- Sensors & Controls

- Motion Control Encoders Market

Motion Control Encoders Market Size, Share, and Growth Forecast, 2026 - 2033

Motion Control Encoders Market by Product Type (Incremental Encoders, Absolute Encoders, Hybrid Encoders), Output Type (Analog Output Encoders, Digital Output Encoders), Application (Industrial Automation, Robotics, Medical Technology, Consumer Electronics), and Regional Analysis for 2026 - 2033

Motion Control Encoders Market Share and Trends Analysis

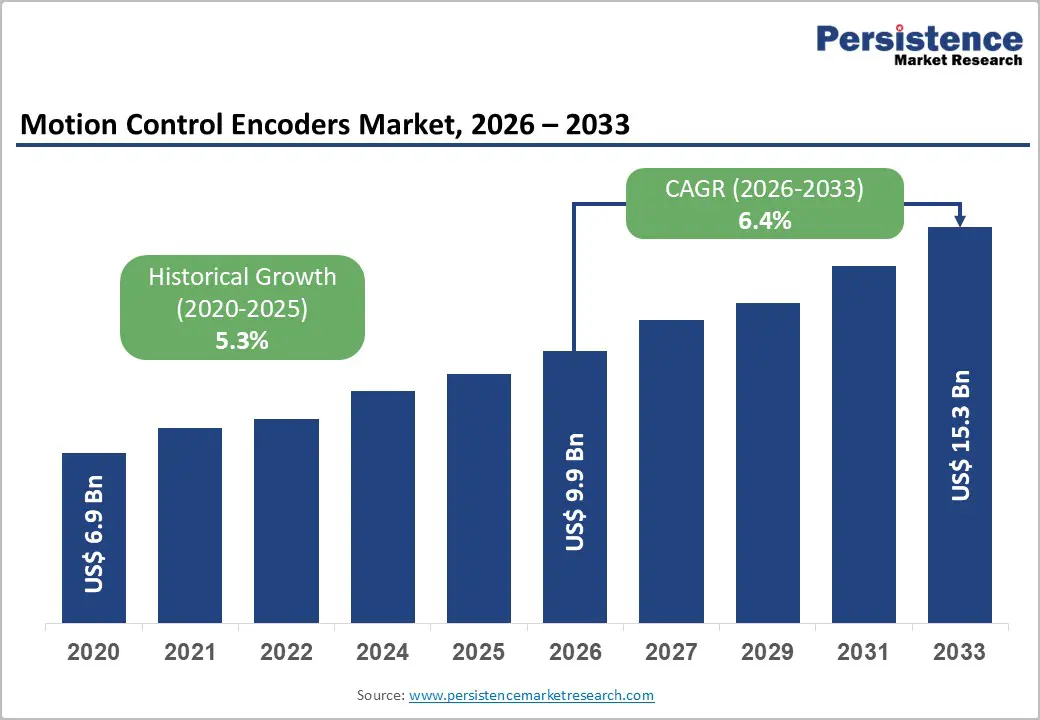

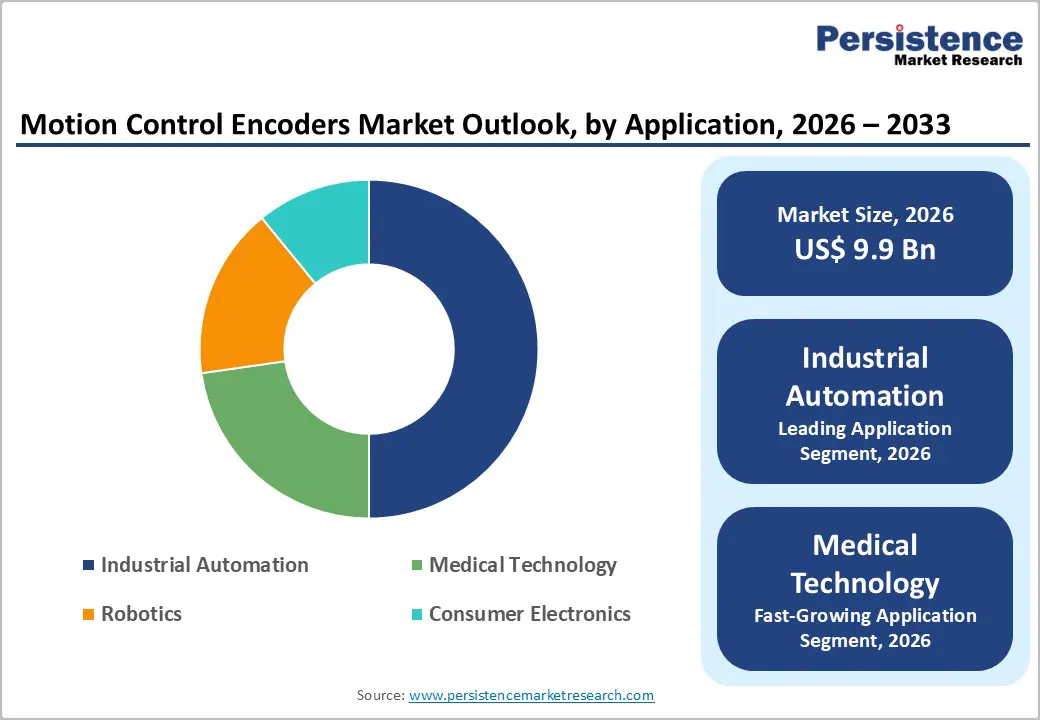

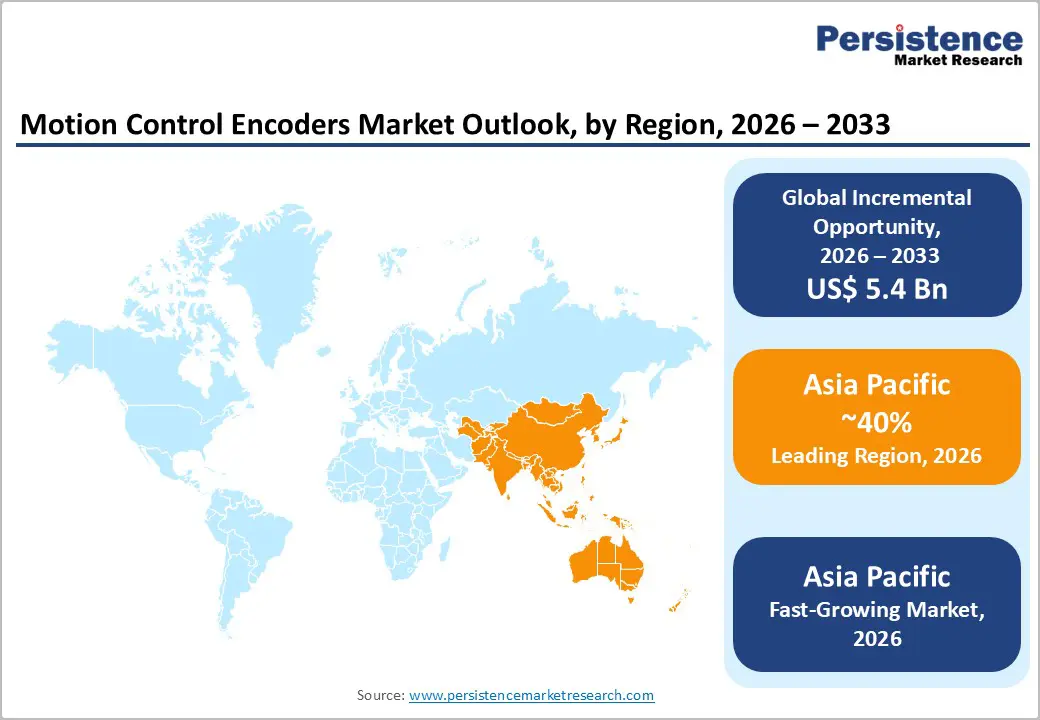

The global motion control encoders market size is likely to be valued at US$ 9.9 billion in 2026, and is projected to reach US$ 15.3 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026−2033. Growth is primarily driven by the increasing adoption of automated systems across industrial, robotics, and consumer electronics sectors. Rising demand for precision motion control in manufacturing and medical applications enhances equipment integration and process efficiency. The expansion of digital infrastructure and the industrial Internet of Things (IIoT) enables real-time monitoring and feedback loops, thereby promoting the use of advanced encoders.

