Industry: Healthcare

Published Date: November-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 169

Report ID: PMRREP34917

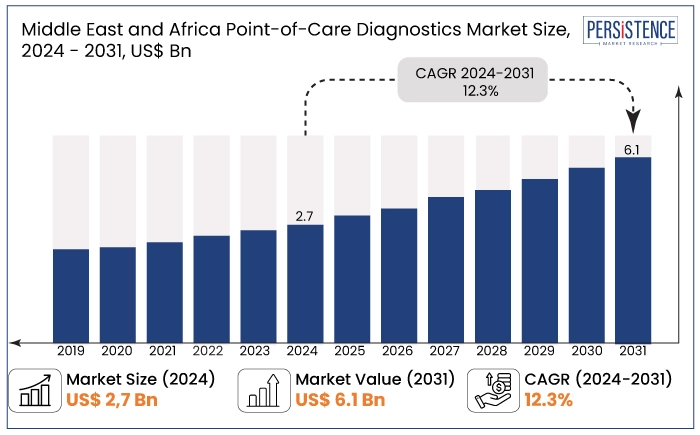

The Middle East and Africa point-of-care diagnostics market is estimated to reach a value of US$ 6.1 Bn in 2031 from US$ 2.7 Bn recorded in 2024. It is anticipated to capture a CAGR of 12.3% during the forecast period from 2024 to 2031. Market growth is mainly attributed to the rising prevalence of respiratory conditions, cardiovascular diseases, and diabetes in the region.

As per the International Diabetes Federation, in the United Arab Emirates, around 12.3% of people had diabetes in 2021. One of the highest rates of type 2 diabetes (T2D) worldwide is seen in the country. The country’s T2D prevalence is predicted to rise to 21.4% by 2030.

The country had around 64% individuals living with undiagnosed diabetes in 2021. To prevent this high prevalence, government agencies are focusing on investing in superior digital pathology systems, thereby creating new opportunities.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Middle East and Africa Point-of-Care Diagnostics Market Size (2024E) |

US$ 2.7 Bn |

|

Projected Market Value (2031F) |

US$ 6.1 Bn |

|

Middle East and Africa Market Growth Rate (CAGR 2024 to 2031) |

12.3% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

11.7% |

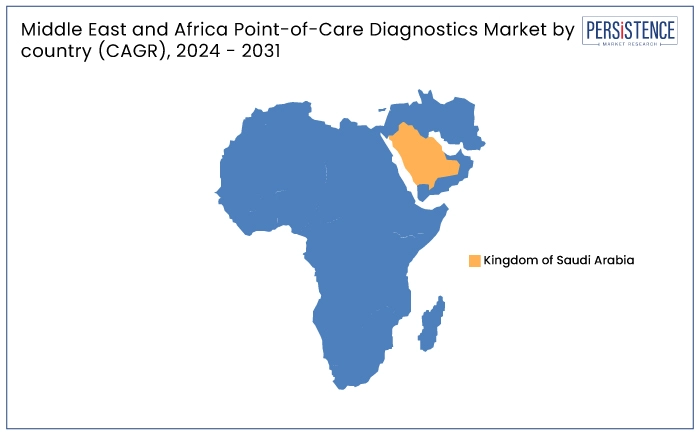

In the Middle East and Africa point-of-care diagnostics market, the Kingdom of Saudi Arabia commands a significant share, accounting for around 30% in 2024. This dominance is set to be driven by the country's robust healthcare infrastructure. Increasing government investments and growing demand for rapid diagnostic solutions are also set to fuel sales.

As Saudi Arabia prioritizes health modernization initiatives, its market for point-of-care diagnostics continues to rise. This factor is anticipated to position it as a key player in the region's medical technology landscape. Additionally, innovations in disease detection is likely to bolster demand in the next ten years.

|

Category |

Market Share in 2024 |

|

Product- Infectious Disease Testing |

30.9% |

By product, the infectious disease testing products segment is projected to lead by holding a market share of 30.9% in 2024. This is attributed to the rising incidence of infectious diseases and increasing demand for rapid, accurate diagnostics.

