Industry: Healthcare

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 194

Report ID: PMRREP2982

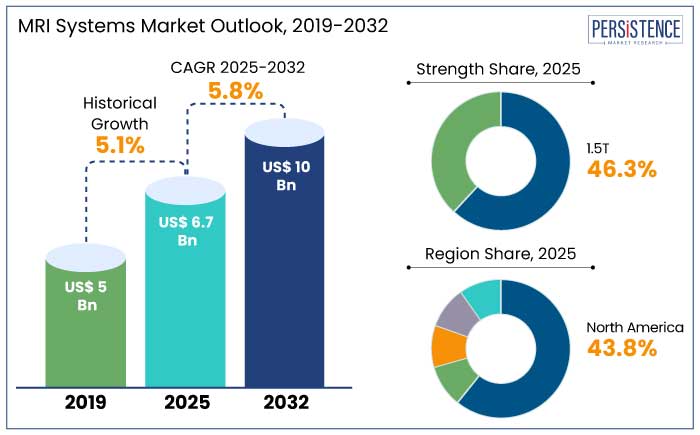

The global MRI systems market is predicted to reach a size of US$ 6.7 Bn by 2025. It is anticipated to showcase a CAGR of 5.8% during the forecast period to attain a value of US$ 10 Bn by 2032.

AI integration in MRI systems enables real-time image analysis, improves accuracy, and minimizes diagnostic times. AI-based MRI systems are estimated to reduce scan times by 50%, enhancing patient throughput.

Development of lightweight and portable MRI systems is a growing trend, especially for point-of-care diagnostics in rural and remote areas. Silent MRI systems, which reduce acoustic noise during scanning, are gaining traction to improve patient comfort and compliance. Prominent players like GE Healthcare and Siemens Healthineers have launched systems with noise levels as low as 77 dB compared to traditional levels of 110 to 120 dB.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

MRI Systems Market Size (2025E) |

US$ 6.7 Bn |

|

Projected Market Value (2032F) |

US$ 10 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

5.1% |

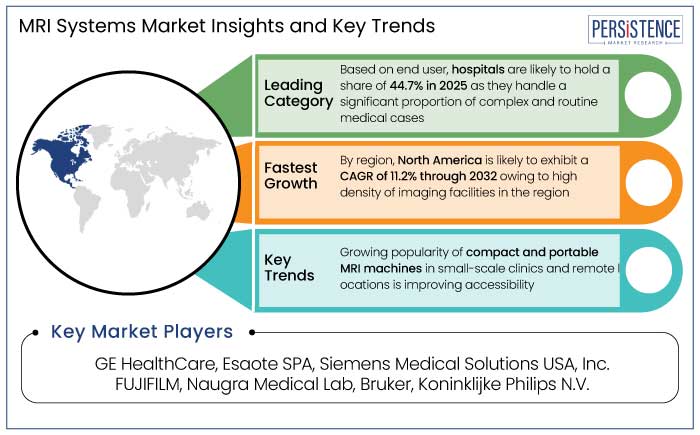

North America MRI systems market is estimated to hold a share of 43.8% in 2025. The region has one of the most developed healthcare systems across the globe with a strong focus on diagnostic imaging.

Increasing burden of chronic diseases in the region is propelling the demand for MRI systems. Over 6 million Americans live with Alzheimer’s disease, necessitating advanced imaging solutions like MRI for early detection.

The region is home to leading MRI system manufacturers, including GE Healthcare, Siemens Healthineers, and Philips, which are heavily investing in technological advancements. These companies are at the forefront of developing cutting-edge technologies like AI-enhanced imaging and 7T MRI systems.

1.5T is anticipated to hold a share of 46.3% in 2025. MRI systems with this strength are versatile and well-suited for imaging various clinical conditions, including neurological, musculoskeletal, cardiac, and abdominal disorders.

1.5T MRI systems provide high-quality images with adequate signal-to-noise ratios (SNR), making them ideal for general diagnostic imaging. Lower purchase and operational costs make 1.5T systems the preferred choice for smaller hospitals, outpatient centers, and developing healthcare markets.

These MRI systems cater to a majority of imaging needs in the healthcare settings. They offer excellent performance without the added challenges of 3T systems, like heating issues or susceptibility to artifacts.

Hospitals are anticipated to hold a share of 44.7% in 2025. Hospitals handle a significant proportion of complex and routine medical cases, making them the largest consumers of diagnostic imaging technologies like MRI.

Increasing prevalence of chronic diseases like cancer, neurological disorders, and cardiovascular conditions has further driven MRI demand in hospitals.