Emerging economies are demonstrating rising industrial investments and the modernization of production lines, further stimulating market expansion. Technological innovation in encoder design, including miniaturization, higher resolution, and environmental robustness, improves adaptability across diverse applications. Increased focus on reducing operational costs and downtime compels manufacturers to incorporate accurate feedback mechanisms, reinforcing the adoption of motion control encoders.

Key Industry Highlights

- Dominant Region: By 2026, Asia Pacific is expected to lead the with over 40% market share, driven by industrial automation, robotics, and precision manufacturing.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by smart manufacturing and automation adoption.

- Leading Application: Industrial automation is projected to lead the market in 2026, on account of manufacturing and robotics integration.

- Fastest-growing Application: Medical technology is expected to be the fastest-growing segment between 2026 and 2033, propelled by surgical robotics, diagnostics, and laboratory automation.

| Key Insights | Details |

|---|---|

|

Motion Control Encoders Market Size (2026E) |

US$ 9.9 Bn |

|

Market Value Forecast (2033F) |

US$ 15.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancement in Industrial Automation

Advancements in industrial automation are a primary catalyst for market growth, as manufacturers seek greater precision, efficiency, and productivity in production processes through real-time control systems and automated feedback loops. Progressive automation technologies enable tighter synchronization of machines and mechanical systems, enhancing end-to-end process consistency and reducing variability in output quality. According to the U.S. Census Bureau, about 52% of manufacturing workers are in firms that use automation technologies to enhance production processes, highlighting the pervasive shift toward automated operations in manufacturing sectors. The expansion of robotics, sensors, and control systems in factories has increased demand for high-performance feedback components that deliver accurate positional data under dynamic operating conditions.

Government innovation programs and public policies aimed at strengthening advanced manufacturing capabilities encourage the adoption of cutting-edge automation tools, accelerating the integration of digital technologies into production environments. Federal initiatives and workforce training frameworks support modernization, incentivizing firms to invest in smart systems that link production hardware with data analytics and machine learning tools. These systems require precise motion feedback and control modules as foundational elements of digital workflows that optimize throughput and minimize downtime. As automation penetrates new segments such as precision assembly, high-Volume production and adaptive machining, demand technologies enabling reliable, high-resolution motion control feedback increases accordingly.

Rising Industrial Modernization in Emerging Economies

Industrial modernization in emerging economies drives the adoption of automation technologies, significantly strengthening production efficiency and output quality across manufacturing sectors. Rapid integration of advanced manufacturing systems, such as robotics, programmable logic controllers, and sensor networks, enables firms to reduce labor intensity, enhance throughput, and align with global quality benchmarks, supporting competitiveness on international trade platforms. Policy frameworks in several emerging countries tie incentive programs to technology adoption, lowering barriers for small and medium enterprises to upgrade equipment and embrace data-driven production management. Expanded digital infrastructure and workforce skill development initiatives further strengthen capabilities for scalable production modernization.

Investment in digital manufacturing and automation extends beyond simple cost reduction to strategic repositioning of industrial bases. Economies that integrate smart systems and real-time process control attract foreign investment and strengthen linkages with global supply chains. Digital transformation programs often include public funding for technology adoption, workforce training, and innovation incubation, supporting ecosystem development for high-precision manufacturing technologies. Industrial modernization also accelerates the adoption of productivity curves in legacy sectors such as automotive assembly, electronics fabrication, and capital equipment production, reshaping cost structures and enabling firms to meet stringent international compliance and delivery timelines.

High Cost of Advanced Encoder Systems

The high cost of advanced encoder systems restrains adoption, as precision designs demand specialized materials, micro-engineered components, and complex manufacturing processes, thereby elevating production expenses and final pricing. Optical and high-resolution devices require multi-stage fabrication and the integration of sophisticated electronics, resulting in unit costs significantly higher than those of standard alternatives. Investment barriers are particularly pronounced for small manufacturers with limited capital, where expensive feedback systems extend return-on-investment timelines and limit deployment in new or upgraded automation lines. Operations with tight budgets often prioritize lower-cost alternatives that provide adequate performance, constraining penetration of high-precision solutions in cost-sensitive applications.

