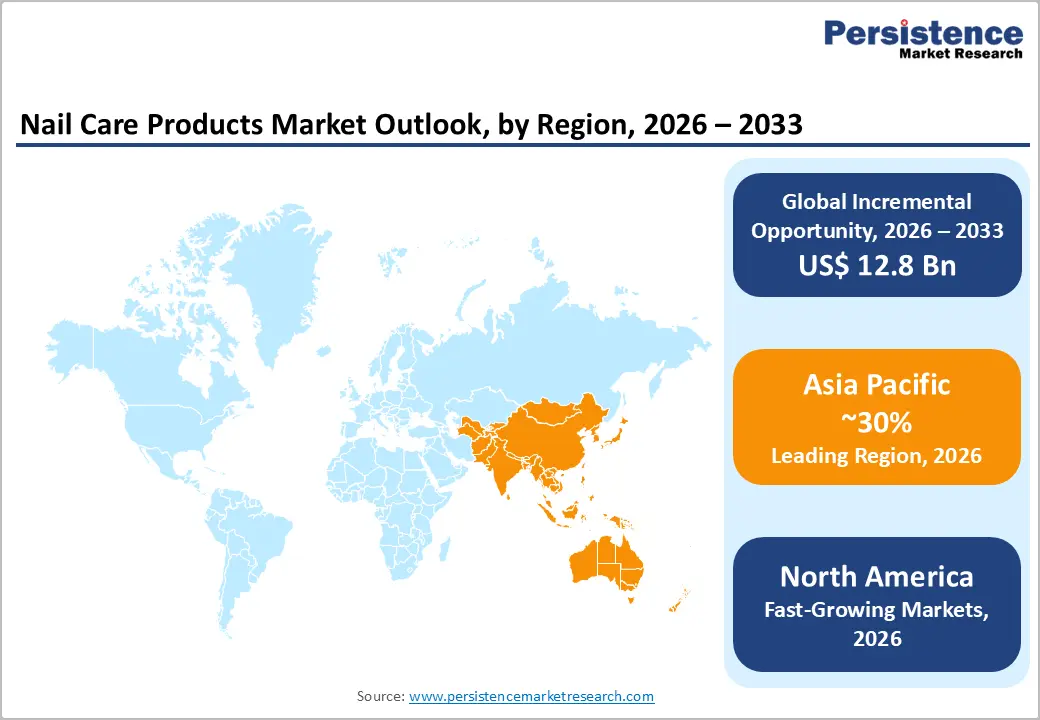

- Leading Region: Asia Pacific leads the global nail care products market with around 30% share in 2026, driven by China's beauty boom and K-beauty influence.

- Fastest Growing Region: North America is the fastest-growing region, expanding at a CAGR of nearly 6.4% through 2032, fueled by premiumization and at-home gel adoption.

- Dominant Segment: Nail polishes dominate with about 35% share in 2026, supported by broad consumer reach, low entry pricing, and viral social-media trend cycles.

- Fastest Growing Segment: Nail extensions & enhancements, especially press-on and gel-x systems, lead growth, propelled by viral nail-art trends and rising at-home application.

- Key Opportunity: Vegan, clean-label, and refillable nail formulations represent a major growth opportunity, with over 60% of global consumers favoring sustainable beauty products.

Market Dynamics

Is the Surge in Self-Grooming Culture Powered by Social Media Beauty Content?

The proliferation of beauty content across Instagram, TikTok, and YouTube has transformed nail care from a niche grooming habit into a mainstream self-expression category. According to Pew Research Center, over 70% of U.S. adults aged 18-29 use Instagram, and beauty content consistently ranks among the top three viewed verticals on short-video platforms, fueling repeat purchases of polishes, gels, and decorative nail tools.

Hashtag-driven movements such as #NailArt and #NailTok have collectively generated billions of views, sustaining purchase momentum across age groups. An American Academy of Dermatology advisory recognizes nail health as part of overall personal grooming, lending credibility to therapeutic and decorative formulations and supporting category-wide premiumization across both mass and prestige tiers within the global nail care landscape.

Do Expansion of Professional Salons and Subscription-Based DIY Nail Kits Attract Market Growth?

The professional nail services industry continues to expand globally, with the U.S. Bureau of Labor Statistics projecting 9% employment growth for manicurists and pedicurists between 2023 and 2033 faster than the average for all occupations. This professional demand translates directly into higher consumption of gel polishes, builder gels, base coats, top coats, and salon-grade implements across both mature and emerging consumer markets.

In parallel, the rise of subscription-based at-home nail kits from brands such as Olive & June and Manucurist is reshaping consumer access. Industry trade body Cosmetics Europe reports steady demand for hand and nail cosmetics, while DIY innovations like press-on nails and gel-x systems are emerging as structural growth levers in the broader nail care products market.

