- Rail

- Metro Rail Infrastructure Market

Metro Rail Infrastructure Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Metro Rail Infrastructures Market by Structure Type (Elevated, Underground, At-grade Level), Infrastructure Component (Station Building, Rolling Stock, Alignment & Trackwork, Electric Power System, Signaling & Telecommunication, Others), and Regional Analysis from 2026 to 2033

Metro Rail Infrastructure Market Share and Trends Analysis

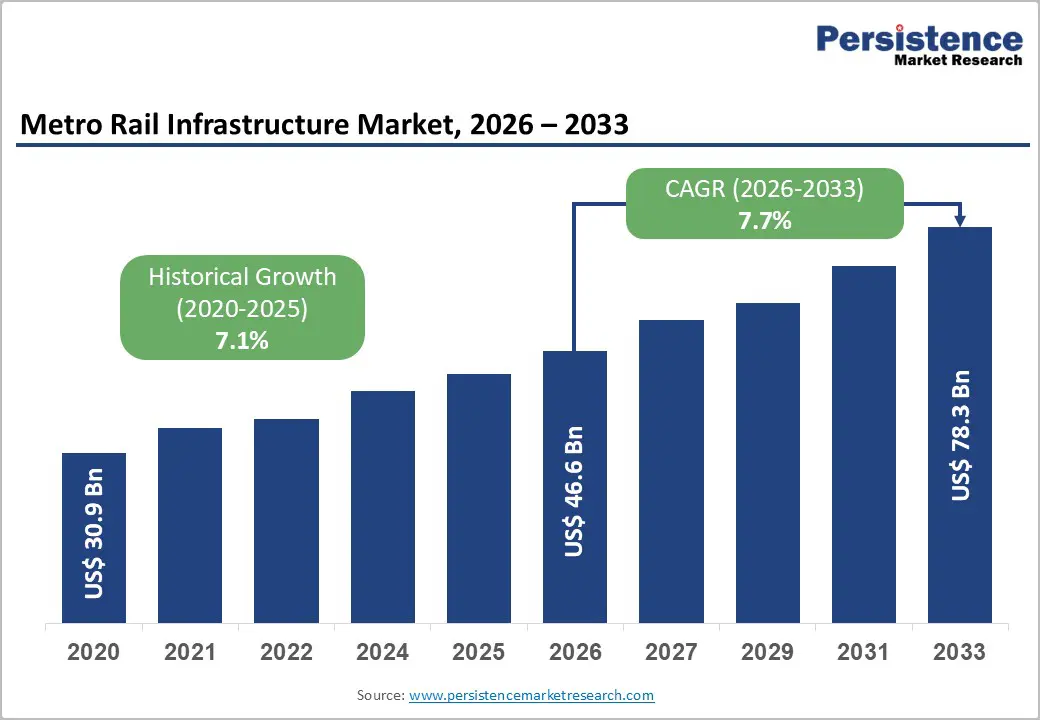

The global metro rail infrastructure market size is anticipated at US$ 46.6 billion in 2026 and is projected to reach US$ 78.3 billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033.

Accelerating global urbanization, government-led mass transit investment programs, and the imperative to decarbonize urban mobility are primary growth enablers. Asia Pacific's infrastructure expansion, Europe's rail modernization mandates, and North America's transit renewal programs collectively sustain demand. Rising urban congestion and national climate commitments are reinforcing long-term policy alignment with metro rail expansion across both developed and emerging economies.

Key Industry Highlights:

- The metro rail infrastructure market expanded from US$ 30.87 Bn in 2020, delivering a steady ~7.1% historical CAGR, underpinned by sustained government investment in urban mobility and mass transit decarbonization programs.