Integration and operational expenses further amplify cost pressures, as retrofitting advanced encoders into existing production lines requires interface modules, calibration, and engineering support, thereby increasing total project expenditure. Continuous operation under demanding environmental conditions requires ruggedized designs and periodic maintenance, thereby increasing lifecycle costs. Procurement decisions factor in initial purchase price along with long-term integration and servicing requirements, influencing deployment timing and adoption scale. Firms frequently opt for phased or incremental upgrades to align with capital constraints, balancing precision needs against budget limitations.

Integration Complexity and Compatibility Challenges

Integration complexity and compatibility limitations constrain growth as modern industrial systems must integrate advanced encoder technologies with existing control architectures, requiring extensive customization, middleware development, and specialized engineering resources to align disparate communication protocols, software interfaces, and hardware standards across production equipment. Retrofitting legacy programmable logic controllers (PLCs), distributed control systems, and older automation hardware often requires significant reengineering of signal pathways and network layers, resulting in extended commissioning timelines and higher implementation costs that deter rapid deployment among manufacturers with limited technical capacity.

The root cause of these challenges lies in the fragmentation of automation standards and the diversity of legacy equipment that predates contemporary digital communication frameworks, limiting the smooth integration of advanced feedback devices into existing operational technology stacks. Many facilities operate machinery designed decades earlier without native support for modern industrial Ethernet standards or real-time data exchange protocols, requiring additional abstraction layers to bridge old and new technologies and increasing system complexity. Compatibility hurdles also extend to software ecosystems where motion control algorithms must interpret encoder feedback through disparate middleware environments, often necessitating bespoke configuration and calibration.

Expansion into Medical Technology Applications

The healthcare sector is experiencing a rapid shift toward robotics-enabled interventions due to the demand for enhanced procedural precision, minimally invasive approaches, and improved patient outcomes. Real-time positional and motion feedback from encoders is critical for robotic arms, surgical manipulators, and diagnostic systems, enabling sub-millimeter accuracy and stable closed-loop control, essential for complex procedures such as radiosurgery and catheter guidance. Integration of encoders ensures reliable synchronization between instruments and imaging systems, enhancing procedural safety and efficiency. Advanced motion feedback supports adaptive control, allowing medical devices to respond precisely to patient-specific anatomical variations, improving clinical performance and reducing operational errors.

High-complexity medical applications require consistent and dependable motion control under stringent regulatory standards, driving adoption of encoder technologies capable of repeatable performance. Government-supported initiatives emphasize precision robotics across areas such as minimally invasive surgery, laboratory automation, and rehabilitation engineering, where automation improves workflow efficiency and patient recovery times. Encoder-enabled systems facilitate accurate positioning, responsive adjustments, and seamless integration with computer-assisted control algorithms, ensuring compliance with safety protocols.

Development of Smart Factories and Industry 4.0 Integration

Integration of smart systems enables real-time data exchange, advanced analytics, and connected production workflows that enhance operational transparency and process optimization, with around 30% of manufacturing small and medium enterprises adopting Industry-4.0 technologies by 2025 according to government-validated data. Industrial operations generate massive volumes of sensor and machine data, and digitized analysis of this information enables proactive equipment maintenance, minimizes unplanned downtime, and improves quality control and yield, which are essential for meeting stringent production standards and competitive delivery timelines.

Emerging policy frameworks that support smart manufacturing adoption and digital transformation expand access to interoperable technologies and catalyze the modernization of traditional production models. Government programs focused on building digital infrastructure, training professionals, and establishing demonstration centers for advanced manufacturing solutions lower barriers to technology deployment and encourage broader ecosystem participation. Implementation of connected platforms that link equipment, analytics, and management systems also enhances visibility into supply chain performance and enables decision-making based on near-real-time operational metrics, improving flexibility to adjust production in response to shifting market demand.