Does the Regulatory Scrutiny on Toxic Nail Polish Ingredients Worldwide Create Challenges?

Increasing regulatory action on harmful substances such as toluene, formaldehyde, and dibutyl phthalate collectively known as the "toxic trio" is constraining traditional nail polish formulations globally. The U.S. Food and Drug Administration (FDA) maintains strict cosmetic labeling requirements, while the European Commission under Regulation (EC) No 1223/2009 continues to expand its restricted-substance list, directly affecting product chemistry decisions.

California's Proposition 65 further obligates manufacturers to issue exposure warnings and reformulate impacted SKUs, while Health Canada enforces parallel hotlist restrictions. Compliance costs, reformulation timelines, and packaging disclosures slow product launches, particularly for small and mid-tier brands operating in the global beauty and personal care landscape, narrowing innovation budgets and delaying time-to-shelf for new color and treatment ranges.

Are the Rising Health Concerns from Gel and Acrylic Nail Systems Valid?

Rising dermatological concerns are limiting usage frequency among certain consumer cohorts within the long-wear nail segment. The British Association of Dermatologists has flagged a rising trend of methacrylate-related contact allergies linked to gel and acrylic nail systems, with patch-test data indicating that around 2.4% of tested patients show sensitivity to (meth)acrylate compounds widely used in salon-grade products.

UV/LED lamp exposure during gel curing has also raised long-term skin safety questions, with peer-reviewed studies in journals such as Nature Communications highlighting potential DNA damage risks from repeated exposure. These health concerns dampen volume growth in long-wear segments and pressure manufacturers to invest in safer methacrylate-free chemistries, slowing near-term innovation momentum and discouraging first-time gel users.

Emergence of Vegan, Clean-Label, and Sustainable Nail Care Formulate Innovation?

Clean beauty has evolved into a structural shift rather than a passing trend, opening significant white space for nail care brands willing to reformulate. Brands such as ORLY, Zoya, and Sundays are scaling "10-free" and "21-free" lacquer lines that exclude controversial chemicals, while bio-based solvents derived from cassava, corn, and sugarcane are gaining traction across both prestige and masstige nail polish portfolios globally.

Recyclable glass bottles, refill systems, and aluminum-cap packaging further differentiate eco-conscious offerings on shelf and online. Players securing third-party endorsements from Leaping Bunny, PETA, EWG Verified, or B Corp stand to capture share within the broader cosmetics and personal care market, especially as Gen Z and millennial consumers increasingly weigh ingredient transparency alongside performance and price when selecting nail products.

Does the Premiumization Through At-Home Gel Manicure System Adoption Generate Opportunities?

The democratization of salon-quality results at home is creating a high-value opportunity, particularly across North America and Europe. Brands like Le Mini Macaron, Manucurist, and Olive & June have launched LED-curing gel kits priced between US$ 50 and US$ 150, achieving strong direct-to-consumer traction with bundled lamps, base coats, top coats, removers, and curated shade libraries tailored for first-time at-home gel users.

According to the U.S. Census Bureau, e-commerce sales of health and personal care products grew over 8% year-on-year in 2024, indicating a highly receptive digital channel. Pairing premium pricing with educational content on YouTube and TikTok enables brands to recruit consumers who previously relied exclusively on professional salons, expanding lifetime customer value within the nail polish and treatment market.

Category-wise Analysis

Product Type Insights

Nail polishes continue to dominate the global nail care landscape, accounting for approximately 35% market share in 2025. The segment's leadership stems from broad consumer reach across age groups, low entry pricing, and continuous innovation in long-wear, vegan, and quick-dry formulas. Frequent shade launches tied to seasonal trends, celebrity collaborations from brands like OPI and Essie, and extensive shelf presence at Walmart and Target reinforce repeat purchases.

Nail extensions & enhancements is emerging as the fast-growing product type within the category. Demand is propelled by the viral popularity of press-on nails, gel-x systems, and dip powder kits popularized through TikTok and Instagram Reels. Brands such as Kiss Products, Static Nails, and Glamnetic are aggressively expanding their portfolios, while consumer preference for salon-style aesthetics at home strengthens long-term traction.

Pricing Level Analysis

Mass-priced nail care products lead the category, holding nearly 68% of total market share in 2025. Their dominance is anchored in widespread availability across drugstores, supermarkets, and discount retailers, with typical price points between US$ 3 and US$ 12. Brands such as Sally Hansen, Maybelline, and Revlon leverage scale manufacturing and dense distribution to deliver affordable, trend-aligned lacquers and treatments to value-conscious shoppers worldwide.