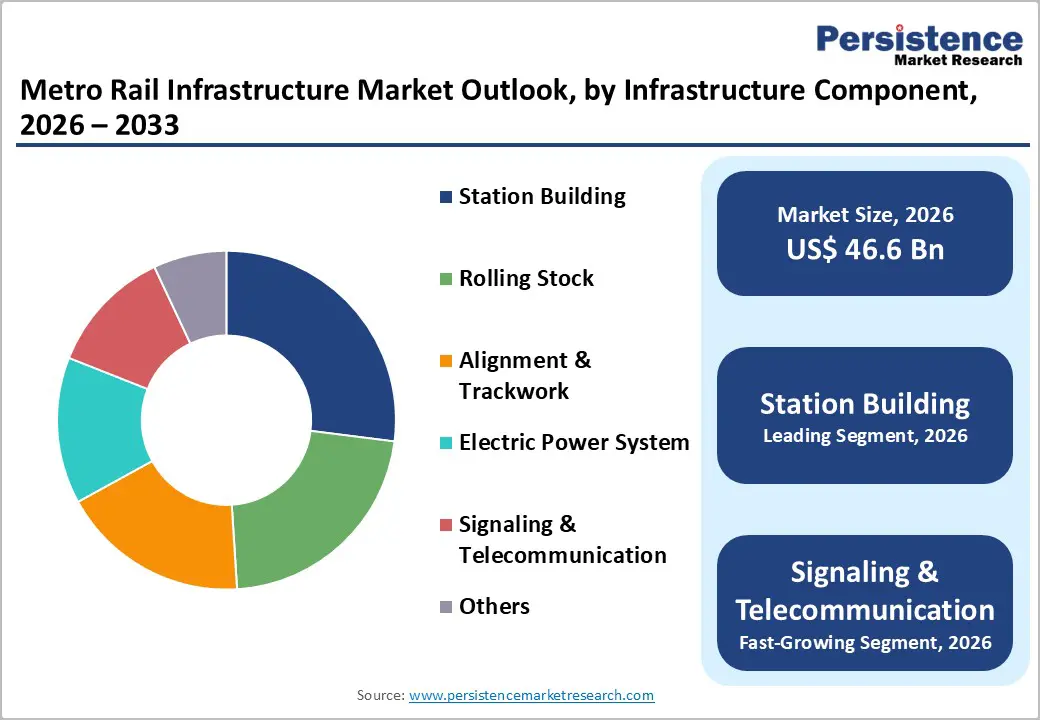

- Elevated corridors dominate with a 46% revenue share, driven by faster execution and lower capex, while Underground systems are the fastest-growing structure (8.7% CAGR) as megacities push for congestion-free urban cores. Station Buildings lead components at 27% share, supported by TOD and multimodal hub investments.

- Signaling & Telecommunication is the fastest-growing component at 9.1% CAGR through 2033, powered by CBTC deployments, cybersecurity regulations, and AI-enabled predictive maintenance platforms.