Category-wise Analysis

Product Type Insights

Absolute encoders are likely to lead with an estimated 45% of the motion control encoders market revenue share in 2026, due to their precise positional feedback and reliability in continuous motion applications. These devices maintain position information even during power loss, making them essential for industrial automation, robotics, and medical equipment. Their capability to provide multi-turn and single-turn positional data improves control accuracy, reduces errors, and ensures operational consistency. Integration with digital control systems enables seamless communication with PLCs and motion controllers, enhancing process automation. The growing need for high-precision, real-time feedback in manufacturing, robotics, and medical technology supports the adoption of absolute encoders.

Hybrid encoders are expected to experience the fastest growth between 2026 and 2033, as they combine optical and magnetic sensing technologies to deliver enhanced resolution and environmental robustness. These encoders deliver precise performance in industrial settings, even under vibration, dust, and temperature fluctuations. Compact design and high durability enable integration into mobile robotics, automated guided vehicles (AGVs), and medical devices. Increasing adoption is supported by technological innovations improving signal quality and output consistency. Hybrid encoders also provide cost-effective solutions relative to purely optical designs in challenging environments, allowing deployment in previously underserved industrial segments.

Application Insights

Industrial automation is poised to dominate, with nearly 55% revenue share in 2026, driven by the integration of motion control encoders across manufacturing, process control, and assembly operations. Automation systems require precise positional feedback for efficiency, quality, and safety compliance. Encoders enable accurate synchronization of conveyor systems, robotic arms, and computer numerical control (CNC) machinery, reducing operational errors and energy consumption. Rising investments in modernizing production lines, digital monitoring, and factory safety regulations further reinforce adoption. Industrial automation demands scalable, high-performance encoders capable of operating continuously under demanding conditions, supporting their dominant market position.

Medical technology is expected to emerge as the fastest-growing segment between 2026 and 2033, driven by automation in surgical robotics, diagnostic systems, and laboratory automation. Precision, repeatability, and reliability are critical for applications such as robotic-assisted surgery, automated imaging devices, and laboratory sample handling. Integration of encoders with compact medical devices and wearable diagnostic tools expands application potential. Technological developments supporting sterilization compatibility, miniaturization, and wireless data communication enhance adoption. Increasing hospital investments in digitalized equipment and rising patient throughput requirements accelerate encoder deployment.

Regional Insights

North America Motion Control Encoders Market Trends

North America maintains a substantial presence in the market for motion control encoders, owing to its established industrial infrastructure and advanced automation adoption across automotive, aerospace, and electronics manufacturing. High penetration of robotics and machine tools in production processes drives consistent demand for both incremental and absolute encoder technologies. Industrial equipment manufacturers prioritize the integration of encoders for precision control, reliability, and predictive maintenance capabilities, enabling enhanced operational efficiency. Adoption of advanced sensor technologies and high-resolution feedback systems reinforces industry stability, while mature supply chains and localized production facilities ensure rapid deployment across multiple verticals.

Strong investment in research and development supports innovation in encoder miniaturization, wireless communication compatibility, and integration with IoT-enabled platforms, enabling improved process monitoring and control. Demand is further influenced by stringent quality and regulatory standards that necessitate precise motion feedback systems for compliance in automotive and aerospace applications. High adoption of servomotors, CNC machines, and collaborative robotic systems contributes to sustained expansion. Strategic partnerships between system integrators and equipment manufacturers accelerate solution implementation, while service and maintenance contracts generate recurring revenue.

Europe Motion Control Encoders Market Trends

The motion control encoder sector in Europe is gaining strength, bolstered by a mature industrial base and established manufacturing clusters in the automotive, aerospace, and electronics sectors. Demand is driven by precision-engineering requirements, with high-accuracy absolute and optical encoders integrated into robotic assembly lines, CNC machinery, and automated material-handling systems. Growth is further reinforced by the modernization of legacy manufacturing infrastructure alongside the adoption of Industry 4.0 standards, resulting in the steady uptake of mid- to high-range encoder technologies. Advanced engineering capabilities and research and development initiatives enable deployment of customized solutions, particularly for high-reliability and safety-critical applications in transportation and heavy machinery production.