The Premium segment is registering the fastest growth within the pricing-level category. Affluent consumers are increasingly drawn to luxury lacquers from Chanel, Dior, and Hermès, alongside niche prestige players like Aprés Nail and Smith & Cult. Premiumization is further reinforced by clean-formula launches, refillable glass bottles, and salon-grade gel kits that justify higher price points and elevate aspirational brand positioning across mature beauty markets.

Distribution Channel Insights

Offline channels comprising specialty beauty retailers, supermarkets, hypermarkets, drugstores, and salon supply outlets continue to lead distribution with around 62% market share in 2025. Physical retail remains essential because shade-matching, finish previews, and brush-quality evaluation are inherently tactile experiences. Beauty specialists like Sephora, Ulta Beauty, and Boots continue to expand store footprints and dedicated nail bars to anchor in-store discovery and trial.

The Online channel is the fastest-growing distribution route, reshaping consumer purchase journeys across both mature and emerging markets. Direct-to-consumer brands such as Olive & June and Manucurist, paired with dominant marketplaces like Amazon, Shopee, and Lazada, are accelerating reach. Live-commerce on TikTok Shop and Instagram, influencer-led tutorials, and AI-powered shade-matching tools further fuel digital momentum and drive frequent, content-led repeat purchases.

End-user Insights

Individual consumers represent the leading end-user segment, capturing roughly 70% of total market share in 2025. The shift was accelerated during the COVID-19 pandemic when salon access was restricted, and the behavior has persisted as consumers grew comfortable with at-home manicures. According to Eurostat, household expenditure on personal care goods in the EU-27 has shown consistent year-on-year increases, with cosmetics forming a meaningful share.

Professional Salons & Spas form the fast-growing end-user segment, fueled by recovering footfall and the rapid global rollout of nail-focused franchises. According to the U.S. Bureau of Labor Statistics, employment of manicurists and pedicurists is projected to grow 9% between 2023 and 2033. Chains like Lakmé Salon, Regal Nails, and boutique nail bars across Asia Pacific are scaling rapidly, driving consumption of professional gels, builder formulas, and salon-grade tools.

Regional Insights

North America Nail Care Products Market Trends and Insights

North America is the fast-growing regional market, projected to record a CAGR of around 6.4% through 2032. Growth is fueled by premiumization, rising at-home gel kit adoption, social media-driven nail-art culture, and expanding clean-beauty offerings. Strong e-commerce infrastructure and a mature professional salon ecosystem further amplify regional momentum across both mass and prestige tiers.

- U.S. Nail Care Products Market Size

The U.S. accounts for nearly 85% of North America's nail care revenues, with an estimated market size of around US$ 6.5 billion in 2026. Growth is supported by U.S. Bureau of Labor Statistics data showing nearly 160,000 employed nail technicians, robust DTC brand activity, and consumer willingness to spend on premium and clean-label nail products.

Europe Nail Care Products Market Trends and Insights

Europe represents a mature yet steadily expanding market, supported by stringent product safety standards under Regulation (EC) No 1223/2009 and high consumer awareness of clean ingredients. Trends include vegan formulations, refillable packaging, and minimalist nude shades. According to Cosmetics Europe, the region's cosmetics retail value exceeded €88 billion in 2023, anchoring sustained demand for nail care.

- Germany Nail Care Products Market Size

Germany leads continental Europe with around 18% share of the regional nail care market. Strong drugstore retail through chains like dm and Rossmann, combined with consumer preference for vegan and dermatologist-tested products, drives demand. Statistisches Bundesamt data shows steady growth in cosmetics retail turnover, supporting the country's premium nail product expansion.

- U.K. Nail Care Products Market Size

The U.K. holds approximately 16% of the European nail care market. Growth is propelled by salon culture, influencer-led nail trends, and strong e-commerce penetration. According to the U.K. Office for National Statistics, online retail accounts for over 26% of total retail sales, benefiting digital-first nail brands such as Mylee and Manucurist UK.

- France Nail Care Products Market Size

France contributes nearly 14% to European nail care revenues. Backed by its global beauty heritage, the country drives demand for premium, eco-conscious lacquers. FEBEA (the French Federation of Beauty Companies) reports cosmetics as one of France's leading export industries, with nail care benefiting from the prestige of homegrown brands like Manucurist and Kure Bazaar.

Asia Pacific Nail Care Products Market Trends and Insights

Asia Pacific is the largest regional market with around 30% share in 2025, anchored by a thriving Chinese beauty industry, K-beauty influence, and rapid urbanization. China alone accounts for over 40% of regional revenues, supported by National Bureau of Statistics of China data showing cosmetics retail sales exceeding RMB 414 billion in 2023, with nail care a fast-rising sub-segment.