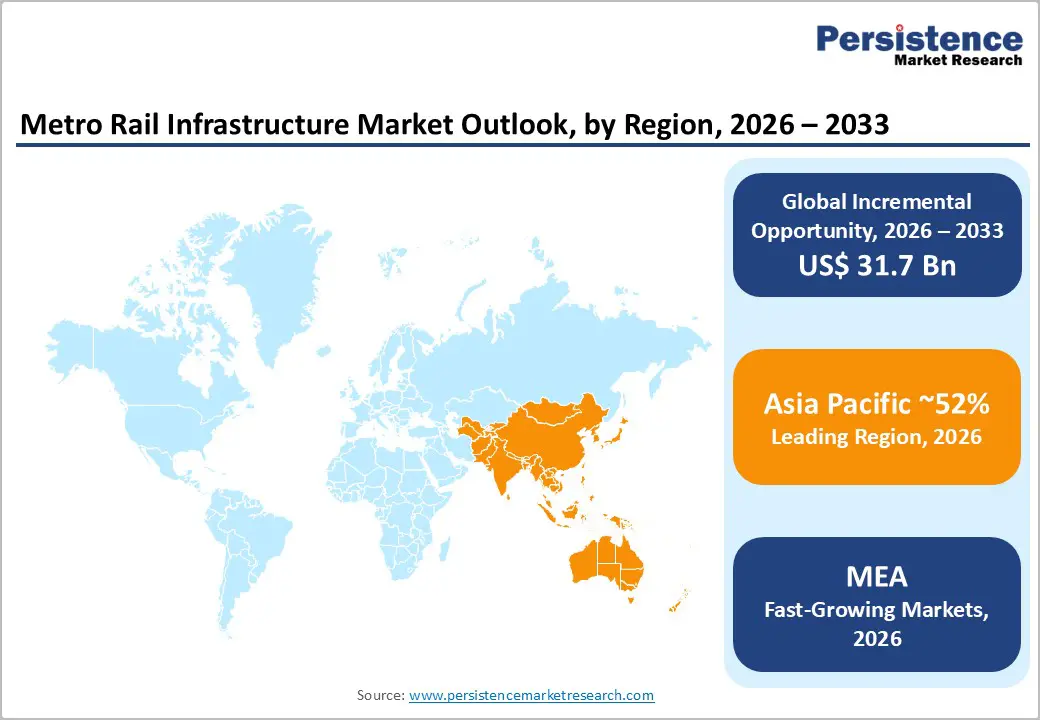

- With ~52% global share, Asia Pacific remains the growth epicenter, fueled by China’s megacity metro programs and India’s multi-city corridor expansions. Europe follows with a solid 7.2% CAGR, led by network modernization and green transport mandates.

- The US$ 39 billion IIJA transit allocation represents the largest federal metro investment in U.S. history, accelerating digital signaling upgrades, rolling stock renewal, and station modernization across major metropolitan areas.

- Post-2023 deal flow is dominated by integrated systems contracts, CBTC technology alliances, and CRRC-led Southeast Asian projects exceeding US$ 1.2 billion, signaling a shift toward full-lifecycle, technology-led metro infrastructure models.

| Key Insights | Details |

|---|---|

| Metro Rail Infrastructures Market Size (2026E) | US$ 46.6 Billion |

| Market Value Forecast (2033F) | US$ 78.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.7% |

| Historical Market Growth (2020 - 2025) | 7.1% |

Market Dynamics Analysis

Drivers - Accelerating Urbanization and Rising Urban Transit Demand

The United Nations projects that 68% of the global population will live in urban areas by 2050, adding 2.5 billion city dwellers, predominantly across Asia and Africa. Urban congestion costs the global economy an estimated US$ 1 trillion annually in lost productivity, according to INRIX Global Traffic Scorecard data. Metro rail systems directly address this structural demand by moving 40,000-70,000 passengers per hour per direction, far exceeding bus or road-based solutions. Government-backed National Urban Transport Policies in India, China's 14th Five-Year Plan, and the EU's Sustainable and Smart Mobility Strategy are channeling hundreds of billions into metro expansion, creating durable, policy-protected demand for metro rail infrastructure across both greenfield and network-extension projects.

Government Capital Expenditure and Public Transit Investment Programs

Global public investment in urban rail infrastructure exceeded US$ 175 billion in 2023, with the International Association of Public Transport (UITP) recording over 220 active metro construction projects worldwide. China's National Development and Reform Commission approved over 40 new metro line extensions in 2023 alone. India's Ministry of Housing and Urban Affairs is funding metro rail projects across 27 cities under Phase III of the National Metro Rail Policy. In the U.S., the Infrastructure Investment and Jobs Act allocated US$ 39 billion for public transit over five years. This sustained public capital commitment across key geographies provides infrastructure developers, rolling stock manufacturers, and systems integrators with a visible, multi-year project pipeline.

Restraints - High Capital Expenditure and Extended Project Gestation Periods

Metro rail infrastructure projects are among the most capital-intensive public investments globally, with underground metro construction costs averaging US$ 100-500 million per kilometer depending on geology, urban density, and technology specifications. Extended project timelines, typically 8-15 years from planning to commissioning, create fiscal exposure to cost overruns, which historically average 45% above initial estimates per Oxford University research. Sovereign credit constraints in developing nations and competing fiscal priorities limit project financing availability, particularly for countries with debt-to-GDP ratios exceeding recommended thresholds, slowing pipeline conversion to active construction.