Innovations in molecular testing technologies and point-of-care solutions further fuel the segment's growth. With a surging focus on infectious disease management, this segment continues to lead the market.

|

Category |

Market Share in 2024 |

|

Prescription Mode- Prescription-based |

65% |

Based on prescription mode, the prescription-based testing segment is set to lead the market with a share of 65% in 2024. This is attributed to the increasing reliance on healthcare professionals for accurate diagnoses and treatment regimens.

Prescription-based products ensure proper usage, minimize misuse, and align with regulatory standards, making them the preferred choice for patients and healthcare providers. As healthcare systems evolve, prescription modes remain key in driving the market’s growth.

The Middle East and Africa point-of-care diagnostics market has significantly evolved in recent years. It is experiencing robust growth, driven by increased demand for rapid, efficient, and affordable diagnostic solutions.

Rising prevalence of chronic diseases, government investments in healthcare infrastructure, and innovations in mobile health technologies contribute to market growth. Historically, the market faced challenges such as limited access to centralized diagnostic laboratories and high healthcare costs, hindering widespread adoption.

The regional market is anticipated to broaden substantially through 2031. Technological innovations in point-of-care devices, such as portable diagnostics and mobile apps, will likely help improve healthcare accessibility and affordability.

The Middle East and Africa point-of-care diagnostics market showcased a CAGR of 11.7% in the historical period from 2019 to 2023. It experienced steady growth, driven by increased demand for rapid, efficient, and affordable diagnostic solutions.

Rising prevalence of chronic diseases, government investments in healthcare infrastructure, and innovations in mobile health technologies also contributed to this growth. Historically, the market faced a few challenges, such as limited access to centralized diagnostic laboratories and high healthcare costs, which hampered widespread adoption.

The market is anticipated to rise substantially with a CAGR of 12.3% through 2031. As governments prioritize healthcare modernization, innovations, rising healthcare awareness, and increasing healthcare expenditures will likely fuel the market growth.

Future trends are set to focus on enhancing diagnostic accuracy and efficiency. At the same time, the integration of Artificial Intelligence (AI) for generating quick results is set to bode well for the market.

Rising Prevalence of Infectious and Chronic Diseases to Fuel Demand

Growing prevalence of infectious and chronic diseases is a significant driver of the Middle East and Africa point of care diagnostic devices industry. As the region faces increasing incidences of conditions such as diabetes, cardiovascular diseases, and infectious diseases like COVID-19, tuberculosis, and HIV, there is a rising need for rapid and accurate diagnostic solutions.

Point-of-care (POC) diagnostics offer immediate results, enabling healthcare providers to diagnose and treat these conditions more effectively and efficiently. It is especially evident in areas with limited access to centralized labs.

Chronic diseases, particularly diabetes and hypertension, are on the rise due to lifestyle changes, surging aging population, and urbanization. Similarly, infectious disease outbreaks demand swift responses, which POC diagnostics can deliver.

Governments and healthcare providers prioritize diagnostic technologies that offer quick results and help manage disease spread with healthcare systems under pressure. Rising demand for timely diagnostics is set to continue driving growth, positioning POC solutions as essential tools in disease management.

Need for Rapid and Accurate Diagnostics to Boost Demand

Demand for rapid and accurate diagnostics is a significant driver of growth in the Middle East and Africa point of care molecular diagnostics industry. As healthcare systems strive to enhance patient outcomes, the need for quick, reliable diagnostic solutions has never been more significant. Point-of-care (POC) diagnostics provide immediate test results, enabling healthcare providers to make timely decisions. It is particularly crucial in managing infectious diseases, chronic conditions, and emergencies.

The urgency for fast diagnostics is further amplified in regions with limited access to centralized laboratories, where delays in test results can negatively impact patient care. Moreover, with the rise of healthcare awareness, patients are increasingly seeking quicker and more accessible diagnostic options.

Accurate results are vital for effective treatment, minimizing the risk of misdiagnosis and improving the quality of care. As healthcare systems prioritize efficiency, demand for rapid and accurate diagnostic technologies will continue to propel the market.