- India Nail Care Products Market Size

India represents one of the fastest-growing nail care markets in Asia Pacific, accounting for nearly 9% of regional revenues. Rising disposable incomes, expanding salon chains such as Lakmé Salon and VLCC, and Ministry of Statistics and Programme Implementation data showing growing personal care expenditure are key tailwinds for the country's nail care expansion.

- Japan Nail Care Products Market Size

Japan holds about 15% of Asia Pacific's nail care market, supported by a strong nail-art culture and the global influence of Japanese gel innovations. According to Japan External Trade Organization (JETRO), cosmetics remain a leading consumer category. The presence of brands like Bio Sculpture Japan and dense urban salon networks in Tokyo and Osaka sustain demand.

- Southeast Asia Nail Care Products Market Size

Southeast Asia accounts for nearly 12% of regional nail care revenues, led by Indonesia, Thailand, Vietnam, and the Philippines. ASEAN Cosmetic Association reports a vibrant cosmetics trade environment, with growing youth populations, rising urbanization, and rapid e-commerce growth via Shopee and Lazada driving accessible nail product distribution.

Competitive Landscape

The global nail care products market is moderately fragmented, with a healthy mix of multinational beauty conglomerates, regional specialists, and emerging direct-to-consumer disruptors competing across prestige and mass tiers. Established players leverage scale manufacturing, dense omnichannel distribution, and diversified brand portfolios spanning lacquers, treatments, and tools, while indie challengers differentiate through clean-label positioning, refillable packaging, and influencer-led storytelling.

Strategic priorities are converging around R&D in plant-based solvents, hybrid gel-lacquer chemistries, and skin-safe UV-LED curing systems. Emerging business models include subscription nail kits, salon-to-DTC hybrids, AR-powered shade matching, and viral social-commerce launches that compress traditional product life cycles and accelerate consumer acquisition.

Key Market Developments

- In January 2025, OPI (a Wella Company brand) launched its 'Big Zodiac Energy' collection, expanding its long-wear gel and lacquer portfolio with 12 zodiac-inspired shades, leveraging TikTok-led influencer marketing to deepen engagement with Gen Z and millennial nail enthusiasts globally.

- In September 2024, Olive & June was acquired by Helen of Troy for approximately US$ 240 million, signaling sustained M&A momentum in the at-home nail care segment and reinforcing strategic interest in direct-to-consumer beauty brands with strong digital communities and recurring revenue.

- In March 2024, Sally Hansen (owned by Coty Inc.) expanded its 'Good. Kind. Pure.' vegan and clean nail polish line with over 30 new shades, responding to rising clean-beauty demand and reinforcing its leadership in mass-market sustainable nail care formulations across North America.

Global Nail Care Products Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 22.6 billion |

|

Current Market Value (2026) |

US$ 26.4 billion |

|

Projected Market Value (2033) |

US$ 39.2 billion |

|

CAGR (2026-2033) |

5.8% |

|

Leading Region |

Asia Pacific, 30% market share |

|

Dominant Category-1 (Product Type) |

Nail Polishes, ~US$ 9.2 billion in 2026 |

|

Top-ranking Category-2 (Pricing Level) |

Mass, ~US$ 17.9 billion in 2026 |

|

Incremental Opportunity |

US$ 12.8 billion (2026-2033) |

Companies Covered in Nail Care Products Market

- L'Oréal S.A.

- Coty Inc.

- Revlon, Inc.

- Estée Lauder Companies Inc.

- Shiseido Company, Limited

- Wella Company (OPI Products)

- Kao Corporation

- Henkel AG & Co. KGaA

- Sally Hansen (Coty Inc.)

- Olive & June (Helen of Troy)

- Manucurist

- Mylee Cosmetics Ltd.

- ORLY International, Inc.

- Zoya / Art of Beauty, Inc.

- CND (Creative Nail Design)

- Kiss Products, Inc.

- Essie

- Maybelline

- Sundays Studio

- Le Mini Macaron

Frequently Asked Questions

The global nail care products market is expected to be valued at US$ 26.4 billion in 2026 and is projected to reach US$ 39.2 billion by 2033, growing at a CAGR of 5.8%.

Rising self-grooming culture, social media-driven nail trends, expanding professional salons, and growing adoption of at-home gel kits are the leading demand drivers, supported by data from the U.S. Bureau of Labor Statistics and Cosmetics Europe.

Asia Pacific leads with around 30% market share in 2025, driven by China's beauty industry, K-beauty influence, urbanization, and rapid e-commerce expansion across the region.

Vegan, clean-label, and sustainable nail care formulations represent the most significant opportunity, as over 60% of global consumers favor sustainable beauty products.

Leading players include L'Oréal S.A., Coty Inc., Revlon, Inc., Estée Lauder Companies, Shiseido, Wella Company (OPI), Olive & June, and Manucurist.