Expansion is primarily influenced by investments in smart factory initiatives and automation optimization programs. Facilities increasingly implement real-time feedback systems, predictive maintenance tools, and closed-loop control mechanisms that rely on precise encoders, creating consistent replacement and upgrade cycles. Collaborations between technology providers and system integrators accelerate the deployment of tailored motion control solutions, improving operational efficiency and reducing downtime. Focus on sustainability and energy efficiency also drives the adoption of low-power encoder variants, supporting incremental growth.

Asia Pacific Motion Control Encoders Market Trends

Asia Pacific is expected to lead with an estimated 40% share of the motion control encoder market in 2026, driven by concentrated demand across industrial automation, robotics deployment, and precision manufacturing sectors. This regional market captures a substantial portion of global market volumes, driven by high adoption rates in electronics assembly lines, automotive manufacturing, and semiconductor production facilities. Within this share, major economies contribute significantly, with leading contributors accounting for nearly half of regional demand, while others maintain material portions through advanced factory automation projects and precision machinery integration. Market segmentation reveals strong penetration in both incremental and absolute encoder technologies, reflecting rapid expansion alongside modernization of production processes.

Asia Pacific is also forecasted to be the fastest-growing market for motion control encoders between 2026 and 2033, stimulated by the strategic integration of encoders within smart manufacturing ecosystems that enhance process precision and operational efficiency. Investment in automation and digital transformation initiatives, coupled with incentive frameworks for advanced manufacturing adoption, accelerates technology uptake. The regional market demonstrates strong adoption rates for mid-tier magnetic encoders and high-precision optical encoders, addressing a wide range of industrial requirements. Local innovation in encoder design and cost-optimized production supports rapid scaling, while collaboration between manufacturers and system integrators enhances solution deployment speed.

Competitive Landscape

The global motion control encoders market exhibits a moderately consolidated structure, combining the presence of multinational corporations with specialized regional manufacturers. Key players such as Kübler Group, Hohner Automation, Baumer India, SICK AG, HEIDENHAIN, and Panasonic dominate the competitive landscape, leveraging advanced technology portfolios and high-precision encoder solutions. These firms focus on delivering both incremental and absolute encoder systems tailored for applications in industrial automation, robotics, electronics manufacturing, and automotive assembly. Competitive strategies revolve around innovation, reliability, and adherence to international safety and quality standards, which are essential for maintaining credibility in high-precision sectors.

Market positioning emphasizes collaboration with system integrators, original equipment manufacturers, and industrial automation solution providers to expand reach and strengthen after-sales support frameworks. Partnerships enable seamless integration of encoder technologies into complex automation workflows, enhancing process accuracy, monitoring capabilities, and predictive maintenance efficiency. Investments in research and development support development of miniaturized, high-resolution, and smart encoder variants compatible with IoT platforms, reinforcing differentiation in competitive bidding and project execution.

Key Industry Developments

- In December 2025, Geehy launched its dedicated G32R430 encoder microcontroller unit designed specifically for high-precision motion control and position feedback in industrial servo, automation, and robotics applications, offering enhanced real-time performance and accuracy for next-generation motion systems.

- In July 2025, Maxon introduced a breakthrough encoder-free brushless direct current (BLDC) motor control method that enhances precision and reduces design complexity by generating accurate motor feedback from Hall sensor data without requiring a dedicated encoder.

- In May 2025, FLUX GmbH partnered with SEUM Tronics to expand distribution of high-precision encoders and accelerate adoption of advanced motion control feedback technologies in the South Korean industrial market.

Companies Covered in Motion Control Encoders Market

- Kübler Group

- Hohner Automation S.L.

- Baumer India Pvt. Ltd.

- SICK AG

- HEIDENHAIN

- Panasonic Industry Co., Ltd.

- AMETEK, Inc.

- Renishaw plc.

- US Digital.

- Broadcom.

Frequently Asked Questions

The global motion control encoders market is projected to reach US$ 9.9 billion in 2026.

Rising adoption of industrial automation, robotics, and precision manufacturing is driving the market.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Integration of smart manufacturing, IIoT platforms, and high-precision automation systems presents key market opportunities.

Some of the key market players include Kübler Group, Hohner Automation S.L., Baumer India Pvt. Ltd., SICK AG, HEIDENHAIN, and Panasonic Industry Co., Ltd.