Low Healthcare Spending in a Few Countries to Hamper Demand

Regions like the United Arab Emirates and Saudi Arabia are investing huge sums in healthcare modernization. Various countries in Africa and a few parts of the Middle East, on the other hand, struggle with limited healthcare budgets. This will likely impact the adoption of advanced point-of-care (POC) diagnostic technologies. The lack of sufficient funding for healthcare infrastructure, medical devices, and diagnostic tools is anticipated to restrict the widespread implementation of POC solutions.

In countries with financial constraints, the high upfront cost of POC diagnostic devices and ongoing maintenance expenses may deter healthcare providers from investing in these technologies. Moreover, these countries may prioritize essential healthcare services over unique diagnostic systems, limiting market growth.

The lack of reimbursement policies or financial support for diagnostic products can discourage adoption. As a result, low healthcare spending in a few regions limits the market’s potential, slowing down the widespread adoption of POC diagnostics.

Investments in Molecular Point of care Testing for Remote Areas to Create Avenues

Several remote areas need easy access to centralized healthcare facilities, often leading to delayed diagnoses and treatment. Point-of-care (POC) diagnostics offer a solution by providing quick, reliable test results at the point of care. It helps in eliminating the need for patients to travel long distances for lab-based testing.

Governments and private organizations are increasingly focusing on improving healthcare access in underserved areas. POC diagnostic technologies are becoming essential in overcoming geographical and infrastructural barriers.

Rapid expansion is significant for managing infectious diseases, chronic conditions, and emergency health situations where timely diagnosis can significantly impact outcomes. With the rise of mobile health solutions and portable devices, healthcare delivery in rural areas is becoming highly efficient. Growing investments in healthcare infrastructure for remote regions are set to present a promising opportunity for the market to rise and enhance healthcare access.

Key Companies Invest in Telemedicine and Mobile Health to Extend Presence

Expansion of telemedicine and mobile health presents a significant opportunity for the Middle East and Africa POC diagnostic devices industry. As digital health solutions continue gaining traction, telemedicine platforms and mobile health applications are being integrated into POC diagnostics to improve healthcare access and delivery.

In countries with limited healthcare infrastructure, telemedicine enables patients to remotely consult healthcare providers. POC diagnostics offer immediate testing results, facilitating timely and accurate treatment. Also, the rapid convergence of telemedicine and mobile health with POC diagnostics can enhance patient outcomes by enabling continuous monitoring, early detection of diseases, and quick decision-making.

Growing penetration of smartphones and internet connectivity across the region makes these digital health solutions more accessible. These are particularly gaining momentum in remote and rural areas. As governments and healthcare providers invest in telemedicine networks and mobile health services, integrating POC diagnostics will be a key driver in improving healthcare access. It is set to further help in reducing costs and surging the market.

The Point-of-Care (POC) diagnostics industry in the Middle East and Africa is highly competitive. Leading companies are concentrating on joint ventures and new product development to increase their market share.

Key firms with cutting-edge point of care testing product offerings include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Danaher Corporation. Small-scale regional companies and local distributors also contribute to improving accessibility and meeting rising demands.

Cost-effectiveness, ease of use, and compatibility with mobile health platforms are critical components of competitive strategies. These help small-scale businesses to reach a position where they can take advantage of expansion prospects as the region's healthcare needs increase.

Recent Industry Developments in Middle East and Africa Point-of-Care Diagnostics Market

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Countries Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Product

By Prescription Mode

By Type

By End User

By Country

To know more about delivery timeline for this report Contact Sales

It is estimated to surge from US$ 2.7 Bn in 2024 to US$ 6.1 Bn by 2031.

F. Hoffmann-La Roche Ltd, Abbott, and Danaher Corporation are few of the leading players.

It includes electrolytes analysis, blood glucose testing, urine strips testing, food pathogens screening, and others.

It involves conducting diagnostic tests outside the laboratory.

It refers to pathology testing performed by a healthcare worker in close proximity to a patient.