Hospitals are often better positioned to invest in expensive MRI systems owing to their access to funding through government support, grants, or private investments. For instance,

Potential growth in the global MRI systems industry is predicted to be driven by increased demand for advanced imaging technologies. AI-driven imaging systems are estimated to enhance diagnostic accuracy and decrease operational costs. For example,

Emerging economies are anticipated to witness double-digit growth in MRI installations owing to improving healthcare access and government investments. Compact MRI systems are projected to witness rapid adoption, particularly in rural and underserved areas, with portable MRI segment projecting substantial growth.

The MRI systems market growth was steady at a CAGR of 5.1% during the historical period. Growth during this period was driven by increasing adoption of high-strength MRI systems, technological innovations, and expanded healthcare infrastructure in emerging economies.

Introduction of portable and compact MRI machines expanded the market, especially in remote areas with limited healthcare access. Advancements in functional MRI (fMRI) enabled better diagnosis of neurological disorders, fueling demand.

Demand in the forecast period is likely to be driven by advancements in imaging technologies and an increasing demand for non-invasive diagnostic tools. The period is likely to witness increased adoption of 3T and 7T MRI systems as they offer superior image quality and detailed diagnostics.

Emergence of Customization and Modular MRI Systems

Modular MRI systems enable healthcare facilities to focus on specific diagnostic areas instead of investing in general-purpose MRI machines. For instance, orthopedic-focused MRI systems are gaining popularity owing to their lower cost and specialized imaging capabilities. Custom-built MRI systems assist in decreasing initial capital investment by avoiding unnecessary features. This flexibility is particularly appealing to small to medium-sized clinics.

Modular systems provide a scalable approach, enabling facilities to upgrade components such as coils or software without replacing the entire system. This reduces downtime and extends the system's lifecycle.

Rising Demand for Portable and Point-of-care MRI Systems

Portable MRI systems enable diagnostic imaging in remote or underserved areas with limited access to healthcare infrastructure.

Point-of-Care MRI systems provide immediate imaging in emergency departments and intensive care units (ICUs). This enhances diagnostic accuracy and patient outcomes during critical situations. For instance,

Mobile imaging solutions equipped with portable MRU systems are being deployed for onsite diagnostics in rural clinics and industrial settings. These systems are designed to be compact and lightweight, making them easy to transport and set up in various locations. For instance,

Risk of Claustrophobia and Noise Levels

Enclosed designs of conventional MRI systems can induce claustrophobia, anxiety, and panic in patients. For instance,

MRI scanners generate loud noises owing to their rapid magnetic field changes and gradient coil vibrations. These sounds can reach an uncomfortable level at some point. Extended exposure to such high noise levels can pose risks, especially for children.

Increasing Utilization in Neurological and Musculoskeletal Imaging

Rising prevalence of neurological disorders is propelling demand for MRI systems. For example,

Musculoskeletal disorders are the leading cause of disability worldwide. These conditions are often diagnosed and managed using MRI.

MRI systems offer a non-invasive and radiation-free alternative for detailed imaging of the brain, spinal cord, joints, and soft tissues. This is especially crucial for neurological patients where avoiding radiation exposure is critical for long-term monitoring.

Rising Adoption of AI and ML Integration

AI-driven MRI systems significantly decrease scan times, addressing one of the primary challenges in MRI procedures. Studies showcase that AI algorithms can cut MRI scan times by 50%, making the process more patient-friendly and cost-effective. For instance,

AI and ML enhance the sensitivity and specificity of MRI interpretation by identifying subtle patterns and anomalies that may be missed by radiologists.

AI-powered solutions streamline workflows by automating repetitive tasks such as image segmentation, lesion detection, and volumetric measurements.

Companies in the MRI systems market are developing innovative MRI technologies with better imaging capabilities, faster scan times, and improved patient comfort. Siemens Healthineers invested heavily in developing novel 3T MRI systems like the Magnetom Lumina, which integrates AI and accelerates scan times.

Businesses are adopting AI to improve diagnostic accuracy, automate workflows, and decrease scan times. Philips Healthcare launched its AI-powered ‘SmartSpeed’ technology for faster MRI scans.

Manufacturers are developing patient centric solutions to address concerns regarding patient comfort and enhance satisfaction. Companies like Hitachi and GE Healthcare offer open-bore and wide-bore MRI systems to reduce patient anxiety.

Recent Industry Developments

|

Attributes |

Detail |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Strength

By Architecture

By End User

By Region

To know more about delivery timeline for this report Contact Sales

The market is anticipated to reach a value of US$ 10 Bn by 2032.

Open and close are the two main types.

North America is anticipated to emerge as the leading region with a share of 43.8% in 2025.

Prominent players in the market include GE HealthCare, Esaote SPA, and Siemens Medical Solutions USA, Inc.

The market is predicted to witness a CAGR of 5.8% throughout the forecast period.