Land Acquisition Challenges and Regulatory Approval Complexity

Urban metro projects routinely face protracted land acquisition disputes, particularly in densely populated Asian and African cities where resettlement and compensation processes require extensive multi-stakeholder negotiation. Environmental impact assessments, heritage preservation reviews, and multi-jurisdictional regulatory approvals frequently extend pre-construction timelines by 2-5 additional years. In India, delayed land acquisition has deferred several Phase III metro projects by 18-36 months. Regulatory fragmentation across municipal, state, and national authorities creates compliance complexity that drives up transaction costs and delays financial close for infrastructure developers.

Opportunity - Metro Rail Expansion in Emerging Markets

Emerging markets across South Asia, Southeast Asia, the Middle East, and Africa present the most significant greenfield metro development opportunity through 2033. India's metro network is projected to expand from 900 km to over 1,700 km by 2030, driven by RRTS and Phase III metro programs. Southeast Asia, including Indonesia, Vietnam, and the Philippines, has over US$ 50 billion in metro projects in active planning or construction. Middle Eastern nations, including Saudi Arabia's NEOM and Riyadh Metro Phase 2 are committing multi-billion-dollar allocations. These markets offer long-duration EPC contracts, PPP structures, and multilateral financing through ADB and World Bank, creating substantial entry opportunities for global infrastructure players.

Public-Private Partnership Models and Blended Finance

Fiscal constraints in developing economies are accelerating the adoption of PPP and availability payment models for metro infrastructure delivery, with the World Bank's Private Participation in Infrastructure database recording a 37% increase in transport PPP transactions between 2020 and 2023. Blended finance mechanisms combining multilateral development bank (MDB) guarantees with private equity and green bonds are unlocking metro project financing in markets previously considered unbankable. Green metro bonds issued by transit authorities in Europe and Asia raised over US$ 12 billion in 2022 - 2023. This structural shift toward innovative financing models expands the investable universe and accelerates project development timelines for private sector participants.

Category-wise Analysis

Structure Type Insights

Elevated metro structure holds the leading share at 46% of the global Metro Rail Infrastructure Market in 2026, attributable to its substantially lower construction cost compared to underground alternatives, typically 60-75% less expensive per kilometer. Elevated structures are the preferred choice across rapidly expanding Asian and African metro networks where right-of-way availability exists and cost efficiency is prioritized. Their faster construction timelines, reduced geological risk, and compatibility with modular prefabrication methods make them the dominant structural format for metro expansion in China, India, and Southeast Asia, where the majority of active global metro projects are concentrated.

Underground metro is the fastest-growing structure type, expanding at a CAGR of 8.7% through 2033. Urban densification in developed city centers and land scarcity in high-density Asian metropolises Tokyo, Singapore, and Hong Kong, are driving progressive underground adoption, as surface and elevated options become operationally or politically infeasible.

Infrastructure Component Insights

Station Building is the leading infrastructure component segment, commanding 27% market share in 2026. Stations represent the single largest cost center in metro projects, integrating civil construction, architectural finishes, mechanical and electrical systems, accessibility infrastructure, and increasingly, transit-oriented development (TOD) components. The growing complexity and scale of metro stations driven by multi-modal interchange requirements, retail integration, and smart technology deployment are expanding the station construction value per project. Landmark metro station projects in cities including Riyadh, Doha, Mumbai, and London consistently exceed US$ 200-500 million per station, reinforcing the segment's revenue dominance.

Signaling & Telecommunication is the fastest growing infrastructure component at 9.1% CAGR through 2033, driven by mass adoption of CBTC and ETCS Level 2+ systems, cybersecurity investment mandates, and the expanding integration of AI-based predictive maintenance and passenger information platforms across new and legacy metro networks.

Regional Insights and Trends

North America Metro Rail Infrastructure Market Trends

North America holds approximately 14% of the global Metro Rail Infrastructure Market in 2026, with the United States representing the region's primary demand driver. The US$ 39 billion public transit allocation under the Infrastructure Investment and Jobs Act (IIJA) is the most significant federal transit investment in U.S. history, catalyzing metro system modernization across New York, Los Angeles, Washington D.C., and Chicago. Canada's Transit Fund allocates C$ 14.9 billion for urban transit expansion. The regulatory environment, governed by the Federal Transit Administration (FTA), emphasizes Buy America provisions, driving domestic supply chain investment and technology localization across rolling stock and systems segments.

Innovation leadership in fare technology, autonomous metro operations, and digital infrastructure management positions North America as a technology benchmark market. FTA-compliant procurement frameworks and strong capital markets support PPP-structured transit expansions in major urban corridors.

Europe Metro Rail Infrastructure Market Insights

Europe is likely to expand at a CAGR of 7.2% through 2033, underpinned by the European Green Deal's urban mobility agenda and the EU's Horizon Europe research funding for next-generation rail. Germany, the U.K., France, and Spain lead regional metro investment, with Germany's Deutschlandticket policy and Paris's Grand Paris Express Europe's largest metro project at €36 billion representing flagship programs. The EU's Connecting Europe Facility (CEF) provides co-financing for trans-European transport network upgrades. Regulatory harmonization under the EU Rail Package IV is streamlining cross-border interoperability standards, reducing procurement friction and enabling pan-European rolling stock and signaling deployments at scale.

Spain's infrastructure modernization under its PERTE Movilidad program and the U.K.'s Urban Integrated Transport Strategy are generating steady pipeline additions. European metros are global leaders in automated train operation (ATO) and energy-efficient station design, setting international benchmarks.

Asia Pacific Metro Rail Infrastructure Market Trends

Asia Pacific commands the dominant position with approximately 52% of the global Metro Rail Infrastructure Market in 2026, growing at a CAGR of 9.5% the highest among all regions. China alone accounts for over 60% of the world's metro construction activity, with CRRC and state-owned construction entities executing at an unprecedented scale. India's National Metro Rail Policy supports 27 active metro cities, with Phase III projects in Bengaluru, Pune, and Nagpur advancing rapidly. Japan's advanced signaling and driverless metro technologies establish operational benchmarks globally. ASEAN metros in Bangkok, Jakarta, and Hanoi are progressing through construction, supported by Japan International Cooperation Agency (JICA) and ADB financing.

Manufacturing cost advantages in China, India, and South Korea drive competitive procurement pricing for rolling stock and civil infrastructure. Government-mandated localization policies across India's metro programs are creating domestic component manufacturing ecosystems with long-term supply chain resilience.

Competitive Landscape

Leading metro rail infrastructure players are deploying integrated systems strategies combining civil construction, rolling stock, signaling, and digital services to capture full project value chains. Cost leadership via modular prefabrication and localization, technology differentiation through CBTC and AI-enabled operations, and geographic expansion into Asia Pacific and Middle East metros define dominant competitive positioning and emerging business model convergence.

Strategic Developments

- In November 2023, Hitachi Rail and Thales Group entered a strategic signaling technology alliance to jointly deliver integrated ETCS Level 2 and CBTC signaling solutions for metro network upgrades across the U.K., Italy, and India, covering an estimated 350 route-kilometers.

Companies Covered in Metro Rail Infrastructure Market

- Alstom SA

- Siemens Mobility GmbH

- Bombardier (now Alstom)

- CRRC Corporation Limited

- Hitachi Rail Ltd.

- Thales Group

- Ansaldo STS (Hitachi Rail STS)

- CAF (Construcciones y Auxiliar)

- Hyundai Rotem Company

- China Communications Construction

- Larsen & Toubro Limited

- Balfour Beatty plc

- Cubic Transportation Systems

- Kapsch TrafficCom AG

Frequently Asked Questions

The global Metro Rail Infrastructure Market is projected at US$ 46.6 Billion in 2026, expanding to US$ 78.3 Billion by 2033.

Global urbanization, government capital expenditure programs, and decarbonization mandates driving electrified urban transit investment are the primary market growth drivers.

The metro rail infrastructure market is projected to grow at a 7.7% CAGR between 2026 and 2033.

Smart metro digital integration, emerging market greenfield expansion across South and Southeast Asia, and blended PPP financing models represent the most actionable near-term growth opportunities.

Leading players include Alstom, Siemens Mobility, CRRC Corporation, Hitachi Rail, Thales Group, CAF, Larsen & Toubro, Balfour Beatty, and Hyundai Rotem, among others.